On the streets of Beijing’s Shunyi district, Meituan’s squat yellow delivery robots have been shuttling groceries and takeout since 2020. Looking like miniature vans, the vehicles roll slowly along the curb with two side doors that lift open to reveal packed orders. Sometimes they work hand-in-hand with human couriers, pulling up to a drop-off point where nea rby riders unlock the doors, grab the packages inside, and dash to the customer’s doorstep.

“People treat them as part of the normal traffic flow. It’s no longer a novelty,” says Lei Xing, founder of AutoXing, a popular Wechat channel covering the auto industry. Over the past two years, he has made multiple research trips to Shunyi’s autonomous driving demonstration zone.

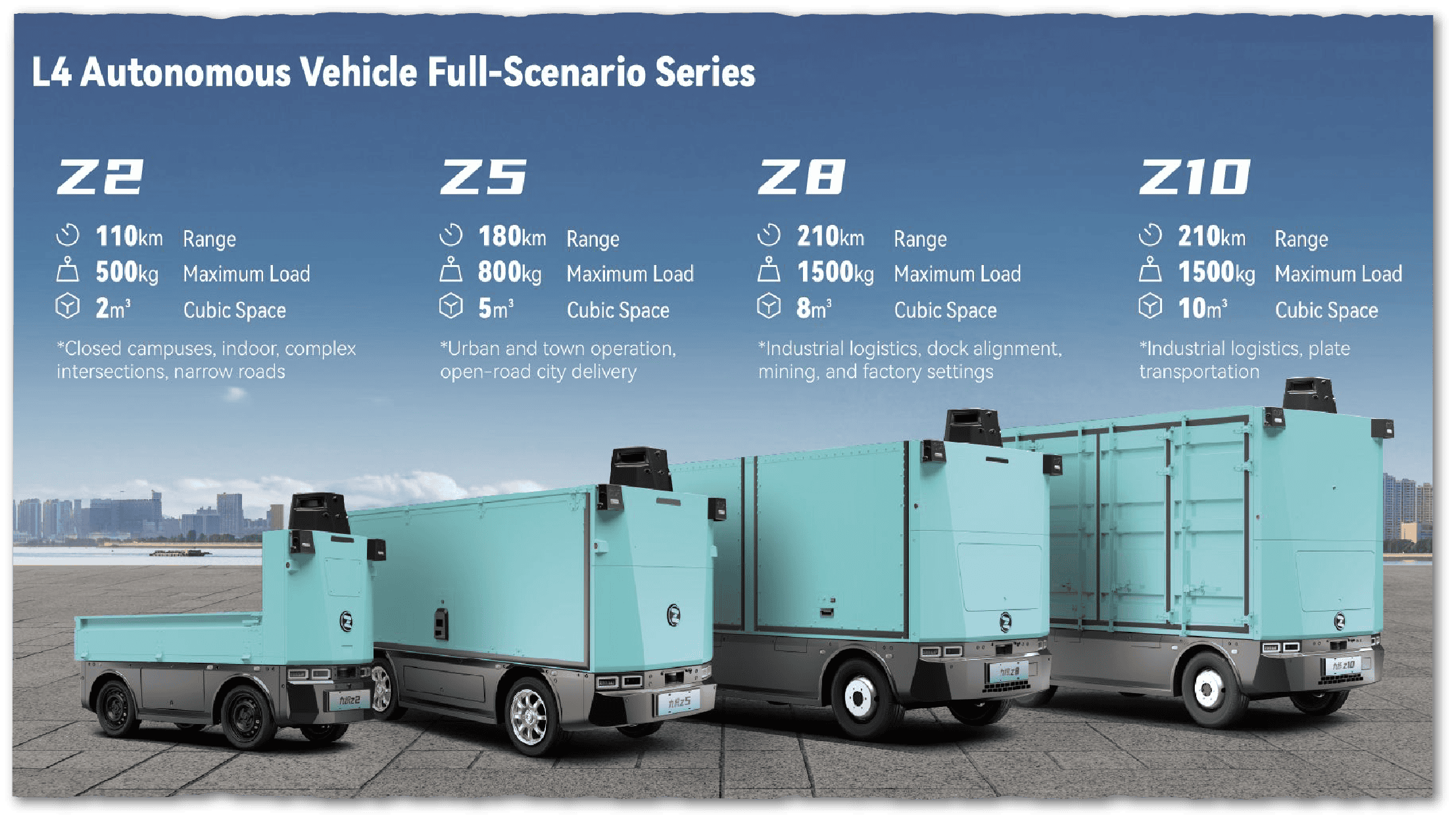

While China’s high-profile robotaxi industry races to deploy 1,000 cabs across 50 cities by the end of this year, the autonomous delivery vehicle (ADV) industry has quietly surged ahead. As of July, more than 15,000 ADVs — mid-sized electric vans with two to ten cubic meters of storage that can handle payloads of up to a ton — had been put on the road nationwide, with approvals to operate in over 200 cities.

The surge has been driven by start-ups. Last year Zelos Tech, the sector’s frontrunner, received more than 5,000 orders within a day of unveiling its new model. Another leading player, Beijing-based Neolix, founded in 2018, has received around 30,000 global orders for its ADVs, according to a media report.

As orders soar, prices are plummeting. Just a few years ago, an ADV cost more than 1 million yuan; today, they can sell for under 20,000 yuan. Together, the top three companies have raised over 10 billion yuan in funding.

Logistics giants are leading investors and major buyers. SF Express has deployed over 800 ADVs and expects its fleet to reach 8,000 by 2025. ZTO Express has expanded its robo-fleet from just over 350 ADVs in late 2024 to more than 2,000 today, while J&T Express plans to add 3,000 ADVs next year. In September, China Post announced it would lease 7,000 vehicles to serve its extensive network.

For investors, the appeal is clear. Moving goods is easier than moving people. Compared to robotaxis, ADVs run at lower speeds over repeatable routes — from warehouse to pick-up station or store — within fixed operating areas.

…the rise of autonomous delivery services in China is the natural next step, given China’s existing strengths in related industries such as sensors, Lidar systems, electric vehicles, batteries, chips — a lot of the basic parts that go into these delivery systems, as well as AI.

Kyle Chan, a postdoctoral researcher at Princeton University

They have ready buyers — parcel carriers, e-commerce platforms, retailers — that already budget for logistics. Handling goods rather than passengers lowers safety requirements, and can be done with less sophisticated vehicles.

“The result is a cleaner bridge from pilot to purchase order and cash cycles from the business operations perspective,” says Ivy Yang, a China tech analyst and founder of consulting firm Wavelet Strategy. “Robotaxis chase the ceiling, delivery AVs chase payback.”

RACING AHEAD

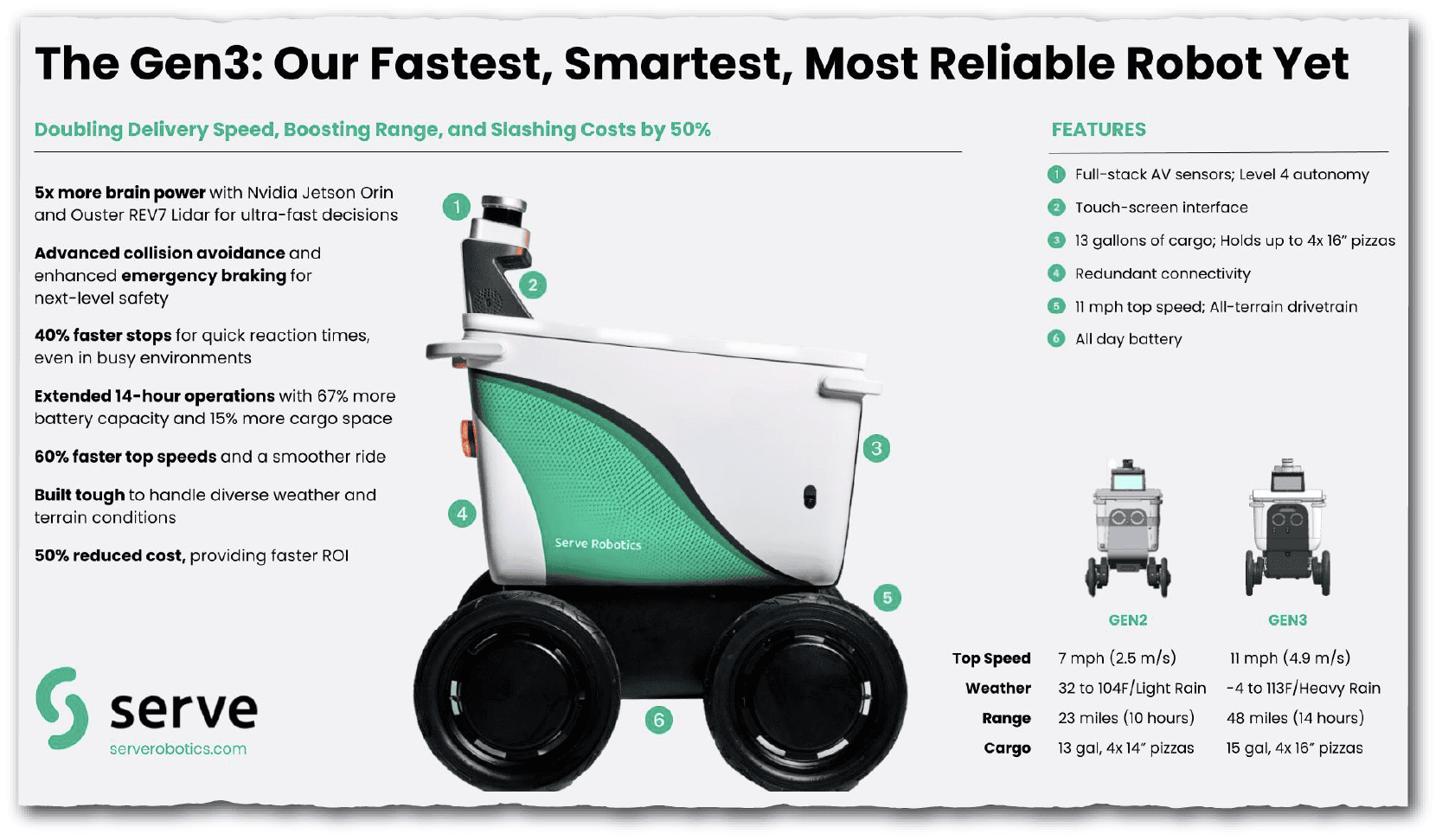

In the U.S., the ADV industry has not gained the kind of scale now emerging in China. Amazon and FedEx shut down their ADV projects in 2022. Even today new players such as Coco Robotics and Serve Robotics, both headquartered in Los Angeles, are still in the early stages of pilot projects with about one thousand bots on the road each.

DoorDash’s autonomous robot, Dot. Credit: DoorDash

In September, San Francisco-based DoorDash unveiled Dot, a four-wheeled autonomous delivery robot developed in-house after years of research. Before that DoorDash had been partnering with Coco Robotics for its sidewalk robot delivery operations in the U.S. However, Dots have yet to be deployed in even a pilot project and DoorDash is still in discussions about where to manufacture the robot and source its components.

Nuro was almost the exception. Founded in 2016 by two former engineers at Waymo, the California autonomous car company, Nuro pioneered low-speed delivery bots and struck a deal with China’s BYD to mass-produce thousands of vehicles. But after multiple rounds of layoffs in 2022 and 2023, Nuro decided to focus on core autonomous driving technology instead.

“The way American VCs value companies is problematic, and it ends up distorting how they operate,” says David Yufei Chang, CEO of Shenzhen-based autonomous delivery startup Whale Dynamic. “They’ll claim robotaxis can capture ten percent of a trillion-dollar autonomous driving market. But this isn’t like the airline industry, where a few players such as Boeing can dominate. The market is huge, but no single company can realistically secure such a large global share.”

The divergence reflects deeper cultural differences, according to some analysts. Kyle Chan, a postdoctoral researcher at Princeton University focusing on China and U.S. tech policy, says that in Silicon Valley, venture capitalists dream of world-changing technologies and moonshot bets that may not come good — robotaxis, for example.

“Whereas for China, a lot of policy makers at the central or local level are more interested in trying to find areas for incremental improvement and direct integration into the real economy and people’s daily lives,” says Chan.

“In many ways,” he adds, “the rise of autonomous delivery services in China is the natural next step, given China’s existing strengths in related industries such as sensors, Lidar systems, electric vehicles, batteries, chips — a lot of the basic parts that go into these delivery systems, as well as AI.” Lidar, which stands for Light Detection And Ranging, is often described as the “eyes” of autonomous vehicles; it uses lasers to create a real-time, 3D map of the vehicle’s surroundings.

FROM BIG TECH MUSCLE TO START-UP AGILITY

China’s autonomous delivery push began with its internet giants. Around 2015, JD.com, Meituan and Cainiao (Alibaba’s logistics arm) all established autonomous driving departments. Yet each struggled to turn early experiments into sustainable models for their own delivery businesses.

JD’s self-driving team was quickly marginalized, and its core engineers soon departed.

Around the same time, a group from Baidu’s Apollo autonomous driving project also departed. Among them was Zhuang Li, who had previously worked at JD and later teamed up with two former JD colleagues, Kong Qi and Zhu Weicheng, to establish Zelos, a Suzhou-based startup.

The Apollo project brought together China’s first generation of autonomous driving pioneers. Unlike Waymo or Tesla, which built their own proprietary systems, Baidu envisioned a shared technology backbone that could serve buses, trucks, taxis and delivery vans alike.

But Apollo proved too ambitious. “It’s extremely difficult to build a generic AI that can serve long-haul trucks, city buses, street sweepers and delivery vans all at once,” recalls Whale Dynamic’s Chang, a former Apollo engineer who eventually shifted his focus to the logistics sector. “Each vehicle type and scenario requires its own specialized tuning.”

Meituan also experimented early, rolling out pilot delivery vehicles. But its ADVs could not cope with the unpredictable routing and split-second turnarounds that food delivery demands.

As those pilots dragged on without any breakthroughs, the programs lost momentum. JD’s operations team turned to outside suppliers such as Beijing-based Rino.ai — an ADV startup founded in 2018 by a team that broke away from Baidu’s self-driving division — while its in-house tech group kept tinkering on the sidelines.

Cainiao took a different tack. It focused on deployments at easier-to-navigate “closed campuses”, such as universities and logistics hubs.

Then came COVID-19, which turned autonomous delivery from a novelty into a necessity. As the outbreak hit Wuhan in early 2020, JD rushed ADVs into quarantined neighborhoods while Rino.ai became the first ADV company to operate inside makeshift hospitals. Meanwhile, Meituan deployed ADVs to bring groceries and meals into sealed-off communities in Beijing. During Shanghai’s 2022 lockdown, more players such as Neolix followed, partnering with supermarkets.

“Startups have played an important role in giving the sector real momentum,” says Tian Ye, former head of strategy at a leading Chinese ADV company who is now with Robomart, a California-based ADV startup. “Free from the baggage of internet giants, they could pivot rapidly between use cases, running trial after trial to find where autonomous delivery made the most sense.”

Rino.ai initially focused on instant deliveries for supermarkets and restaurants. At that time, autonomous driving was still in its “Level 4” infancy. L4 systems are confined to tightly mapped routes and require human supervision for exceptions — a far cry from the “Level 5” dream of complete automation no matter the road or weather conditions. Fleets were modest in size and vehicles operated at lower speeds, says Leann Xu, Rino.ai’s overseas sales manager.

Levels of Vehicle Automation

| Level | Automation Label | Description |

|---|---|---|

| L0 | Momentary Driver Assistance | Driver is fully responsible for driving the vehicle while system provides momentary driving assistance, like warnings and alerts, or emergency safety interventions. |

| L1 | Driver Assistance | Driver is fully responsible for driving the vehicle while system provides continuous assistance with either acceleration/braking OR steering. |

| L2 | Additional Driver Assistance | Driver is fully responsible for driving the vehicle while system provides continuous assistance with both acceleration/braking AND steering. |

| L3 | Conditional Automation | System handles all aspects of driving while driver remains available to take over driving if system can no longer operate. |

| L4 | High Automation | When engaged, system is fully responsible for driving tasks within limited service areas. A human driver is not needed to operate the vehicle. |

| L5 | Full Automation | When engaged, system is fully responsible for driving tasks under all conditions and on all roadways. A human driver is not needed to operate the vehicle. |

Even so, the L4 requirements of early ADV users proved invaluable for developers. “Corporate clients demanded high reliability and efficiency,” says Xu. “They wanted 30-minute grocery deliveries, with a single robot making up to 18 trips a day from one store. That gave us a challenging but valuable environment to refine our L4 technology and products.”

“We tried everything,” Tian recalls. His team delivered bulky furniture, experimented with police patrol cars, partnered with gas companies to detect leaks, and helped pharmaceutical manufacturers deliver medicines to pharmacies and hospitals. Most of these pilots fizzled. “But because we were small,” Tian says, “we could drop an idea quickly and move to the next.”

That agility eventually led Rino.ai to a challenge it could meet: fixed warehouse-to-pickup station routes for e-commerce clients. As China’s supply chains matured and local governments expanded road access for driverless vehicles, the company shifted from small urban robots to larger vans capable of carrying heavier parcel loads.

“These courier routes are high-volume, high-frequency and route-stable — ideal conditions for autonomous vans,” says Xu. “Compared with the last-mile delivery cost of traditional courier logistics, Rino.ai’s autonomous vehicles can contribute to reducing costs by 30–50 percent.”

Rino.ai’s R5 model has been rolled out rapidly through its partnership with SF Express, whose highly standardized in-house network provided a platform that could be easily expanded.

But China’s courier industry is not uniform. Unlike giants such as SF Express or China Post, smaller companies including ZTO, YTO and J&T operate on a mixed model where most local outlets are largely subcontracted to small business owners. They, rather than their large corporate contractors, decide on how to automate their operations.

Startups have played an important role in giving the sector real momentum. Free from the baggage of internet giants, they could pivot rapidly between use cases, running trial after trial to find where autonomous delivery made the most sense.

Tian Ye, SVP at Robomart, an ADV startup based in California

Subcontractors’ willingness to invest in automated delivery technologies is another sign of the sector’s potential, Tian says. “When independent operators invest in autonomous vans, it isn’t just a corporate PR exercise, it’s a sign the economics truly work,” he argues.

An owner of a ZTO package pickup station in Hangzhou, who asked not to be named, told Wire China he recently ordered a Zelos ADV for less than 20,000 yuan. Previously, he rented a truck for about 3,000 yuan per month and paid a driver around 8,000 yuan per month. His ADV investment, he says, will pay for itself in two months.

As costs come down, companies that had suspended or abandoned ADV research are returning to it.

JD recently hired Cai Yiqi, a high-profile engineer prodigy from autonomous driving startup Deeproute.ai in Shenzhen. Cai earned his PhD in computer graphics from the University of Texas at just 25 and worked at Google on Street View 3D reconstruction and high-precision mapping. At Deeproute.ai, he was a core member of the team developing high-precision maps and pushing the frontiers of autonomous driving.

Cainiao, meanwhile, is beginning to deploy its own autonomous delivery vans and also selling them to other companies.

MANUFACTURING LEAP

The take-off of China’s ADV industry has also been propelled by a transformation of the supply chain. The cost of critical components has fallen dramatically. “Without cheaper, durable sensors and standardized chassis, even the best-chosen use cases wouldn’t balance the balance sheet,” says Tian.

When Lidar was first used for autonomous driving, it was essentially a fragile lab prototype — highly precise but expensive, with many failing to pass quality control checks. They were also prone to breakdowns because units mounted on vehicle roofs were vulnerable to extreme weather. But in the space of just a few years in China, it evolved into a reliable, mass-produced component.

Data captured by RoboSense’s RS-Ruby Laser Rangefinder Lidar unit. Credit: RoboSense

“Instead of a single large mechanical [Lidar] unit, we used multiple smaller modules, and to cut costs we reduced the number of lasers from more than a hundred to just a handful in each device,” says Yang Xiansheng, vice president of the Lidar division at RoboSense, a leading Lidar company.

The shift was further driven by the rapid adoption of advanced driver-assistance systems (ADAS) in passenger cars and the rise of the robotaxi sector, for which Lidar became the cars’ core “perception” sensor.

Since 2021, China’s ADAS market has exploded. What began with a few premium Lidar-equipped models from Xpeng and Huawei soon became standard across nearly all cars priced above 150,000 yuan ($21,060), says Yang Xiansheng. As production soared from tens of thousands to hundreds of thousands of units, costs plunged — from nearly 4,000 yuan per Lidar unit to lower than 1,000 yuan today.

Industry figures say the transformation was driven by advances in Chinese semiconductor chip technologies.

Engineers are now integrating Lidar lasers, receivers, and processors onto semiconductor chips, rather than bolting them together as separate components. The future perfection of this “chip-level” design will make Lidar smaller, higher in resolution, and cheaper to produce, says Yang Xiansheng.

In the past, most of these chips came from overseas giants such as Germany’s Osram and Sony. But now Chinese firms such as Hesai and RoboSense, both of which claim to be the country’s largest Lidar developer, can outsource the manufacturing of components to Chinese fabs that are able to handle mass production of them. RoboSense, which designs its own receivers, emitters and processing chips, says it now only outsources to Chinese fabs. Hesai also says its chips are self-designed.

Neolix’s autonomous vehicle factory. Credit: Neolix

Globally, RoboSense and Hesai’s closest comparable rival is Ouster in the U.S. But Ouster continues to focus on older mechanical Lidars and manufactures in the U.S., which Yang Xiansheng says makes its products more expensive.

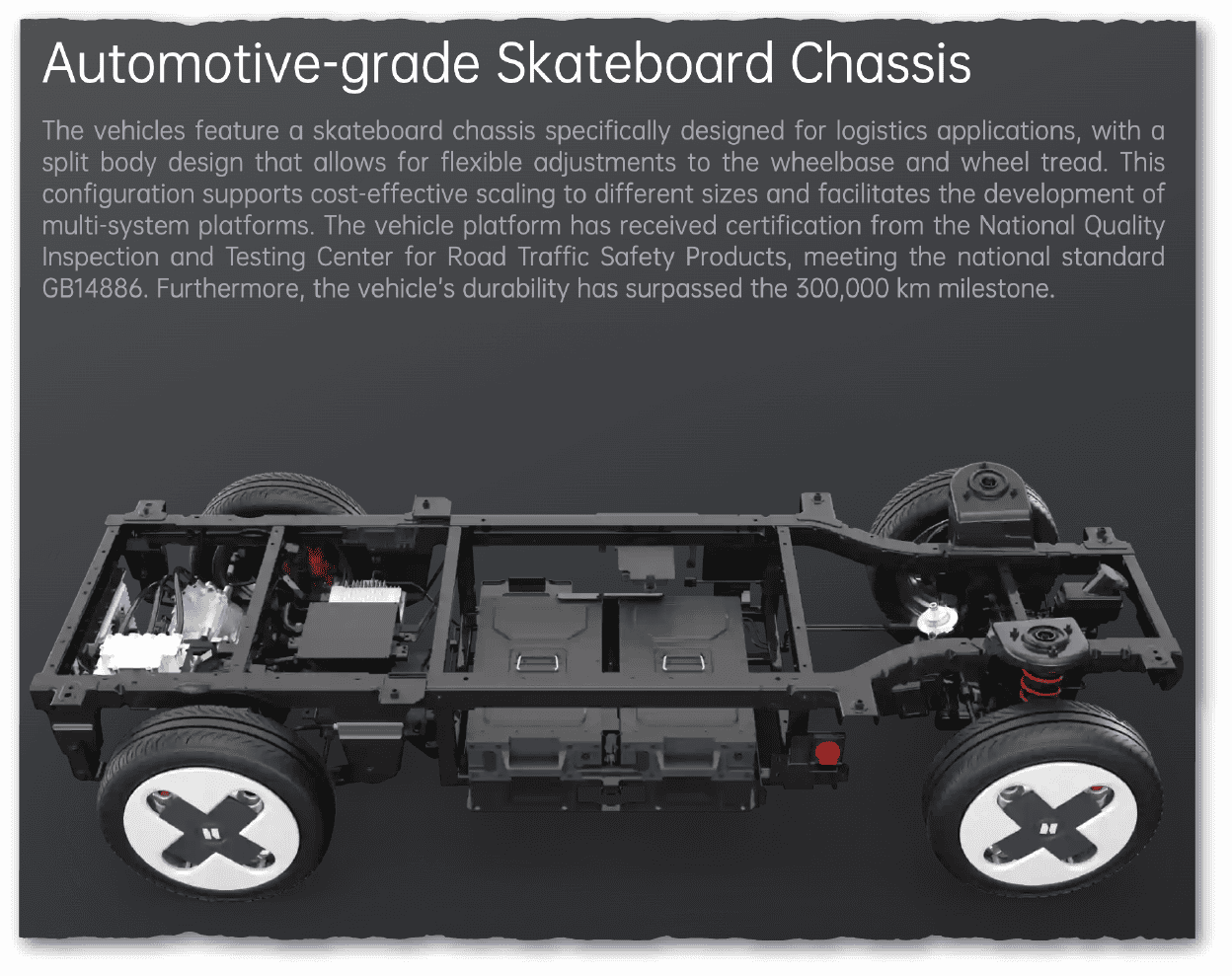

A similar transformation occurred in the chassis, the car’s underbody “skeleton” that connects the engine, wheels and steering.

Autonomous driving requires every digital signal — for acceleration, braking, steering — to translate seamlessly into physical motion.

Initially, only very few autonomous cars and delivery vehicles could “drive-by-wire” — and then only partially and at a high cost. Tian worked with automakers to build fully integrated platforms. “You don’t just digitize steering or acceleration,” he says. “You have to unify them into one system and sync it with the autonomous software. That polish across the supply chain takes years.”

The payoff has been dramatic. In 2021, the hardware of an ADV cost about $30,000. By 2023 it was closer to $20,000. Today, it’s under $10,000. “At that point, the math flips,” Tian says. “The vehicle becomes cheaper than paying a human courier.”

There are now dedicated chassis makers for ADVs in China, such as Ecar Tech. Its factory, in Nanjing, has an annual capacity of 10,000 units; it is building another plant to reach 100,000 units per year.

DIVERGING PATHS, CHINA VS THE U.S.

American companies face a much tougher challenge.

Ivy Yang, the analyst, notes that Chinese ADV makers are increasing production as rapidly as electric car companies did before them, lowering their per unit costs. And, again following the EV industry, they will likely export what they cannot sell at home. By contrast, she says, “U.S. players often outsource or stitch together partnerships, which raises cost per unit and lengthens iteration cycles.”

Serve Robotics, for instance, builds its ADVs with Magna International, the Canadian supplier that also manufactures for Waymo, while sourcing various components from around the world. Serve Robotics declined to disclose its per-unit manufacturing cost, but said it has recently managed to cut production expenses to one-third of their original level.

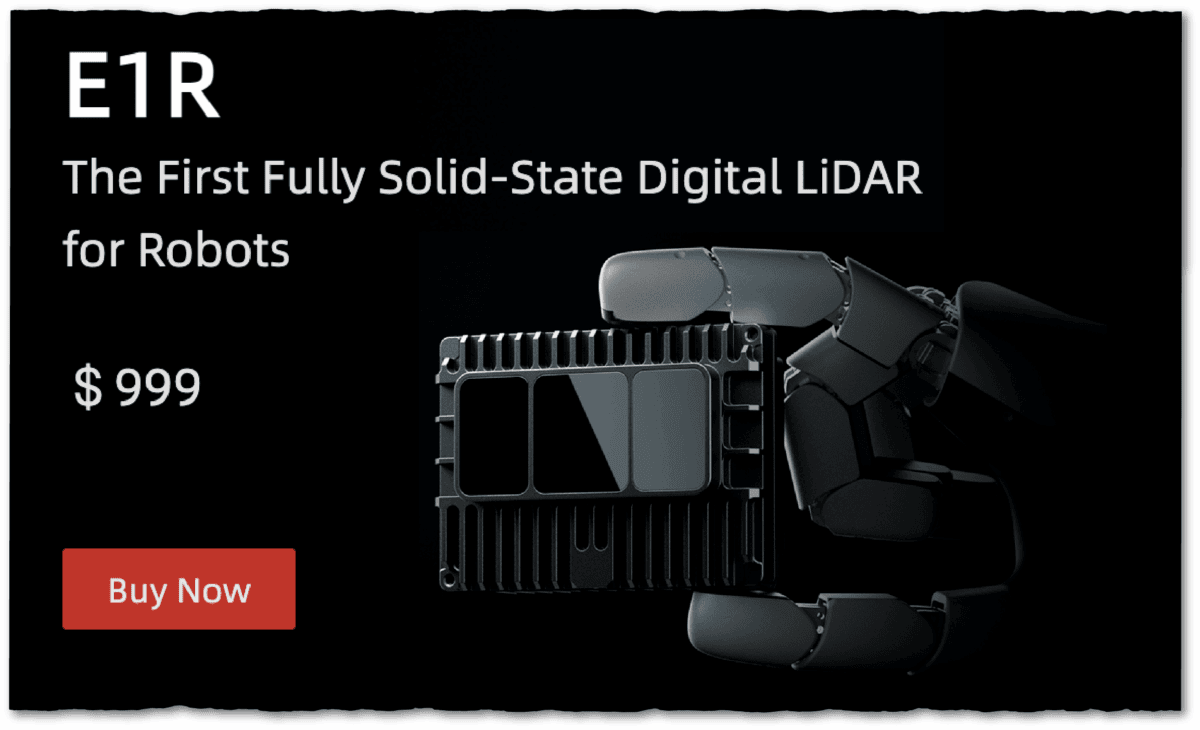

China’s supply chain advantages are so pronounced that many American startups source critical parts from China. Coco, for example, buys custom chassis from Segway Robotics in Beijing and Lidar from RoboSense in Shenzhen.

“Coco uses our E1R — the world’s first fully solid-state digital Lidar in mass production, and so far the only one at scale,” says Yang Xiansheng at RoboSense, referring to devices that have no moving parts. They are therefore smaller, cheaper and more durable than traditional mechanical Lidars that spin.

In China, logistics is so deeply embedded in everyday life that companies are already using ADVs to move large volumes of goods. Dense e-commerce flows, community pickup hubs and ubiquitous parcel lockers standardize delivery routines and generate huge amounts of logistics data, while also providing ready-made infrastructure for autonomous delivery systems, says Ivy Yang.

In another classic divergence with the U.S., the Chinese government has also moved rapidly to bolster the industry with supportive policies. Beijing districts such as Shunyi opened demonstration zones in 2020; official guidelines allowing low-speed delivery vehicles to operate on public roads with defined traffic rights followed in 2021 — propelling the sector beyond closed campuses.

Nationwide, more than 200 cities have opened test zones, enabling firms to amass vast data sets. Meituan, for example, had already been running its fleet in Shunyi and other locally approved “demonstration zones” for over a year and a half when the guidelines were issued, completing nearly 100,000 orders and logging more than 500,000 autonomous kilometers.

“The fundamental reasoning [in each country] is different,” adds Ivy Yang. “China is solving for throughput, while the U.S. is figuring out what to do with the liability issues.”

The story [ADV makers] sell is that they’re building volume fast to attract capital and go public, but the reality is the financing is showy, the profits aren’t there.

David Yufei Chang, CEO of Shenzhen-based autonomous driving startup Whale Dynamic

Whale Dynamic, the Shenzhen-based startup, focuses on export markets but still conducted all its early testing in China, because it was faster and cheaper. “You test things much more quickly at low cost in China,” says Chang, the company’s CEO, adding that the whole process costs one-tenth of what it does in the U.S. “Meanwhile, the complexity of China’s roads creates countless real-world challenges.”

A ZTO Express ADV drags a scooter along the road after knocking it over. Credit: 新闻晨报 via Weixin

Illustrating these challenges, domestic and social media have reported more than a dozen traffic incidents involving ADVs since their use began to soar during the pandemic. Most were minor scrapes with private cars or collisions with buses. The most serious case involved an ADV that knocked over an electric scooter parked at the roadside and dragged it along the road. No humans were reported injured in any of the accidents.

More recently, a dispute involving an SF Express delivery robot drew widespread attention. Following its programmed route through a village road, the robot ran over peanuts and corn that local residents had laid out to dry in the sun. Villagers reacted furiously, striking and kicking the vehicle.

In the U.S., the regulatory landscape is much more decentralized. Objections from residents, fragmented local rules and litigation risk make it hard for the industry to move beyond sidewalk-bot pilots tied to food-delivery platforms.

In 2020, when Amazon tried to deploy its delivery robots, the company had to lobby state capitols to change the legal definition of “vehicle” so that ADVs could operate on sidewalks.

Serve Robotics CEO Ali Kashani frames his mission as one that reduces the number of cars on the road. “Why move a two-pound burrito in a two-ton car?”

“A car has about 3,000 times more kinetic energy than one of our robots,” Kashani added. “So we don’t pose the same kind of safety risk to people when we are out there. In fact, we kind of make the city safer already when we replace a car trip with a robot trip.”

Coco and Serve both design their systems with human teleoperators monitoring in the background, which reassures U.S. regulators and the public but adds to costs.

Chinese companies such as Zelos, Rino.ai and Neolix also set up remote monitoring centers. When vehicles encounter an accident or obstacle, an emergency slowdown is initiated and they pull over to the curb. Remote operators only intervene when they detect an unusual situation.

SCALING AT A LOSS

As with so many industries in China before it, the ADV sector’s rapid growth has triggered a brutal price war. Zelos Tech offers certain models for 19,800 yuan ($2,700). Cainiao has launched a model at 16,800 yuan. Neolix offers installment plans with a down payment as low as 888 yuan and monthly payments of 3,000-4,000 yuan.

Chang, at Whale Dynamic, says that many vehicles are being sold at unsustainably low prices: “The story [ADV makers] sell is that they’re building volume fast to attract capital and go public, but the reality is the financing is showy, the profits aren’t there.”

The economic advantages of ADVs in China are also constrained by low human wage baselines. With the economy slowing, many unemployed white-collar workers have flooded into blue-collar jobs, keeping human delivery remarkably cheap.

“Labor isn’t scarce,” Chang says. “A single [short distance] delivery costs less than 1 yuan. Compared to Japan or Hong Kong, where a human courier is far more expensive, it’s very hard for an autonomous vehicle to undercut labor costs on multi-point delivery.”

Chan, the Princeton analyst, sees this dynamic as a classic case of involution, or neijuan — a form of excessive internal competition where ever more resources are poured in without realizing greater returns. The term, now commonly used in China, has been identified by the central government as a structural obstacle to sustainable growth.

“The irony is that we already saw a previous generation of this phenomenon in regular human delivery services — compression of wages … [and] harder pressure to reach delivery targets,” he says. “This is moving some of that into just a new area, but [it is] the same pattern. [Companies] are bleeding cash, running, trying to scale up quickly. It makes logical sense in many ways at the individual company level, but might not be healthy for the whole industry.”

As the use of ADVs increases rapidly, some delivery workers have expressed concerns about being replaced. But they are a marginalized group with little political power, given the Chinese Communist Party’s intolerance for labor activism, let alone independent unions.

DISPLACING THE MEN FROM SNOWY RIVER

Even before fully consolidating their positions at home, China’s ADV startups are also chasing big ambitions abroad.

Zelos has launched its first operational rollout in Austria and is preparing to expand into Germany, Switzerland, France, the Netherlands and other European markets. In Singapore, it is currently the only company whose L4 vehicles are allowed on public roads and is testing there, the company says.

Neolix has deployments in 13 countries, including Japan, South Korea, the UAE and Saudi Arabia. Its ADVs are being used by Swiss Post. German retailer REWE uses them for mobile retail services inside industrial parks, such as snack and drink sales.

In the U.S., Whale Dynamic has a joint venture with an American mapping company and a second project with a local EV charging provider. From the start, Chang says, the company has tried to navigate compliance risks carefully. He uses Nvidia processors and initially used U.S.-made Lidar before later switching to cheaper, more advanced Chinese Lidar.

But some Chinese suppliers, such as Hesai, have already landed on the U.S. Entity List, accused of military ties — a designation Hesai has fought to overturn.

Since 1988, federal law has required foreign vehicles to undergo a lengthy, costly process to prove compliance with U.S. safety and emissions standards — a measure originally designed to protect against Japanese and European imports but one that now blocks Chinese newcomers.

There are, however, workarounds. Cao Yang, owner of Los Angeles-based CDM Import, says Chinese minivans have trickled into the U.S. for two decades as “golf carts” or “farm vehicles”. Some states, including Texas and Oklahoma, have separate rules for low- and medium-speed vehicles that don’t use highways. And to reduce taxes and ease customs clearance, many shipments arrive as “parts” without engines, then are reassembled locally.

“As long as … a shipment is parts, not a complete vehicle, it can get through,” Cao explains. For now, ADV startups see such niches — private logistics parks, farms, and low-speed zones — as the most practical entry points, compared to tackling the regulatory gauntlet governing public roads.

Yet scaling up will not be simple. “When the numbers are small, nobody pays much attention,” says Chan at Princeton. “But once these vehicles expand and show up on the radar of politicians or the media, they can quickly become a flashpoint for drastic policy changes.”

For now, Whale Dynamic has found a less contentious testing ground — an Australian wagyu beef farm where its vehicles trundle across the plains, dropping feed for the herd. While ranch-hand wages are as high as AUD 130,000 ($84,420) a year, an ADV costs the farm only about AUD 55,000.

CLARIFICATION: This article has been amended to note that RoboSense designs its own receivers, emitters and processing chips — and that both RoboSense and Hesai claim to be China’s largest Lidar developer.

Peiyue Wu is a journalist based in New York City, where she mostly writes about China’s technology and business.

{kind=link}