For the past two decades Chinese development finance has filled major energy and infrastructure gaps in the global South, helping to fuel economic growth. However, COVID-19 and other woes within China have collided with increasing levels of debt distress among borrowing nations, reversing the promising growth of Chinese finance. To make matters worse, finance from the West has also decreased, especially from the private sector.

This decline in the finance available for developing countries will not only restrict their ability to meet the needs of their citizens, but could also stunt global economic growth. Numerous analyses show that Chinese development finance has spurred growth where private finance and the World Bank have been less effective. Reviving Chinese development finance will be crucial in helping some of the world’s poorest countries to revive their economies, and could also help China regain global market share in the Global South and allies in an increasingly divisive world.

Data from the Boston University Global Development Policy Center show how significant China’s role has been. China’s two overseas development banks, the China Development Bank and the Export-Import Bank of China, have provided close to $500 billion in combined financing to developing countries since 2008. That’s equivalent to about 70 percent of the lending made by the World Bank over the same period. Given that financing from the World Bank and its counterparts has remained stagnant since the 1990s, China has helped fill widening infrastructure gaps across the Global South.

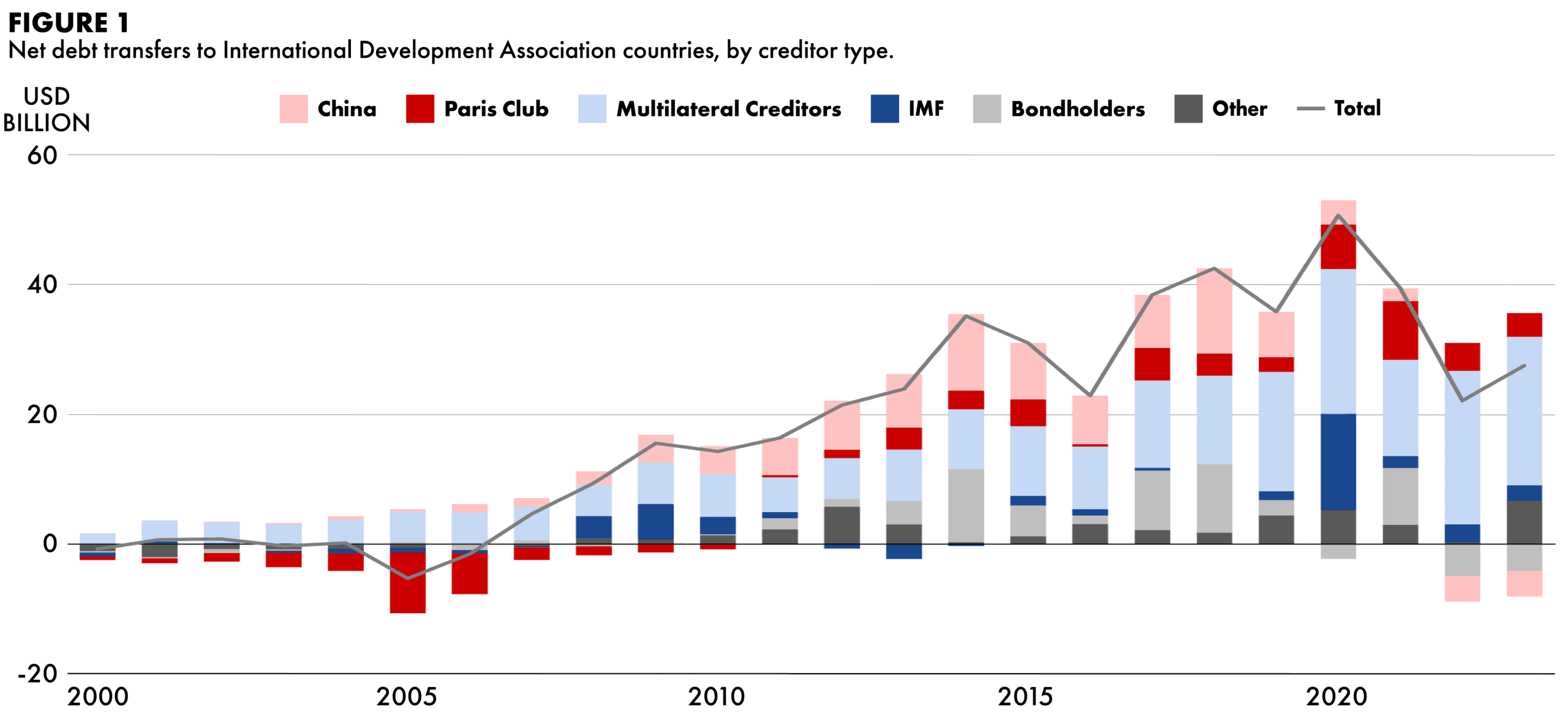

That’s the good news. The bad news is that China has pulled back on sovereign lending to low-income countries at the same time as private lenders have also retreated. In 2022 and 2023, countries eligible for concessional lending through the International Development Association (IDA), an arm of the World Bank for the poorest countries, sent more money to repay China and bondholders than they brought in through new loan disbursements. Figure 1 shows how these reversals have dampened the financing available for IDA countries.

Given the increase in global economic uncertainty and the growing impact of climate change, now is an opportune time for China to revive its overseas lending. It is also in China’s interest to look beyond simply issuing new debt. In Sub-Saharan Africa where the situation is the most acute, several countries are already spending as much government revenue on external debt service as they did on the eve of the 1990s debt crisis in the continent. While China played little to no role in causing this crisis, as Chinese finance represents only 8 percent of Africa’s external debt, the perception that countries cannot pay China back will not encourage Beijing to authorize substantial new lending.

China has already played a large role in efforts to ease debt pressures, providing the most debt suspension to countries in distress since the outbreak of COVID-19. The G20 group of leading nations created a Debt Service Suspension Initiative in 2020, which was extended in 2021, to suspend the external debt of the poorest countries. Participation was voluntary, and the private sector and multilateral development banks like the World Bank did not join. In the end, China provided 63 percent of the debt relief provided under the initiative despite being owed only 30 percent of the payments due. Returning to simply issuing new debt would be difficult so soon after supporting such a major debt relief initiative.

China could instead return to engaging with development finance through a combination of: refinancing old debt, judiciously issuing new debt to countries that have the economic capability to use it for growth, and complementing it with additional investment and trade. The first option — refinancing — would be particularly advantageous in the current environment. The Chinese interbank rate hovers at close to 1.5 percent, far lower than U.S. interest rates. China could swap its expensive dollar-denominated loans with newer, longer term RMB-denominated bonds issued at much lower interest rates. That would give lower-income countries much more fiscal space to be able to borrow and invest again, and ease pressure on the balance sheets of China’s banks.

As the country faces decoupling from Western markets, it is in China’s interest to revive financing to the developing world to help create new market opportunities.

Moreover, China could expand its foreign direct investment into countries that are developing their manufacturing capacity, and could share some of its technology and business expertise, as well as employment opportunities, with host countries — just as China required Western countries to do in its earlier days of reform.

Trade policy also matters: It is essential that China commit to importing more goods and services from countries paid for in RMB. Otherwise, developing countries will struggle to pay back their RMB-denominated debts, in the same way that they struggle to pay back dollar liabilities currently.

Some steps in this direction are already underway. In October last year, China refinanced its debt with Kenya, swapping dollar debt for longer term RMB loans and lowering the interest rate from 6 to 3 percent, saving the Kenyan government $215 million per year in debt service. However, Kenya is still not earning enough RMB by exporting to China to guarantee this debt can be paid back; nor was the refinancing coupled with new lending to spur economic growth.

China’s retreat from overseas lending has come at precisely the wrong moment. As the country faces decoupling from Western markets, it is in China’s interest to revive financing to the developing world to help create new market opportunities. Refinancing developing country loans into RMB will also alleviate pressure on Chinese bank balance sheets, and help China expand the internationalization of China’s currency. Such a strategy should also help recipient countries to restart productive investment and growth. In a world marked by rising geopolitical tensions and fragmentation, there is now a critical opportunity for China to solidify and expand its relationships.

Kevin P. Gallagher is Professor and Director of the Boston University Global Development Policy Center.

Rebecca Ray is a Senior Academic Researcher at the Boston University Global Development Policy Center.