Kyle Chan is a postdoctoral researcher at Princeton University whose substack High Capacity has become a must-read for anyone looking to understand China’s industrial policy and technological development. The following is a lightly edited version of a recent interview which took place in two parts: We updated the first part after the U.S. and China decided to mutually slash tariffs on each other on May 12.

Illustration by Kate Copeland

Q: To begin with the latest news and the agreement between the U.S. and China to cut tariffs back from their dizzying levels: where do you think we now stand in the trade war?

A: I have to admit, I was a little bit surprised. I didn’t expect them to come, come together and reset so quickly. I suspect this has happened because the Trump administration was prepared to cave quite quickly.

I see this as a temporary detente or walk back. The situation feeds into broader trends that extend beyond the reciprocal tariffs into a much longer-running and much more expansive battle between the two countries that covers not just trade, but also technology, even the movement of people between the two countries. On the positive side, it shows that they can walk back from the brink. But on the negative side, it offers a glimpse of how bad things can get and how far they are willing to go. As surprising as this recent truce is, it was also surprising how quickly things had escalated after the reciprocal tariffs were announced. How far both sides went really shocked a lot of people.

| BIO AT A GLANCE | |

|---|---|

| AGE | 37 |

| BIRTHPLACE | Los Angeles |

| CURRENT POSITION | Postdoctoral researcher at Princeton University |

This whole thing has really been a giant experiment that revealed the limits of how far Trump can go with tariffs. Now we can see that, at a certain point, markets will react so badly that Trump is faced with either shepherding the American and global economy into a recession, and perhaps even jeopardizing the dollar — or having to step back from the brink. Up until this point, you had Trump talking about tariffs, making really big, bold statements that were meant to shock. Now reality has called his bluff, to some extent.

I think that from Beijing’s point of view, this is a very useful piece of information. There will always be limits for China, despite all the tough talk about the amount of pain and damage they can suffer in a trade war. But now they can keep those limits quiet or more ambiguous; their red lines can be kept to themselves, whereas now I think the U.S.’s red lines have been revealed.

Where this ties in with your work is in the area of China’s industrial policy. The American argument is that this has led to overcapacity in many areas that Chinese companies are exporting abroad, disrupting global trade. Is it now time for China to do what many economists have long urged: reorient its economy towards more domestic demand, and less towards exports for growth.

China might not have any choice. I see rising tariffs, not just from the U.S., but from the European Union, from parts of the Global South — whether you’re talking about Brazil, Indonesia, or even parts of Southeast Asia that had previously been some of the greatest beneficiaries of integration with Chinese global supply chains. There’s growing pushback. You can break it down by sector, but there is a limit to how far the pure export-driven model can go in ramping up production to the extent that you are not just the largest producer of a particular item, but that you produce more than the rest of the world combined.

Beijing has a tin ear about the trade concerns of other countries, simply put. They see trade and access to affordable, decent quality Chinese goods as a win-win for other countries. And to a certain extent, it is, if you are focused on the buyers of those goods. But it is a way of seeing the world that fails to account for the domestic politics of these countries, and their concerns about workers, producers and the broader implications for their economic growth and prosperity.

A lot of people might say that industrial policy is simply what China does: its socialist system is very good at producing, whether it’s steel or electric vehicles. They’re less good at designing policies to create demand within China itself.

Definitely. These industrial policy tools that China has been using have been successful in ramping up production. But it is not a strategy for generating demand, and for creating the kind of domestic consumer base that would otherwise complement that kind of production. The system is focused clearly on one type of economic activity, and one idea of a trade relationship that not every country will be keen on.

Now it seems like Beijing is contemplating adjusting. One big area of change is the globalization of Chinese manufacturing: the spread not just of Chinese exports of finished goods, but also the rise of Chinese factories in other parts of the world. I’m talking about the actual building of factories that can employ, in theory, local workers, and that can contribute to local economic activity, and possibly offer channels for tech transfer or cooperation on innovation and technology.

That model is different, and we’re starting to see the beginnings of that in a number of countries. I don’t think, frankly, that Beijing is following this policy purely as a form of generosity to the world. I think there is demand from countries like Brazil, from Indonesia, and now perhaps from the EU as well, to bring Chinese manufacturing into their markets, and to try to re-adjust the share of the pie that is taken by different parties.

Do you think countries should contemplate copying the China playbook — agreeing to take investment from the likes of BYD or CATL or whoever, but saying: we want a joint venture, we want some of your technology and IP?

Yes, it would be at least useful to try this approach. The devil is obviously in the details. It will boil down to the specifics of how many jobs are created, what types of jobs are created, what type of production is happening — how much of the broader supply chain is being brought over, and also the details about any kind of technology sharing or cooperation.

But it’s a playbook worth exploring. Not only was it quite effective for China, it also offers an opportunity for other countries to become more competitive more quickly, to learn in areas where China is at the technology frontier, rather than trying to reinvent the wheel.

A big question for Europe and others is not just what sort of deal, or IP, they can get from China, but can they trust Chinese companies, their links to the state, what they’re doing with the data that they collect? How can China do better on the reassurance front?

I think the suspicion will always be there. And honestly, there are very good reasons for that. The evolution of technology towards greater connectivity, and a much greater emphasis on data transfer, collection and processing, and the diffusion of these technologies into new areas — like connected vehicles — together make concerns about surveillance and data collection all the more pressing.

…not only is China a useful case study for understanding the potential role of the state in the economy, but China itself is a huge factor causing other countries to rethink their approach to state involvement.

The question, then, is whether there could be a way in which data can be controlled. It may be that things have to be more extreme in terms of siloing responsibilities, covering even who gets to work on the code base, not just where “the data is stored”.

One extreme option is to wholly embrace Chinese investment in making everything from EVs to batteries to various consumer electronics, trying to bring some of that production back to the U.S. or Europe, and hope that the data doesn’t get used for nefarious purposes. I think that’s the wrong approach.

But I also wonder if it’s too extreme to go the opposite direction and to try to shut China out, essentially. You’d have to shut out almost all consumer electronics at this point, or even almost all household goods: Our refrigerators and microwaves are increasingly being connected to the internet, for better or worse. There’s a question of whether there’s a third path here.

You write about all these issues and more in your High Capacity substack. What are you trying to achieve with that?

Kyle Chan testifies at a hearing on ‘Made in China 2025’, held February 6, 2025. Credit: USCC

One of the biggest reasons I started High Capacity was because I felt the understanding of China and China’s industrial policy, and industrial policy more generally, was getting oversimplified, if not outright distorted, in public discussions. I wanted to add to the broader discussion in my own small way, from my own understanding of China’s development, and see if I can contribute greater understanding in this area.

One of the ironies is that my research was originally focused on a different but related topic, which is development. Development, for a long time, was seen as something that poor countries do to get rich, to get better educated, to move up the ladder. And China is one of the most interesting stories of development. Its pathways offer a way to understand development more broadly.

With the rise now of industrial policy and discussions about innovation and competitiveness coming out of the United States and Europe, as well as other parts of the world, I realize that the concepts that I used to associate purely with this older term, ‘development’, are now being applied more broadly, across so-called rich and poor countries alike. The effort to use some degree of state intervention in markets is something that is being reconsidered in a serious way in many parts of the world. Some of the lessons or insights from thinking about development in a previous era are being brought back and rethought in an era of rapid technological change, pressing climate change issues and broader geopolitical tensions. All of these are making countries that previously might have looked skeptically at state intervention reconsider their approach.

And a major factor in a rethink on all this is that people are looking at China and saying, hang on, they seem to have got something right…

That’s right. And not only is China a useful case study for understanding the potential role of the state in the economy, but China itself is a huge factor causing other countries to rethink their approach to state involvement.

You can imagine a world where you don’t have a player like China on the world stage: some American companies might do well, some — through the Darwinian process — might go extinct, and ultimately, the market system plays out, and that’s the end of it.

But having a player like China around, with the degree of its state intervention and state support in certain industries, and the sheer scale at which this is all being carried out, means that countries that were previously hoping to rely on purely the market find themselves caught out in the cold. You have companies, again and again, that perhaps would have done okay in a different situation, now running up against this much broader, much more different competitor than they had previously faced. So China is not only sort of an interesting case in itself, but it is actually one of the driving factors in the rise of industrial policy in the West.

What are some of the big misunderstandings about China’s industrial policy then?

One of the biggest misconceptions is the focus on its subsidies and a more limited China toolkit. One of the things that I try to emphasize in my writing is the range of different tools they use, the different actors involved, the different tactics and strategies, both domestically and even through international relations, that China has used — sometimes successfully and sometimes not.

Another misconception is this oversimplified, top-down view of how the Chinese political economy works. A lot of these industrial policy strategies entail some degree of signaling from Beijing — say, a national strategy plan with targets, goals, perhaps even a long wish list of areas where China hopes to become either strong or even dominant. But when it comes to the execution, in terms of the funding, the resources, the cultivation of companies on the ground, even some of the efforts to bring in foreign companies, and the broader formulation of strategies for industrial policy — a lot of this is happening at the local government level.

You see this again and again, whether you’re talking about electric vehicles or solar, or whether you’re talking now about AI. There is this pattern where, rather than having a single, coherent, unified national plan that’s just rolled out, you oftentimes have an overall agenda, and then the formation of different strategies locally. There’s a high degree of experimentation and competition that drives a lot of this among local jurisdictions, and among companies that they are trying to support. This is such a crucial aspect of what makes China’s industrial policy successful where it has been successful — and actually, marks a very strong departure from China’s failed experiment, previously, of a more top-down model.

The weakness of the current system is that while it’s all less coordinated than people think, you have provinces and companies competing with each other, leading to problems such as overcapacity and strains within the financial system. Is that fair comment?

Absolutely, there are repeated structural problems that arise from this approach. There is a tremendous amount of waste, there is a tremendous amount of ‘amateur hour’ when it comes to local government investment and their efforts to try to promote local industries — where people who don’t know what they’re doing, who are not industry specialists, are rolling out, say, data centers in a way that just doesn’t make sense, and also wastes resources.

This leads to a problem for a lot of companies trying to operate in this environment in which there is a race to the bottom: there’s an aggressive expansion of production capacity, and not as much attention paid to long term profitability, in the hopes that your friendly local government will bail you out or support you in some way. In a worst case scenario — and this has happened often in solar, batteries, wind, EVs — these companies end up with thin to no profit margins, and very little ability to invest in research and development into genuine innovation that would create a sustainable, long term competitive edge. This is a problem that is absolutely endemic to how China is going about all this.

…we don’t want to be in a position where we look back and wish that we had at least tried to slow down China’s access to the most cutting edge chips — in the way that we now look back and regret some of our failures to respond adequately to Chinese industrial policy in certain industries.

One way to think about this is that the kind of over-exuberance that this process creates is not totally different from the sort of bubbles that form in more market-driven economies — where investors get really excited and pile in to companies that don’t really have much to show in the way of immediate profits, but have the promise of being a good long term bet.

There’s smarter, more refined ways for Beijing to try to formulate some of its policies, where not every local government is jumping in to start an EV factory. The expansion of data centers, as I mentioned earlier, should be done in a way that meets certain minimum technical criteria. There should be efforts to adjust as the industry unfolds. Where Chinese industrial policy has been more successful is where it has been more flexible and able to adjust for some of the problems that inevitably arise.

One other critique of Chinese industrial policy is that it’s not creating enough jobs: these new industries won’t generate enough employment for China’s vast population in future. Do you see that as an issue?

The jobs issue is a weird one in China. Not so long ago, it was very, very important. It was such a delicate issue that local governments were afraid to stop supporting zombie industries in their areas, for fear that they would have mass layoffs and potentially social unrest. You had a lot of policies that were really designed not to be pro-worker, per se, but were designed to bring large scale, especially manufacturing jobs, to the economy. That was a key focus for a long time.

Top: Industrial robots at work inside Xiaomi’s ‘smart’ EV factory. Bottom: Baidu’s Apollo Go autonomous vehicle. Credit: Lei Jun, Baidu

Now what’s strange is China’s push for automation, and embrace of technologies like self-driving cars that, almost by definition, will result in fewer workers, or at least fewer workers per unit of production. This is something that I’ve been puzzling over.

One way of seeing this is that Beijing is hoping to embark on a kind of preemptive creative destruction, in Schumpeterian terms — they see the writing on the wall, that there are industries of the future that will rely increasingly on automation, that global competitiveness will depend on who can install more industrial robots in their factories than others. And when it comes down to preserving jobs versus maintaining economic competitiveness, it appears that Beijing is willing to emphasize the latter over the former.

There is already a backlash to this. You see taxi drivers upset about the rollout of say, Baidu’s Apollo Go, with autonomous vehicles you see concerns from delivery drivers. Many of them chose to go into food delivery because they lost jobs in other areas, and now they’re facing, potentially the loss of this way of earning a living. I don’t have an easy answer for that one, but it seems like a shift in priorities, or at least a short-term trade-off between different goals.

Could the longer term answer be the greater promotion of leisure industries and sectors like tourism and restaurants: the sort of thing that we’ve done in the West for years but seems an anathema, in a way, to Xi Jinping and his austere view of the world?

It could be, but I share your view of Xi Jinping’s austere vision. It seems that Xi really does not like consumerism, and these “softer” parts of the economy. China does promote leisure and tourism, but they just don’t have the kind of policy priority focus that, say, infrastructure still gets, and so-called hard-tech sectors, ranging from the automotive industry to aircraft production.

There’s perhaps even a view that the American way is the way to avoid — a primarily consumer demand-driven society that has lost the ability to produce real, physical goods. That is the foil to Xi’s vision of China’s economic trajectory.

One thing I would point out to help support this idea, is Alibaba’s change of fortunes now that it is one of the AI leaders in China, and can play a critical role, not just in pioneering world class foundation models, but in terms of rolling out the technology and increasing adoption, building the infrastructure for the cloud computing that will power all this. Alibaba’s value to Beijing has arguably shifted, from before being a provider of unnecessary consumer services and low value-add financial services to being an engine for AI.

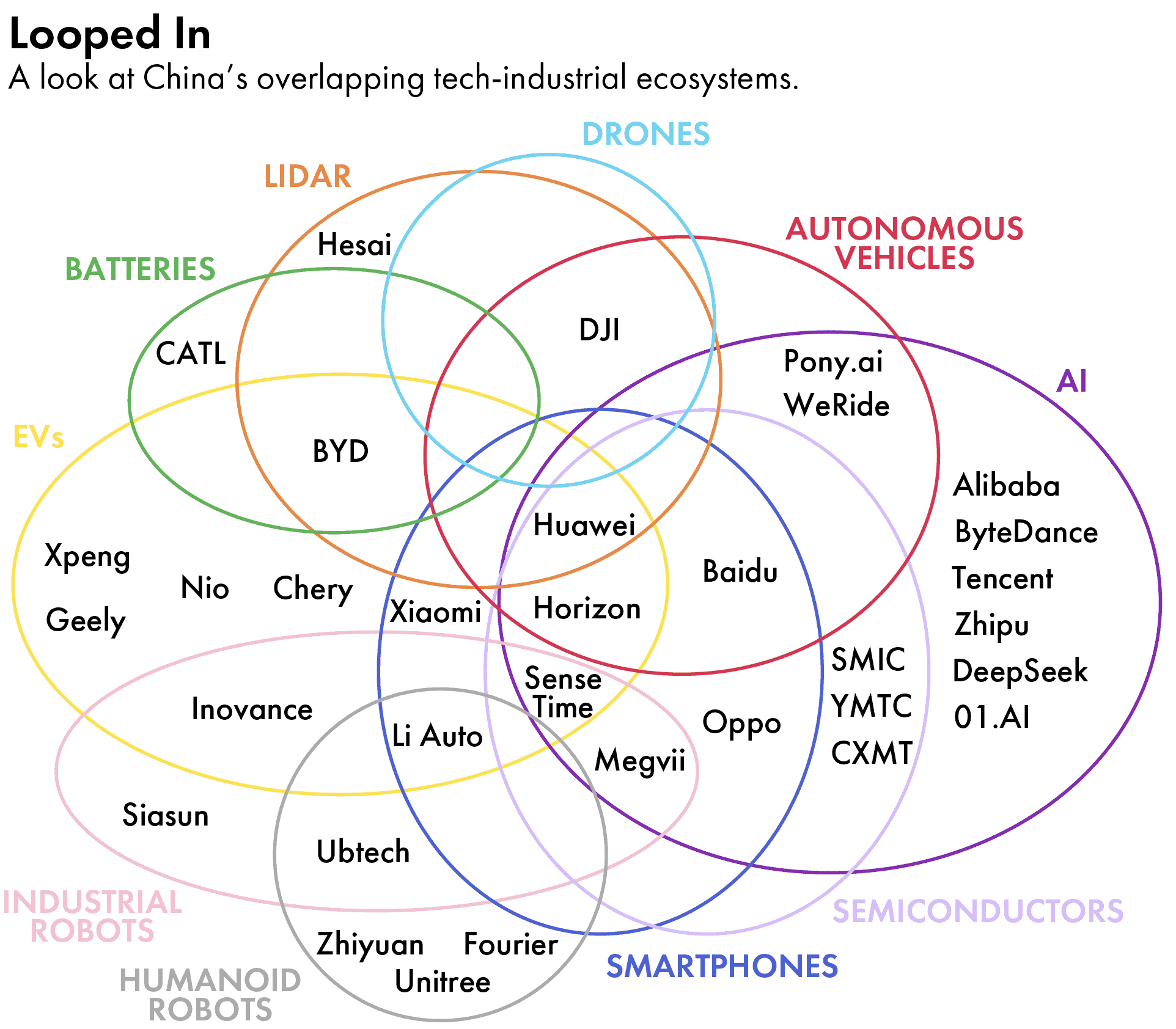

One of the pieces you wrote recently pointed out that one of China’s strengths now is that many of the new industries that the government has focused on are mutually reinforcing. Could you explain your thinking there?

The idea here is that it’s not just about being strong in EVs or batteries or drones per se, but that these industries have a lot of overlap, and that as you get stronger in a number of them, they actually mutually reinforce each other, creating an almost sort of interlocking ecosystem.

An example of that is autonomous vehicles and its reliance on a booming EV industry, and on domestic sensor makers for LiDAR such as Hesai, Robosense and Huawei, and the broader overlap with the push into AI as well as similar autonomous systems like drones. So China’s progress in autonomous vehicles is partly driven by its success in many of the underlying industries that go into or overlap with autonomous vehicles.

…if we really come to realize that China is a genuine technological competitor, we are more likely to be on our A game when it comes to playing in this competition.

It’s not only that they might share similar supply chains, but literally, you might have the same companies operating across these different spaces. You have EV makers like BYD getting into sensors after they originally began in batteries. You have smartphone companies like Xiaomi getting into EVs. You have industrial automation companies branching out.

So both in terms of the evolution of these industries, and even down to the individual companies themselves, you see something very interesting happening. Of course, at the heart of all that is Huawei, which is the paradigmatic example, the Hydra of the tech industry.

In the West, for many years, investors have argued that it creates more value to break up conglomerates. But that’s not the mindset at all in China it seems.

Yes. Some of this is driven by signals and policy support coming out of Beijing, as well as local government support for specific industries, that encourages some of these companies to branch out.

One other thing I have noticed is that this is part of a broader pendulum swing happening across China and the U.S., and maybe globally. There was also a time when China was trying to downsize its state-owned enterprises to focus them on core businesses, rather than them becoming a sort of state within a state. Now there is a broader shift towards Swiss Army Knife-type companies that can branch out. I think part of this is driven by something that is not specific to China, but is more fundamental to technology itself today, which is that you have a cluster of technologies that can build on each other, that connect with AI — where it can make sense to build on strong foundations in one area, to branch out into adjacent ones.

What’s your assessment of where China is in terms of its semiconductor manufacturing capability?

Semiconductors have been a huge priority for decades for Chinese industrial policy. It goes even further back than the recent export controls. Huawei, for example, was part of an effort in the 1990s to help develop semiconductors. And so there’s a long history there.

You can see it as both a success and a failure, because at the cutting edge, there is still a huge gap between what Chinese semiconductor companies, both in terms of design and manufacturing, are able to do domestically, and where the global industry cutting edge is — whether you’re talking about Nvidia’s GPUs, or you’re talking about TSMC’s ability to manufacture. In terms of mature node semiconductors, though, there has been a huge amount of catch up, and those chips matter tremendously to many sectors of the economy.

As for the U.S.-led export controls — I think they’re a good idea, and that we should keep and expand on them. We should be strengthening our enforcement. But we have to do this in a smart way that takes into account China’s response to what we’re doing. So far, it feels like these tools have been used in a more blunt and less strategic way than they could be.

We have to think carefully about what areas of Chinese semiconductor self-reliance we want to be incentivizing. That process of greater self-reliance will happen, and it doesn’t mean that export controls are useless. There is still a huge lag in, say, China’s ability to develop EUV lithography machines. That seems to be one area where a decade or more of a gap may exist.

But in other areas, we have to think hard about whether we are, in some ways, supporting China’s industrial policy, by forcing them to make a hard switch, which Beijing is often trying to do with its private sector players — trying to get, for example, EV makers to switch away from Infineon chips to domestically produced ones. We risk potentially helping Chinese companies make that leap if we don’t do this in a careful way.

And, just to clarify, why do you think export controls are the right approach?

Part of it is a national security issue — these cutting-edge chips go into missiles, autonomous weapons systems. They can be used in a variety of areas. I think about this within a ‘regret minimization’ framework: We don’t know how effective these export controls will be in the long run, as China may be able to develop some of these semiconductor manufacturing capabilities over time. But we don’t want to be in a position where we look back and wish that we had at least tried to slow down China’s access to the most cutting edge chips — in the way that we now look back and regret some of our failures to respond adequately to Chinese industrial policy in certain industries.

| MISCELLANEA | |

|---|---|

| FAVORITE BOOK | All That Is Solid Melts into Air by Marshall Berman |

| FAVORITE FILM | The Lives of Others |

| FAVORITE MUSIC | I love Bollywood music. |

| MOST ADMIRED | My fifth-grade teacher, Mrs. McConlogue, for her dedication to her students. |

The future is uncertain, but it is clear to me that we don’t want to be supporting China having a military edge in the future.

What is your sense of the general understanding of how successful China’s become in certain industries?

It seems like the understanding is starting to shift of where China is technologically and how China got there. It was not that long ago that you could still publish an op-ed about how China can’t innovate, they’re copying and stealing — and to be fair, that was a big part of the story before.

Now there seems to be at least the beginning of a shift. In the media, in policy debates, in even things like podcasts and the attitudes of people in Silicon Valley, there has been a slow shift towards a more accurate understanding. I think that’s really important, in terms of how we in the U.S., and the West more broadly, should be responding. If we were still in the mindset that China’s success was about cheap labor, stealing and copying, then that would entail a certain set of responses. But if we really come to realize that China is a genuine technological competitor, we are more likely to be on our A game when it comes to playing in this competition.

Andrew Peaple is a UK-based editor at The Wire. Previously, Andrew was a reporter and editor at The Wall Street Journal, including stints in Beijing from 2007 to 2010 and in Hong Kong from 2015 to 2019. Among other roles, Andrew was Asia editor for the Heard on the Street column, and the Asia markets editor. @andypeaps