On a Friday morning in April this year, Simon Thompson, the outgoing global chair of the mining giant Rio Tinto, addressed the company’s shareholders in London for the last time. Thompson, who chose not to stand for re-election after Rio Tinto destroyed an ancient Aboriginal site in Western Australia in 2020, spoke with the somber optimism of a leader emerging from scandal and vowing to do better.

But amidst talk of “transition,” “rebuilding” and “strengthening,” Thompson1Rio Tinto has appointed Dominic Barton, the longtime McKinsey executive with extensive experience in China, as the company’s new chair. brushed over a development at one of the company’s long-stalled mining projects: the Rio Tinto board had agreed to a path forward for the Simandou site, an iron ore venture in the African nation of Guinea.

The Simandou update was awkwardly slotted into the “climate change” section of the chair’s remarks, and Thompson made no reference to what some observers say is the real driver of Rio’s decision to proceed with a project long plagued by corruption scandals, political upheaval and near-impossible logistics: China, Rio’s largest customer2In 2021, 57.2 percent of Rio Tinto’s revenues came from China., wants it done.

“Rio wants to prevent any hiccups [in the China relationship],” says Philip Kirchlechner, an iron ore industry veteran who ran Rio Tinto’s operations in Shanghai from 1996 until 2001. “To be a positive force in Simandou would be appreciated by the Chinese government.”

Luke Hurst, an expert on China’s iron ore market and the managing director of Asia-focused strategy firm Lydekker, agrees that Simandou “is about having that almost halo effect of working with China.”

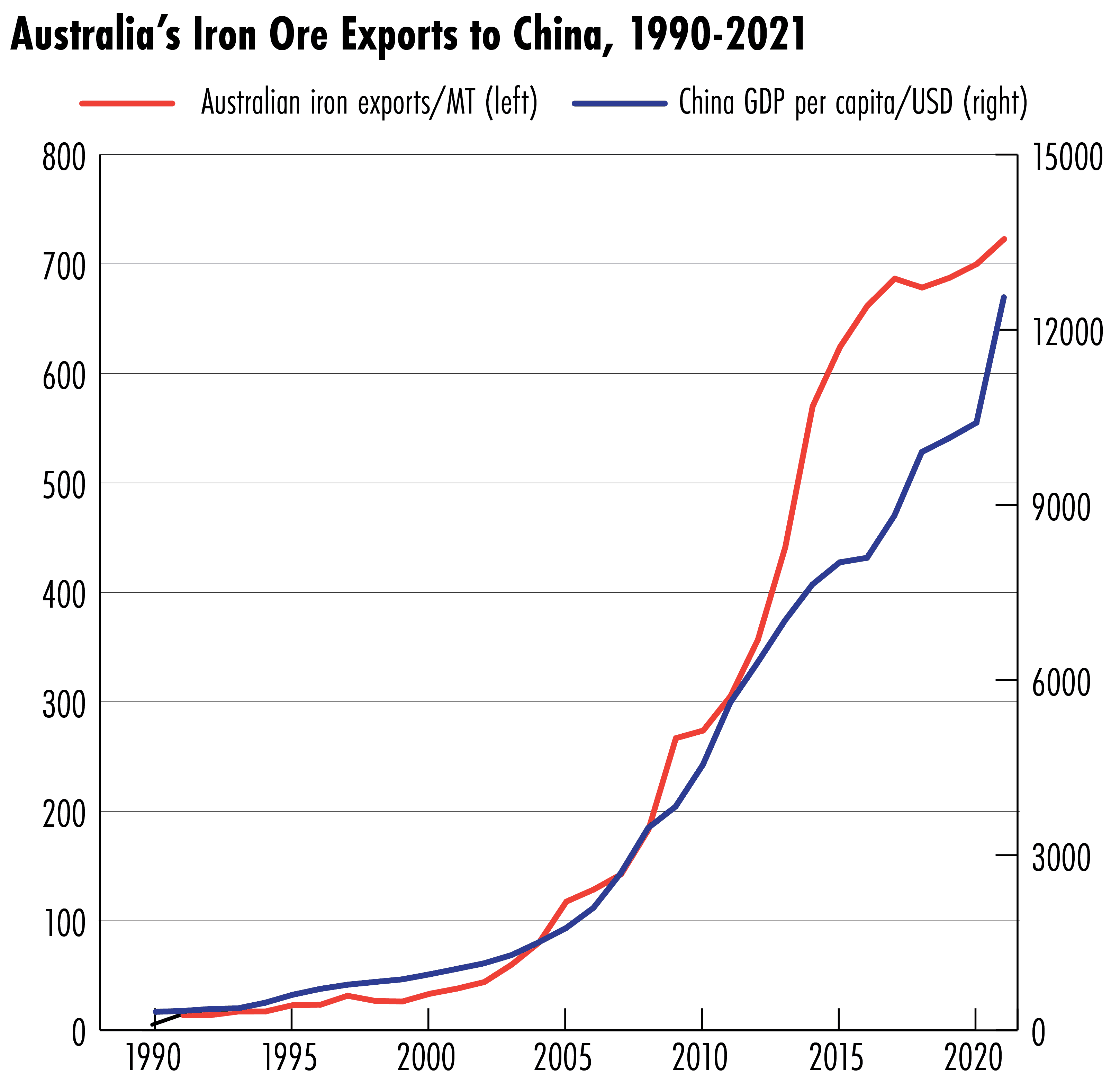

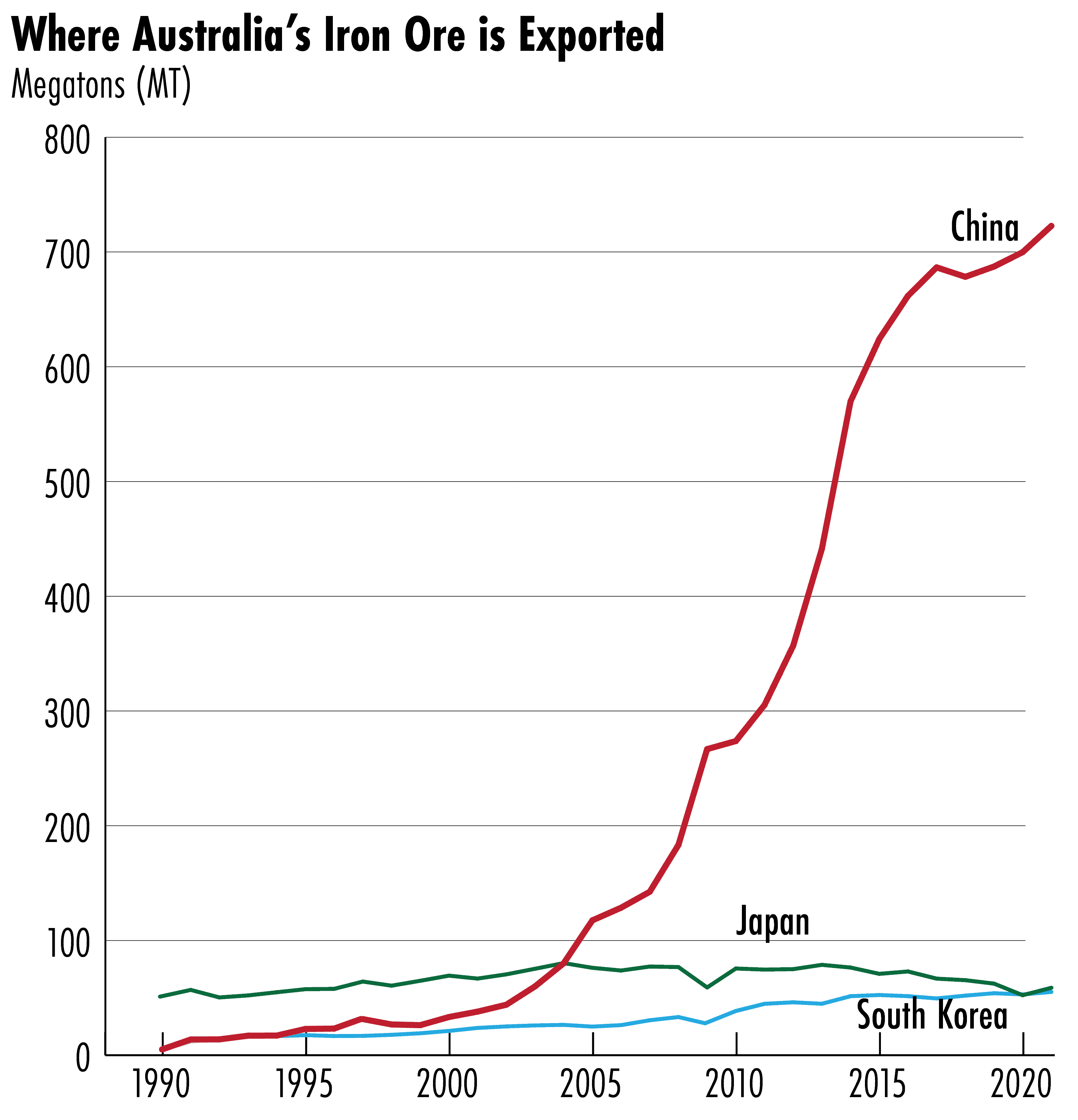

Rio Tinto’s main business is digging up iron ore, the unassuming rock that’s processed into the scaffolding of the modern world — steel. Over the last three decades, the British-Australian company’s rise as a global super producer has closely tracked China’s development boom: as China urbanized and industrialized, its steel mills’ insatiable hunger galvanized Australia’s mining industry, which supplies more than 60 percent of China’s imported ore.

But China’s heavy reliance on a single country for such a critical natural resource has never been entirely comfortable, and the deterioration in the China-Australia political relationship in recent years has brought this dependency into even sharper relief.

“There are planners in China who think they’ve become unhelpfully dependent on Australia,” says Laurie Smith, a China expert, businessman and former Australian trade official in China. “It really did come as a shock that iron ore, of all things, would become such a key commodity and that a second tier player in their eyes — Australia — could be a price maker, and thus would give them such grief.”

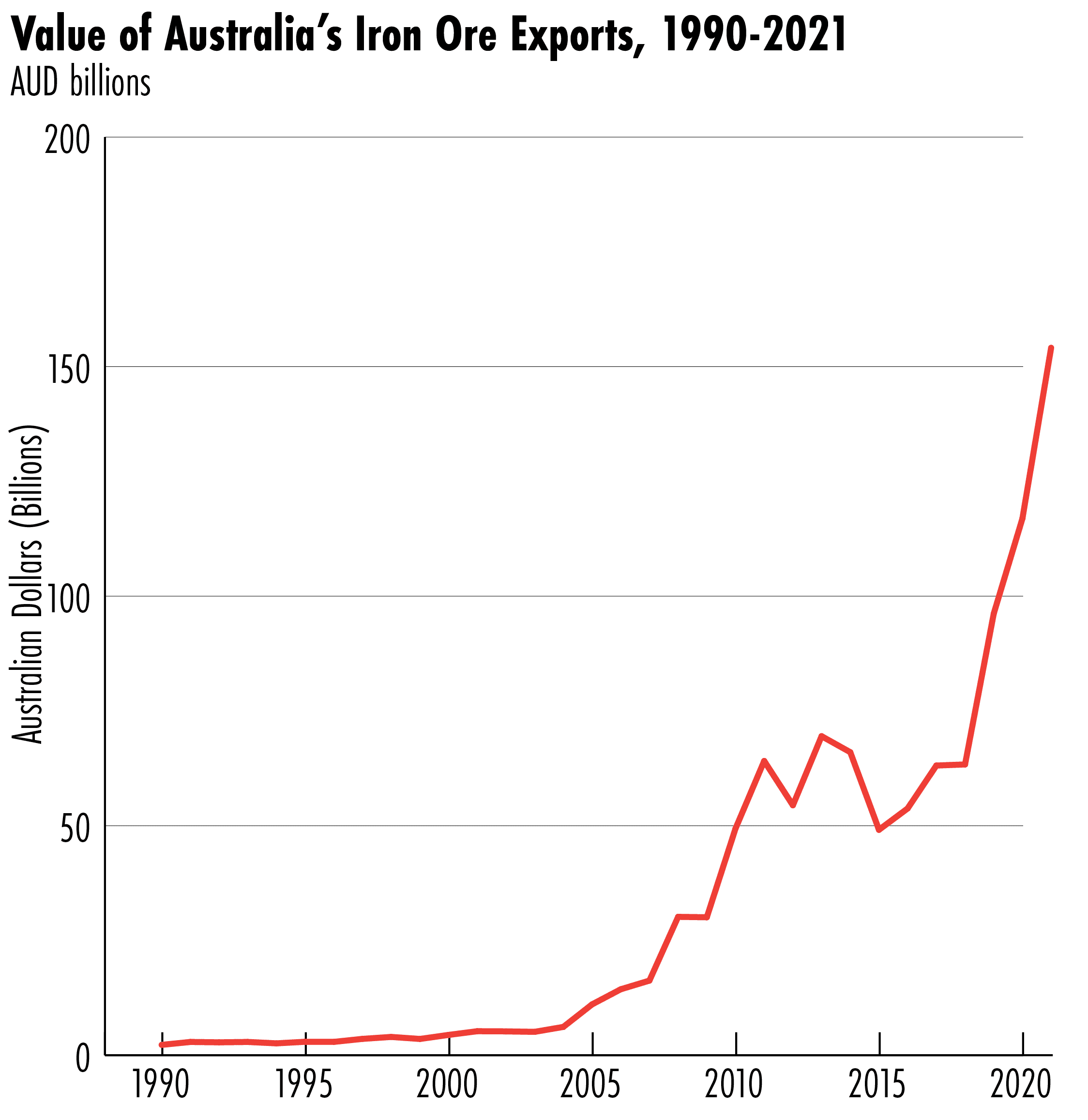

Indeed, since 2020, China has waged a trade war against Australia for perceived political provocations, including Australia’s ban on Huawei from its 5G infrastructure in 20183Soon followed by a range of other countries, including U.S., UK, New Zealand and Japan. and its April 2020 call for an inquiry into the origins of Covid-19 in China. Beijing has slapped sanctions on Australian goods ranging from barley and coal to lobsters and wine, but, to its likely chagrin, the coercive campaign hasn’t inflicted sufficient pain on Australia to elicit political concessions. Australian producers have successfully diversified, but even more importantly, China hasn’t touched Australia’s $103 billion4About $150 billion AUD iron ore export industry — the backbone of the China-Australia trading relationship, which has generated mutually reinforcing economic growth for both countries. Beijing simply can’t afford the hit to its domestic steelmakers, who play a central role in the country’s economy.

“They need it, we’ve got it,” summarizes Robert Williamson, an iron ore industry veteran. “I’ve got friends with large wineries that have suffered, people in the crayfish industry that have suffered, but those are just things for their [China’s] middle classes and upper classes. Iron ore is about everybody.”

The reality is that China has limited options when it comes to escaping Australia’s dominance in iron ore trade. Brazil, the next largest producer and the oft-looked to alternative, has been dogged by production disruptions over the years, and produces less than half of Australia’s output. China’s total iron ore imports were more than three times greater than Brazil’s global exports in 2021. Plus, to get to China, Brazilian ore has to travel across two oceans and up through Asia — adding significantly to the cost of supply.

That’s where Simandou, in Guinea, comes in.

China has tried to buy influence and assets on the supply side of the iron ore industry for years. It has secured stakes in undeveloped projects around the world and even went so far as to seek installation of two members to the Rio board during a failed 2009 deal. But, even after arresting some of Rio’s employees in China — a move that was widely seen as intimidation — the closest it has come to a owning a top-tier operation is buying a 10.3 percent stake in Rio and negotiating a joint venture at Simandou — an investment it is now desperate to see to fruition.

In the mining world, Simandou is regarded as the best undeveloped iron ore resource. Almost all of Rio’s ore currently comes from the Pilbara, a remote region in Western Australia, and Simandou has been dubbed the “Pilbara Killer” for its potential to flood the market with high quality rock, reducing the global iron ore price and denting Australia’s resource revenues. When mining industry people talk about Simandou’s “grade,” or quality, they get almost dreamy about its raw potential. It’s especially promising for new, lower-carbon steel-making processes, which require purer ore than China has historically consumed.

“This stuff is as black as my iPhone. It’s very, very high grade,” says Williamson.

Simandou has been an industry talking point for more than two decades, but since Rio was first granted the exploration rights to the region in 1997, not a single rock has been extracted. The deposit is buried under the hills of southern Guinea, in west Africa — a country that’s geologically blessed, but politically blighted. Guinea ranks 178 out of 189 countries on the United Nations’ Human Development Index, and Simandou’s well-known promise to catapult the country’s GDP has made it the political football of successive Guinean leaders. For example, on July 5, the Guinean government halted all preliminary work on the project for the second time this year, out of frustration with the slow pace of development. The deposit’s remote location — over 600 kilometers from the coast, in the jungle — makes the logistics a nightmare.

Rio came to the brink of selling its problem-plague stake in Simandou in 2016. But in the last two years, the company — alongside its joint venture partner, a consortium led by China’s state-owned aluminum and copper producing giant Chinalco — began making positive noises about the project.

Rio Tinto declined to comment on the motivation for pushing the Simandou project forward.5In the past, Rio executives have said Simandou ore won’t compete with Pilbara ore, precisely because it lends itself to different kinds of steelmaking. Some industry experts say that Simandou could serve as useful replacement capacity – rather than overcapacity – if commissioned far enough into the future. But given the notorious difficulty of predicting steel demand, in many ways, a risky project like Simandou is the last thing Rio needs. The company is already wrangling one politically complex project in Mongolia and grappling with other controversies in its business — namely, the destruction of the Aboriginal site at Juukan Gorge and revelations of widespread bullying and sexual harassment within the company. But with the project high on Beijing’s priority list, Rio appears to be in a bind: stall the project and risk angering its number one customer — or press on and pour shareholder money into the Simandou abyss?

‘AN UNHAPPY CHINA’

Rio is no stranger to Beijing’s ire. On July 5, 2009, secret police showed up at the Shanghai home of Stern Hu, Rio’s chief iron ore representative in China, and detained the Chinese-born Australian citizen on charges of stealing state secrets.6Bloomberg Businessweek published this superb account of the case in 2018.

Those charges — also leveled against three of Hu’s Chinese colleagues — were later downgraded to bribery and stealing commercial secrets, but after a partially closed-court case, the four men were sent to prison. Hu’s sentence was ten years.7Hu served eight years before being released in 2018.

In the years leading up to Hu’s arrest, as Chinese demand for Australian iron ore skyrocketed, relations between the major Australian suppliers — including Rio and British-Australian company BHP — and the Chinese government were markedly tense. It’s hard to imagine now, says Clinton Dines, BHP’s former senior country executive for China, but back then “international organizations like BHP didn’t think of China as a significant opportunity.” But “the whole world knew by 2003,” he says. “The whole world went ‘oh shit’ by 2003.”

The result was a tight market, as Australian iron ore miners scrambled to ramp up production and keep up with Chinese steelmakers’ insatiable appetite. Prices rose from $30 a tonne in 2001 to almost $200 in early 2008.

This sent the Chinese government into a panic. Conscious that “they were going to have to import this stuff for forever and a day,” according to Dines, Beijing tried to pressure iron ore prices down, but struggled against the severe supply-demand imbalance, which kept prices elevated. Additionally, the producer side of the market was highly concentrated among the big three miners, and with their product in short supply, they had significant leverage in negotiations. At the same time, the Chinese steel industry was fragmented and uncoordinated, preventing it from extracting the best deal.

Beijing was infuriated by its inability to influence the price. In March 2006, The Australian quoted a joint statement from China’s National Reform and Development Commission and the Commerce Ministry, which accused iron ore suppliers of having “taken advantage of their monopoly status in the iron ore trade to reap huge and unreasonable profits.”

“The Chinese Government will pay close attention to the negotiations. If there are unreasonable prices, which we regard as unacceptable, the Chinese Government will adopt necessary measures to protect the interests of the state and its companies,” the two agencies said, according to The Australian.

But the market dynamics were too powerful. In 2008, the price agreed by Baosteel, China’s largest steelmaker, and Rio Tinto was 86 percent higher than the 2007 price. Beijing tried to crack down on the process by implementing a centralized purchasing system through the China Iron and Steel Association (CISA). But China’s steelmakers quickly learned to circumvent the bureaucrats at CISA to get their hands on Australian ore more quickly, further enraging Beijing.

Meanwhile, in 2007, BHP went public with an offer to buy Rio Tinto, which would have caused even greater consolidation in the industry and further decreased China’s leverage in price negotiations. Rio’s board rejected the deal, but as BHP mulled upping its offer, China’s state-owned aluminum enterprise Chinalco shocked the industry by raiding Rio’s shares on the morning of February 1, 2008, securing — jointly with U.S. aluminum company Alcoa — 9 percent of Rio for $14 billion. The move was widely interpreted as an attempt to make BHP’s takeover more difficult.

“The Chinese have been grumbling, but we did not realize they would be so aggressive in trying to thwart BHP,” a mining industry consultant in Shanghai told the Financial Times at the time.

BHP eventually abandoned its Rio takeover bid in October 2008, after the Global Financial Crisis sent commodity prices tumbling and Europe’s competition commissioner considered antitrust restrictions on such a deal.

Rio Tinto was, at this point, highly leveraged after a 2007 acquisition of its own and struggling for survival. Beijing saw another opening. On February 12, 2009, Rio Tinto announced that Chinalco would pay $19.5 billion to increase its stake in Rio to 18 percent.

The deal immediately stirred controversy among Australian policymakers who announced they would examine it under the country’s foreign investment screening process.

BHP, too, was concerned about the implications of a Chinese state-owned company exerting influence over iron ore prices from the supply side. According to U.S. diplomatic cables published by Wikileaks, BHP mobilized its well-oiled lobbying machine to pressure the Australian government to torpedo the deal. But, in the end, the government didn’t need to: Rio jumped ship in June 2009, paying Chinalco almost $200 million in break fees and — with the ultimate knife-twist — immediately announcing a joint venture with BHP in Western Australia.8The deal fell apart in 2010, after negative signals from regulators.

“The [Chinalco] deal’s sudden collapse spares the GOA [Government of Australia] from making a difficult decision,” reads a U.S. Foreign Service cable from Canberra. “It leaves PM Rudd to deal with an unhappy China. We noticed a very glum Chinese Ambassador Zhang Junsai waiting outside Rudd’s office with Chinalco CEO Xiong Weiping on the afternoon of June 5.”

A month later, Stern Hu and his three Chinese colleagues were arrested in Shanghai. While most industry insiders The Wire spoke to did not wish to speculate on whether Hu and the other convicted Rio staff had engaged in bribery, it is widely assumed the Stern Hu affair, as it’s now known, was retribution for the abandoned Chinalco deal.

“There was a sense the case was not being dealt with purely on its merits and was being used to teach a lesson to Australia, or at least its iron ore companies,” says Smith, the former Australian trade official and China expert. “Not everybody would have interpreted it that way, but I think many companies did with good reason.”

Rio, facing an escalating crisis with its most important customer, hastened to patch things up. While the four Rio employees were awaiting trial, the company began negotiating with Chinalco to buy into the Simandou iron ore concession in Guinea. Rio had originally held rights to the entire concession, but was unexpectedly stripped of the northern half of the deposit in 2008, when it was transferred to BSG Resources, the family company of notorious Israeli diamond trader Beny Steinmetz.

In March 2010, just before Hu’s trial, Rio and Chinalco signed a non-binding agreement to transfer 44.65 percent ownership of Rio’s piece of Simandou to Chinalco for $1.35 billion dollars. For Chinalco, thwarted in its efforts to snap up more Rio shares and exert greater influence over Rio’s prized Australian assets, joining a new development with an experienced player was the next best option.

My view of Simandou is that it can never really work. You’ve got to spend an absolute fortune on infrastructure to get the stuff to a port. And you’ve got an unstable political environment in that part of the world.

Stephen Joske, former chief China economist for the Australian government

The following five years, however, saw the Simandou site beset by problems: Steinmetz sold his stake to Rio’s Brazilian rival, Vale; a corruption probe was launched into the original Steinmetz deal; Rio was forced to pay $700 million to the Guinean government and offer it the right to a 35 percent stake in the project to keep the ball rolling; the Ebola epidemic spiraled out of control in West Africa; and Rio ended up suing BSG and Vale on the grounds they were part of a conspiracy to steal its rights to Simandou. (The lawsuit ultimately failed but in 2021, a Swiss court sentenced Steinmetz to five years in prison for bribery relating to Simandou.) And after a decade of owning a 5 percent stake in the project, the World Bank’s commercial finance arm, the International Finance Corporation, pulled the plug.

By 2016, Rio also wanted out. That October, Rio signed a non-binding agreement to sell the remainder of its interest in Simandou to Chinalco, but the two parties never reached a deal, and the agreement collapsed by 2018.9In 2016, Rio confronted fresh scandal as it disclosed an email exchange from 2011 between senior Rio executives discussing a $10.5 million payment to a Guinean government adviser. UK and U.S. regulators are still probing the payment in a possible bribery case; the Australian regulator recently closed the case and cleared Rio of wrongdoing.

China, meanwhile, was working on other routes into Simandou. The Guinean government, ever eager to see the site developed, auctioned off the former BSG/Vale concession in 2019. SMB Winning10The consortium is already a leading Bauxite exporter in Guinea., a consortium including Singapore’s Winning Shipping, Guinea’s Societe Miniere de Boké and United Mining Supply, and China’s Shandong Weiqiao Pioneering Group and Yantai Port Group, won the rights for a reported $15 billion.

Today, around 31 percent of Simandou is owned by Chinese companies.

‘WITH OR WITHOUT RIO TINTO’

According to industry experts, it is in China’s interest to keep Rio in the Simandou tent — at least for now. While Chinese companies are increasingly successful in lithium and cobalt mining, iron ore is a different game. Because it’s such a low value commodity — its price peaked last year at $233 per tonne, compared to cobalt and lithium carbonate peaks this year of $82,000 and $78,000 per tonne respectively — it needs to be mined at an enormous scale for the business case to stack up. The joint venture arrangement allows Chinalco to capitalize on the knowledge Rio has developed over years running such behemoth operations.

Still, even though the iron ore at Simandou may be world class, getting it from the mine site to the end customer will require colossal effort. According to planning documents published by SMB Winning in November 2021, more than 600 kilometers of new railway will be needed to connect Simandou to a port south of Guinea’s capital Conakry.11SMB Winning has commenced preliminary work on the railway, but Rio and SMB Winning’s failure to reach a formal infrastructure sharing agreement by a government-imposed deadline triggered the recent order to stop work. Given the mountainous terrain, four tunnels will be required, as well as 169 bridges and 592 road crossings. More than 400 villages will be impacted, with at least several being relocated, according to the consortium. On top of that, the water immediately off the Guinean coast is too shallow to launch an iron ore freighter, so the project proponents will have to chip in for a new deepwater port.

The estimated total cost is reported to be between $12 and $20 billion. And, when completed, the Guinean government says it will claim ownership of the infrastructure. This adds significant risk: the miners won’t have complete control over their transport costs and will likely face interruptions and diversions, all of which impacts their bottom lines. According to the Guinean Minister for Mines, the railway will be used to transport people, property and agricultural products, as well as mining outputs. In the Pilbara, by contrast, privately-owned trains travel a straight shot between mine and port.

“My view of Simandou is that it can never really work,” says Stephen Joske, formerly the Australian government’s chief China economist in Beijing. “You’ve got to spend an absolute fortune on infrastructure to get the stuff to a port. And you’ve got an unstable political environment in that part of the world. You’re going to get hit sooner or later.”

Beijing, however, is rarely deterred by the politics and terrain of countries like Guinea. In recent years, Chinese mining companies have ramped up their presence in Africa, including in the resource-rich Democratic Republic of the Congo, a country deemed too risky by most major Western companies but embraced by Beijing. Indeed, in some ways, China is better placed than most to weather Simandou’s challenges — especially given the potential rewards.

“China can think in a much longer term horizon than pretty much anyone else,” says Hurst, at Lydekker. Although there are no guarantees with a project like Simandou, he says, China has “developed serious experience on the ground with tricky governments in tricky places.”

By 2020, China’s renewed ambition to get the project up and running became clear. In March, Bloomberg first reported that China’s powerful State-owned Assets Supervision and Administration Commission of the State Council (SASAC) was looking into backing the project.

As China launched a post-pandemic stimulus campaign and manufacturing picked up after the initial Covid-19 wave, demand for iron ore soared. Meanwhile, friction in the bilateral relationship with Australia was intensifying: in April 2020, Australia called for an investigation into the origins of Covid-19 in China. It was soon widely reported that then-Prime Minister Scott Morrison was advocating in private conversations with foreign counterparts for the World Health Organization to be granted ‘weapons inspector’ style powers in such an investigation. In May, China slapped duties on Australian barley and began blocking Australian beef imports — the first signs of a broader campaign of economic coercion and Beijing’s determination to start “decoupling” from Australia.

They’re not talking about doing away with the [iron ore] dependency, just reducing it. For the Australian economy, if China reduced its dependency by 10 percent, that would be a huge hit.

Linda Jakobson, a leading Australia-China expert and founding director and deputy chair of China Matters

Although iron ore was left untouched, the writing was on the wall: Beijing wouldn’t leave Australia’s dominance unchecked.

“Under all scenarios Simandou will be developed, with or without Rio Tinto,” Rio’s then-CEO Jean-Sébastian Jacques told Bloomberg News in July 2020. “There is a huge incentive for the Chinese to make it happen now.”

Linda Jakobson, a leading expert on the Australia-China relationship and the founding director and deputy chair of China Matters, an independent Australian policy institute, says the relationship breakdown between Australia and China has “absolutely” impacted China’s view of its iron ore dependency.

“As long as the [Australia-China] relationship was, generally speaking, a very constructive one — which I would say was the case all the way to 2016 or 2017 — the dependency on Australia was talked about amongst strategic thinkers [in China], but it was a remote prospect,” she says. “Before the deterioration, [the problem of dependency] was still very hypothetical.”12The diplomatic freeze between the two countries ended in June 2022, when their Defence ministers met on the sidelines of a security summit in Singapore. However, relations are still tense, and China has so far rejected Australia’s calls to lift trade sanctions.

Analysts also point to rising global tensions as a potential source of anxiety for China. Recently, former Australian Treasurer and Ambassador to the U.S. Joe Hockey told Australia’s Sky News that, in 2014, President Barack Obama asked him and then-Prime Minister Tony Abbott to stop sending iron ore to China, in an effort to combat China’s rise. Australia didn’t listen then, but given that the U.S.-China and Australia-China relationships are both significantly more strained now than they were during Obama’s tenure, and that the Australia-U.S. alliance, in turn, is stronger than ever, many say China’s attempts at iron ore diversification are motivated partly by fear.

“I think it’s because they are afraid of us, and they think that we would cut off iron ore to them, especially in the context of a Taiwan contingency or some other political dispute,” says Darren Lim, a senior lecturer in international relations at the Australian National University and expert in economic statecraft. “If the Americans told us to do it, they think that we would do it.”

Fear may contribute to Beijing’s drive to get Simandou up and running, but it doesn’t make the project any easier. Many observers think Australia’s geographic advantage will forever give it an edge in China’s iron ore market. As James Laurenceson, director of the Australia-China Relations Institute, notes, the fact that China is concerned about dependence on Australia “doesn’t mean [they] can get away from it.”

Jakobson, the China Matters expert, agrees that total diversification is impossible, but she’s more circumspect when it comes to assumptions about what Beijing will or won’t achieve.

“The PRC has been agile and very cleverly focused on reducing dependency on one source, and has successfully diversified in many cases before iron ore. That’s something Australia needs to bear in mind,” she says, citing Beijing’s diversification of its oil imports away from the Middle East. “They’re not talking about doing away with the [iron ore] dependency, just reducing it. For the Australian economy, if China reduced its dependency by 10 percent, that would be a huge hit.”

Rio Tinto, for its part, is moving forward with Simandou. The company says it will work with the Guinean government and its Chinese partners to “develop this nation-transforming project,” pointing to their preliminary agreement on the infrastructure needed to ship the iron ore to market. In a speech in May, Rio Tinto’s CEO, Jakob Stausholm, said he was “committed to ensuring that the people of Guinea benefit from Simandou.” The government wants Rio and its partners to prove it, by formalizing the infrastructure agreement immediately.

How long it will take for Rio and its partners to reach such an agreement is unclear. In any case, by progressing with Simandou, Rio Tinto is now in the awkward position of trying to help China on its mission to reduce reliance on the country where Rio itself is partially headquartered. How the company will iron out that wrinkle remains to be seen.

Isabella Borshoff is a staff writer based in Australia. Previously, she worked as a climate policy adviser in Australia’s federal public service. She earned her Master’s in Public Policy at Harvard’s Kennedy School. Her writing has been published in POLITICO Europe.

{kind=link}