It was not the restrictive visit, surrounded by military personnel, that many of David Peng’s friends had predicted for his trip to one of the largest space-launch facilities in China. “There were balloons and kids in astronaut outfits, drawing and singing songs,” the Hong Kong-based investment advisor said of his recent trip to the Wenchang Space Launch Site on Hainan island, a critical facility for China’s commercial satellite launchers.

“China is in its space era, no different than the Americans in the 60s,” Peng added. “There’s this pride that — with the Americans keeping them outside the international system — China has done this on its own.”

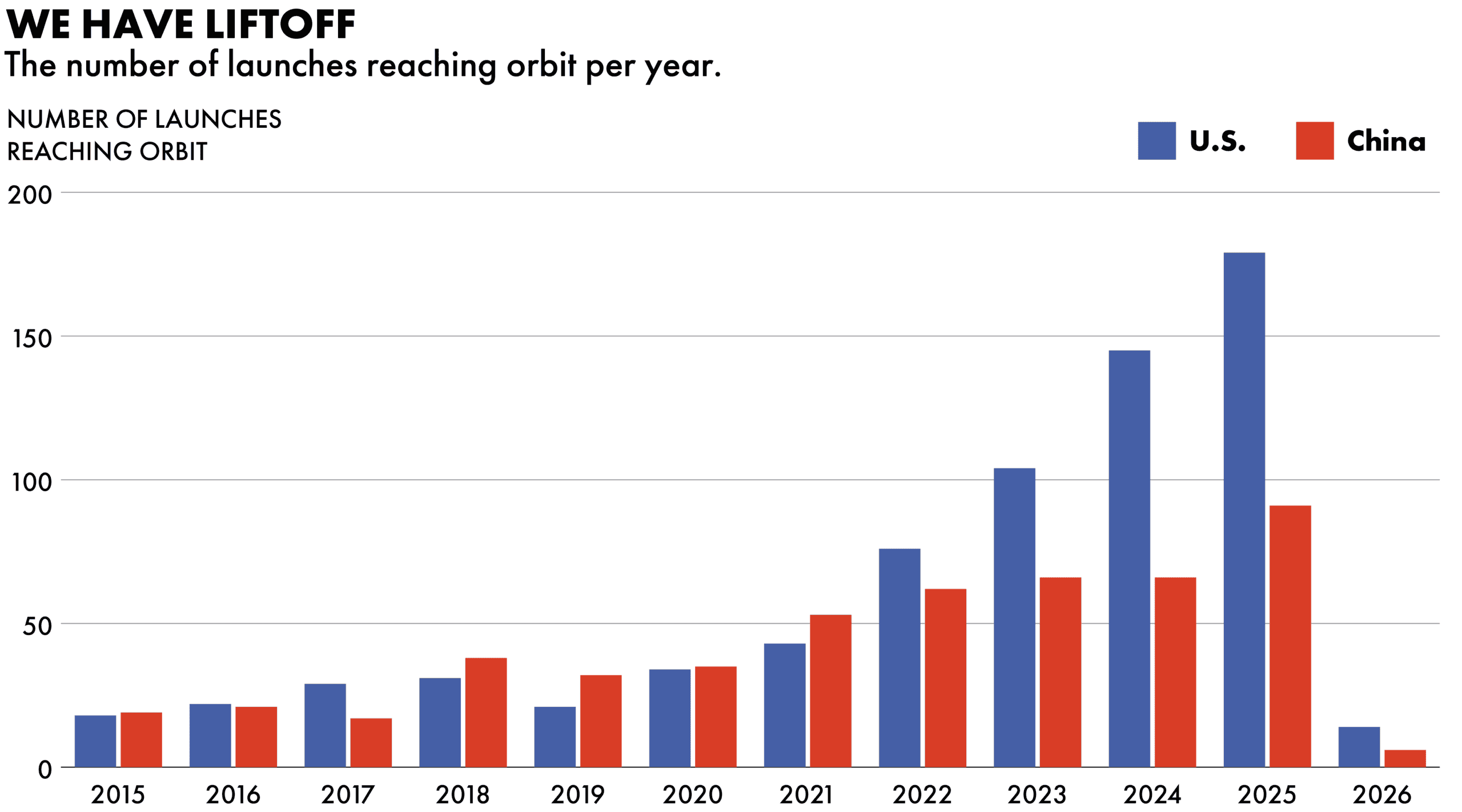

The recent progress in China’s space sector has been impressive. Last year the country managed 92 launches, up from its previous record of 68 in 2024. Leading commercial rocket companies such as LandSpace and Galaxy Space have made a major contribution to this — one that is likely to grow as the Chinese government looks to the private sector to help realise its lofty space ambitions.

That marks a significant change for a sector over which the state had a monopoly until 2014.

“It was forbidden [for private companies] to invest in rocket launchers in China. It was considered a defense technology, just as everywhere else in the world,” says Alexandre Najjar, Manager and Space Industry Analyst at NovaSpace, a space consultancy.

As their budgets were cut in the 1980s, state-owned companies had started to engage in some commercial activity, launching satellites for foreign customers.

“As part of the policy of reform and opening, Deng Xiaoping tried to sell Chinese rocket launch services to the West, and he was initially modestly successful,” says Brian Harvey, a Dublin-based space historian. “They got licenses to launch Western payloads in the early 1990s.”

But U.S. restrictions on Chinese space exports in the late 1990s brought this to a halt, and were reinforced by the 2011 Wolf Amendment. Sponsored by Representative Frank Wolf, the amendment prohibited NASA and other government institutions from using public funds for bilateral projects with China without approval from the Federal Bureau of Investigation, severely curtailing space-related cooperation between the two countries.

The early 2010s was also the beginning of a new era in the global space industry, marked by the growing participation and success of commercial companies, most notably Elon Musk’s SpaceX. China was no exception.

“The rapid rise of foreign commercial space companies, such as SpaceX, exerted significant pressure on the national team,” said Han Yuexia, a space expert at the Chinese Academy of Sciences, referring to the existing state-owned space industry.

A key moment came in 2014 when, to the astonishment of observers, SpaceX successfully tested a reusable Falcon-9 rocket. “The Chinese were taken aback by it. They should have been — we all were”, said Harvey.

Faced with SpaceX’s Sputnik-like breakthrough, many wondered if China’s existing state space companies could keep up. “Policymakers and people working in state-owned enterprises realized that they might fall behind the U.S., which would be unacceptable,” said Dr Lucie Sénéchal-Perrouault, a researcher affiliated with the Alexandre Koyré Center near Paris.

SOEs were not built for the kind of risky and rapid innovation needed to keep up with SpaceX. “They’re not supposed to squander public money, so they would rather use technologies that are well-established rather than try out new things”, adds Sénéchal-Perrouault.

Yang Fang, a professor at Southeast University in Nanjing whose team researches biotech applications related to aerospace, said the Chinese government “recogniz[ed] the strategic and economic benefits of incorporating commercial dynamism”.

“The government identified that leveraging private capital and innovation could accelerate technological progress, reduce costs and foster a more robust space industry chain, all critical for great power competition,” she added.

“China does not yet lead globally across space innovations, but it has built a strong state-directed program that is advancing at scale,” says Altynay Junusova, an analyst at MERICS, the Berlin-based think tank. “It’s only a matter of time before it catches up to the leading edge.”

China aims to be a major space power by 2030 and a fully comprehensive space power by 2045, with ambitious plans for a lunar base, space exploration and space resource utilization.

Commercial companies are expected to play a role. Yang notes that in recent policies there are “clearer pathways for private involvement in major projects like lunar missions”.

In the long term, the involvement of commercial companies “will definitely make, for example, deep space exploration more cost effective”, said Jie Gao, a research associate at the Asia Society Policy Institute in Washington.

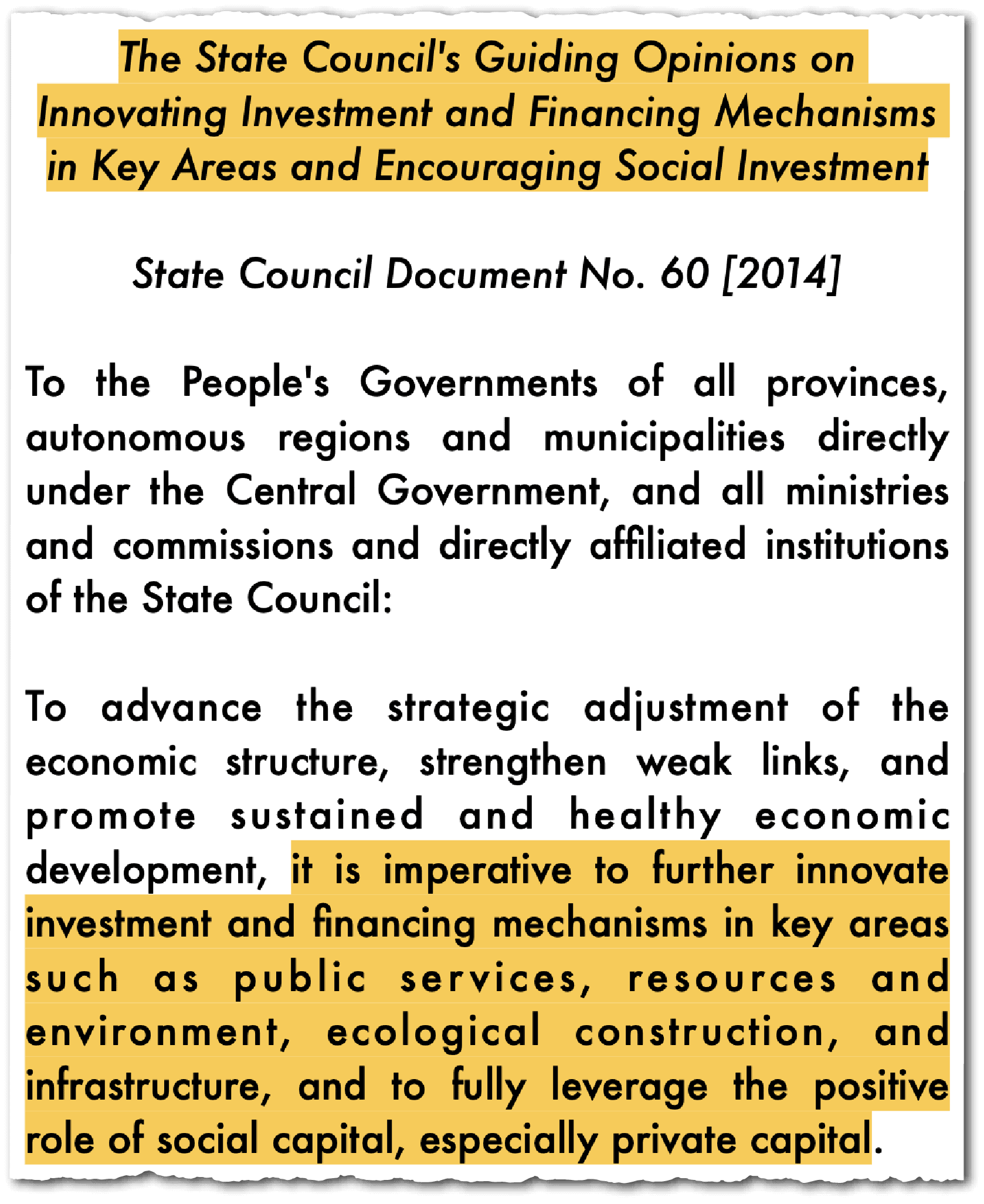

DOCUMENT 60

In November 2014, a guiding opinion — known as ‘Document 60’ — was issued by the State Council. It encouraged “private capital to participate in the construction of national civil space infrastructure”, which was then the exclusive domain of SOEs.

It was a “watershed moment”, says Yang, adding that it “provided the legal and political legitimacy for commercial ventures”.

But many in China’s space industry were wary about the nascent sector’s prospects.

One issue was that, in a legal and regulatory context designed for SOEs, the commercial launch industry operated within what Sénéchal-Perrouault has described as “a vague and poorly adapted framework”, until new regulations were introduced in 2019.

Another concern was how the SOEs would respond.

Chinese commercial space companies exist because the state decided to create a controlled, complementary commercial sector to serve its broader strategic objectives. Success is measured not just by market profit but by contributing to the overarching goal of making China a space power.

Yang Fang, professor of Biomedical Engineering at Southeast University in Nanjing

“Initially, there was a certain amount of caution,” said Blaine Curcio, founder of Orbital Gateway Consulting and a leading authority on China’s space industry. “There was a lot of skepticism about the openness of the established entities like CASC to allow this competition,” referring to one of China’s largest space SOEs.

Nonetheless, many were excited about the new opportunities commercial space offered.

“People were tired of working in state-owned enterprises, and they wanted to be China’s Elon Musk”, said Sénéchal-Perrouault. “The culture differs from SOEs, where hierarchical structures are rigid and communication styles feel very old-school. Private enterprises have this cooler vibe.”

Though the success of Musk’s SpaceX was critical in convincing the Chinese government to allow the creation of commercial space companies, China’s sector is very different from that of the U.S. — particularly with regards to the role of the state.

Anup Gholap, a space industry analyst at Resonance, characterizes China’s commercial space sector as one that features “policy-guided competition” and combines “state strategic control with private-sector execution speed”.

“Chinese commercial space companies exist because the state decided to create a controlled, complementary commercial sector to serve its broader strategic objectives”, says Yang. “Success is measured not just by market profit but by contributing to the overarching goal of making China a space power.”

Alongside fully commercial companies, which still enjoy various kinds of state support, commercial space in China also includes spin-offs from CAS and SOE subsidiaries.

The result is that China’s commercial rocket industry is “very fragmented and very heterogenous”, says Najjar.

“FIGHTING TO THE DEATH FOR MARKET SHARE”

The commercial space sector has expanded rapidly from a dozen companies in 2015 to more than 300 by 2022.

But with SOEs still dominating much of China’s space sector, these new commercial players are directed into a limited number of areas. Yang says the central government “sets the direction [and] defines the permissible ‘track’ for commercial activity”.

She adds that there is a complementary relationship between SOEs and commercial companies: “SOEs outsource niche tasks to agile private players. The state guides commercial companies toward non-critical or innovative segments, such as small rockets, while SOEs focus on strategic national projects.”

Ultimately, says Sun at Southeast University, “the two [sectors] form a closed loop from basic technology research and development to market application and back to basic research, achieving mutual complementarity and promotion.”

Commercial innovation also benefits the state programs. “State-owned enterprises could, in theory, scoop up some of that technology,” said Dean Cheng, a Senior Advisor to the United States Institute of Peace, a Congressional-funded think tank.

There are examples of SOEs supporting private companies, particularly in their first few years, by for example selling critical technologies to them.

But the sometimes complementary relationship between commercial and the state space firms can also be competitive and antagonistic.

While there is, says Han, “talent mobility and technological exchange” between state and private-sector firms, there is also “debate and intense competition over national resources, funding, launch sites, and more”.

Within the broader space industry, “some argue commercial firms should have more access to state resources,” says Yang, “others emphasize maintaining SOE dominance for national security.”

Talent is another area of intense competition. Before 2014, the country’s aerospace engineers worked exclusively at SOEs. “They worked for the state programs, and then they moved to the private sector,” says Junusova.

“Some of the commercial companies can actually offer better salaries than the SOEs,” said Ian Christensen, Senior Director of Private Sector Programs at the Secure World Foundation (SWF).

Top engineers are sometimes headhunted from the state sector. In 2018 Zhang Xiaoping, a sought-after researcher, reportedly multiplied his salary by a factor of ten when he left a state facility, the Xi’an Aerospace Propulsion Institute, to work for private rocket company LandSpace.

But SOEs retain strong influence over regulatory frameworks, funding mechanisms and procurement decisions, making it difficult for fully commercial companies to compete with them, according to research by Sénéchal-Perrouault.

“[Private-sector] companies really had to fight to get to the launch pad, and now they are fighting to the death for a market share — and always with some pressure from state-owned enterprises who, because it’s a policy that’s encouraged by the central [government], cannot publicly oppose commercial space,” says Sénéchal-Perrouault.

Many commercial players are still closely tied to national projects or have business models that depend on the state launch projects, somewhat limiting true market-driven innovation.

Rachel Kong, an Industry Analyst at ABI Research

At the same time, many provincial and municipal governments have become keen supporters of commercial space companies, particularly in recent years.

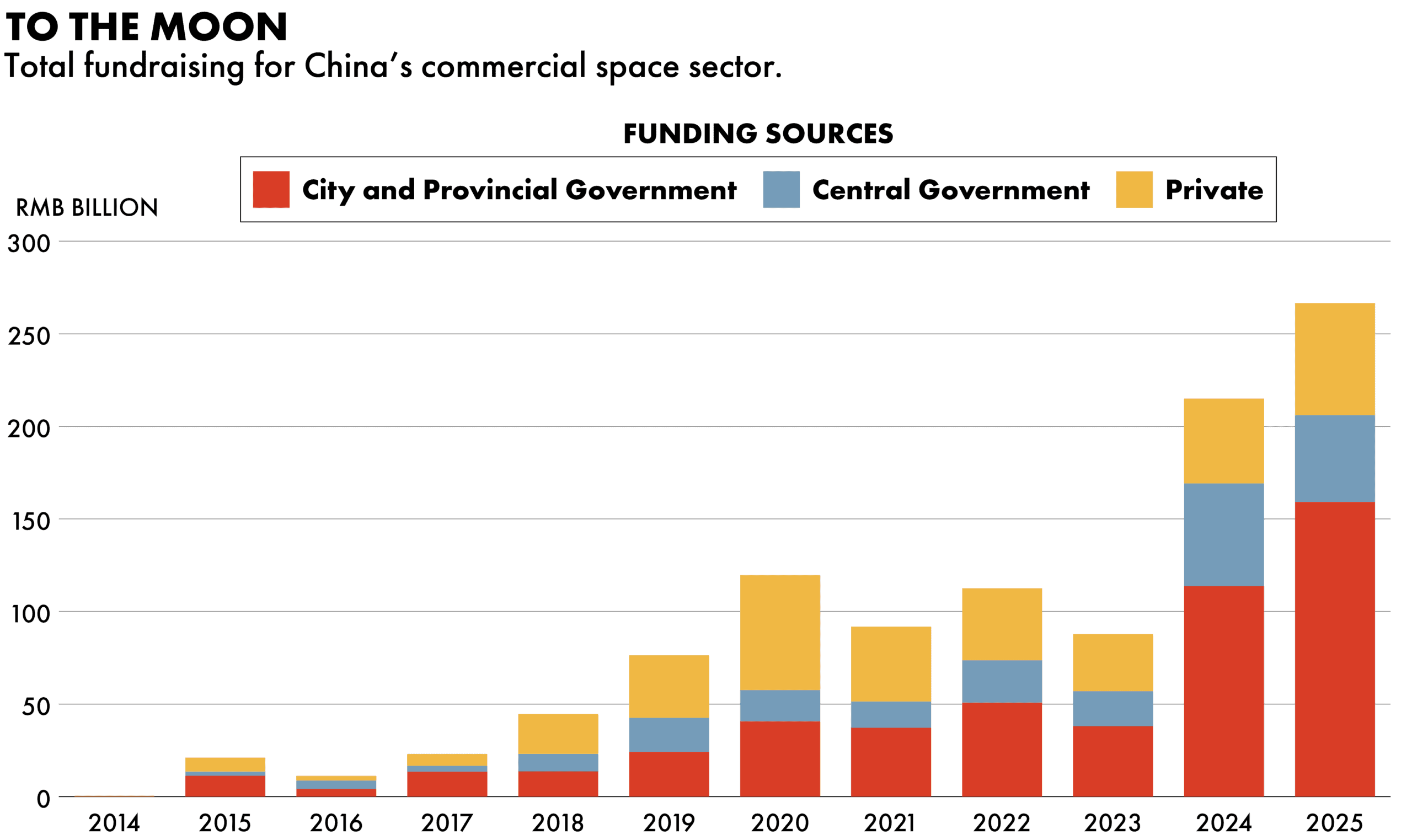

In 2025, local governments accounted for about 60 percent of total funding for Chinese commercial space companies — their highest ever share, according to estimates by Orbital Gateway Consulting.

This is, in part, a response to central direction. Han notes that “commercial space was included in the national government work report in 2024, recognizing it as a national innovation-driven engine — thus [local governments have] an obligation to fulfill the call from the central government”.

But many provinces and cities also see commercial space as a high-tech industry that could drive development. “Local governments are highly focused on cultivating new industries and economic growth, and commercial space provides a rare opportunity,” says Sun.

Local governments offer a range of policies to attract and develop commercial space companies. One is industrial parks and clusters such as Beijing’s “Rocket Street”, which opened in January. Another is targeted financial support. Beginning this year, space companies based in Shanghai’s Songjiang district can apply for various subsidies including for fixed asset investments, successful rocket launches, and insurance costs for satellites.

Alongside established centres like Beijing and Shanghai, less developed provinces including Heilongjiang and Gansu have also implemented policies to foster a local commercial space industry.

STRUGGLING TO GET OFF THE LAUNCH PAD

But even with staunch local government support, the rocket launch sector in particular faces serious challenges.

Some Chinese commercial space companies have made significant strides. In July 2023, LandSpace became the first company worldwide to successfully launch into orbit using methane-liquid oxygen, a clean propellant well-suited to reusable missions. But doubts remain about how innovative the sector is as a whole.

“Many commercial players are still closely tied to national projects or have business models that depend on the state launch projects, somewhat limiting true market-driven innovation,” says Rachel Kong, an Industry Analyst at ABI Research.

Another issue is the sheer number of companies, many of which were started with local government backing.

Curcio estimates there are “several dozen” Chinese launch firms, only eight of which have managed to put a rocket into orbit.

On February 14, 2026, SpaceX launched 24 satellites into orbit with its Falcon 9 rocket. Credit: SpaceX

Unlike in the U.S. — where SpaceX’s dominance makes it a magnet for aerospace talent — in China “you have so many launch companies that there’s no clear leader”, he says. That can lead to further fragmentation. “Such a broad dispersion of talent”, Curcio adds, “[means that] if I’m a really good rocket scientist in China and I’m not convinced by the technology at my company or I have my own ideas, I go set up my own”.

THE MEGACONSTELLATIONS

There are also concerns around how many will ever manage to become profitable. Building successful rocket businesses is notoriously difficult — and not just in China.

“Launch is just not a good investment”, says Najjar. “It’s by nature a business that does not make a lot of money. It’s really challenging to be profitable.”

While China’s space companies have cost advantages in areas like manufacturing, overall costs remain too high.

These companies face particularly challenging economics because of the high upfront capital costs required to build rockets.

One way to make launch more affordable is to use larger rockets, which generally offer lower costs per satellite launched, says Najjar.

Launching larger reusable rockets more frequently would allow Chinese companies to significantly reduce launch costs, he says. Economies of scale have allowed SpaceX — which in 2025 launched into orbit more times than the rest of the world combined — to achieve profitability. “But you will need to launch thousands of satellites,” he adds.

Such a scale-up requires a clear source of demand, which China’s commercial sector has long lacked.

…the race track has become narrower, and more commercial space companies are pitted against each other in narrowly defined areas.

Han Yuexia, a space expert at the Chinese Academy of Sciences

Commercial space companies have often avoided competing with state launchers for major national projects, such as China’s Tiangong space station. “As a result the race track has become narrower, and more commercial space companies are pitted against each other in narrowly defined areas,” Han and other researchers have argued.

“There’s no clear project to take up enough launches to create a clear-cut leader”, says Curcio.

Companies therefore focused on small, single-use rockets which they could use to demonstrate the reliability of their technology, potentially raising more funding.

That, however, is changing with the emergence of satellite “megaconstellations”.

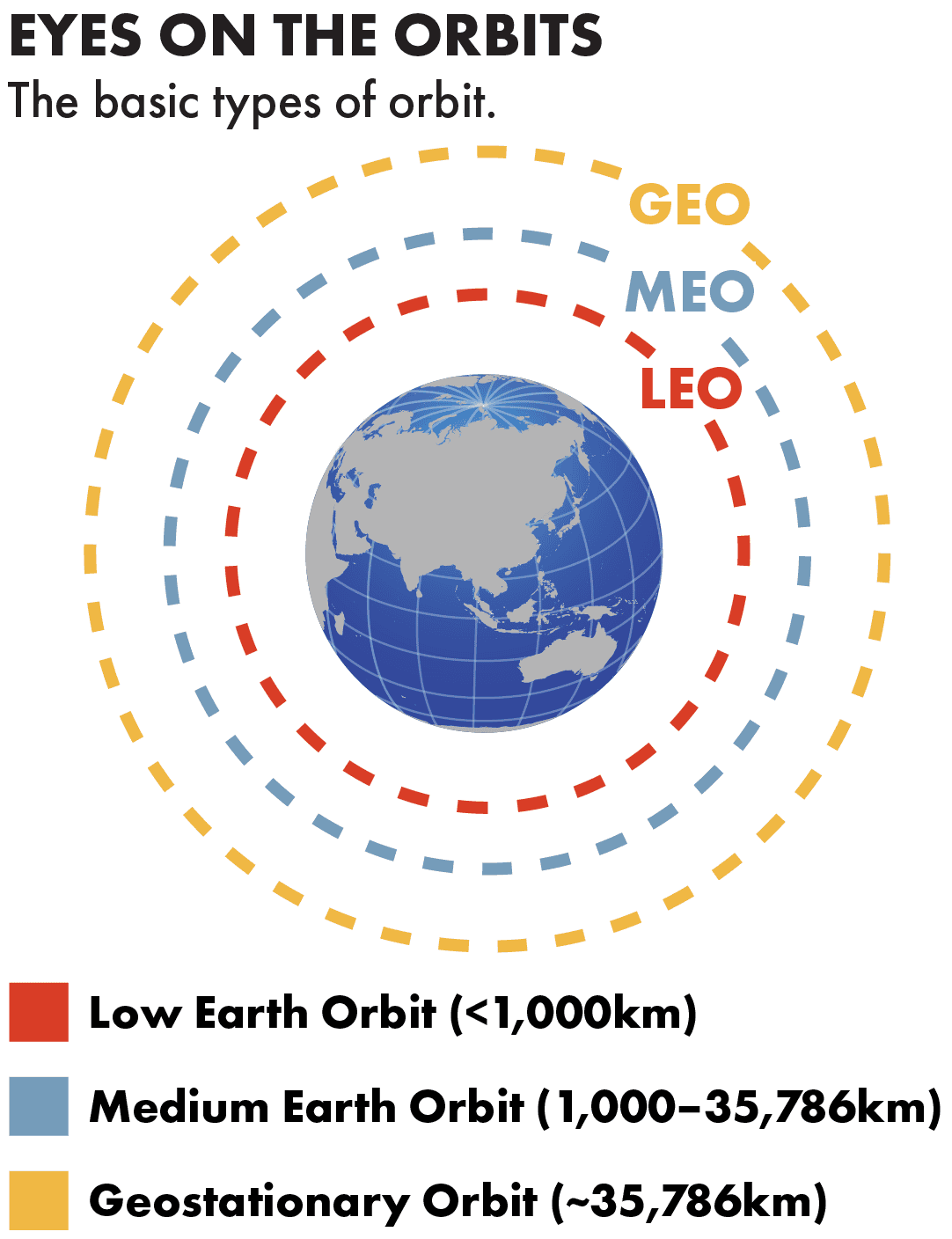

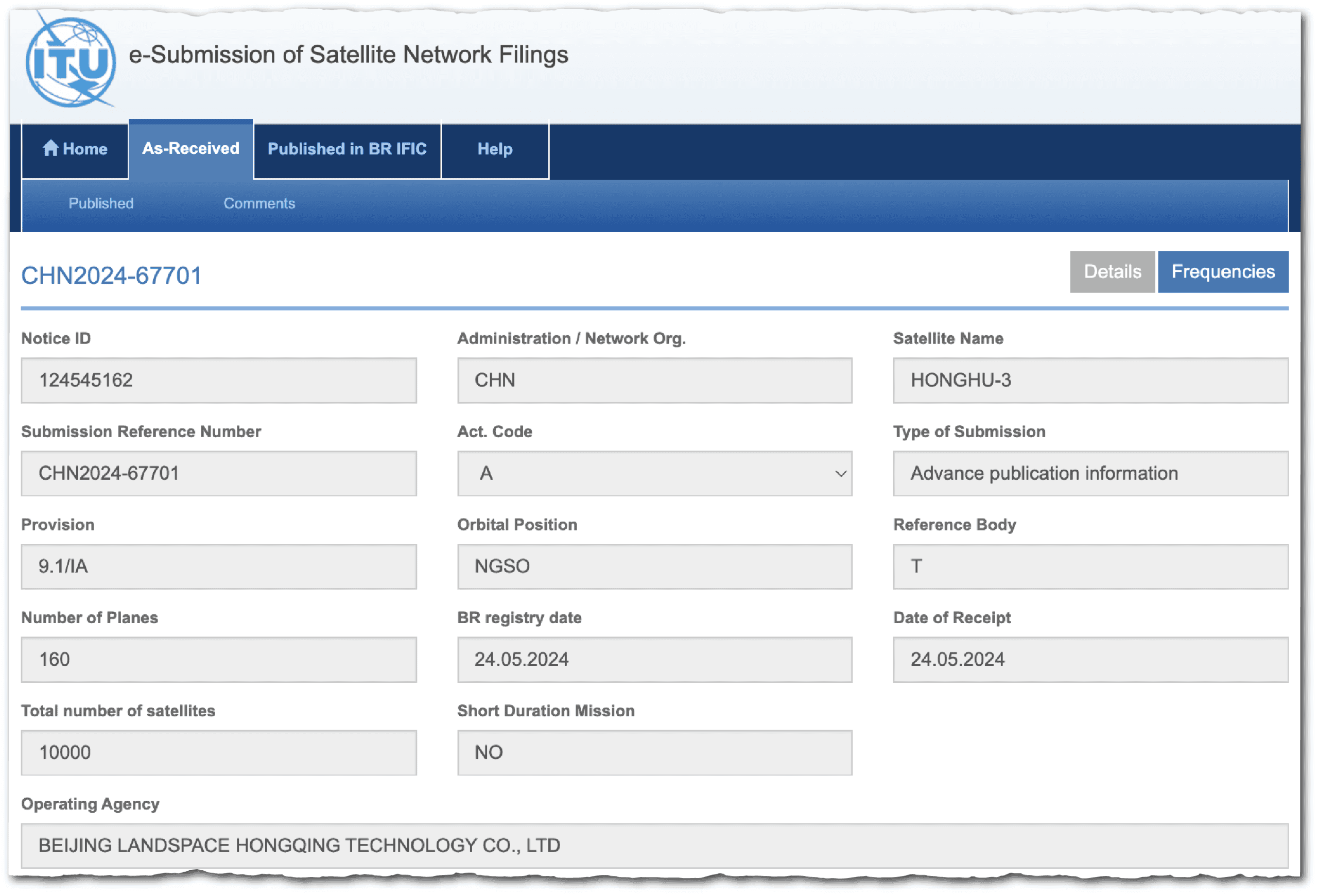

China has plans for several of these. The two most important are Guowang — a national project developed by CASIC starting in 2022 — and Thousand Sails (Qianfan), backed by the Shanghai municipal government. Both began launching in 2024, and Guowang leads with 154 satellites in orbit. Commercial companies also have plans for a third megaconstellation called Honghu-3 which has not yet begun launching.

These three projects — all in low Earth orbit — would provide global satellite internet coverage. Thousand Sails and Honghu-3 will function as commercial broadband providers. Because of the lack of transparency surrounding the size and design of Guowang satellites, some analysts believe they may have additional military applications.

China’s planned megaconstellations are “not purely to match what SpaceX is doing [with Starlink]”, says Gao. Beijing “has its own long-term military and economic goals”, she adds.

China filed its proposal for Guowang to the United Nations’ International Telecommunication Union in 2020. But the three megaconstellations became even more of a priority from 2022 onwards, when China saw how important Starlink was to Ukraine’s defense.

“We started to see them thinking: ‘holy cow, this is a strategically important piece of infrastructure’,” says Curcio.

For China’s commercial launch companies, the megaconstellations marked a “real turning point”, says Sénéchal-Perrouault.

“It’s the first big, almost guaranteed source of demand for these launch companies,” adds Curcio. “[The megaconstellations] totally changed the calculus for launch because it increased the market size for commercial medium launch vehicles that could send around 30 small satellites to orbit.”

If China does manage to deploy these three megaconstellations, Kong says they will enable “near-global, uninterrupted broadband coverage [with] very reliable, low latency links”.

LOOK TO THE SKY

China’s ambitious plans for satellite infrastructure go beyond communications, Kong adds, to include “smart-city” applications, drone operations and environmental monitoring.

Many different actors in China, including local governments and commercial companies, have plans to deploy or make use of satellites. Auto maker Geely has started launching its own Internet of Things satellite constellation — Geesatcom.

Stay on top of China news.

Join the thousands of policymakers and business leaders who rely on The Wire China.

Commercial company ADA Space is collaborating with Zhejiang Lab, backed by the provincial government, to build the “Three-Body Computing Constellation”. It ultimately aims to provide computing infrastructure in orbit, offering processing and analysis for satellite data, without needing to first send all the data down to Earth.

China also has plans to upgrade BeiDou — its equivalent to GPS used for navigation and timing — with three test satellites due to launch around 2027 and full deployment starting in 2029.

Starlink satellites over the Netherlands, May 24, 2019. Credit: Dr. Marco Langbroek

But to realise these lofty ambitions, China needs the launch capacity to put a huge number of satellites into orbit. Completing Guowang and Thousand Sails alone would require around 27,000 satellites.

“If we think about how big these constellation projects are, [China’s launch capacity] is not even close,” says Curcio.

In 2025 China hit a new record for satellites launched into orbit — but that record was still just 371. By comparison, SpaceX’s Starlink, the global leader accounting for 70 percent of launches, managed 3,169 last year.

While SOEs are boosting rocket production and unveiling new models, Curcio’s conservative estimate is that China will launch at least 500 satellites this year.

“China’s launch system — even with private rockets — cannot yet sustain the deployment tempo required,” says Gholap.

PUT UP OR SHUT UP

Low Earth orbit satellites also have limited lifespans. They eventually decay and re-enter the Earth’s atmosphere. Starlink’s satellites, for example, plummet towards the Earth after five years.

This means that satellites that cannot start operations until others have been launched end up wasting part of their lifespan before they can even begin service, notes Carlos Placido, an industry consultant based in Argentina.

International regulation adds further pressure. Plans have to be filed to, and be accepted by, the ITU before a satellite constellation can be launched. Satellites are given the right to operate in approved orbits and broadcast on certain radio frequency bands — so long as their operators meet certain deployment milestones.

If operators miss these deadlines, they may still be able to submit new filings and apply for extensions — but only up to a point. As Gholap puts it, “frequency rights are awarded on a use-it-or-lose-it basis”.

“You don’t automatically lose the spectrum but you have to prove you’re going to be using it, otherwise they may reallocate it elsewhere,” adds Victoria Samson, Chief Director of Space Security and Stability at SWF.

Chinese launchers don’t have access to the wider market for commercial addressability reasons. They cannot launch European constellations because of geopolitics and national preference

Alexandre Najjar, Manager and Space Industry Analyst at NovaSpace

The main challenge for commercial rocket firms is proving their reliability, especially if they want to win Thousand Sails and Guowang contracts.

LandSpace is cited by most analysts as the current industry leader. Chinese media reported in early January that the company had secured formal contracts to launch satellites for both Guowang and Thousand Sails.

Jack Congram, Editor of the China in Space Substack, says LandSpace’s track record has been successful enough that it “can go to regulators and say ‘our engines work, this propellant [fuel] mixture works — we can launch stuff’”.

The company’s reusable Zhuque-3 had a partially successful launch attempt in December. The rocket reached orbit, but the reusable first-stage crashed on the recovery pad rather than landing softly.

Gholap says that even so, the test was “widely viewed by industry observers as a meaningful — though incomplete — step toward Falcon-9-style reusability”, referring to SpaceX’s most frequently used rocket. Another test is planned for the second quarter of this year.

Other major companies such as Space Pioneer also expect to test reusable rockets this year.

LandSpace holds a 48 percent stake in Honghu-3, which should generate additional demand for its rockets. This vertically integrated approach seems to take inspiration from a certain successful American company.

But some analysts are still skeptical of the plan.

“LandSpace lacks the billions needed to invest in manufacturing and launch,” says Najjar. The company is currently aiming to raise RMB 7.5bn ($1.09bn) through an IPO on the Shanghai Stock Exchange.

There is also a question of whether there will be sufficient demand for Honghu-3, given the competition from Guowang and Thousand Sails. “It’s just not a very viable business model to begin with, to have a third constellation like this in China,” said Curcio.

Najjar agrees: “You don’t need three mega constellations to serve China and its allies.”

LandSpace did not reply to a request for comment.

“A STATE-DIRECTED CAPITAL ARCHITECTURE”

In November, the China National Space Administration (CNSA) released a plan to incorporate commercial spaceflight into its overall space development, including opening a new CNSA department for commercial space. The plan, according to Han, “elevates the importance of commercial space to a national level, with far-reaching implications”.

As policymakers have prioritised the sector, funding has soared.

According to Orbital Gateway Consulting, annual central government funding has doubled since 2022 to RMB 4.7bn, while investment from city and provincial governments has more than tripled to RMB 15.9bn.

“Most of that is provincial or city government money from big cities that are far behind [in developing a space industry],” says Curcio, who points to Chongqing as an example.

“China’s commercial space sector is not financed by conventional venture capital logic,” adds Gholap. “It is built through a state-directed capital architecture.”

Private sources still play some role, accounting for about 20 percent of total investment in the sector last year, according to Orbital Gateway Consulting. Rocket launch has been a core focus of this funding drive, rising 46 percent to RMB 8.6bn in 2025.

Commercial launch companies LandSpace and Space Pioneer both concluded bumper investment rounds in the second half of last year while Galactic Energy raised RMB 2.4 billion in September, the largest ever funding exercise by a Chinese rocket startup.

“I think that’s a response to central government policy,” said Andrew Jones, a space journalist. “They’ve designated commercial space as a national priority. I see the investment from those kinds of places following the central direction.”

Yang believes central government space policies have helped smooth relations between SOEs and private companies by promoting “more concrete measures for technology sharing”. These include opening up SOE-operated test facilities to private sector firms. Han agrees, noting that “talent flow and technological exchanges have increased”.

Meanwhile, other policies are helping to develop the sector further. “Post-2023 policies show a shift toward quality, safety and systemic support, with an increased emphasis on standardization, safety protocols and risk management,” says Yang.

Most of these commercial companies are going to ultimately need some kind of bailout or there’s going to have to be consolidation. Some might just die. And those that do consolidate will be the ones that have close relationships with provincial or city governments.

Blaine Curcio, founder of Orbital Gateway Consulting

Cheng adds that early worries the government would move to quash potential private-sector competition have subsided: “That’s really the dog that didn’t bark in this case: the state is not throwing this push towards the private sector into reverse.”

Launching rockets has become easier as China expands its infrastructure. China’s two leading launch sites for commercial firms — Jiuquan in Inner Mongolia and Wenchang in Hainan — are both growing. This year, Wenchang plans to add two more commercial launch pads to its existing two.

CHINA HAS CAUGHT UP WITH TESLA, IS SPACEX NEXT?

But the outlook for China’s many commercial launch companies remains uncertain. A key issue is that even with the megaconstellations offering a critical new source of demand, China has far too many rocket companies.

“Most of these commercial companies are going to ultimately need some kind of bailout or there’s going to have to be consolidation”, says Curcio. “Some might just die. And those that do consolidate will be the ones that have close relationships with provincial or city governments”.

“You might have a handful of companies which demonstrate that they can reliably get to orbit and launch often,” says Jones. “The ones that do that first will get contracts for Thousand Sails and for Guowang, and we’ll see those survive.

“You have so many [launch] companies, it’s looking like the [electric vehicle] market.”

But unlike China’s EV makers, many of whom were able to expand overseas, rocket companies have limited prospects when it comes to launching for foreign customers.

“Chinese launchers don’t have access to the wider market for commercial addressability reasons,” says Najjar. “They cannot launch European constellations because of geopolitics and national preference.”

Most developed countries already have — or are developing — their own sovereign launch capabilities. That leaves developing countries with very limited demand for launches, such as Pakistan or Venezuela, as potential customers.

“The best case scenario would be that, with so many [Chinese] satellites being launched, the commercial launch companies have the chance to win a lot of launches,” says Curcio. He adds they could be helped further by the “opening up of things like commercial cargo spacecraft or space tourism – that would create some real demand”.

The current moment may well be an inflection point for the leading rocket companies – before their launch rates start to take off.

Najjar adds that “in five to ten years, once the new Chinese rockets ramp up launch rates and the mega factories are fully operational, it’s possible that they can [achieve] super low manufacturing and launch costs.

“Should LandSpace succeed in reusability and in increasing their launch rates, we could have a Chinese SpaceX in a few years”.

Paddy Stephens is a freelance tech and energy journalist based in Taipei. He has written for The Economist, Financial Times, and Sinification newsletter, and is the author of The New Space Race Substack.