In December 2020, as the first year of the Covid-19 pandemic drew to a close, Chen Derong wiped away tears of joy while addressing the company he chairs, China Baowu Steel Group Corporation.1Baowu is the result of a consolidation of the steel industry with Baosteel and Wuhan Iron & Steel merging, along with Ma Steel. State-owned Baowu had just cracked a major milestone: It had churned out its 100 millionth tonne of steel that year, cementing its lead as the world’s largest steel producer. Chen, a former engineer, reportedly called it a “dream come true.”

In a year when the pandemic slowed global steel output, Baowu was thriving. Beijing had wheeled out its stimulus playbook, announcing government spending plans worth hundreds of billion dollars and looser borrowing requirements for local governments, with both measures supercharging steel-hungry infrastructure investment. Baowu finished the year with over $100 billion in revenue — a 22 percent year-on-year increase. By comparison, European conglomerate ArcelorMittal, the world’s second largest steelmaker, saw sales drop to around $53 billion, a nearly 25 percent decrease on 2019 levels.

Steelmaking is not exactly a sexy industry, like electric vehicles or artificial intelligence. But no other sector has quite embodied China’s rise from a poverty-stricken agrarian state to a modern industrial powerhouse. Indeed, for better or worse, steel has long been central to Beijing’s economic model: Mao Zedong’s obsession with steel underpinned the failed Great Leap Forward. Deng Xiaoping’s reforms, meanwhile, ushered in steel-fuelled economic growth, and ever since, steel titans like Baowu have quite literally undergirded decades of China’s rise.

As recently as 2020, China’s steel industry — like its economy — was in gloating mode after a stronger-than-expected bounce back from the pandemic. As Baowu’s corporate social responsibility report said after the company’s “glorious achievement” of 100 million tonnes, Baowu was set “to cast dreams for a century.”

But shortly thereafter came a tectonic shift in China’s economic outlook, and the long-revered steel industry began to wobble and then shake.

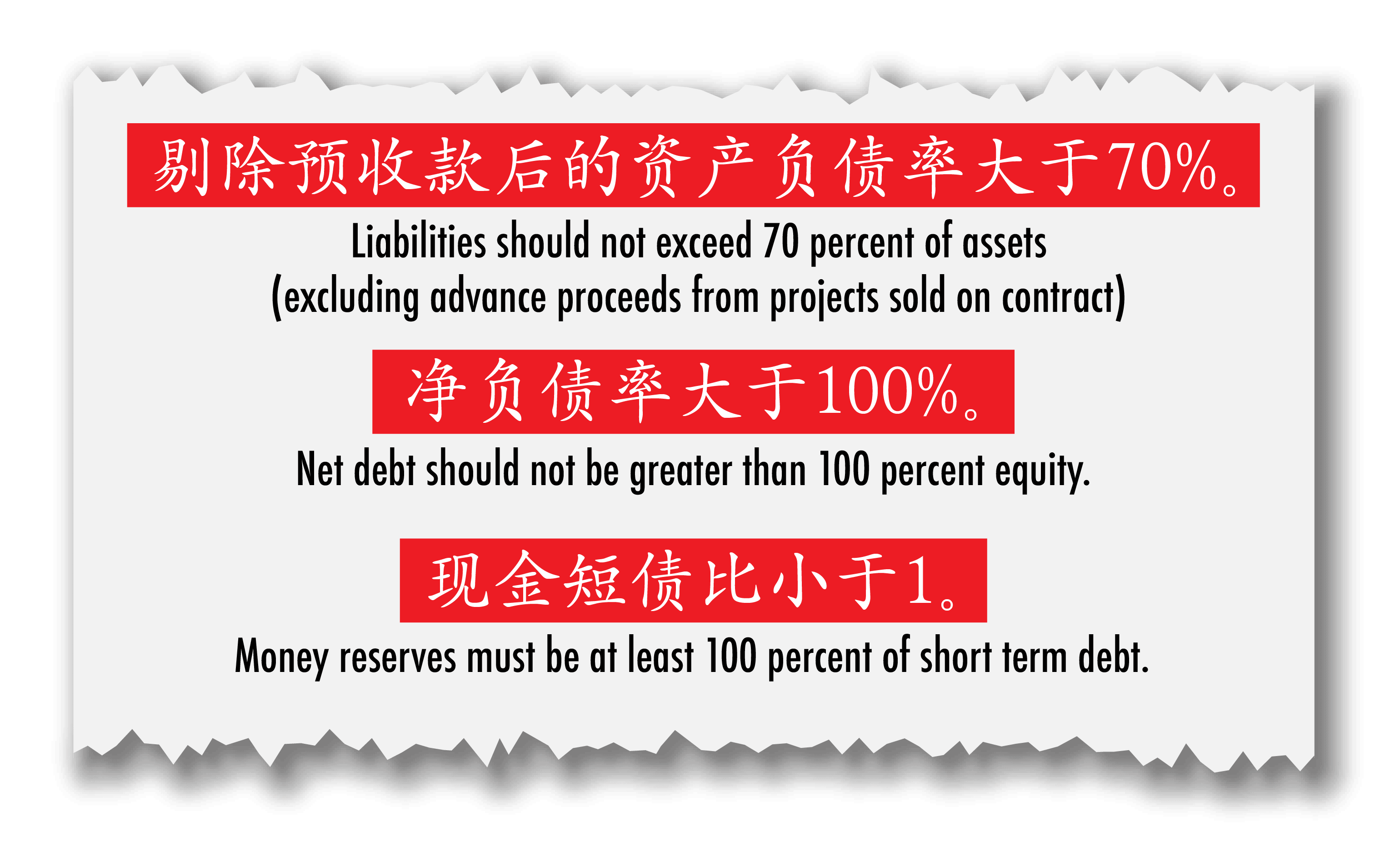

In August 2020, China’s economic regulators issued the so-called ‘Three Red Lines’ policy, which imposed restrictions on how much debt the country’s buccaneering property developers could carry. Up to this point, developers had grown accustomed to demanding prepayments from homebuyers, which they used to purchase ever more land. Historically, this worked, with sky-high demand for housing ensuring the developers remained flush with cash to meet their obligations. But it has long been clear to many that the model was unsustainable.

“Property developers were running a Ponzi scheme,” says Nancy Qian, an expert in the Chinese economy at Kellogg School of Management at Northwestern University, adding that the practice wasn’t illicit. “Developers can only keep doing that as long as there are more people buying the next round of housing. It’s easy in the beginning when everyone needs housing, but at some point it’s going to stop.”

Seeing the writing on the wall, Beijing intervened. Evergrande, the country’s largest developer, soon spiraled into a liquidity crisis, before eventually defaulting on its bond obligations in December 2021. Other firms followed suit. According to BondEValue, an information service, Chinese developers failed to meet $37 billion in debt obligations between January and August 2022. During approximately the same time period, the square footage of completed housing fell about 20 percent year-on-year, and sales of residential housing fell almost 30 percent, according to China’s National Bureau of Statistics.

As thousands of homebuyers refused to make mortgage payments on their unbuilt apartments,2It has long been common in China for home buyers to make payments even before construction of the home begins. the crisis for real estate was immediately obvious and urgently felt — after all, the property sector comprises about a quarter of China’s GDP, according to Goldman Sachs. But, like dominoes falling, it soon became apparent that other sectors could also crash — especially steel.

“In terms of construction and sales volumes, the crash landing scenario is already in progress for the housing sector,” says Gabriel Wildau, a managing director at risk consultancy Teneo. “There’s major financial risk in the property sector. It’s reasonable to expect that distress would spread to the steel industry.”

More than a third of China’s steel demand comes from real estate. So, as property crashed, so did steel profits. Just 18 months after the triumph of “100 million tonne Baowu,” Chen’s tears of joy had given way to a sense of foreboding. “It’s time to prepare for a long winter,” Chen said in July, according to Nikkei Asia, adding that the industry faced a steep downturn with “no end in sight.”

Li Ganpo, founder and chairman of Baowu rival Hebei Jingye Steel Group, warned at a private company meeting in June that almost a third of China’s steel mills could go into bankruptcy. “The whole sector is losing money, and I can’t see a turning point for now,” he told the group, according to Bloomberg News.

The steel industry, which employs millions of people in China3According to the World Steel Association, steel mills in China employ about 2 million people in China; MySteel estimates that millions more are employed in steel-dependent industries., briefly rebounded from its deep mid-year lows, but it has since sunk once more. Only about 10 percent of the country’s estimated 332 steel mills were turning a profit in early November, according to surveys conducted by MySteel, a market intelligence service. Many experts warn a reckoning is coming for the industry since the problems facing it aren’t just cyclical — they’re transitional.

“Basically, this steel sector was built on a China that wanted artificial growth forever,” says Leland Miller, CEO of economic data firm China Beige Book. “But property can no longer be used as juice to get high levels of growth. Funneling reckless amounts of credit to firms is no longer economically viable.”

Unlike any other industry, steel is one where whole [Chinese] towns and cities can depend on one company. This has the potential to create social unrest if the plant is shut down or lays off large numbers of workers.

Pradeep Taneja, a Senior Lecturer in Asian Politics at the University of Melbourne

In other words, China’s economy is poised for a rebalancing. The most productive investments in infrastructure and property have long since happened; now, unleashing domestic consumption is the most likely pathway to longer-term growth. That means going through the kind of creative destruction that ruptured heavy industry in the U.S. and U.K. as those countries transformed from industrial economies into advanced, service-dominated economies. In the U.S., for instance, cities like Pittsburgh, the heart of the country’s steel industry, plunged into decline.4Pittsburgh has since successfully transitioned into a technology and engineering hub, and recovered economically, but not without a period of pain. In January 1983, unemployment in Pittsburgh soared above 17 percent.

China’s steel firms are crying out because they sense a similar change is coming. And since China’s steel industry and its related sectors are much larger, the fallout could be even more devastating. In addition to the 332 steel mills tracked by MySteel, emerging market research firm EMIS estimates that there are over 5,000 enterprises operating in China’s iron and steel industry.

“Unlike any other industry, steel is one where whole [Chinese] towns and cities can depend on one company,” says Pradeep Taneja, a senior lecturer in Asian politics at the University of Melbourne, who lived in Wuhan and worked in the 1990s as a consultant in China’s steel industry. “This has the potential to create social unrest if the plant is shut down or lays off large numbers of workers.”

The Chinese Communist Party (CCP) is committed to few things more than social stability, and historically, the steel industry has played a useful role ensuring it. The question now is whether Beijing can bear to let this prized sector shrink so the rest of the economy can grow.

TOO MANY FIRMS, TOO MANY PEOPLE, TOO MUCH STEEL

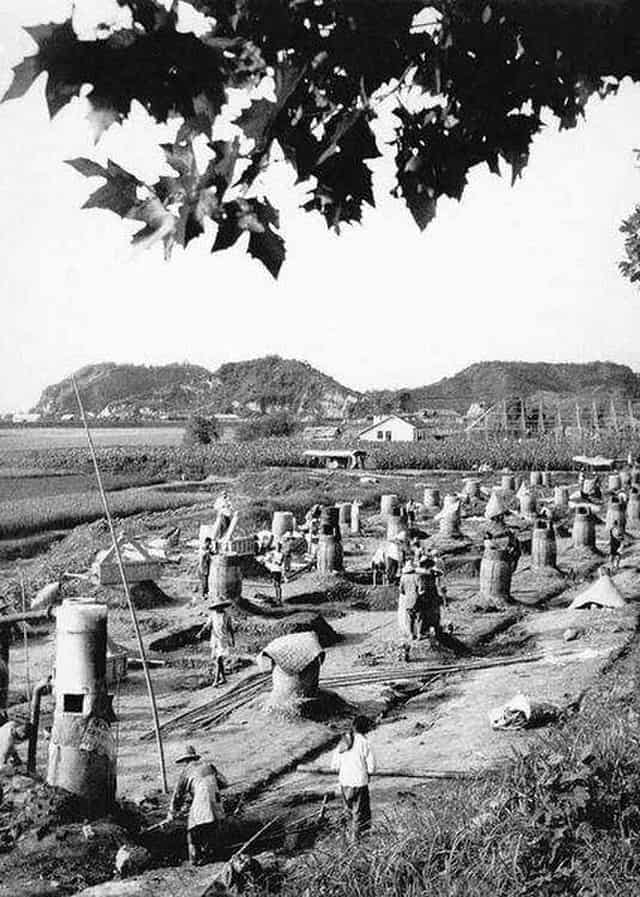

Since the nation’s establishment, the CCP has dreamt of producing a world-class steel sector. In 1958, Mao Zedong set ambitious targets for China to surpass Britain — then an industrial powerhouse — in steel production. Under the Great Leap Forward, millions of Chinese farmers abandoned the plow to produce “pig iron,” a brittle metallic substance made from smelting iron ore with coking coal, which is further refined into crude steel. The effort — done largely in backyard furnaces — backfired spectacularly, causing severe famine and an estimated 30 million deaths.

Twenty years later, however, Deng Xiaoping took a decidedly different approach to rapid industrialization. In October 1978, according to a Shanghai government press release, he toured a steel factory outside Tokyo, and what he saw blew him away.

“Just like this, build a steel plant for China,” he reportedly said.

Plans were already afoot to build a steel project to mark the country’s entry into a new stage of development. In March of that year, China’s State Council approved a proposal to establish Baoshan Iron and Steel Works (Baowu’s predecessor), according to research by Jeffrey Wilson, then of Murdoch University. But it was Deng’s Japan visit several months later that confirmed the view that China would need help if it was going to create a world-leading industry.

“At the time, Japan’s Nippon Steel represented global best practice,” says Clinton Dines, who ran iron ore giant BHP’s China operations from 1988 to 2009, and worked closely with then-Baoshan. “The Baoshan plant as it was first set up and built was essentially modeled on Nippon Steel’s main plant.”

Beijing contracted 10,000 engineers from Nippon Steel to relocate to China and work on the Baoshan project, which began churning out steel in earnest in 1985. Several larger steel companies — such as Anshan Iron and Steel, Wuhan Iron and Steel and Shougang — pre-dated Deng’s reforms, but Baoshan’s access to cutting edge technology made it something of a darling in Beijing, and it came to represent China’s modern steelmaking era.

Beijing deemed steel a “strategic industry” — central to China’s rise as a global economic force — and the CCP remained deeply entangled with the sector. The ubiquitous alloy, after all, was required for just about all of the country’s infrastructure projects, including railroads, utilities, phone towers and housing. Steel mills came to be like golden geese to local governments looking to bump up employment, reap tax revenues and hit GDP targets.

Baoshan — later known as Baosteel, and eventually Baowu after its 2016 merger with Wuhan Iron and Steel Corporation — has always boasted close ties to the Party. From 2007 to 2016, the chairman of Baosteel Group was Xu Lejiang, who now serves as deputy head of the United Front Work Department, China’s controversial agency for influence operations at home and abroad. Chen Derong, the current chairman at Baowu, has served in multiple Party positions, including as deputy governor of Zhejiang Province.

The state’s tie-up with the steel industry, however, has also been driven by social stability imperatives. As the industry grew, steel mills came to define entire cities. Anshan Iron and Steel, for instance, employed around 180,000 people in 1997 — roughly 14 percent of the city of Anshan’s population. Another large company, Shougang, reportedly had more than 200,000 employees on the books.

With China’s deeply entrenched “iron rice bowl”5The “iron rice bowl” idiom refers to stable, lifelong employment but was not inspired by the iron and steel industry. culture of lifetime employment compounded by government pressure, many steel firms essentially ran employment and benefits programs. Local governments encouraged mills to ‘grow into’ their workforces, which often meant novel workarounds to simply firing people.

Taneja, the consultant to China’s steel industry in the 1990s, says that within months of a round of layoffs at Wuhan Iron and Steel, where he was housed, “hundreds of new restaurants came up [in Wuhan], with exactly the same menu.” The staff at all of them, he says, “were steel workers, and the restaurants were run out of buildings owned by Wuhan Iron and Steel.”

While ‘too many people’ and ‘too many firms’ had long challenged Beijing in different ways, it was the advent of the Global Financial Crisis — and China’s almost $600 billion stimulus package — that truly tipped the industry into ‘too much steel’ territory.

Dines, who was working for BHP in China during a round of mass layoffs in 1997, witnessed a similar trend. “Often, they shed a lot of staff, but the workers were still living in the dorms and getting a pension from the company,” he says.

While the state-owned enterprises (SOEs) were struggling to bring their bloated workforces under control, the nascent private sector was about to have its moment. In 1998, Beijing announced reforms that would allow market-based housing supply for the first time, unleashing a voracious demand for new property. For the steel industry — especially smaller, more nimble private firms — this was like rocket-fuel, as they battled to feed the metal-hungry market.

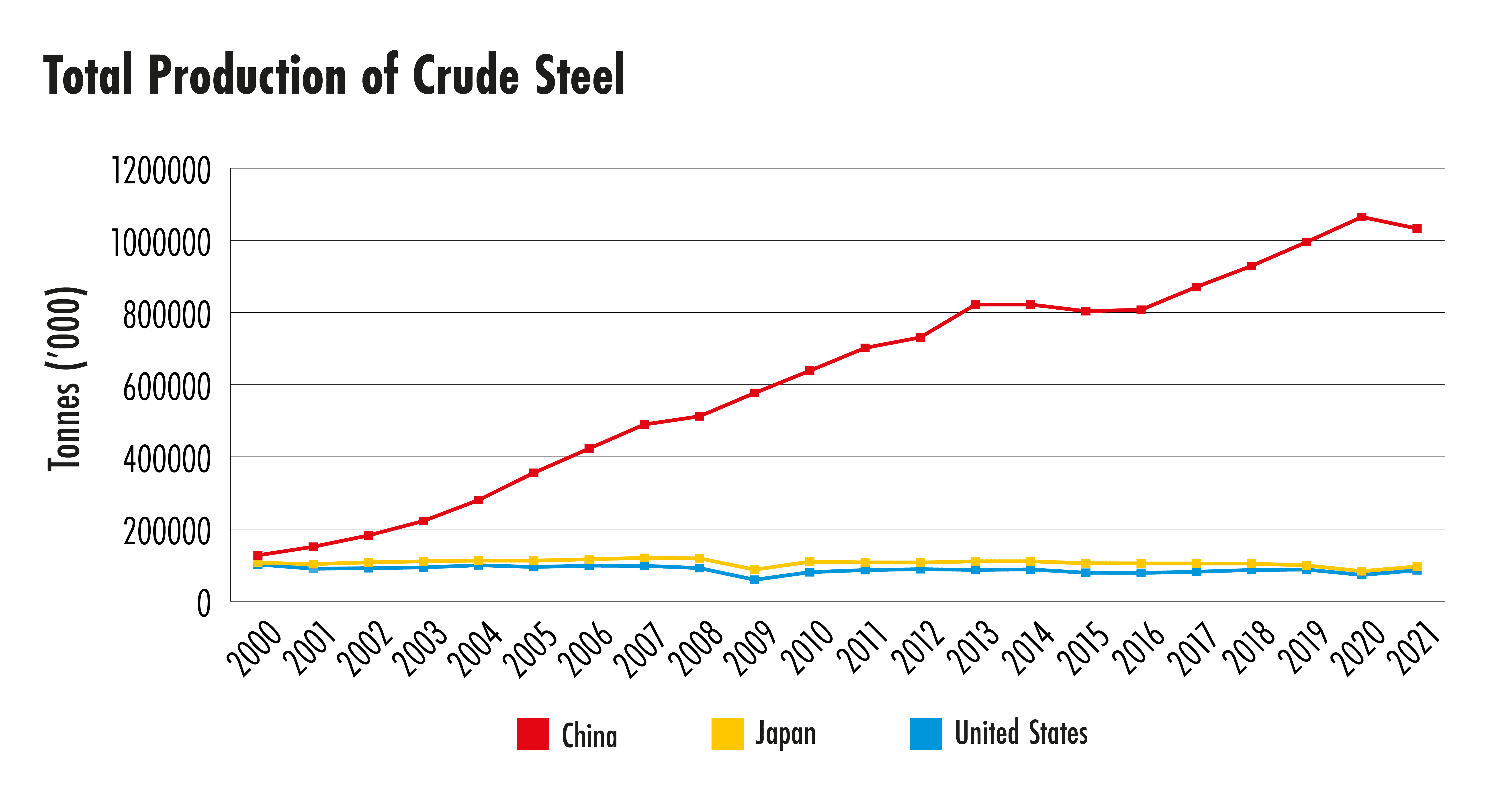

In 1999, China and the U.S. were consuming roughly the same amount of steel per year, according to World Steel Association statistics; by 2005, China’s steel consumption was well over triple that of the United States.

“You couldn’t imagine it in any other country,” says Alexander Hu, an independent consultant who worked for a privately-owned steel mill in China from 2006 to 2009. “The steel mill I worked for, they built their first blast furnace within six months from scratch,” he says, noting the usual time taken for such an operation would be two to three years.

Around the turn of the century, Beijing was growing increasingly concerned about the number of steel mills mushrooming across the country. It felt a fragmented industry couldn’t effectively negotiate with suppliers, like the big Australian and Brazilian iron ore companies, nor could it achieve economies of scale or minimize pollution. At the same time, it was staring down the problem of lumbering, overmanned SOEs.

Beijing could have allowed the steel market to work itself out, letting inefficient steel firms go bankrupt, for instance, or letting companies fire workers to stay afloat. But instead, it settled on a new strategy: directing high-performers like Baosteel to acquire laggards, with the goal of encouraging technological upgrades and productivity improvements in targeted firms, while minimizing layoffs.

As early as 1997, for example, Baoshan got the call to merge with two poor-performing mills owned by the Shanghai municipal government. The company’s chairman at the time, Li Ming, was not happy about it: “If these companies are merged,” he told Bloomberg that year, “economic efficiency” would suffer. According to an O.E.C.D. report from 2000, Baoshan’s debt rose from 17.8 percent of equity in 1996 to almost 40 percent at the end of 1998, after the acquisition.

Government-directed mergers picked up after 2005, when the National Development and Reform Commission issued the Iron and Steel Industry Development Policy, which outlined goals for significant consolidation of the industry. Baosteel became a favored acquirer, merging with at least 5 steelmakers between 1998 and 2015. While most of its rivals in China have between 100,000 and 150,000 workers, Baowu now has 227,000 employees.

While ‘too many people’ and ‘too many firms’ had long challenged Beijing in different ways, it was the advent of the Global Financial Crisis — and China’s almost $600 billion stimulus package — that truly tipped the industry into ‘too much steel’ territory. It was around this time, analysts say, that China’s natural rate of growth had slowed, but with Beijing opening the coffers to stimulate an economy in crisis, China’s heavy industries — including steel — only ramped up.

In a universe of rampant overcapacity, no one has been a bigger offender over the years than Chinese steel firms.

Leland Miller, CEO of economic data firm China Beige Book

China’s aims for its broader economy were, in this case, at odds with its purported goal of reducing capacity in the steel sector. Beijing was under pressure from international steelmakers who complained about cheap Chinese steel being dumped in overseas markets. But with cash for construction flowing and local governments eager to boost growth, steel mills faced little incentive to reduce output.

“In a universe of rampant overcapacity, no one has been a bigger offender over the years than Chinese steel firms,” says Miller, from China Beige Book.

In 2013, according to the state-owned China Daily, a Beijing official warned that “existing regulatory measures failed to stop the indiscriminate development of the steel sector,” and that a new strategy was required. Those comments presaged the introduction of Xi Jinping’s Supply-Side Structural Reform (SSSR), first announced in late 2015. Geared at reducing industrial capacity and debt that had ballooned during the stimulus years, the SSSR targeted the steel sector as an initial priority, alongside coal.

Under the SSSR, Baosteel, at that time the second largest steelmaker in China, was approved to merge with Wuhan Iron and Steel, the fifth largest steel firm, to create the behemoth Baowu that would soon overtake ArcelorMittal as global number one. Through mergers and “capacity swaps” — which were designed to ensure mills retired more capacity than they built in environmentally sensitive areas — Beijing aimed to reduce steel capacity by 100 to 150 million tonnes by 2020.

Analysts note, however, that Beijing’s efforts to rein in the steel industry have been partly counteracted by powerful forces in favor of the status quo, such as local governments chasing cheap growth. In 2020, after all, China’s steel production reached record levels.

Data: World Steel Association, Steel Statistical Yearbooks

To truly see a difference, some say, more tough love is necessary.

CRASH LANDING?

Baowu, despite its chairman’s dark rhetoric, is one of the lucky ones. A champion among national champions, it is still on China’s cutting technological edge, and it supplies more metal for electrical equipment and car-makers than it does beams to hold up apartment buildings.

It’s also at the leading environmental edge among Chinese steel firms, which is crucial in an industry that generates around 15 percent of the country’s greenhouse gas emissions. Mitigating pollution and meeting the country’s emissions reduction targets are central to Beijing’s drive to cap steel capacity. And while China’s steel sector isn’t exactly a global leader when it comes to innovations like so-called “green steel” (which is made from renewable hydrogen with no carbon emissions), Baowu stands out among Chinese steelmakers for its commitment to peak emissions by 2023 and carbon neutrality by 2050. If it can achieve those goals, it will maintain competitiveness even as the overall sector declines.

For these reasons, analysts say, Baowu will be far from the front lines in the “long winter” of steel’s discontent — rather, the hundreds of smaller and less efficient mills will be the ones facing the crunch.

Nevertheless, it seems to finally be sinking in that the era of unfettered growth is over. And this has been a tough pill to swallow.

At some point economies go from heavy industry into services, and that comes with a lot of pain… Will China go through it? Or will the process be delayed because, in a benevolent effort to cushion the blow, Chinese industrial policy might slow down its transition?

Nancy Qian, from Northwestern University’s Kellogg School of Management

In 2021, for instance, Chinese officials noted that the steel industry had “some deep-rooted contradictions” and that authorities would again be focused on cutting production. Yet, just a year later, as the property sector teetered on the edge and Covid-19 lockdowns further ravaged demand, China’s steel industry incongruously ramped up production.

Analysts say the steel industry acted this way in expectation of a government stimulus package to bolster the ailing property sector. After all, that has always been Beijing’s playbook in times of economic trouble: build, build, build.

“This is the way that China’s growth model has worked for decades,” says Miller. “China grew organically at around 4 percent, then wanted to hit 7 percent so it would just build stuff. It would ease credit for property, which would turn into GDP growth to meet the target..”

A CGTN video covering Baosteel’s zero-waste mission, July 8, 2022.

This time, though, the stimulus took longer to come than they expected, as Beijing contemplated how to bolster property developers without inflating the bubble. When the bulk of the infrastructure stimulus finally came in June 2022, it didn’t have the desired impact. Through the course of this year, tax breaks, interest rate cuts and policy bank lending haven’t been able to counteract low consumer confidence in the housing sector.

The steelmakers, says Cory Combs, an associate director at Trivium, a China-focussed policy analysis firm, “got caught with their pants down.”

With record high supply and historically low demand, the big question is: What happens next?

“It’s not like demand for steel is going to crash to zero,” says Qian, from Kellogg. Indeed, many experts note that China remains a large country with a large population, which will continue to demand improvements to public infrastructure and their own homes.

“But this is a turning point,” Qian says. “At some point economies go from heavy industry into services, and that comes with a lot of pain. America went through it. The UK went through it. Will China go through it? Or will the process be delayed because, in a benevolent effort to cushion the blow, Chinese industrial policy might slow down its transition?”

In other words, Beijing faces a dilemma. Continuing to prop up heavy industries like steel, including indirectly through infrastructure and property investment, delays tough decisions — like regional economic transitions that will inevitably include layoffs. But it also delays China’s own economic transition, risking a sharp slowdown in growth and, as a corollary, a threat to the CCP’s legitimacy.

“If you subsidize an industry to maintain employment, what’s the sacrifice? What price are you paying in order to do that,” Qian adds. “Is it good to keep people in a stagnant industry? In the short run, yes, because you don’t lose jobs. In the long run, the industry is no longer productive and people need something else to do. You’re not helping them by keeping them in that industry.”

On the other hand, allowing the restructuring to unfold naturally could mean a wave of unemployment concentrated in certain regions — and the potential for political and social unrest. Given that, few analysts think Beijing will let its steel industry crash and burn.

“If nothing else, I just think the size of the industry will mean that the government will be keen for it not to collapse,” says Caroline Bain, the chief commodities economist at research firm Capital Economics.

Some point to the government’s success at managing limited waves of redundancies in the past, particularly in the Supply-Side Structural Reform era in the mid-2010s, as a sign that China could handle a gradual transition away from its heavy industries.

“Arguably the net capacity cuts were too small, but they were able to do them with quite a bit of success,” says Wildau, from Teneo. “Obviously that caused some localized economic pain and unemployment, but it didn’t cause major social unrest. Beijing has a pretty strong record of being able to manage restructuring.”

Others, though, say the harder part will be letting the transition happen at a time of such economic uncertainty. The industry has already gained some experience when it comes to shutting down steel plants, says Richard Lu, a senior analyst at market intelligence firm CRU Group, “but there still might be risks and unexpected impacts. If we go back to the beginning of the year, no one expected the Covid lockdown to disrupt the economy this way, so sharply. If it happens again, this will make layoffs very difficult, especially given the very high unemployment rate for younger people in China right now.”

Faced with distractions like Covid, Combs at Trivium says facilitating a restructuring in the steel sector runs the risk of falling to the bottom of Beijing’s list of priorities. But in reality, managing the transition away from heavy industries like steel and toward a more consumption-driven economy is exactly the bitter pill that would resolve many of the economic challenges on Beijing’s list.

“There’s going to be a need for a leaner and greener future for the sector,” Combs says. “But steel still has to shrink in the macro picture in China. What’s not clear is: Who’s going to take up this huge steel-sized hole in China’s economy once that happens?”

Isabella Borshoff is a staff writer based in London. Previously, she worked as a climate policy adviser in Australia’s federal public service. She earned her Master’s in Public Policy at Harvard’s Kennedy School. Her writing has been published in POLITICO Europe. @iborshoff

{kind=link}

{kind=link}