The U.S. and China are on a collision course over an overlooked part of the semiconductor supply chain. But unlike cutting-edge chips — which the U.S. still dominates — this time, America is playing defense.

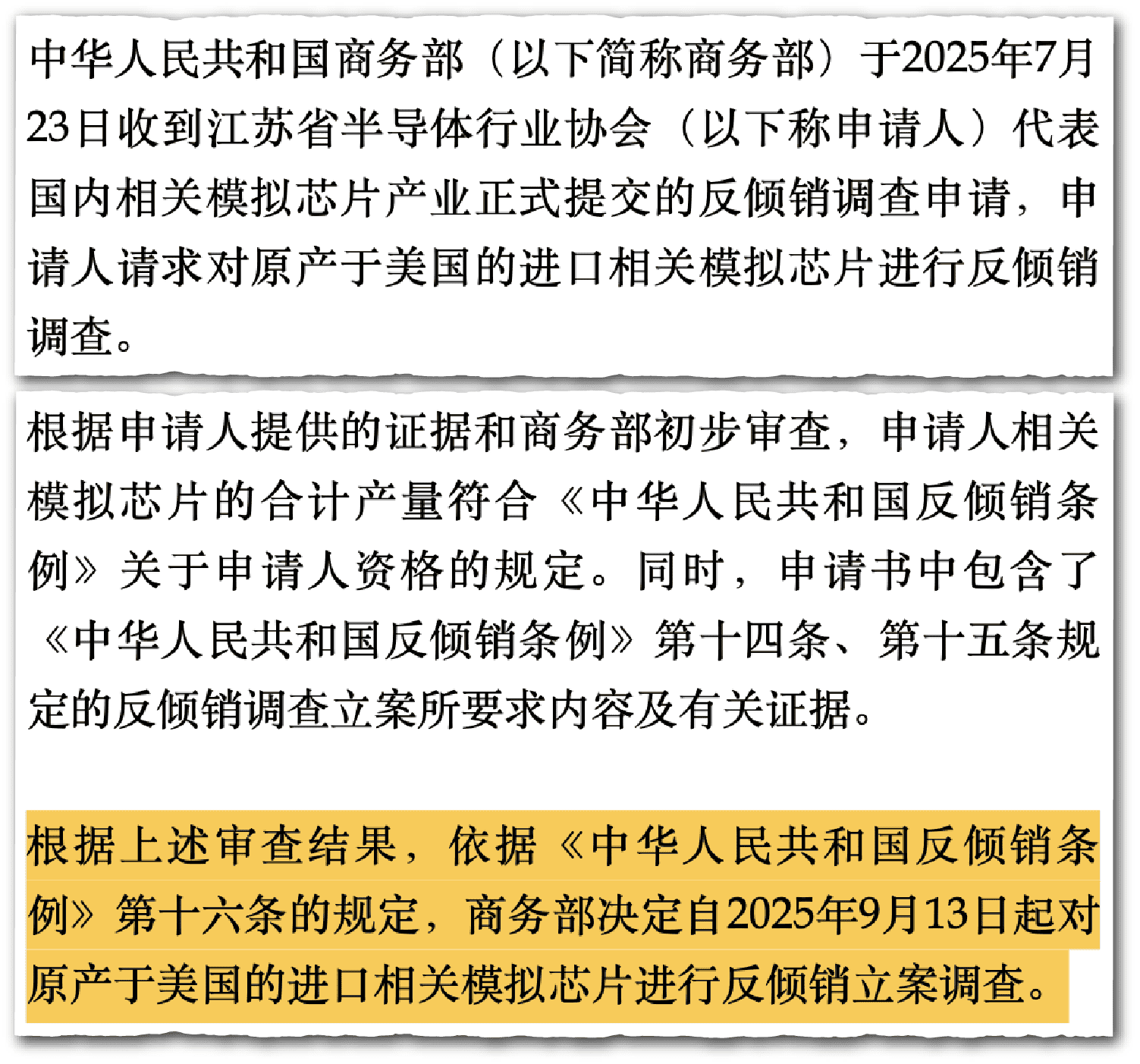

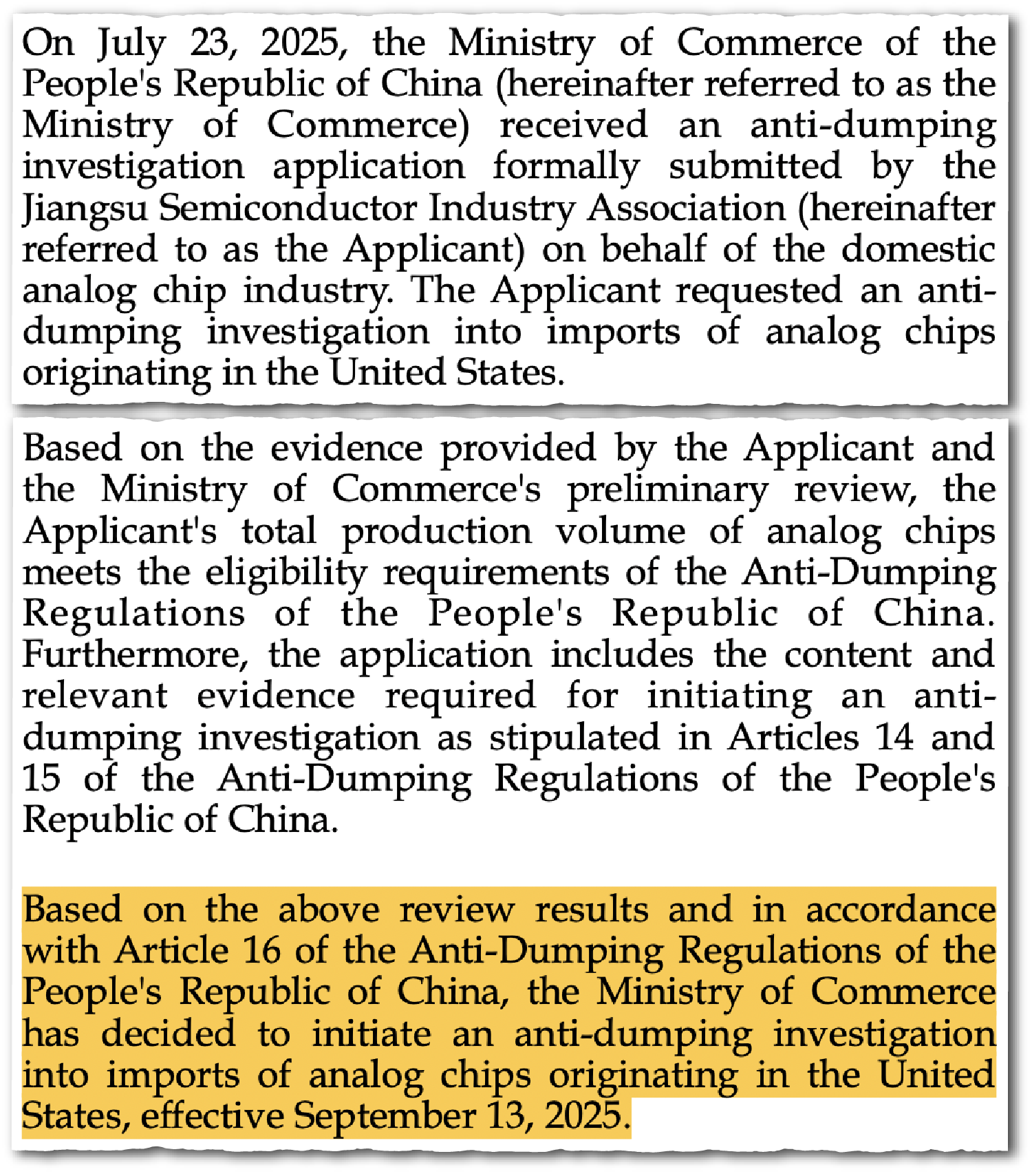

Last month, China’s Ministry of Commerce announced a probe into allegations that the U.S. is dumping legacy chips in the Chinese market. The move appears to be retaliatory after Washington launched its own trade and national security probes targeting Chinese chips in December 2024 and April of this year.

Legacy chips is a term used to describe older, more mature semiconductor technologies. The name is somewhat of a misnomer: while technically less sophisticated than the cutting edge hardware put into smartphones and AI chips, these chips are essential components to everyday electronics from TVs to refrigerators.

Over the last decade, China’s chip fabs have been aggressively expanding their output of legacy (also known as ‘foundational’) chips, part of the country’s all-out effort to become a leader in semiconductor manufacturing. That has triggered alarm bells in Washington and European capitals about growing dependence on Chinese chips, and overcapacity in the global market.

What to do about it, however, is a vexing question. Thanks to China’s position as the world’s factory, America will have a harder time compelling manufacturers to give up Chinese legacy chips than China will have in keeping America’s out. And in imposing trade barriers, U.S. policymakers face a real risk that China retaliates and stops buying chips from Western competitors like Texas Instruments and Analog Devices.

“It’s a hard problem,” says Chris McGuire, a former White House official who helped to design the Biden administration’s chip export controls. “The decision involves tradeoffs, which people don’t like to make. But not making a decision is also a decision. The longer we wait the more painful it gets.”

Part of the problem is that lots of manufacturers don’t even know where their chips come from. Even some defence manufacturers probably have no idea to this day whether they’re using Chinese chips.

Michael Kuiken, a commissioner on the U.S.-China Security and Economic Review Commission

Roughly 60 percent of global chipmaking capacity goes to producing legacy chips, according to the Semiconductor Industry Association. Chinese fabs, including Hua Hong and Semiconductor Manufacturing International Corp (SMIC), make up an increasingly large share of that market. From 2015 to 2023, China’s share of global legacy chip production soared from 17 to 31 percent, according to a report by Rhodium Group last year. More recent data from Rhodium shows China’s share has leaped to 40 percent in the third quarter of 2025, an expansion rate that has blown past analysts’ projections.

Some see the increasing ubiquity of Chinese chips in daily life as a potential security risk.

“Part of the problem is that lots of manufacturers don’t even know where their chips come from,” says Michael Kuiken, a commissioner on the U.S.-China Security and Economic Review Commission. “Even some defence manufacturers probably have no idea to this day whether they’re using Chinese chips.”

A 2024 survey of U.S. industry by the Commerce Department found that 44 percent of companies couldn’t determine if their products contained Chinese-made chips: Because legacy chips are often intermediate products built into other goods, customers often don’t have insight into where the chips are fabricated. It also estimated that most products in the defense industrial base likely contain at least one Chinese-origin chip. In April, the Trump administration launched a Section 232 investigation, looking into the national security risks of America’s dependence on chip imports.

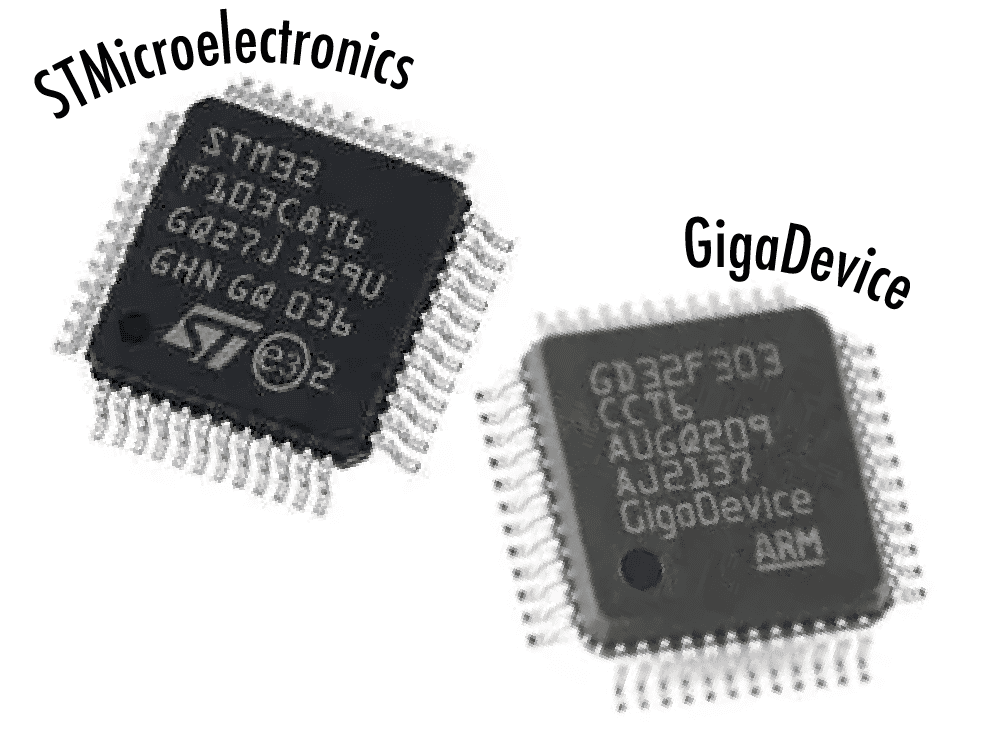

Politicians also have economic concerns. Aided by state subsidies, Chinese chipmakers have consistently been able to price their wares 20 to 30 percent below equivalent offerings from Western competitors, according to a 2023 report by Silverado Policy Accelerator, a Washington think tank founded by Dmitri Alperovitch. In one case, a chip from Chinese firm GigaDevice was priced at one quarter that of a comparable product by Switzerland’s STMicroelectronics.

All of that is squeezing the profits of Western legacy chipmakers like STMicro, Texas Instruments (TI) and Massachusetts-based Analog Devices. Many are already recording fewer sales from Chinese customers: from 2022 to 2024, Analog Devices’ China revenue fell 17 percent; TI’s fell 37 percent.

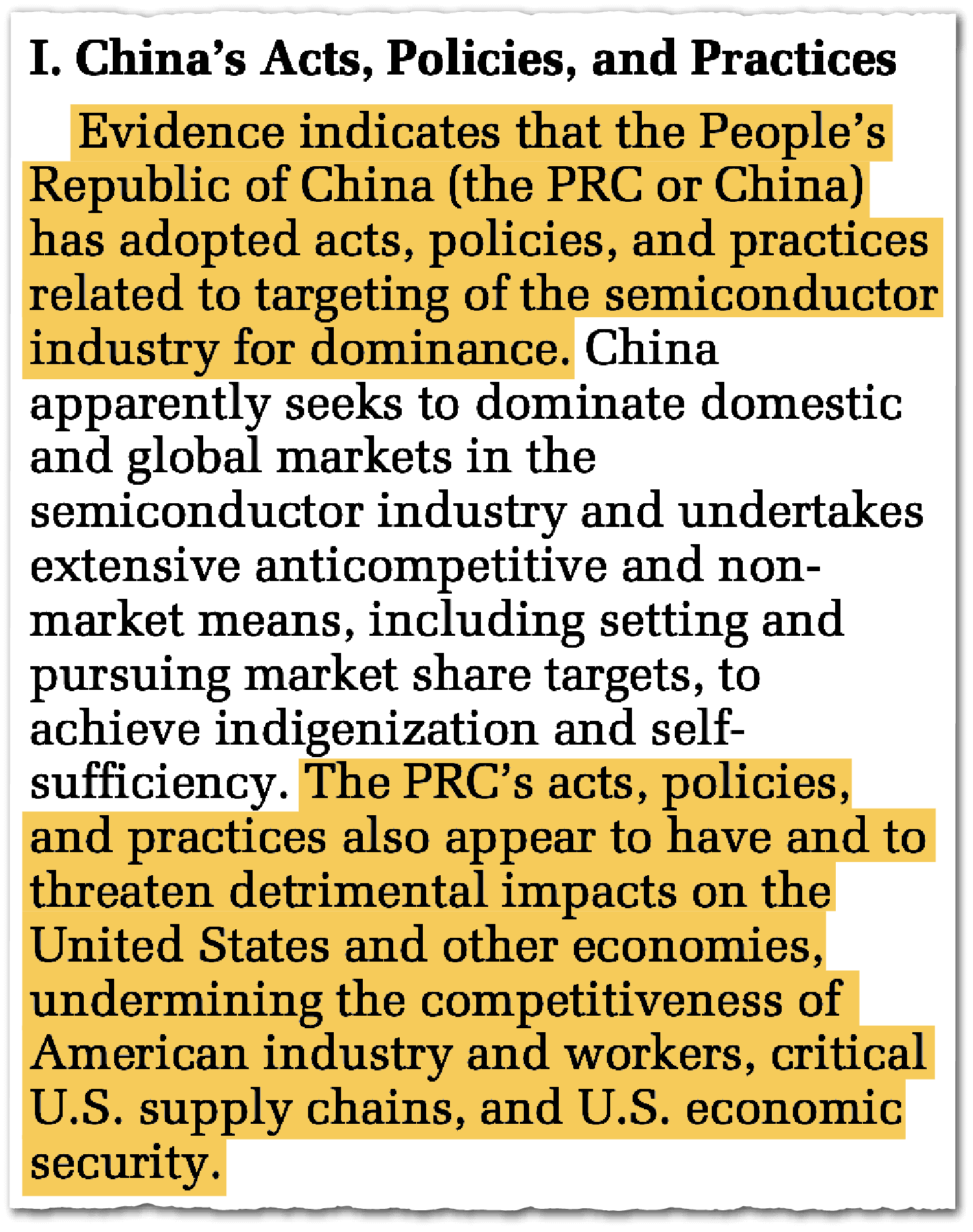

Last December, the Biden administration launched a Section 301 investigation — carried on under the Trump administration — into China’s “targeting of the semiconductor industry for dominance.” But not all analysts are sure that China’s legacy chip expansion is creating overcapacity. The ambiguity may not deter Trump officials, who have wielded tariffs aggressively, but it could stop the EU, another major market, from taking equivalent action to protect its legacy chip sector.

A major reason for the uncertainty is that it’s hard to calculate the global demand for legacy chips.

“A lot of it is about looking at China’s future demand, to what degree China is going to absorb the increase in supply, and what is the remainder that will spill into global markets,” says Reva Goujon, a director at Rhodium. “Isolating domestic demand… is very difficult. But it needs to happen, given Europe’s conservative approach to any sort of preemptive restrictions.”

A finding from the 301 investigation that China is flooding the market could be used to justify Washington imposing steep tariffs or an import ban on Chinese legacy chips, and even final products that contain them.

But such trade restrictions would be hard to execute, not to mention politically risky. The ubiquity of Chinese legacy chips means any restriction would inflict widespread pain on consumers in the form of higher prices. Moreover, many Chinese chips are assembled and inserted into final products abroad, meaning any tariffs would have to encompass goods made globally.

Restrictions could also invite retaliation from China, which is now examining whether to impose its own ‘anti-dumping’ tariffs on U.S. legacy chips. Chinese trade restrictions could hasten the decline of Western legacy chipmakers by closing off what remains one of their largest markets.

And with so much electronics manufacturing happening in China itself, Washington will likely have a hard time compelling factories there to give up Chinese legacy chips — especially if Beijing’s trade restrictions make alternatives harder to acquire.

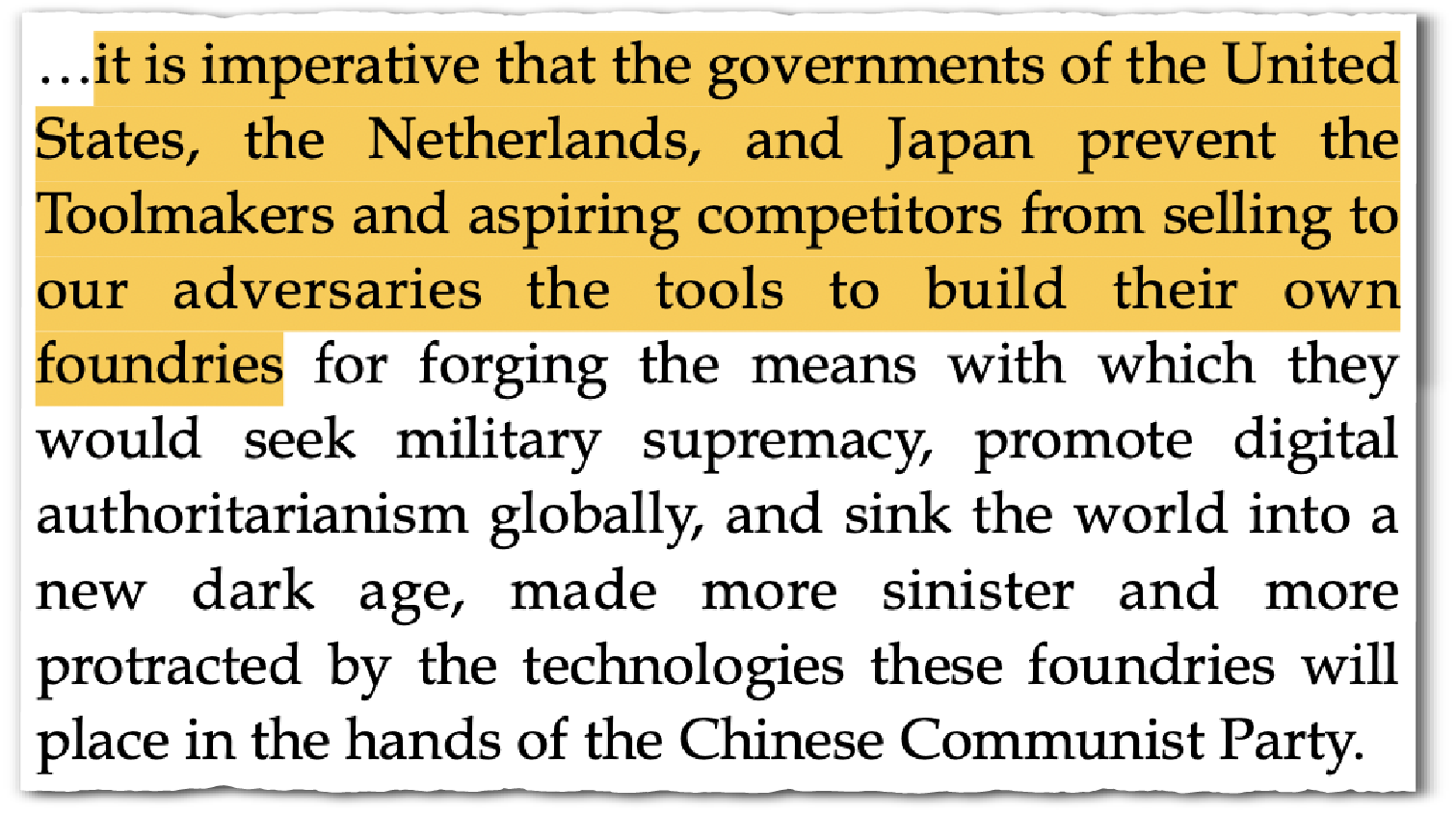

Some policymakers advocate a third approach: export controls to slow the buildout of China’s legacy chip factories.

A new report by the House China Select Committee this week highlighted Chinese fabs’ heavy reliance on chipmaking equipment made by five foreign toolmakers, which include The Netherlands’ ASML, California-based Applied Materials and Japan’s Tokyo Electron. Since 2022, Chinese purchases of toolmaking equipment have increased by 66 percent, the report found.

Any new controls that would cut into sales by U.S. firms of manufacturing equipment for mature nodes would further undercut leading U.S. technology companies’ ability to generate revenue from equipment that has been fully amortized in terms of R&D.

Paul Triolo, partner at DGA-Albright Stonebridge Group

“Without the U.S. and its allies’ equipment, they would struggle tremendously,” says McGuire.

He agrees with one of the report’s recommendations that the U.S. should broaden its chipmaking tool ban. “It’s the only way to prevent diversion of that equipment for advanced production, and would have the secondary benefit of being an enormous help to the legacy chip problem,” he says.

Export controls are likely only a stopgap, however, given China’s heavy investments and advances in developing its own chipmaking equipment, particularly for less advanced chips.

“Any new controls that would cut into sales by U.S. firms of manufacturing equipment for mature nodes would further undercut leading U.S. technology companies’ ability to generate revenue from equipment that has been fully amortized in terms of R&D,” says Paul Triolo, partner at DGA-Albright Stonebridge Group. “This critical source of revenue is what allows U.S. technology leaders in the tool space to continue to fund R&D and innovation.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen

{kind=link}