Soumaya Keynes is an economics commentator at the Financial Times and host of its podcast The Economics Show. She has teamed up with long-time collaborator Chad Bown, a senior fellow at the Peterson Institute for International Economics and former chief economist at the State Department, on their timely and entertaining new book, How to Win a Trade War. In it, the pair talk about the pros and cons of launching such a war, and the best tactics and strategies to employ. In a recent interview with The Wire China, we discussed the book’s main themes: what follows is an edited transcript of that conversation.

Illustration by Lauren Crow

Q: Before we get into the main topic of your book — how to win a trade war — I wanted to ask how you define when you are actually in one, as opposed to the normal cut and thrust of countries complaining about each other’s trade practices.

A (Soumaya): I remember having this argument when I was at The Economist [at the time of the first Trump administration]. I maintained that a trade war was an escalation of tit-for-tat trade barriers in a kind of spiral, whereas some people wanted to call the round of tariff events at that time a trade war.

Today, I have a much broader definition of trade wars — that they happen when governments are essentially weaponizing trade flows. That needn’t take the form of tariffs, of course: it could take the form of export restrictions.

And it also needn’t be an explosion. It could be happening behind the scenes in a very slow way. One of the arguments in the book is that while Trump has started many trade wars, there was a different trade war going on before he came along, which was effectively due to China’s mercantilist approach to trade. There is a different, bigger trade war that China started, which I wouldn’t have referred to in that way back at the beginning. But now we both think that’s the main one; and that we’re definitely in one now.

| SOUMAYA: BIO AT A GLANCE | |

|---|---|

| BIRTHPLACE | London, UK |

| CURRENT POSITION | Economics columnist and host of The Economics Show with Soumaya Keynes podcast at the LSE |

Chad: China’s domestic policies, its subsidies and its industrial policy, which contribute to it producing too much and importing too little, are huge contributors to the trade war. So it doesn’t have to be policies imposed at the border that identify a trade war.

That means, in turn, that it’s actually really hard to then figure out if you’re in a trade war or not. You can’t just look for things like tariffs or export restrictions to know it. Part of the problem today is everyone’s focused on the trade wars that Trump is engaging in and starting, and much less focused on the bigger underlying issue — which is what China’s doing.

What justifications can there be for launching a trade war?

| SOUMAYA: MISCELLANEA | |

|---|---|

| FAVORITE BOOK | Sum: 40 Tales from the Afterlives, by David Eagleman |

| FAVORITE FILM | “Favorite” is stressful but I did really love The Ballad of Wallis Island |

| FAVORITE MUSIC | Folk/singer-songwriter |

Chad: The one we are most concerned about is the excessive dependencies that can build up on unreliable trading partners. We saw some of this during the pandemic, when we suddenly had shortages of things ranging from personal protective equipment to semiconductors, and governments began to look more closely at where they were sourcing essential goods from. We saw with Russia’s invasion of Ukraine, Europe especially being really dependent on Russia for natural gas, and to a lesser extent, oil — a dependency that was really problematic.

And then more recently, but building up over time, it’s really been the rest of the world’s increasing dependence on China for a lot of essential goods, whether it’s raw materials or manufactured goods. The argument is that when those excessive dependencies build up, you may need to take action to reduce them and begin to engage in a trade war,

Illustration by Lauren Crow

Soumaya: I just want to add a nuance to that: it’s not just the high dependencies. It’s high dependencies interacting with a willingness to use those dependencies for coercion. Britain is highly dependent on many other countries for trade, but it’s not always a problem, for example.

There are clearly two problems in the relationship between China and the rest of the world, one at the macro level and one at the micro level — and to an extent the micro level problems are a symptom of macro level problems. Some of these dependencies have built up because of China’s subsidy-soaked model. If China’s trade was more balanced, if it was importing more, there might be a bit more mutual interdependence that would make this less of a problem. I don’t think the two are really separable.

This is another area where we think there’s been an evolution of the narrative. During the first Trump administration, everyone lost their mind explaining why Trump was an idiot for focusing on the bilateral trade deficit — and he still focuses too much on it. But that crowded out the conversation we needed to be having about the U.S.’s overall trade and current account deficit, which has created a financial risk for the country. China’s massive current account surplus is in turn a big problem, not only because it’s a missed opportunity for Chinese consumers, but also because of the financial risks that it’s building up.

| CHAD: BIO AT A GLANCE | |

|---|---|

| BIRTHPLACE | New Jersey, USA |

| CURRENT POSITION | Reginald Jones Senior Fellow, Peterson Institute for International Economics |

Chad: Even if you fixed the imbalances problem at the macro level, you could still have really severe dependencies at the micro level in certain sectors that you would be concerned about, and want to take action over.

That’s a point you make in a very interesting chapter on global imbalances: although you seem to have had a slight disagreement over whether to include these in the book…

Soumaya: Chad didn’t want to include imbalances because he hates macro!

Chad: I do get worried about big imbalances. I just don’t think trade policy is going to be able to do much to fix them. The imbalances problem would really be much better addressed by changes in domestic policies, whether it’s on the United States side, dealing with our fiscal problems, and paying more in taxes and spending less; or on the Chinese side, by encouraging more domestic consumption.

| CHAD: MISCELLANEA | |

|---|---|

| FAVORITE BOOK | Anna Karenina, by Leo Tolstoy |

| FAVORITE MUSIC | Taylor Swift (obviously) |

| FAVORITE FILM | Pitch Perfect (the original) |

| MOST ADMIRED | My daughters |

So I didn’t want to engage on this issue from a trade policy perspective, because tariffs should not be part of the conversation when it comes to trying to fix global imbalances. If you apply tariffs bilaterally, you will only shift the imbalances around. All the U.S. tariffs have disproportionately been imposed on China. Sure, the bilateral deficit with China is smaller, but it’s just led to a rerouting of trade and growing deficits with other countries. The size of the overall U.S. deficit with the world has not changed all that much.

Soumaya: You are pushing on the Soumaya-Chad buttons here! I’m going to add an explanation of why Chad doesn’t like macroeconomic imbalances — they are just much harder to analyze than trade flows at the micro level. The data is, by definition, much more aggregated, and we don’t have a very good understanding of what exactly drives these imbalances. Macroeconomists yell at each other about how it’s all driven by one side or the other, and they have models that tell those stories: But it’s very hard to distinguish between them. Chad has to contend with people yelling at each other about definite truths, when actually it’s much murkier than that.

My counter argument is that one, this is clearly a very important topic in the minds of policymakers, so we had to include it in the book, whatever we think about the theory. Two, as I said earlier, macro problems and micro problems are deeply interconnected. You can’t understand the micro problem without understanding the mechanism by which China has built such enormous capacity in certain areas. It’s not all about rare earths, it’s also about what they have done to manufacturing supply chains.

And three, there is a really important intellectual contribution to be made by saying, look, everyone’s fighting between these binary positions — on the one hand, it’s all to do with U.S. borrowing, or on the other hand, it’s all to do with China’s under-consumption. Actually it’s both, and you are saying something when you say that we can’t determine which causes which. If you’re on a see-saw and it’s unbalanced because there’s a fat person on one end, and a thin one on the other, then it’s both their fault.

The final point is that there is an intellectual case that tariffs could affect the trade deficit, or current account deficit. If you think of tariffs as a tax on consumption, essentially, they should reduce consumption and U.S. borrowing. There is a world in which that dynamic would be important. Empirically what we see, though, is that that can often be overwhelmed by other factors.

Part of the problem today is everyone’s focused on the trade wars that Trump is engaging in and starting, and much less focused on the bigger underlying issue — which is what China’s doing.

Chad Bown

So where we come down on macroeconomic imbalances is that yes, there are genuine problems associated with them, but trade policy is an extremely unreliable tool in terms of tackling them.

Chad: I do want to say we argued a lot, and at the end of it, Soumaya was right, and I’m glad we included it.

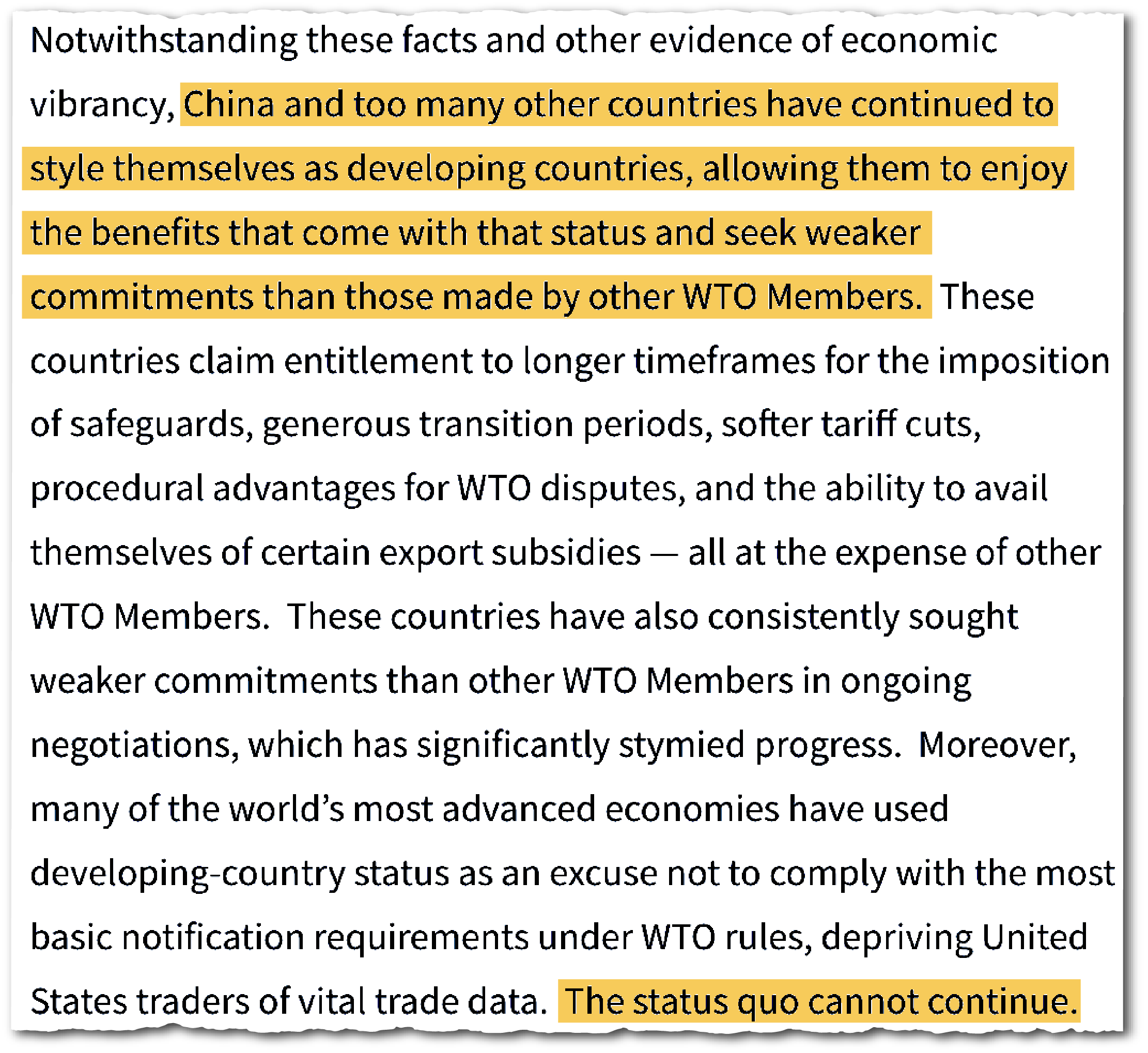

On China more specifically: Do you both now think that its behavior and the model it has developed, particularly since it joined the WTO, is something that justifies trade war-like actions from the U.S. and other major powers?

Chad: There’s two pieces to that answer. The rules of the trading system under the WTO have just not been fit for purpose for dealing with China’s economic model. WTO rules require transparency. You have to have a common definition for what a subsidy is, for example, and with China, that’s just not been the case. Our existing frameworks for both understanding the Chinese system and dealing with it weren’t adequate.

But the second, more important factor, was that it became clear that under President Xi Jinping, China has had a very different view of international trade and interdependencies with the rest of the world. That started with the Made in China 2025 policy, where they set explicit targets for dominating certain sectors; and then later with the dual circulation policy, explicitly saying we want the world to become dependent on China for its supply chains, but for China to not be dependent on the rest of the world for anything else. That really said to everyone, we don’t believe in interdependence in the same way that the international WTO rules were set up to accommodate.

And so you put those two things together, and the fact that China has just become so massive — and so every decision that it makes on its industrial policy or on tariffs has significant repercussions on countries all around the world — and that says you have to do something about it. You have to do things in terms of your own policy interventions to neutralize some of those effects. So to me, at least, those are the main arguments for why, yes, there’s absolutely justification to fight a trade war with China.

At the Wire we have had a long running ‘Rules of Engagement’ series of interviews with U.S. policymakers from the last 30 years, and the core question we asked them was whether it was a mistake for the U.S. and others to accept China into the WTO. What are your perspectives on that?

Chad: I don’t think it was a mistake. You have to think about what the counterfactual would have been. It’s not as if China, had it not entered the WTO formally, was going to live in autarky. It was going to engage in international trade and integration on some terms with the rest of the world. The WTO approach was an excellent attempt to see what would happen.

Now ultimately, the WTO ended up constraining the rest of the world, explicitly through some of its dispute settlement rulings on the use of anti-dumping, countervailing duties, and unfair trade practices by Western economies; but also implicitly, it took countries’ eyes off the ball in terms of what China was actually doing for a very long period of time, with everyone just assuming that China was going to become more market-oriented and play by the rules.

When it turned out that China wasn’t going down that path, the onus was on the rest of the world to prove why. And we’re still trying to do that, as it’s really hard to do that right. How do you explain to the world that no, China is not following the rules, it has all these subsidies — when the subsidies themselves are not transparent? This is a difficult empirical case for data nerds to make, because in many respects, China looks like a market economy to outside observers. It’s got prices, it’s not dictating individual decisions in the same way that the Soviet Union was under communism.

Soumaya: I basically agree. The mistake was in not being creative enough and assertive enough in enforcing the rules and making sure that a balance of rights and obligations was there.

During the first Trump administration, there were many folks acknowledging that there were genuine challenges associated with China. One proposal I heard was for the U.S. to file a big case at the WTO, essentially arguing that China hadn’t, in a broad sense, lived up to its obligations. Had a group of big countries taken that case early enough, maybe it would have achieved something. That was a missed opportunity.

So having decided that some kind of action towards China is now necessary and justifiable, how do you assess the way that the U.S. has gone about it?

Soumaya: The easy analysis with the second Trump administration is that it should not have confused everyone by fighting a trade war against everyone simultaneously. We’re not the first to say that.

If the concern is that there are particular products for which we are over-dependent on China, and you need to send companies a signal that you can’t source from China anymore, then maybe there is a role for tariffs to give that demand signal. But trade is like water: so what’s happened with the bilateral tariffs is that trade has been rerouted. So in case one, imports flow directly from China to the U.S.; in case two, imports go from China to Vietnam to the U.S.; in case three, China exports to Vietnam, and the displaced exporters there export to the U.S., so there isn’t actually any Chinese content in those Vietnamese products.

The second of those could be dealt with, for example, tougher rules of origin on imports coming in from the outside world. That’s a move that the Trump administration has chosen not to make, perhaps out of concern that the Chinese might retaliate. The other thing that is necessary if you’re going to tackle dependencies seriously is a huge amount of data. There have been steps towards investing in more of that infrastructure, but there’s much further to go.

Chad: There is a consistency, albeit with a difference in application, in the way both the Biden and Trump administrations are using industrial policy. Under Biden, you had the CHIPS Act. Part of that was wanting some diversification of supply of high-end chips outside of Taiwan. But China has also shown signs that it might gain market dominance in mature node semiconductors over time — as we saw happen last year with the weaponization of the chips coming out of Nexperia, which nearly shut down automakers in the United States and around the world.

The Inflation Reduction Act also had elements in it recognizing concerns over China’s market dominance for critical minerals; the tax credits for electric vehicles were contingent on the batteries not containing too much Chinese lithium, cobalt or graphite, to encourage the establishment of supply chains in other countries for those sorts of critical minerals.

…I think it’s going to end up being a complete mess: product by product rules, trade barriers, regulations, it’s going to be incredibly incoherent. We’re all just going to stumble along — which is going to be a situation that is going to benefit the biggest players.

Soumaya Keynes

The Trump administration is doing it slightly differently by taking ownership stakes in companies — MP Materials first, and then a number of other critical mineral companies — and establishing price floors: the point being that you can use subsidies to try to establish alternative sources of supply outside of China for the things that you’re really worried about being excessively dependent on China for.

What did you both make of the recent announcements about the Boards of Trade and Investment with China. Is this an effective acknowledgement from the U.S. side that it can’t change China, and that we have to learn to live with that?

Soumaya: I think the Trump administration is probably right to give up, essentially, given where China is. They’re a big country, they are not going to accept the humiliation of having their own economic model challenged or changed by the U.S. or anyone else.

They’re going to react to the rest of the world, but they’re not going to be led. And so it is about managing the risks associated with that situation, rather than coming up with some grand bargain that would structurally fix all the irritants in the relationship.

Chad: The only quibble I have is that the Board of Trade idea isn’t the first time that Trump has done this. This is what the Phase One agreement really was in Trump’s first term. If you look at the details of that, it was completely silent about subsidies — which is them effectively giving up on changing the Chinese model. The deal was saying, ‘please buy this amount of American stuff’. But there was nothing in that agreement about reducing or eliminating all the retaliatory tariffs that China had imposed back during the first trade war. It was going to have to be done through the Chinese government telling companies to buy American stuff, despite the fact that they were faced with higher tariffs. So it was going to have to be some sort of weird managed trade outcome, even back then.

This time around, the question is, what do they mean by managed trade? Is it just on the export side, or is it also going to be on the import side too, what the United States buys from China: and if so, what would that mean? Are they thinking about adjusting the tariffs? Or about having quotas? Are they going to ask China to do voluntary export restraints?

Soumaya: In summary, we think they gave up a long time ago.

One tactic you can use in a trade war again, that you discuss in the book, is export controls. Are you in the ‘Jensen Huang camp’, which argues that in the long run they’re a waste of time; or are you more in the ‘national security side’, which worries China will use the chips to develop their AI and their military, and so on?

Soumaya: This was a fun one. My own position changed as I was reporting and researching, because the Jensen Huang arguments are pretty powerful. The argument that you hear is that China has a large number of engineers; and when you’ve got lots of developers working with your products, whenever there’s a problem, they tell you about it, and that obviously makes the product better. By exporting you are then also importing value, as you’re getting information back on how to make your product better. And so it is a concern if the U.S. is effectively ceding the market and giving that free labor resource to Chinese competitors, that could eventually enable them to surpass the United States.

But there is inherently a zero-sum element to this. I’d love everyone to cooperate and write nice rules about AI safety, but it’s just not the world we are in right now. So while there are some really powerful arguments, overall they’re not powerful enough to justify a free-for-all — which I’m not sure even Jensen Huang would argue for, even he would be in favor of some restrictions on the very highest range. The debate is how high up the sophistication scale do you limit chips.

The reality is that compute is a constraint right now, and the export controls do place further constraints. The critics’ argument is that they’re effectively strengthening the other side, that the unintended consequences are so extreme that they override the benefits. I haven’t seen anything to suggest that those consequences are so big that that is the case. So overall I’m more in favor of the export controls.

One thing that we try to say in the book is that trade wars are so hard to win, which is one reason you should read it! These tools are really hard to use. They have massive unintended consequences, including the ones that Huang describes.

But just because there are unintended consequences, that isn’t always enough to say that you shouldn’t be using these tools at times. The situation that we’re in is that we can’t get the first best world, and so these unintended consequences are something that we may have to accept in certain situations.

At the end of the book, you indulge in some stargazing, looking into where all this will lead in 20 or 30 years time. When we look back at this period then, do you think we will see it as the start of the world splitting into two or three different economic camps; or as a blip in the long march towards a world of free trade and capital flows?

Soumaya: My prediction is that it’s going to be much messier than either of those two outcomes. I suspect that the period [of trade peace] that is ending, or has now ended, was probably what was more likely to have been the blip. And what we’re going to go into now is going to be much more chaotic, and it could last for a really long time. You do already see in the data a shift towards regionalization, towards trading with partners who are in the same geopolitical block as you.

I have so little faith in countries to come together to sort things out that I think it’s going to end up being a complete mess: product by product rules, trade barriers, regulations, it’s going to be incredibly incoherent. We’re all just going to stumble along — which is going to be a situation that is going to benefit the biggest players.

Chad: This is an argument that Soumaya and I have throughout the book, about the willingness of countries to cooperate, especially the Western allies. That’s really going to be the key point. I don’t see much changing in the current administration. There have been small signals about their willingness to do things with partners and allies, but they’re so minor.

The only ones that will really be able to navigate this world, aside from the big countries, are probably big companies that can afford to hire all the lawyers they need and to move their supply chains in ways to be able to take advantage of the increasingly fragmented world.

Chad Bown

So then the big question is, how much will future U.S. administrations retain in terms of tariffs? Is there any more willingness to work with partners, especially as they’re now facing their own China shocks?

Soumaya is probably going to win this argument, too. It’s just really hard to get all these countries to do things together — in which case, we will end up in the world that Soumaya articulated, super messy and dominated by a few big players. The only ones that will really be able to navigate this world, aside from the big countries, are probably big companies that can afford to hire all the lawyers they need and to move their supply chains in ways to be able to take advantage of the increasingly fragmented world. So, it’s a big mess, but hopefully this book provides a way to help folks understand how to understand it a little bit more clearly.

Soumaya: It is optimistic! We are trying to provide positive, constructive things that you can do. But it’s hard.

Andrew Peaple is a UK-based editor at The Wire. Previously, Andrew was a reporter and editor at The Wall Street Journal, including stints in Beijing from 2007 to 2010 and in Hong Kong from 2015 to 2019. Among other roles, Andrew was Asia editor for the Heard on the Street column, and the Asia markets editor. @andypeaps