While humanoid robots have been capturing the headlines and imagination, a quiet automation revolution has been taking place in households and businesses.

Across China and elsewhere, autonomous machines are now delivering meals in restaurants and scrubbing floors in train stations, malls, and office lobbies. In suburban homes, robots are mowing lawns and cleaning pools. In 2024, nearly 20 million of such service robots were sold to consumers worldwide and another 200,000 units to businesses, according to the International Federation of Robotics (IFR). The global market, per one estimate, could grow from $26 billion in 2025 to $132 billion by 2034.

Roborock’s Saros Z70 vacuum is equipped with a mechanical arm. Credit: Roborock

As with industrial robots and humanoids, Chinese companies have captured a large share of this booming sector.

But that surface success has come with some familiar issues. At home, Chinese service robot makers are struggling to make money as they cut prices to gain market share. Overseas, their low-cost products are gaining ground at the expense of domestic competitors — stirring some concern from policy makers.

“If you can only compete by lowering the price, that’s going to be a very tough business,” said Tencent executive Dowson Tong at a recent conference in Hong Kong, when asked about how Chinese robotic companies can avoid a price war. “Only the companies who have many different competitive advantages added together will eventually become the final winners”.

As in areas like electric vehicles and chipmaking, government signaling and support has been crucial to the service robot industry’s development. Beijing identified robotics as a key area in the Made in China 2025 blueprint introduced over a decade ago to guide Chinese manufacturing. The state has lent further support by directing capital to these priority sectors, including via a national fund worth 1 trillion yuan ($138 billion) set up last March.

Robot making companies have piled in. The result: last year, China produced 18.6 million service robots, a 16 percent increase year-on-year, per new data from the National Bureau of Statistics.

Similar to electric vehicles and consumer electronics, China’s edge in robotics lies in its extensive and efficient supply chains, and low production costs.

Many have sustained huge losses as a result of a subsidy war. Prosperity exists only on paper, as the machines have yet to demonstrate the practicality and cost-effectiveness touted by their advocates.

Ni Tao, a Shanghai-based tech analyst

Unlike industrial robots, service robots do not require the most advanced chips or AI models, and are relatively easy to manufacture, says Shengyun Lu, founder of the Shanghai-based LSY Consulting. Startups can readily find suppliers in the manufacturing hub of Shenzhen to build prototypes in small batches, and then figure out what sells through trial and error. “It doesn’t cost a lot in China to fail,” Lu says.

Yet profitability has been harder to come by.

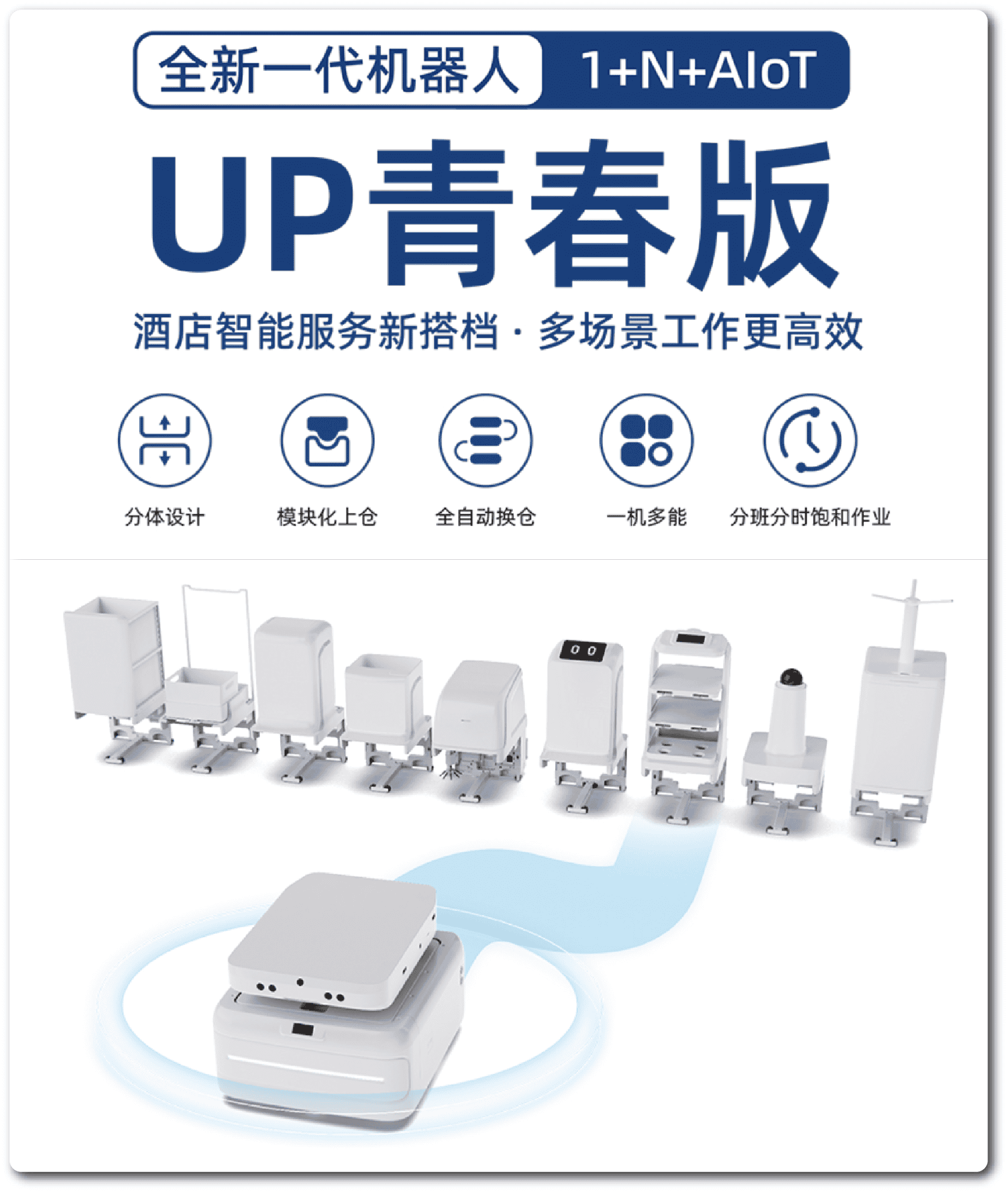

Take Yunji Technology, a Beijing-based company that went public in Hong Kong last October. The firm, whose machines serve over 34,000 hotels across China, is the market leader for service robots in the hospitality industry. Even so, it has accumulated losses of nearly 1.5 billion yuan ($212 million) since 2022, according to its listing prospectus. The average price of its newest series, the UP — multi-functional robots that can clean, patrol, and deliver goods — tumbled by around two-thirds in the first five months of 2025, down to to 17,000 yuan ($2,450) per robot from nearly 50,000 yuan ($7,200) the year before.

Shenzhen-based Pudu Robotics, a leader in catering robots, has burned through the more than $200 million of the funding it raised from the likes of Tencent, Meituan, and Sequoia Capital China, per Pitchbook, but has yet to break even since it was founded in 2016. Its rival, the Shanghai-based Keenon Robotics, has also struggled to stay afloat over the years and has relied on drastic cost-cutting to survive.

Experts say that while service robots are supposed to be cheap replacements for human workers, they often still fall short in terms of both functionality and cost. Customizing robots for different business scenarios can be expensive too, further narrowing profit margins. Producers have often had to offer unsustainable discounts on their products to attract buyers.

“Many have sustained huge losses as a result of a subsidy war,” says Ni Tao, a Shanghai-based tech analyst. “Prosperity exists only on paper, as the machines have yet to demonstrate the practicality and cost-effectiveness touted by their advocates.”

More recently, Chinese companies have turned to foreign markets in search of growth and greater pricing power.

Thanks to its foreign expansion, Pudu doubled its overall sales last year, for example. Three-fifths of its cleaning robots, the PUDU CC1, were shipped to North America and Europe, where they are deployed in nursing homes and supermarkets. The company is preparing for an initial public offering in Hong Kong, its founder confirmed to Nikkei Asia in December.

Keenon partnered with Japanese conglomerate SoftBank in 2021 to target the service industry in Japan: by last year, half of its revenue was coming from overseas. The company now holds forty percent of the food delivery market globally in 2024, according to IDC, a market research firm.

Despite such successes, players in this sector are still barely making profits, according to industry insiders. For one thing, Chinese producers have simply ended up exporting their domestic price competition as they expand overseas.

And while Chinese businesses may be content to deploy a robot simply because it is cheap, foreign clients tend to require more proof that they are safe and reliable. Some are also concerned about data security and privacy, given that the robots are equipped with cameras, sensors, and mapping tools.

Within the service robot sector, Chinese producers that make robots targeted at consumers rather than businesses are faring better, as household robots are easier to make and sell at scale.

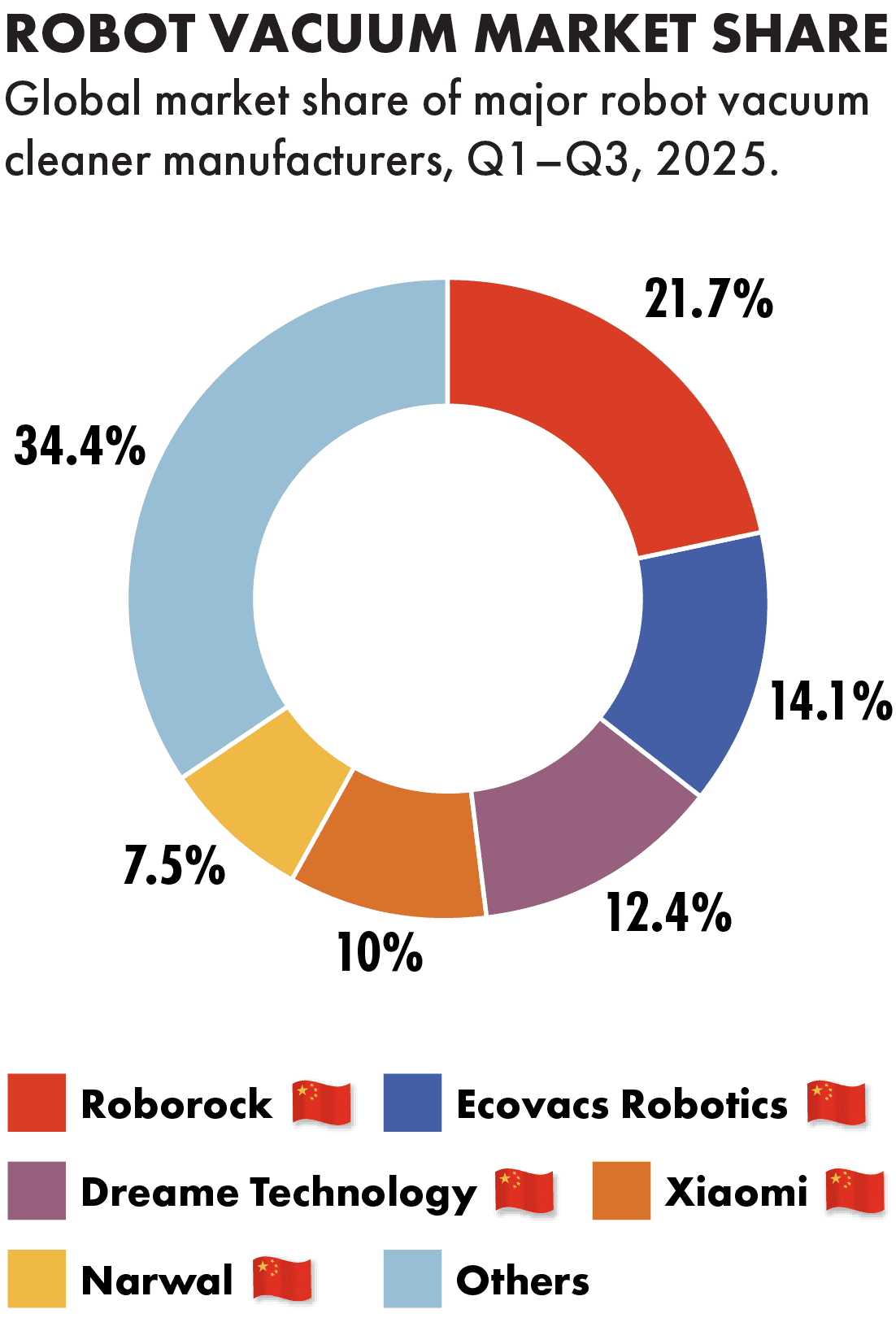

Take robotic vacuum cleaners: the top five sellers, which hoovered up two-thirds of the global market in the first three quarters of last year, are all Chinese companies, according to IDC. They include Xiaomi, the tech giant whose products range from smartphones to EVs, and the Beijing-based Roborock.

Such companies are not stopping at vacuum cleaners. In September, Roborock debuted a lawnmower equipped with the same Lidar technology used in EVs, which helps it to better identify obstacles. Others are moving beyond robots: Suzhou-based Dreame last month introduced new products such as a television with built-in sound bar, and even a sports car.

As Chinese robot makers gain global market share, their next challenge could be political.

In November, the European Commission launched an anti-dumping investigation into robotic lawnmowers from China, following complaints from the Husqvarna Group, a Swedish manufacturer of outdoor power products, which alleged that Chinese companies are benefiting unfairly from state support.

Still, any protectionist measures imposed may not do much to help European firms like Husqvarna. Chinese companies could absorb tariffs of up to 20 percent and still maintain their price advantage, says Georg Stieler, head of Robotics and Automation at Stieler Technology & Marketing Consulting.

Meanwhile, iRobot, the American company behind the first robotic vacuum cleaner Roomba, filed for bankruptcy in December, after losing ground to Chinese companies in recent years.

Chief executive Gary Cohen has admitted in media interviews that the company has failed to innovate. But speaking on the podcast Hard Fork, the firm’s founder Colin Angle blamed its troubles on an unlevel playing field as Chinese companies have access to “a protected market to cut [their] teeth.”

As part of the restructuring, iRobot is set to be acquired by its Chinese supplier Picea Robotics — a deal that is now being reviewed by the Committee on Foreign Investment in the United States (CFIUS). The committee’s main considerations will likely be whether the deal could involve a tech transfer to the Chinese military, and the effect on U.S. supply chains, says Jim Secreto, a former national security official with the Biden administration.

If everybody has the same hardware, then it is the ‘brain’ that is going to differentiate a company. The West will be able to find its openings and carve out a healthy section [of the market].

Aaron Prather, director of robotics at ASTM International

Secreto notes growing concerns in Washington about whether the U.S. can compete with China in robotics. “But as far as I’m aware, iRobot wasn’t making autonomous dog drones with guns on them,” he says. “If the tech isn’t super advanced and there isn’t a really serious supply chain argument…it’s hard to see the deal getting blocked.”

Pudu’s BellaBot service robot at work in an Austrian restaurant. Credit: Pudu Robotics

Some argue it is not too late for Western companies to make a comeback in service robots. The next phase of global competition will not be about making the cheapest robots, they argue, but smarter ones with new use cases.

“Future growth will be driven by deeper technology, stronger scenario fit, and operational capabilities rather than volume alone,” says Lily Li, a research manager for emerging technologies in IDC China.

The U.S. and Europe, for instance, can lean on their strengths in software to build superior products. “If everybody has the same hardware, then it is the ‘brain’ that is going to differentiate a company,” says Aaron Prather, director of robotics at ASTM International, a nonprofit that develops industry standards. “The West will be able to find its openings and carve out a healthy section [of the market].”

Noah Berman contributed reporting.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.