The extent of China’s leverage in trade negotiations with the United States has seemed to stun the Trump administration to date, not least at the leaders’ meeting in South Korea last month. Indeed, China’s ability to put in place export and import controls, particularly over rare earths, has stymied Trump’s efforts to reshape the global trading system.

Yet China’s leverage is not new, nor confined solely to trade. For decades, China has been building countervailing power that is further challenging the U.S.-led world economic system as a whole — sometimes even for the better. If the U.S. now overreacts to China’s growing influence, it could lead to a dangerous fragmentation within the system it did so much to build.

In a new book I have written with Gregory Chin titled China and the Global Economic Order, we trace how China slowly went from being a ‘rule taker’ within the U.S.-led Bretton Woods institutions such as the International Monetary Fund (IMF) and the World Bank, to a ‘rule maker’ outside that system. That transformation has given China the leverage to now become a ‘rule shaker’ back inside those U.S.-led institutions.

Indeed, China has been quite successful in meeting its objectives within these institutions, learning and obtaining what it needs to pursue its own national economic development objectives. It has done so without wholesale assimilation into the norms of the current order, despite the outsized role the U.S. has carved for itself within both institutions thanks to the voting power that gives it an effective veto over their decisions — along with the ‘gentleman’s agreement’ whereby the head of the World Bank is always an American and that of the IMF a European.

The U.S. is now pushing back against China’s increased influence over both the World Bank and IMF. In doing so, however, it runs the risk of further undermining their legitimacy.

Founded in 1949, the People’s Republic of China (PRC) was not, of course, present at the creation of the Bretton Woods institutions, which were set up in 1944 as part of the U.S. and its allies’ preparations for the post-War global economic order.

In fact, the PRC didn’t join the World Bank and the IMF until 1980. For the rest of the last century China was welcomed as a ‘rule taker’ in both institutions, especially at the World Bank. Through that institution, China received important loans to help fund the country’s economic reforms, as well as important technical advice on how to carry them out. China was a rule taker at the IMF as well, but to a lesser degree: it embraced the U.S. dollar-led system and integrated into the fund’s financial accounting systems. But it would never take an IMF loan that came with conditions, such as privatizing state owned enterprises or deregulating the Chinese financial system.

By the turn of this century China began to change its stance at both Bretton Woods institutions. China had graduated by then from low income country status (and from receiving the subsidized World Bank loans that come with it) and was well on its way to becoming the economic powerhouse it is today. At the World Bank and its counterparts, China began to argue for a greater voice and more representation, and for more of their financing to go towards infrastructure and industrialization.

After the IMF’s calamitous performance during the East Asian Financial Crisis of 1997, China joined the chorus of other countries in the Global South saying that the fund should end its insistence on financial deregulation and austerity as bailout conditions, and also began calling for a greater say in its decision-making. When the U.S. exploded the world economy with the 2008 financial crisis, China went so far as to call for the IMF to move away from the U.S. dollar as the key reserve currency of the global system, and replace it with a currency issued by the IMF itself.

These calls were largely ignored in both of the 19th Street buildings in Washington that house the IMF and the World Bank. That’s when China began to assert itself as an alternative global ‘rule maker’ through separate organizations and initiatives. China co-founded and has helped to continually expand the Chiang Mai Initiative, Asia’s alternative to the IMF, as well as the BRICS-led Contingent Reserve Arrangement, set up to provide support for member countries facing short-term financing issues. What is more, the People’s Bank of China, the Chinese central bank, began providing currency swaps to developing nations during times of crisis, a move that has helped to assert China’s claim to global financial leadership.

Two of China’s own development banks (co-designed with the World Bank), began lending overseas and by 2016 were providing just as much lending across the globe as the World Bank — but mainly for infrastructure and industrialization, and without the strings the legacy institutions attach. Later China co-founded the Asian Infrastructure Investment Bank and the New (BRICS) Development Bank, which also prioritize sustainable infrastructure.

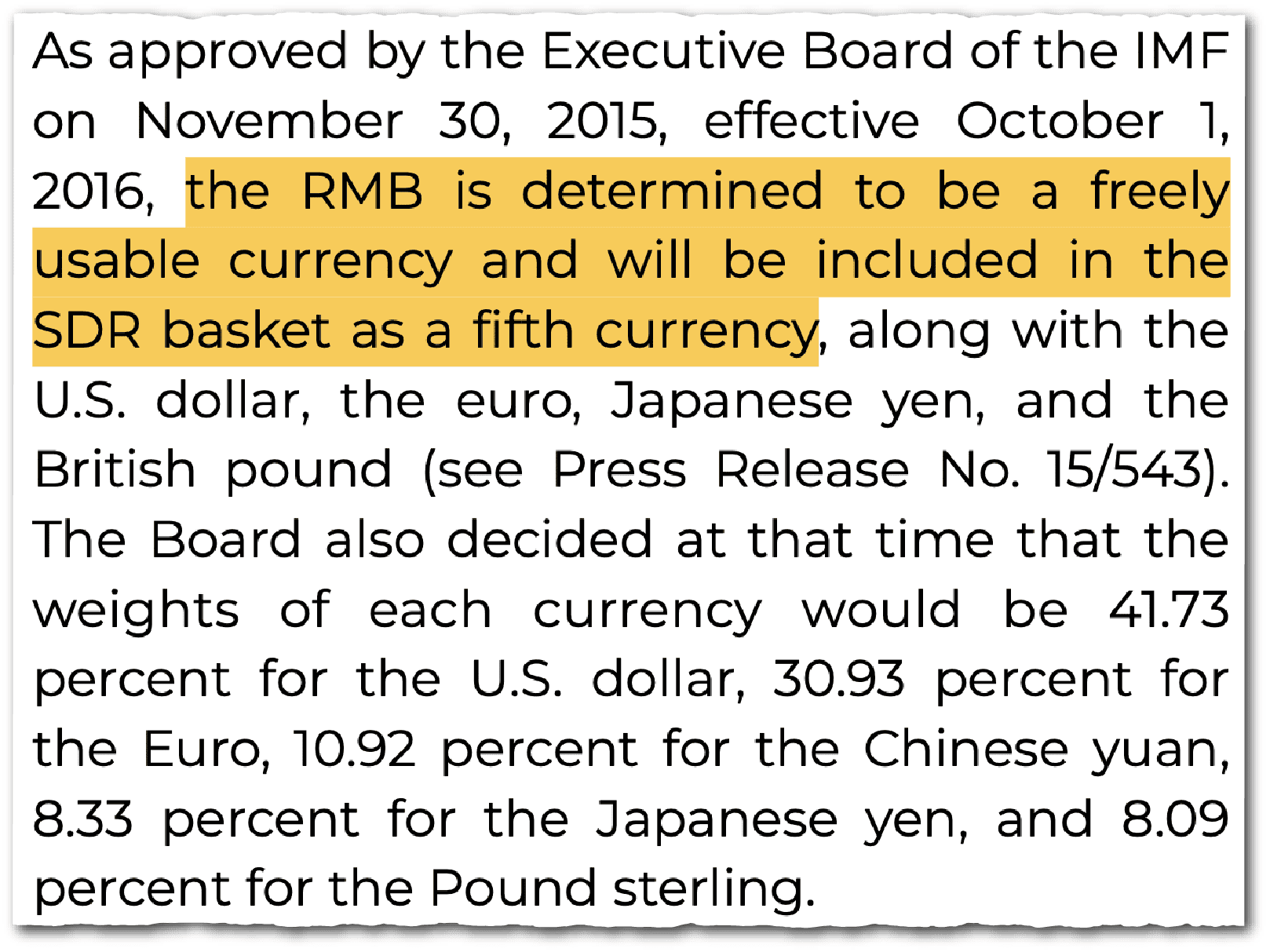

Setting up these alternatives has given China significant leverage both at the IMF and World Bank, despite its relative lack of voice and vote compared with the United States. In 2016 China was able to get its currency added to the basket of currencies that back IMF loans alongside the dollar, the Japanese Yen, the Euro and others — a move that signaled acceptance of the yuan into an elite club of global currencies. It has helped make the IMF more flexible on financial regulation and exchange rate policy, and now has the third largest vote share in the institution, behind the U.S. and Japan.

At the World Bank China has meanwhile helped spur new investment in infrastructure, and to loosen its lending conditions. In our book we argue that not only did China’s entry into these institutions help shape its economic trajectory and make the world economy more stable; China’s ‘rule shaking’ has also improved IMF and World Bank policy.

The U.S. and its allies rightly welcomed China into the global economic system, but China has been able to craft a leverage strategy to get more say than the West could ever have imagined was possible…

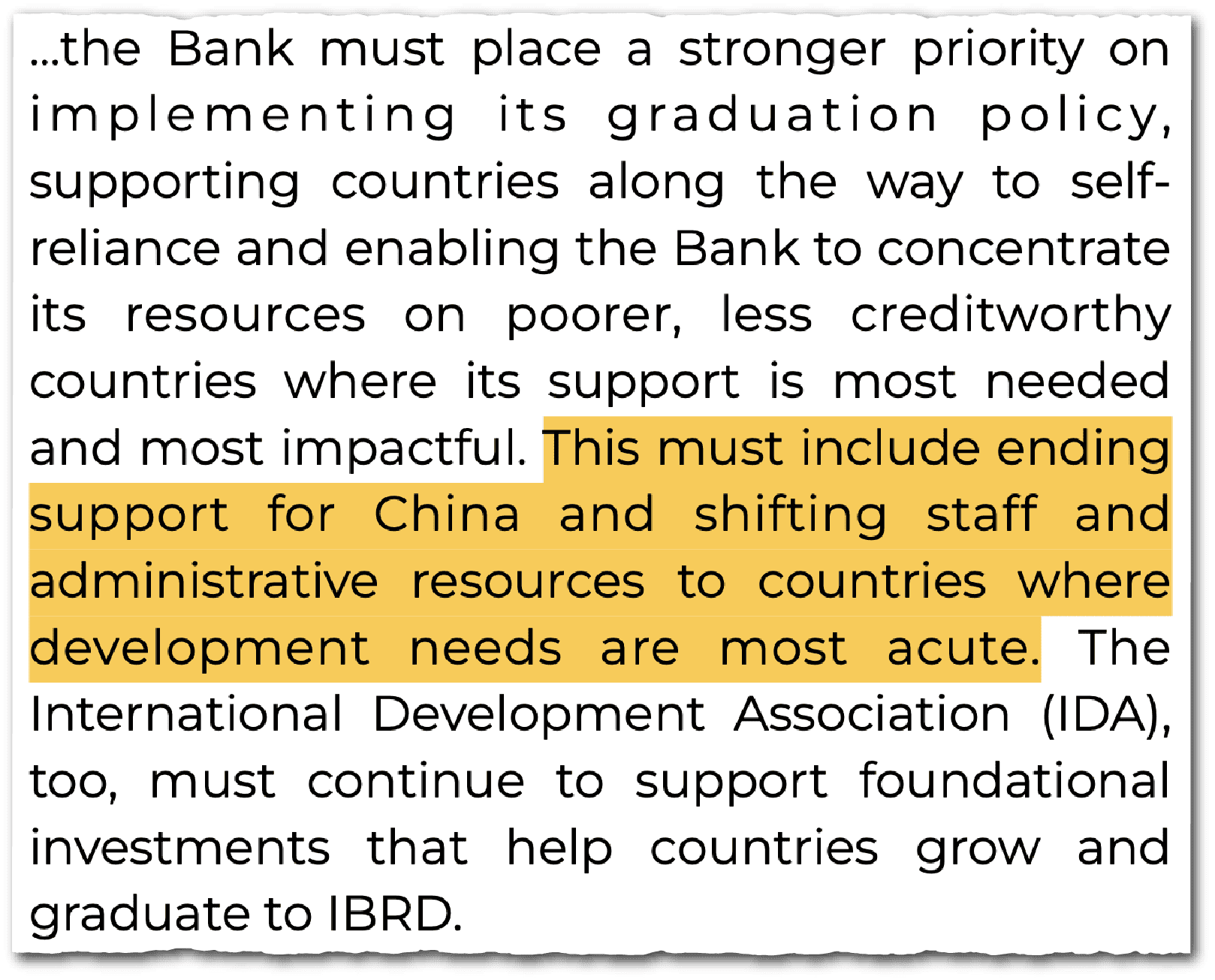

But have China’s efforts hit their limit? Its success has certainly led to a U.S. backlash. In President Trump’s first term his World Bank appointee David Malpass sacked the bank’s arm that conducted research and strategic advice to countries on China’s Belt Road Initiative, and began blaming China for the debt crisis in the Global South (despite the fact that World Bank debt to those countries dwarfs China’s and the fact that China has provided the most debt relief since COVID hit). President Biden, too, refused to enlarge the World Bank in part because his administration didn’t want China to have more voice.

During his second term, Trump has considered withdrawing from these institutions but now says the United States is ‘in it to win it’ — with winning meaning ending support for China at the World Bank and not granting China more voice at either institution.

This poses two problems. By the rules that the U.S. wrote for the IMF and World Bank, China should have more voice in these institutions given its increased economic prowess. Changing the rules or even pushing China out would substantially erode the legitimacy of a set of institutions and jeopardize the stability of the global economy.

China is already far from alone in criticizing the Western stronghold on governing the global economy in an increasingly multi-polar world. Indeed, in many ways China has simply joined and amplified a chorus that had already sounded in the 1980s when these institutions became the beacons of the ‘Washington Consensus’.

After their experience with the Asian and Latin American crises, most middle income and developing countries have already essentially all but stopped borrowing from the IMF; only the poorest countries, with no other lifeline in times of financial crisis, reluctantly remain. For sure, developing countries are more supportive of the World Bank and its counterparts, which have made strides in the way they provide development finance and which played a key role during COVID. Having a plurality of such institutions can provide healthy competition: Those countries that receive development financing from China tend to get more infrastructure financing from the World Bank, under less onerous conditions.

But when it comes to financial crisis fighting, having a fragmented system would make financial stability worse, not better. One need not look further than the example of Europe, where the sometimes poor coordination between the European Central Bank, the European Stability Mechanism, and the IMF accentuated and prolonged the crisis of the early 2010s. If even those relatively like-minded institutions couldn’t collaborate smoothly, how could we expect a diverse set of institutions headed by the U.S., China and others to stamp out the next major problem?

The West is at a crossroads. The U.S. and its allies rightly welcomed China into the global economic system, but China has been able to craft a leverage strategy to get more say than the West could ever have imagined was possible — so much so that its tight grip on the institutions that lead the global order is loosening.

Yet China is now far too big to kick out, especially as it would likely take many other countries with it if that happened. That would lead to a fragmented global order that would struggle to prevent and mitigate global challenges such as threats to financial stability and climate change.

The other option is to figure out a better way to work with China and other countries across the global South and recraft a more inclusive and stable global economic order. It’s pretty clear which way things are heading — it’s high time the U.S. and others learned to adapt.

Kevin P. Gallagher is Professor and Director of the Boston University Global Development Policy Center.