On one of the last days of 2023, Shanghai officials proudly unveiled what they believe to be a game changer in the ongoing space race with the United States: the new smart factory for Shanghai Gesi Aerospace Technology, also known as Genesat.

With the lights dimmed, a flat-panel satellite the size of a motorcycle appeared on the stage. Although it looked unremarkable — flimsy, even — the satellite had just rolled off the factory’s assembly line and represented a giant step forward in China’s quest to produce and launch satellites.

“It used to take two to three months to design and customize a satellite,” Cao Jin, the general manager of Genesat, boasted to the assembled crowd. “Now the factory can churn out a satellite every one and a half days and produce up to 300 a year.”

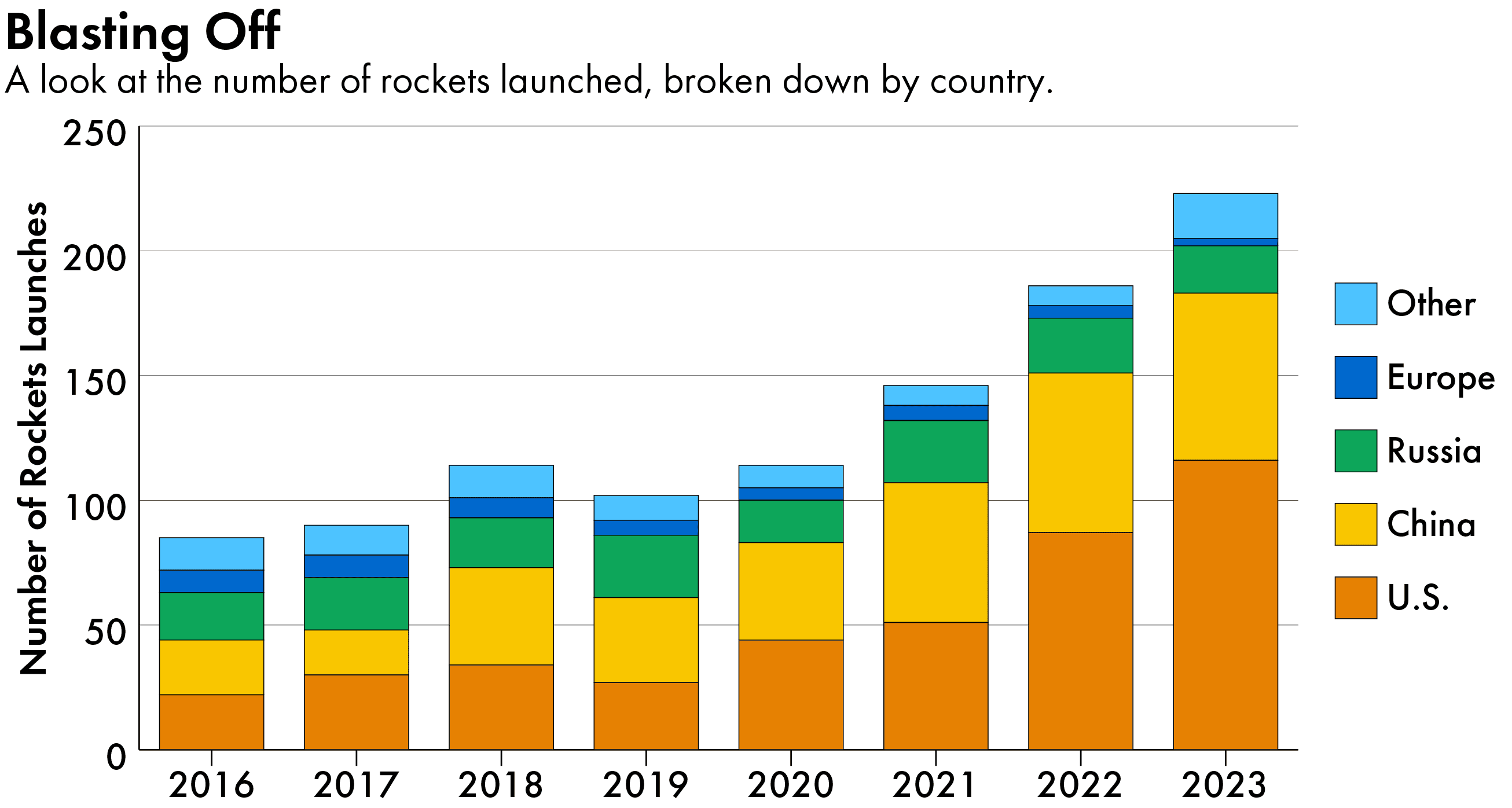

China needs every satellite it can get as it tries to catch up to Starlink, the network of over 6,000 satellites in low earth orbit launched by Elon Musk’s SpaceX. Starlink has plans to launch an astonishing 36,000 more in the next few years. All of China’s efforts together, by contrast, have launched just fewer than 200 satellites into low earth orbit, according to Novaspace, a market intelligence firm focused on the space and satellite sector — and most of them are for tech demonstration and earth observation, not telecoms.

But Beijing is determined to catch up. Starlink has proven itself as a core, 21st technology. It provides high-speed internet to 2.6 million customers across 72 countries, including in isolated regions such as the Arctic and Antarctica. And the mega-constellation has strategic and national security implications, as was proven when Ukraine’s military relied on it during the Russian invasion.

“For Beijing, it’s unthinkable that the United States should pursue the development of this extraordinary satellite constellation and that China would somehow not have an equivalent infrastructure that was domestically developed,” says Alanna Krolikowski, an assistant professor of political science at the Missouri University of Science and Technology.

Beijing, however, has been relatively late to the game. It identified the construction of satellite internet as a national priority in 2020, and a year later consolidated various initiatives to create Guowang, the presumed national champion. A planned mega-constellation of 13,000 satellites, Guowang is overseen by China Satellite Network Group (China SatNet), which is directly under the control of the State-owned Assets Supervision and Administration Commission (SASAC).

By forming a centrally-owned entity dedicated to the project, Beijing clearly hoped to accelerate development. But in the three years since, Guowang seems to have stalled. For starters, China SatNet was swept up in a round of disciplinary inspections last year as Beijing stepped up scrutiny of state-owned enterprises. Then, last July, it debuted its new headquarters in Xiong’an, a remote city that Chinese leader Xi Jinping has envisioned as an innovation hub but which now stands empty and is struggling to draw talents. In November, China sent an “experiment satellite” that was speculated to be a test launch for Guowang, but overall, there have been minimal updates on the project’s progress.

There could be several reasons for Guowang’s low profile, including the national security element of it. But the emergence of new players — like Genesat and its mass-produced satellites — also reflect a change in strategy on Beijing’s part.

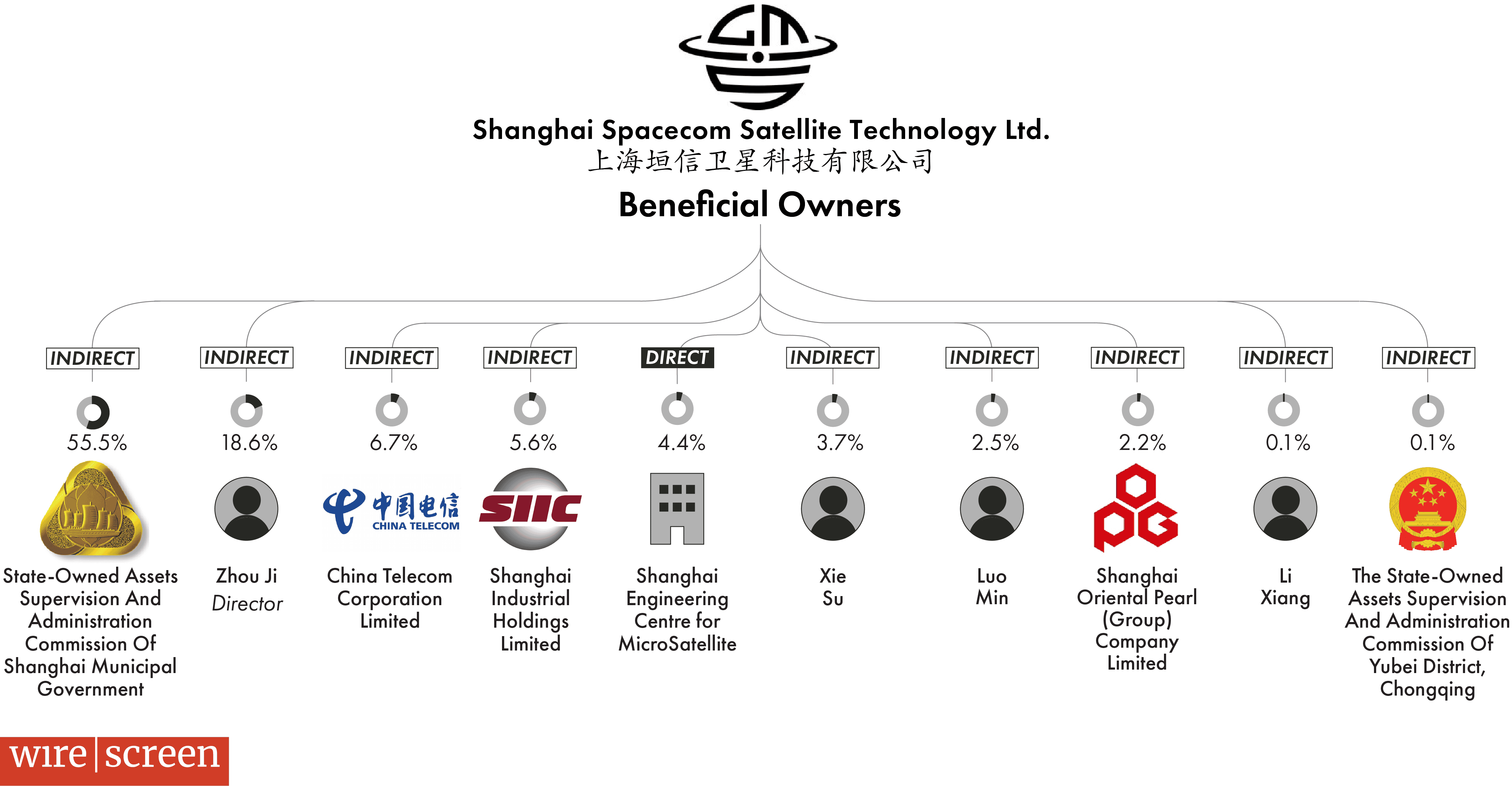

Indeed, the Shanghai municipal government surprised many observers last July when it first announced plans to develop another mega-constellation. Known as G60 Starlink and operated by the Shanghai Spacecom Satellite Technology (SSST), which partially owns Genesat, the constellation will consist of up to 12,000 satellites. Some 648 satellites will be deployed by the end of next year to provide regional coverage, a company executive said at a conference two weeks ago.

Although G60 Starlink is backed by the Shanghai government, it is only partially state-owned — which observers say represents a significant shift.

“There’s this assumption that [satellite internet] is a telecommunications project at the end of the day, so [in China] it is probably going to be centrally controlled,” says Blaine Curcio, founder of Orbital Gateway Consulting, a consulting firm focused on China’s space sector. “It would really only make sense to have one such project.”

For Beijing, it’s unthinkable that the United States should pursue the development of this extraordinary satellite constellation and that China would somehow not have an equivalent infrastructure that was domestically developed.

Alanna Krolikowski, an assistant professor of political science at the Missouri University of Science and Technology

But with Guowang’s progress potentially stalled, it looks like Beijing is placing a second bet.

“The appearance of G60 could possibly be the government saying, ‘We don’t want to take that risk ourselves with Guowang, let’s have the private sector do it if they want. They can fail, we can’t,’” says Alexandre Najjar, a managing consultant with Novaspace.

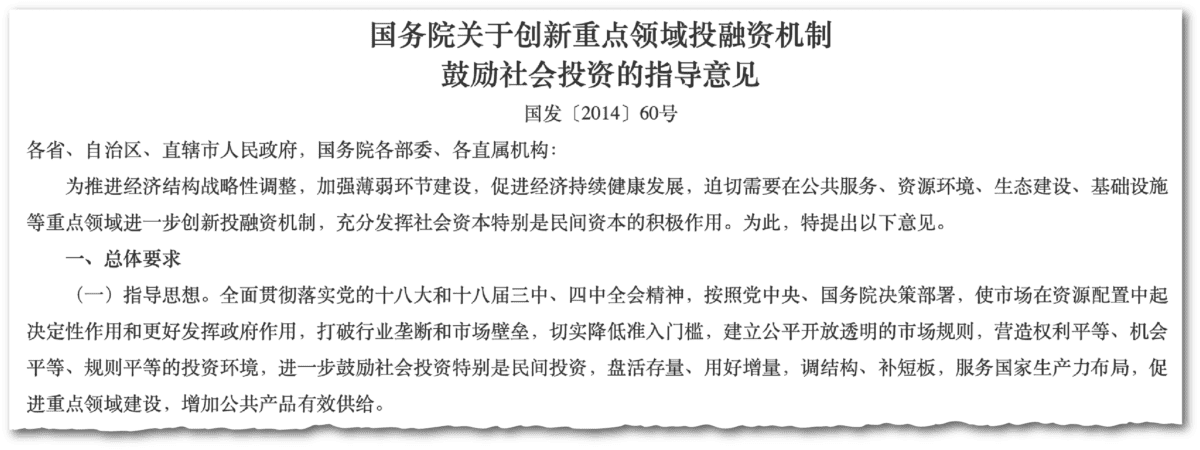

Up until a decade ago, China’s aerospace industry was dominated by two state-owned enterprises: China Aerospace Science and Industry Corporation (CASIC) and China Aerospace Science and Technology Corporation (CASC). That began to change in 2014, when China passed Document 60, which allowed private capital and companies to participate in civilian space infrastructure for the first time. In the years that followed, the central government issued a series of policies that gradually and cautiously opened up the sector.

But with the success story of SpaceX, which has transformed the U.S. space and defense industrial base, Beijing seems more ready to open the floodgates.

“If a government is going into space with taxpayers’ money, they had better not blow up that money,” Ji Wu, former director of the National Space Science Center at the Chinese Academy of Sciences, said in an interview in 2022. “Everything gets super complicated, and the costs keep going up. And the more expensive a project gets, the more afraid people become of failure. This vicious cycle will be there as long as space is done with government money.”

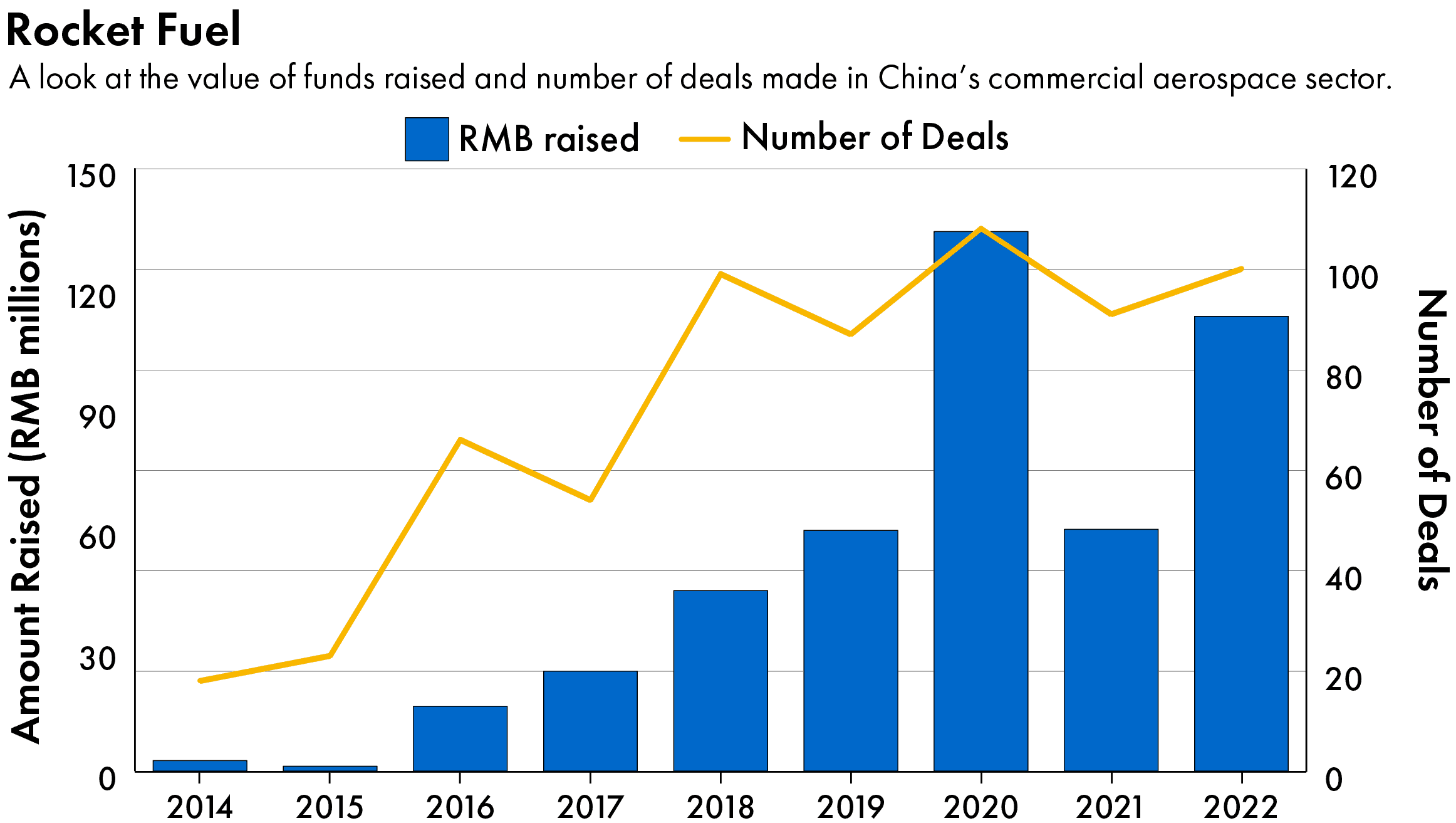

The private sector, by contrast, doesn’t seem afraid at all. In February, G60’s operator, SSST, raised a staggering $933 million from private as well as regional government-led investment funds; it was the largest round of funding by any Chinese commercial space company ever. The Shandong-based start-up Orienspace, which sent three satellites into orbit in January, went on to raise $83.5 million that same month. And last September, when the Beijing startup Galactic Energy became the first domestic private company to launch a rocket from the sea, it raised $154 million.

Overall, the amount of funds raised by Chinese commercial aerospace companies jumped from $262 million yuan ($36 million) in 2015 to $10.3 billion yuan ($1.42 billion) last year, according to the Beijing-based research firm Taibo Intelligence Unit. The industry is projected to reach 2.8 trillion yuan ($345 billion) by 2025 — more than double its size in 2020. (For comparison, the Chinese electric vehicle industry is estimated at $306 billion this year.)

The ecosystem in China is still fundamentally different from that in the United States, of course. In many cases, aerospace companies maintain strong ties to the government, are offshoots of Chinese state-owned enterprises or research institutions, or receive some form of state funding — such as Genesat or SSST. Others are founded by former employees of the state-owned enterprises who went it alone, such as Landspace, a rocket company that appears to be making plans for a mega-constellation as well.

While no private aerospace company in China will ever play the outsized role SpaceX does, the hope is that these startups could come to challenge state-owned enterprises — or at the very least, move faster than them.

“The state system has been there since the mid-fifties, and it’s a very established and powerful system traditionally,” says Wayne Shiong, a partner at China Growth Capital, a Beijing-based early stage tech venture capital firm that has invested in Landspace. “If we want to compete against that system, we have to build something really different.”

ROCKET SCIENCE

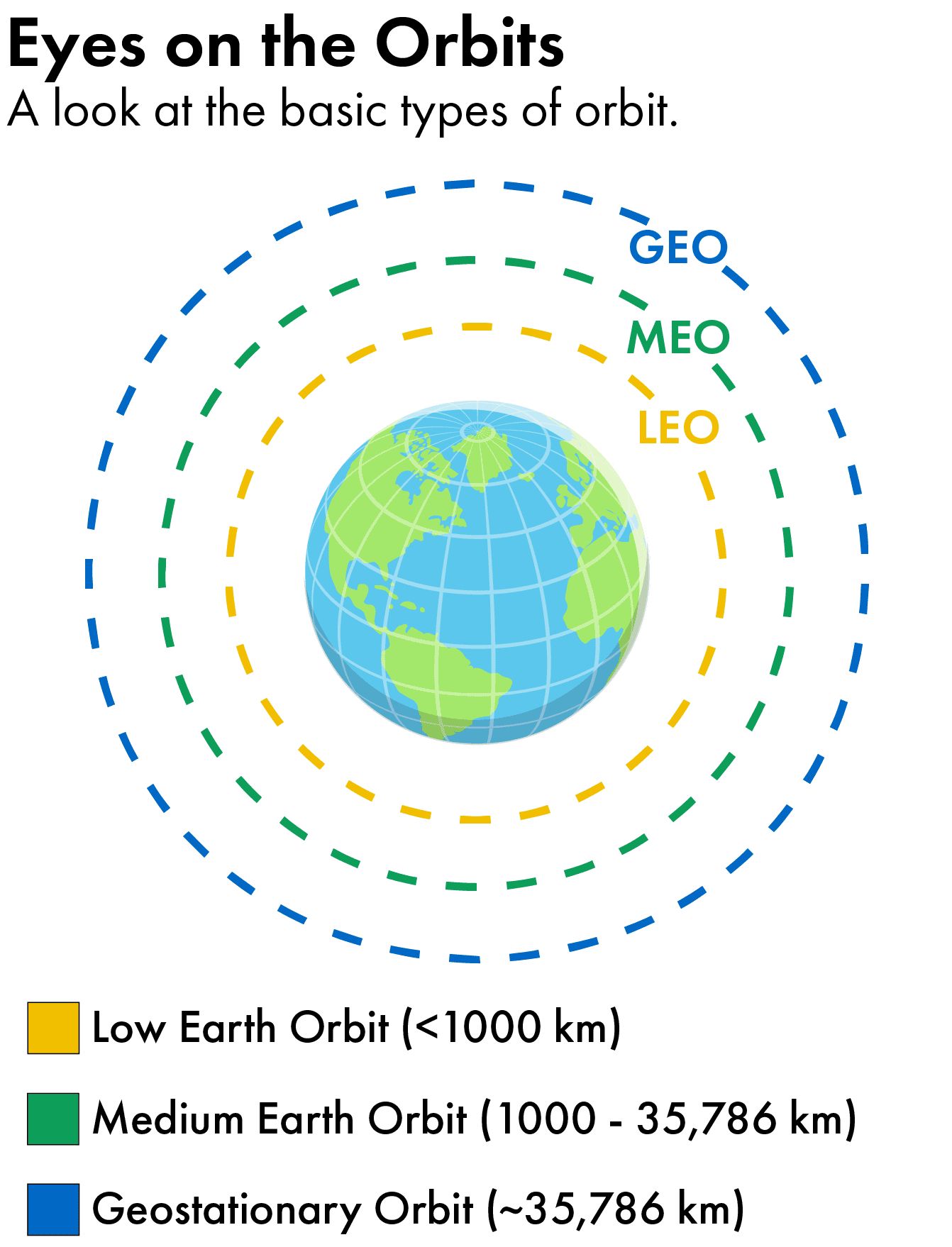

On the surface, it’s easy to see why low earth orbit is so attractive to both companies and investors. By not having to travel so far — geosynchronous orbit (GEO) is more than 30,000 kilometers farther out in space — LEO satellites have fewer delays and faster connection speeds. LEO can also be reached by smaller satellites, which use less fuel and are cheaper to launch.

But given that a LEO satellite can only observe a small area at any given time, continuous coverage requires far more of them spread across the domain — hence, the mega-constellation. And making a mega-constellation is no small feat.

Although Genesat’s manufacturing prowess will help supply China’s satellites, how they get launched into the sky remains a bit of a mystery. China’s rocket launch companies have yet to develop a reusable rocket, which SpaceX achieved in 2015 with the Falcon 9 and which is essential for reducing costs in the long run.

The final assembly of Landspace’s Zhuque-3 VTVL-1 reusable rocket, April 15, 2024. Credit: Landspace

Shiong, the venture capitalist, remains optimistic, however. Landspace, the rocket company his firm invested in, has developed the world’s first rocket powered by methane and liquid oxygen, a fuel that is more challenging to work with but potentially cleaner and cheaper. Although Landspace has yet to show a proven reusable rocket, Shiong points out that it took SpaceX five to six years to reach that milestone. If things go according to Landspace’s plan, the Chinese company may crack the same problem in 12 to 18 months.

“Landspace is basically trying to catch up with SpaceX through a better or more efficient engineering approach, which is a kind of easy card to play,” he says.

Or as Dai Zheng, a rocket designer at Landspace, put it in a recent interview with the Chinese state broadcaster: “We may be lagging behind. But we are running at a faster speed.”

In reality, how far ahead SpaceX is doesn’t really matter to companies like Landspace, since SpaceX and Starlink will likely never have access to the Chinese market. Given its aim for self-reliance in tech and its need to maintain control over information flows, Beijing has blocked out foreign players.

“China can never imagine using, hiring or paying SpaceX to launch any of its satellites. It has to develop its own rocket businesses,” says Shiong. “The bigger the pressure from geopolitical tensions, the better for the Chinese technology sector.”

But while Chinese aerospace companies have some time to catch up to SpaceX, a more vexing challenge for them is figuring out how to actually make a return on their investment.

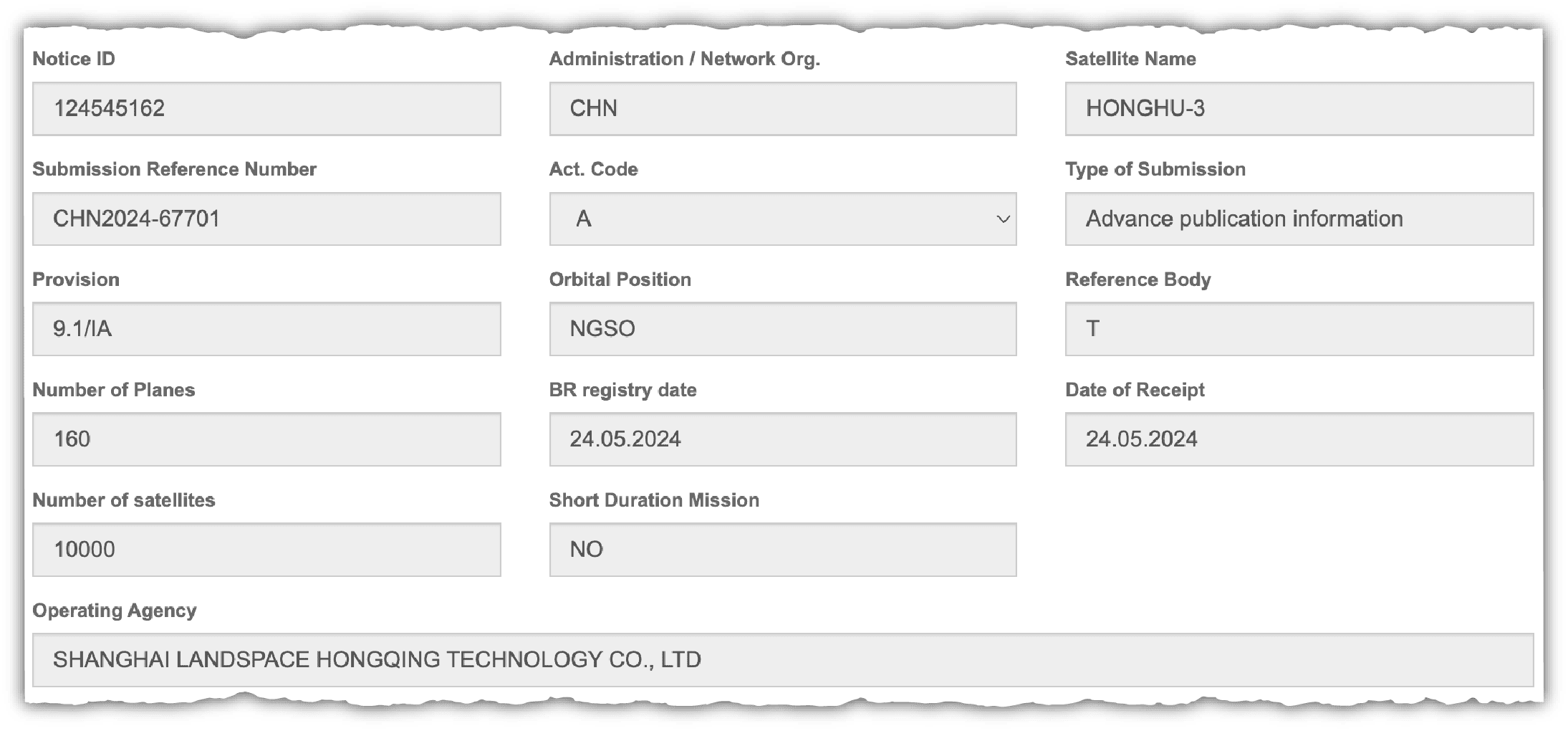

Last week, Shanghai Landspace Hongqing Technology, a company partially owned by Landspace, filed a notice with the International Telecommunications Union (ITU) for a new constellation, named Honghu-3, that consists of 10,000 satellites. By branching out into satellite operation, the rocket company is taking a page from SpaceX’s playbook, but it’s also a risky bet.

“In theory, it’s good to be vertically integrated to minimize launch costs. But in reality, it’s another story,” says Najjar, of Novaspace. “Landspace still needs billions to fund its constellation, and its launch business has yet to become profitable.”

Curcio, of Orbital Gateway Consulting, notes that while Beijing’s new private sector approach to its aerospace industry may help it move the needle on innovation, it could be that private actors get stuck holding the bag.

“There is likely going to be a Chinese mega-constellation deployed sooner than would have previously been the case,” he says. “But I’m not sure [these companies] realize what they’ve signed up for and the cash furnace this really is.”

Indeed, the business model of a LEO broadband system is notoriously unforgiving. Deploying an operational LEO satellite constellation runs between $5 to $10 billion, according to McKinsey’s estimates from 2020. LEO satellites have shorter lifetimes of five to seven years, which adds another $1 to $2 billion in annual maintenance and replacement costs. And while the risk and upfront investment are high, the profit margins are slim and the customer demand uncertain.

AN OVERVIEW OF CURRENT CONSTELLATIONS

| OPERATOR | SpaceX | Shanghai Spacecom Satellite Technology (SSST), aka Yuanxin Satellite | China Satellite Network Group, aka China SatNet | Shanghai Landspace Hongqing Technology |

|---|---|---|---|---|

| NAME OF CONSTELLATION | Starlink | G60 Starlink | Guowang | Honghu-3 |

| TOTAL NUMBER OF SATELLITES PLANNED | 42,000 | Around 12,000 | Around 13,000 | 10,000 |

| CURRENT STATUS | Over 6,000 in orbit | None in orbit so far. 648 satellites to be deployed by the end of 2025 | Several prototypes launched. To deploy 10 percent of the satellites in the next five years | None in orbit so far. |

Starlink, for instance, had only a million active subscribers by the end of 2022 — far fewer than the 22 million it had predicted. The satellite internet business didn’t break even until last November.

When China’s mega-constellations finally come on line, many observers note, it’s likely the centrally-owned Guowang will have an initial monopoly on the Chinese market — pushing out private competitor constellations like G60 and Honghu-3.

There is likely going to be a Chinese mega-constellation deployed sooner than would have previously been the case. But I’m not sure [these companies] realize what they’ve signed up for and the cash furnace this really is.

Blaine Curcio, founder of Orbital Gateway Consulting

“[G60] is moving fast, but it is primarily a provincial level initiative with some support from the central government,” says Ian Christensen, a senior director at Secure World Foundation, a private foundation that promotes space sustainability. “A national initiative like Guowang would enjoy a bit of an advantage.”

The next question for Chinese mega-constellations, then, will be if they are able to capture any international market share. “It’s not clear who is going to pay for [China’s] broadband services beyond the domestic market, as at least Western countries are going to be concerned about data security,” says James Clay Moltz, a professor at the Naval Postgraduate School in California.

SSST has experienced this firsthand. By being late to the LEO game, China missed out on the rush a decade ago to obtain spectrum rights from the ITU, the United Nations body that allocates these rights on a first-come, first-served basis. In 2022, SSST tried to acquire the German firm Kleo Connect and the spectrum rights it owns via a Chinese consortium, after a joint venture fell apart. But the efforts were blocked by the German government last year on national security grounds.

Although the fight is still dragging on in German courts, it doesn’t bode well for SSST. Without those precious orbital spots, G60 will have to resort to frequency bands that put them at a technical disadvantage.

Chinese constellations, however, might have an advantage in the global South, where Beijing has already made digital inroads through the Belt and Road Initiative. The Zimbabwe government, for instance, said in January it was considering services by G60 in addition to SpaceX’s Starlink.

“They’re not just competing on capability and cost,” says Nicholas Eftimiades, a senior fellow with the Atlantic Council and a former senior intelligence official. Space information services, he notes, have also been packaged into the Belt and Road Initiative, which means Chinese constellations “have mechanisms to ensure market share.”

But despite the size of the offline population in developing countries — and thus the potential of these emerging markets — the current price of satellite broadband may limit adoption. Starting at $120 per month, Starlink costs several times more than regular fiber optic. “The willingness to pay from the targeted consumers in Latin America or Africa is much lower than in the U.S.,” Najjar points out.

In other words, even though Chinese commercial aerospace companies are “running at a faster speed,” it’s not entirely clear what their destination is. Last year, in a rather desperate attempt to figure out a sales strategy, Commsat, a leading satellite developer, put several satellites that cost up to $4.22 million on sale on Taobao, China’s Amazon. One of the advertised applications was taking “selfies from space.”

“Selling satellites on an e-commerce platform is a forward-looking experiment,” Xie Tao, the president of Commsat, told the Global Times. Part of the experiment’s goal, he said, was “discovering customers.”

CROWDED ORBIT

Although the profitability of China’s private space industry remains uncertain, what is fairly certain is that China will be adding thousands of satellites to low earth orbit in the near future. And as the area gets more crowded, many in the space community fear there will be increased potential for the Kessler Syndrome: a nightmare scenario in which there is so much junk floating in space that a collision may initiate a massive chain reaction, sending debris everywhere and eventually making the entire domain unusable.

So far, large constellations have strengthened space deterrence. For starters, direct attacks, like anti-satellite missiles, are no longer effective against a constellation of thousands. And, as Moltz notes, “all sides have strong interests in preventing conflict and associated debris cascades, which could harm everyone’s space assets.”

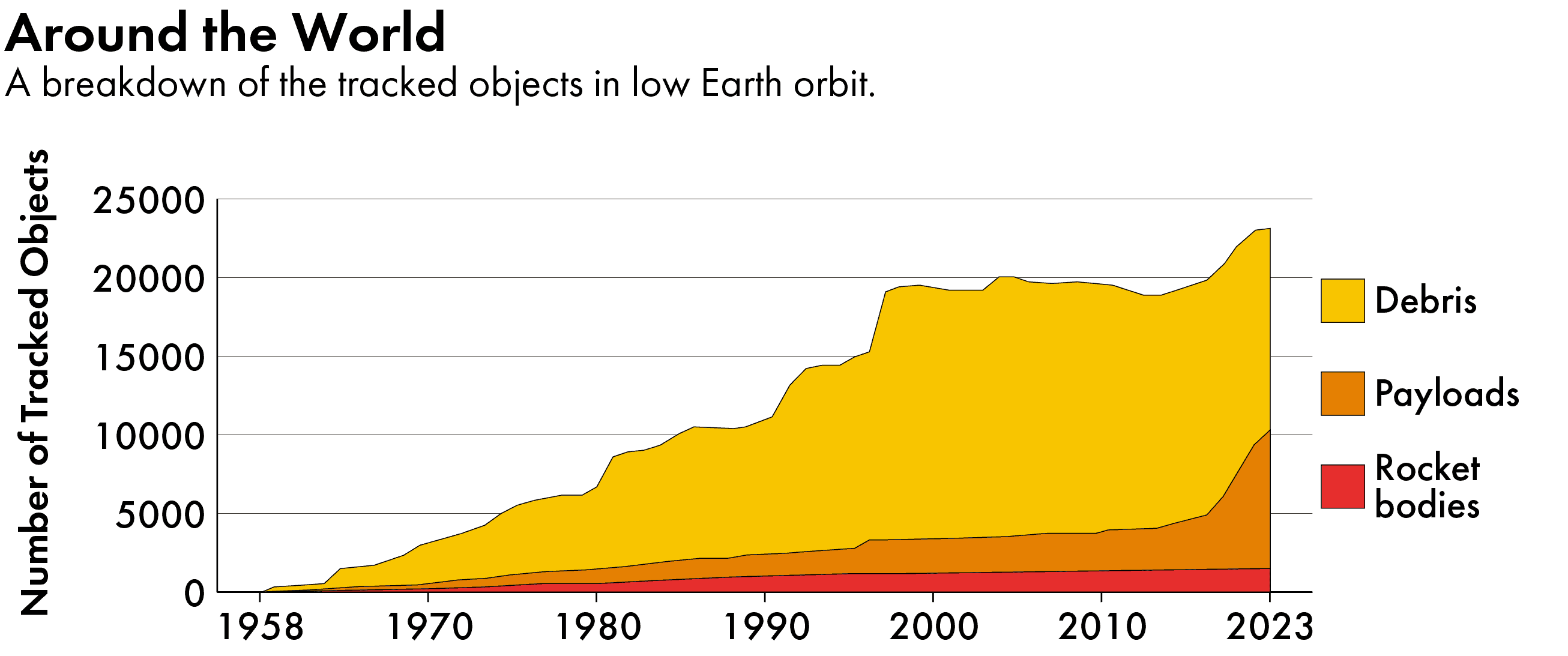

But as satellites proliferate, so does the risk of collisions, intentional or otherwise. According to a recent report by the U.S.-based space tracking firm Slingshot Aerospace, the total number of spacecraft in orbit reached 12,597 by the end of December. Driven by Starlink’s deployment, 2,877 satellites were added in 2023 alone.

While the ITU performs some form of space traffic coordination by regulating spectrum rights, there is currently no international system that manages space traffic. Instead, avoiding potential clashes in space often relies on a decidedly old school method.

“You pick up the phone, call the other operator, and say, ‘who’s gonna move?’” says Juliana Suess, a research analyst on space security at the Royal United Services Institute, a think-tank in Britain. “Which is tricky, because ultimately, no one wants to move as moving means expending fuel.”

There can also be disagreements over whether a move is necessary at all.

“There is potential for miscommunication,” says Benjamin Silverstein, a former research analyst for the Space Project at the Carnegie Endowment for International Peace, who notes that the methods and standards for analyzing potential collision courses are different for each entity, as is the risk tolerance.

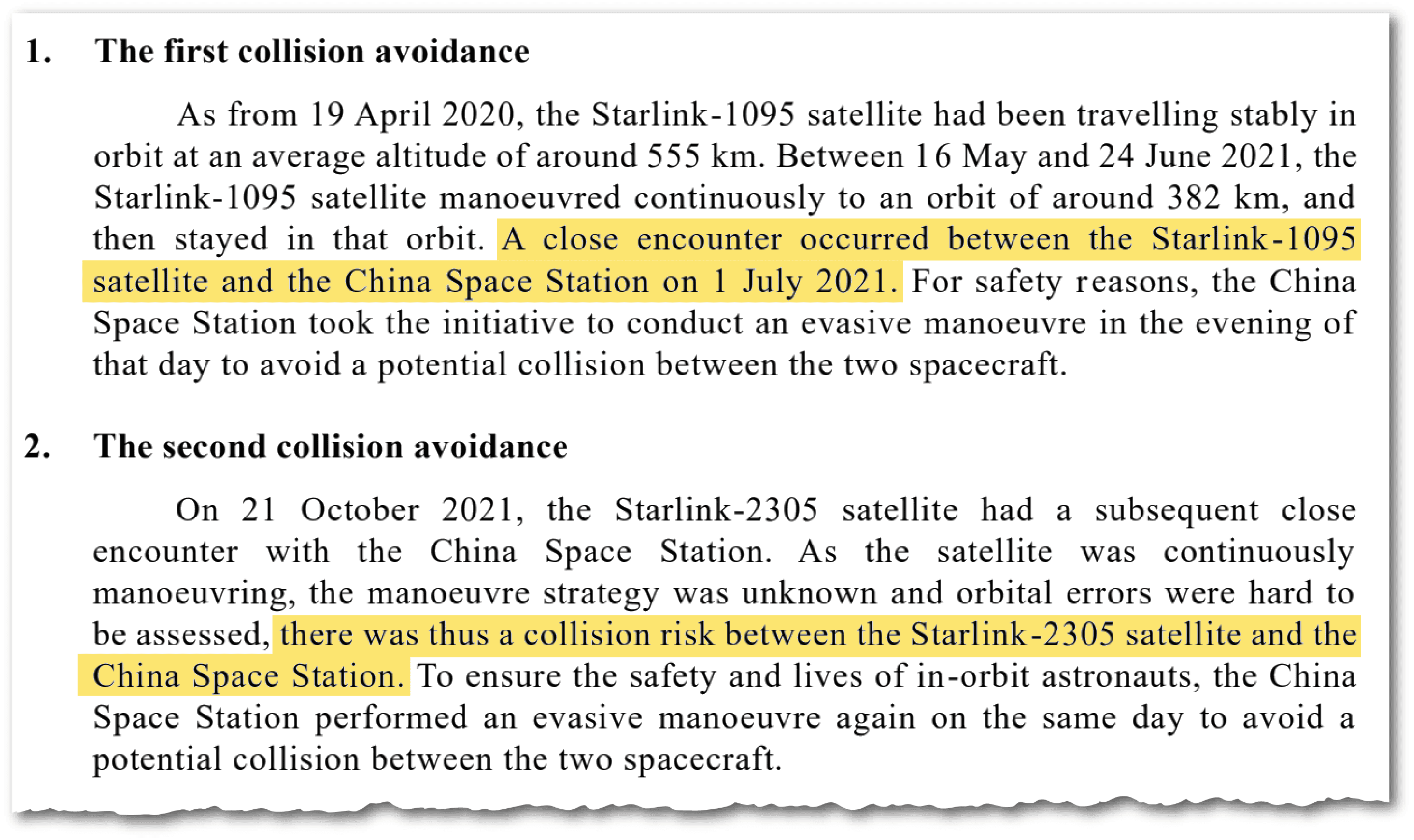

In 2021, for instance, China complained to the United Nations that two Starlink satellites had had two separate “close encounters” with the Chinese Space Station, forcing the station to dodge. The U.S., however, maintained that the U.S. Space Command didn’t see “a significant probability of collision” in those instances.

The U.N., meanwhile, didn’t do anything since such disputes are outside its purview.

“As we enter this new space era, the growing congestion makes that really an untenable approach for the long term,” says Bruce McClintock, a senior policy researcher who leads the Space Enterprise Initiative at RAND. “Currently there is no tiebreaker or referee or international organization that exists to decide who gets to arbitrate in those situations who should move, and then in the eventual case of a collision, who’s liable?”

That is not a popular sentiment with a lot of states, McClintock adds, as they would prefer to maintain their independence. But it’s a reality that countries, especially leading space powers, will have to confront if they want to protect their space assets. And that includes China whose satellites will soon dot the sky.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.