It has been just over a year since DeepSeek shocked markets and its American rivals with the launch of a cutting-edge model. Since then Chinese AI companies have churned out one competitive model after another, proving their ability to keep up with OpenAI, Google and other leading U.S. tech companies.

But as AI makes its way from research labs to workplaces, households and phones, the competition is no longer just about creating the smartest model. “In the early years of the AI boom, the race was about designing more capable systems,” says Ryan Fedasiuk, a fellow at the American Enterprise Institute. “Now the capability is here and so the question is one of markets, of services, and of selling a product.”

To ensure the technology can be deployed at scale, companies and policymakers in China and the U.S. are increasingly looking at all the factors necessary for the AI sector’s development.

“Industrially, AI is actually essentially a five-layer cake,” Nvidia chief executive Jensen Huang told audiences at the World Economic Forum’s annual meeting in Davos in January. From financial services to healthcare, there had been a lot of progress in AI adoption in 2025, he said, adding that this was possible by other vital layers including models, chips and computing infrastructure, data centers and energy.

The U.S. is pouring large sums into AI data centers and equipment, while Chinese companies are scrambling to secure computing resources as the impact of the American export controls on semiconductors becomes more apparent. ByteDance, which runs TikTok and the AI app Doubao, is in talks with Korean company Samsung to develop AI chips designed in-house, Reuters reported last month.

…U.S. companies woke up to the importance of AI infrastructure earlier… Eventually a lot of Chinese companies were also trying to invest heavily… but, because of the semiconductor export controls, they were just more limited in the number of chips they could actually deploy.

Konstantin Pilz, a researcher at RAND’s Center for AI, Security, and Technology

“Which AI platforms are being used has direct implications for privacy, for data security and for national sovereignty,” says Fedasiuk. “To actually get to that point where more people are using your services, you need reliable input at different layers.”

A layer-by-layer review shows how China stacks up against the U.S. — and the chokepoints for each country.

ENERGY

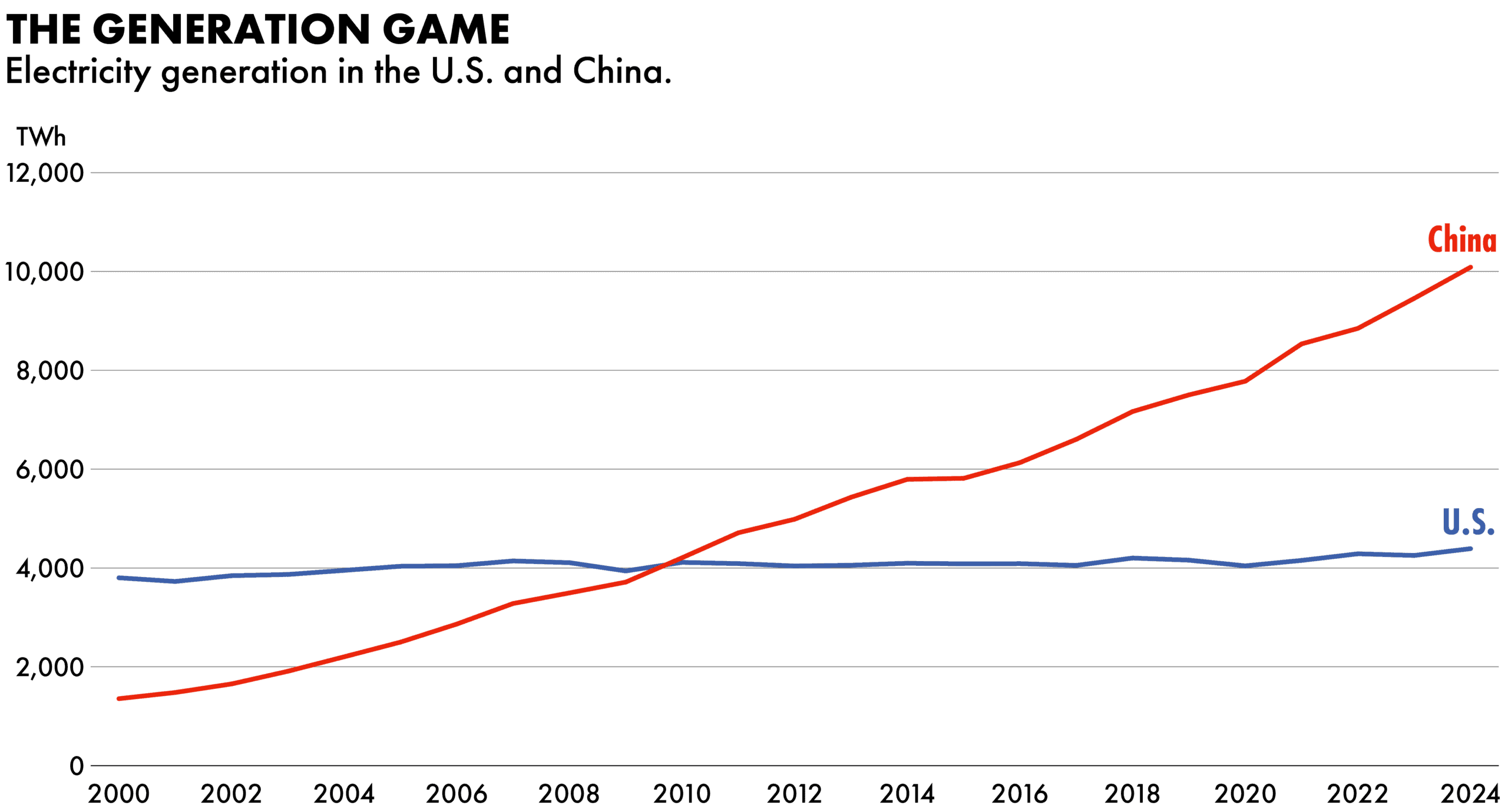

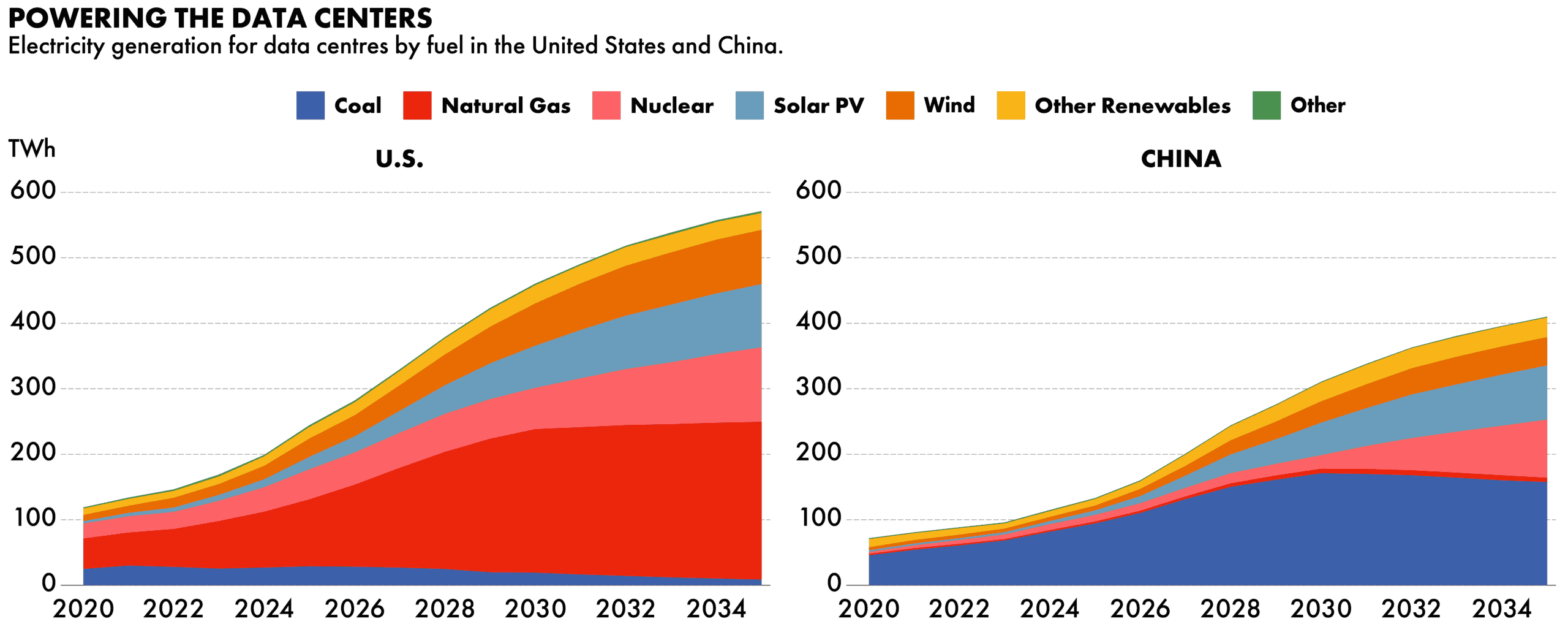

China holds the upper hand at the bottom layer — energy.

To meet growing demand for electricity, China has been ramping up its power generation capacity, particularly in renewable sources such as solar and wind. According to the National Energy Administration, China spent more than $500 billion on energy projects and added 543 gigawatts of new power capacity last year, double that of Germany’s total capacity.

Such aggressive expansion will help China meet rising demand from data centers. One recent study found that thanks to the investment in power generation, AI data centers will account for less than 10 percent of the country’s total power demand by 2030.

The U.S., by contrast, is facing what OpenAI CEO Sam Altman calls “an electron gap.”

In the U.S. power consumption by data centers is set to increase by 240 terawatt-hour (TWh) from 2024 to 2030, a 130 percent jump, according to the International Energy Agency. But with total energy production largely flat over the past two decades and red tape slowing the addition of new capacity, Morgan Stanley projects data centers in the U.S. may face a shortfall of about 49 GW by 2028.

Inside an Amazon data center (left) and inside a Google data center (right). Credit: Amazon, Google

OpenAI is among companies that have petitioned the U.S. government to upgrade the grid. This month, leading tech firms signed a pledge proposed by the White House, agreeing to cover the costs of securing additional capacity for their data centers in order to prevent price hikes for consumers and households.

But capacity alone doesn’t tell the full story. China’s advantage may not be as big as it seems, because of long-standing problems that affect the transmission of electricity.

China is hampered by institutional bottlenecks in the way that electricity is traded and utilized, says Anders Hove, a senior research fellow at the Oxford Institute for Energy Studies. “That is one of the reasons why, even with cheaper capital costs and low interest rates, electricity is not that much cheaper in China.”

INFRASTRUCTURE

Data centers host the advanced chips and computers that process large amounts of data to train AI models. And data centers running trained models, a process known as AI inference, have to be located near the models’ users to prevent delays.

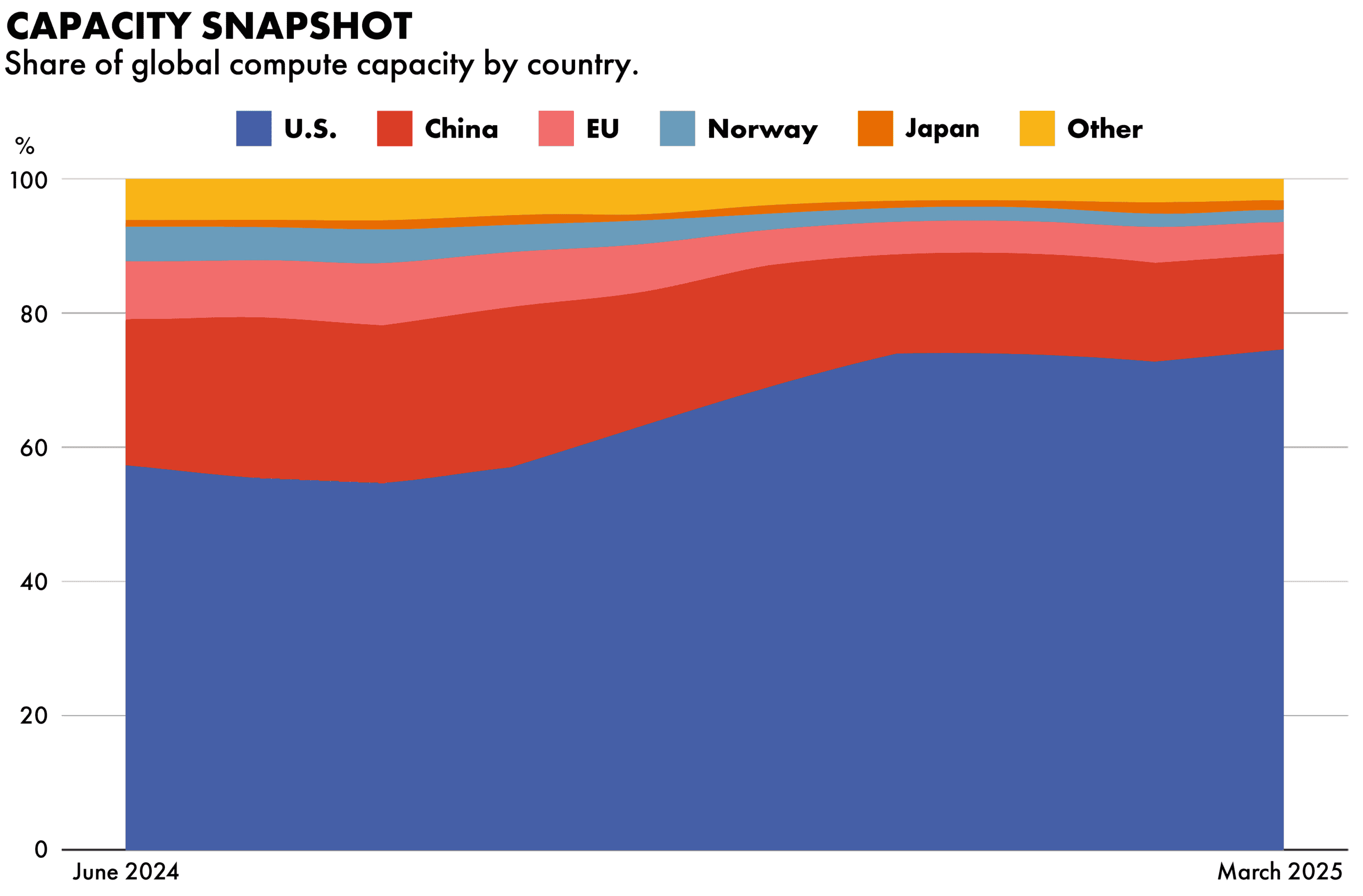

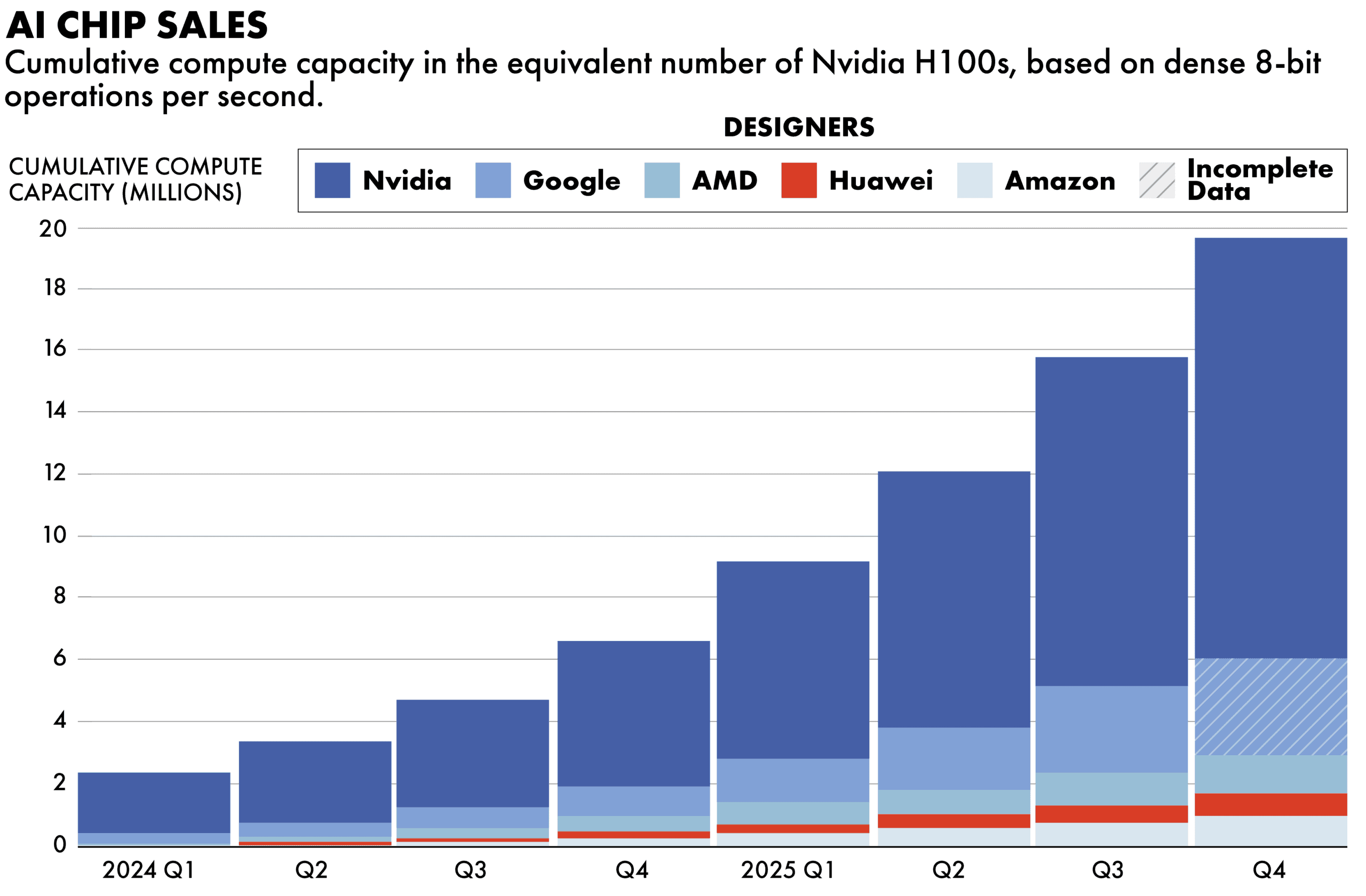

Several statistics underscore America’s lead in this layer. The U.S. is home to nearly 5,500 data centers, ten times more than China has, and hosted three quarters of the world’s computing power as of last May, according to a study by EpochAI, a San Francisco-based research institute. Its share has likely further increased since, says Konstantin Pilz, a researcher at RAND’s Center for AI, Security, and Technology who led the study.

“With ChatGPT, U.S. companies woke up to the importance of AI infrastructure earlier than Chinese companies,” Pilz says. “Eventually a lot of Chinese companies were also trying to invest heavily in AI infrastructure but, because of the semiconductor export controls, they were just more limited in the number of chips they could actually deploy.”

…based on all available indicators, I expect China will not be able to produce a sufficiently large amount of computational power on par with the U.S.-led ecosystem until at least about 2028.

Ryan Fedasiuk, a fellow at the American Enterprise Institute

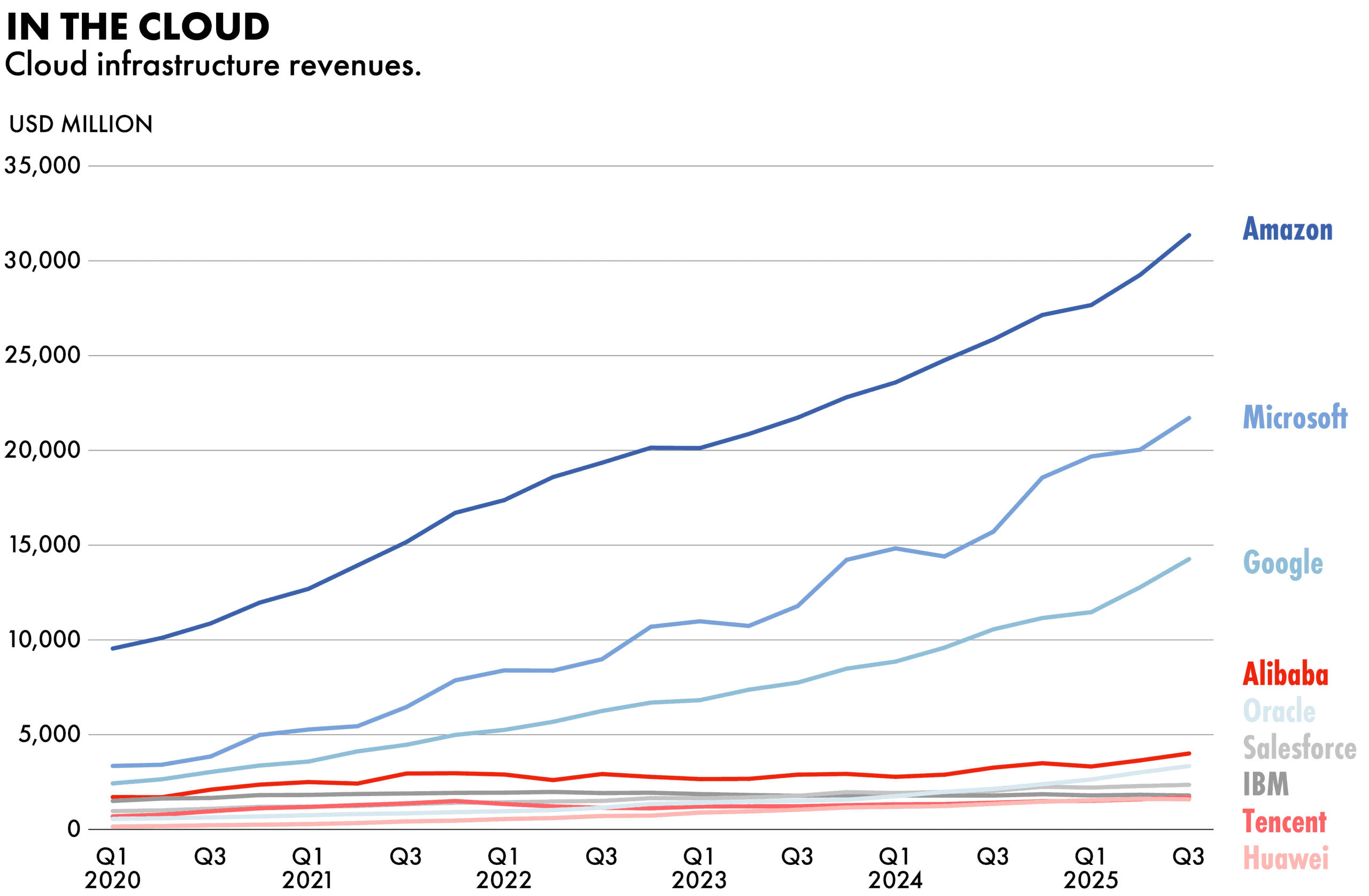

Chinese companies have also been slow to catch up because of financial constraints. While the cloud revenues of Chinese players, such as Alibaba and Tencent, are growing at double-digit rates, they are still a fraction of Microsoft and Amazon’s cloud revenues.

ByteDance plans to invest $23 billion this year on AI infrastructure, including chips, the Financial Times has reported. But the spending of Chinese companies is still no match for their American counterparts: capital expenditures by Microsoft, Amazon, Alphabet and Meta are set to reach $650 billion this year.

CHIPS AND COMPUTING POWER

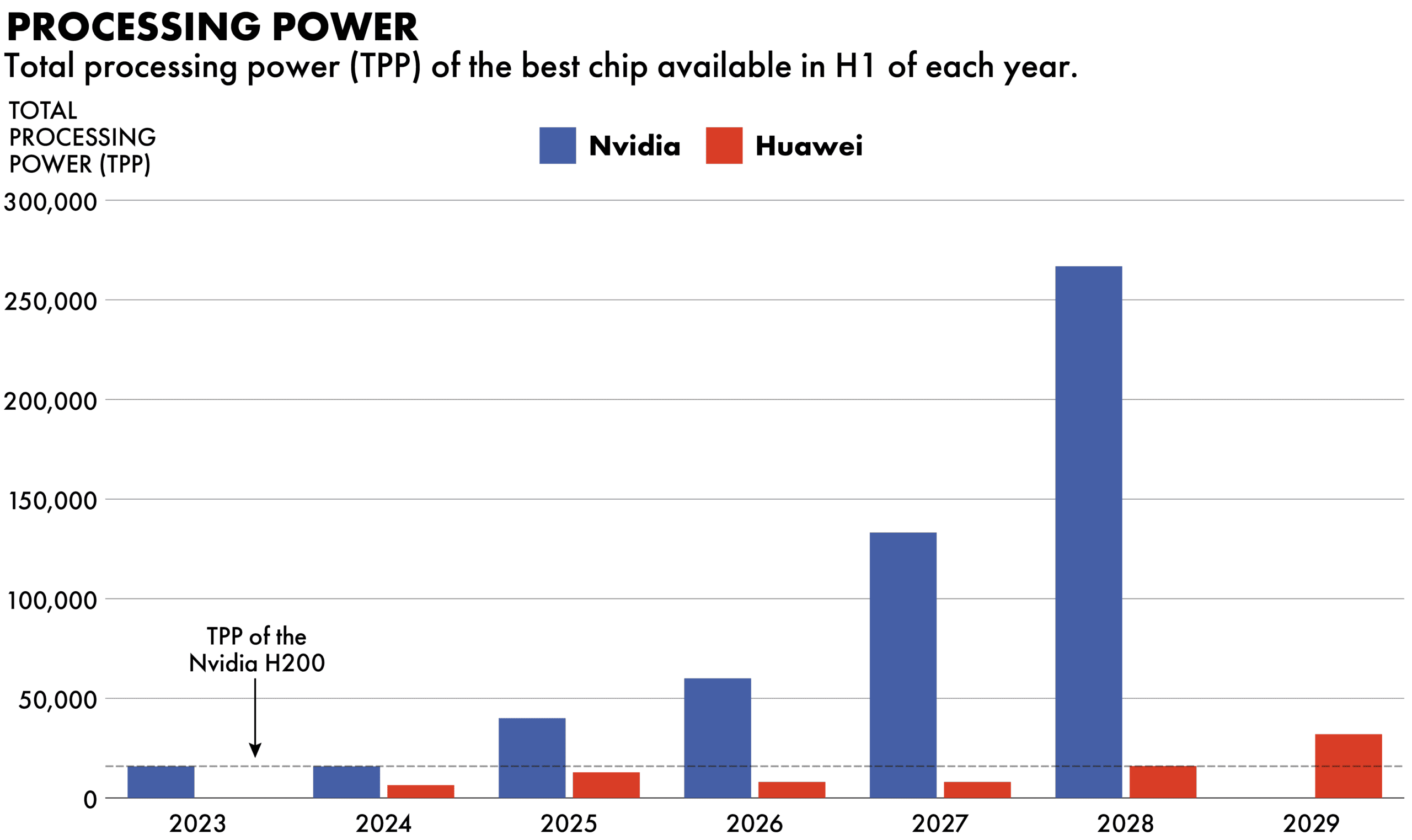

America’s biggest AI advantage over China is still in semiconductors, thanks to restrictions on the exports of advanced chips and equipment.

Despite Beijing’s push to reduce reliance on foreign technologies, the country’s most powerful chip available, produced by Huawei, still trails behind Nvidia’s in terms of both total processing power and bandwidth memory. The disparity in their performance will also increase substantially in the coming years, according to a recent study by the Council on Foreign Relations.

“Even if you assume that China can make millions of chips, it still only puts them at 1 to 4 percent of the U.S.’s computing power because the quality gap is so large,” says Chris McGuire, author of the study.

China’s chipmaking industry is, however, making steady progress towards self-sufficiency. State-owned Hua Hong Group has become the second Chinese company, after SMIC, to develop the capability to produce 7 nanometer chips, Reuters reported last week. Morgan Stanley estimates that by 2030, the domestic supply chain can meet 76 percent of the country’s demand for AI chips.

In the meantime, Chinese companies are also exploring different technical workarounds, including “stacking” chips to compensate for the performance gap or leasing data centers overseas. Some have even resorted to smuggling banned chips from the U.S. to China.

But, says Fedasiuk, “based on all available indicators, I expect China will not be able to produce a sufficiently large amount of computational power on par with the U.S.-led ecosystem until at least about 2028.”

Computing shortfalls have also become more acute for Chinese AI companies. The popularity of ByteDance’s new video tool, Seedance 2.0, took off recently, but the model is struggling to meet users’ demand and now can take hours to process requests. Similarly, Beijing-based Zhipu issued a desperate call for compute providers last month, after users’ complaints about long delays and usage limits sent its stock price plummeting. Some tech executives have submitted proposals at China’s annual parliamentary session last week, calling on the government to help secure more computing resources for AI inference.

MODELS

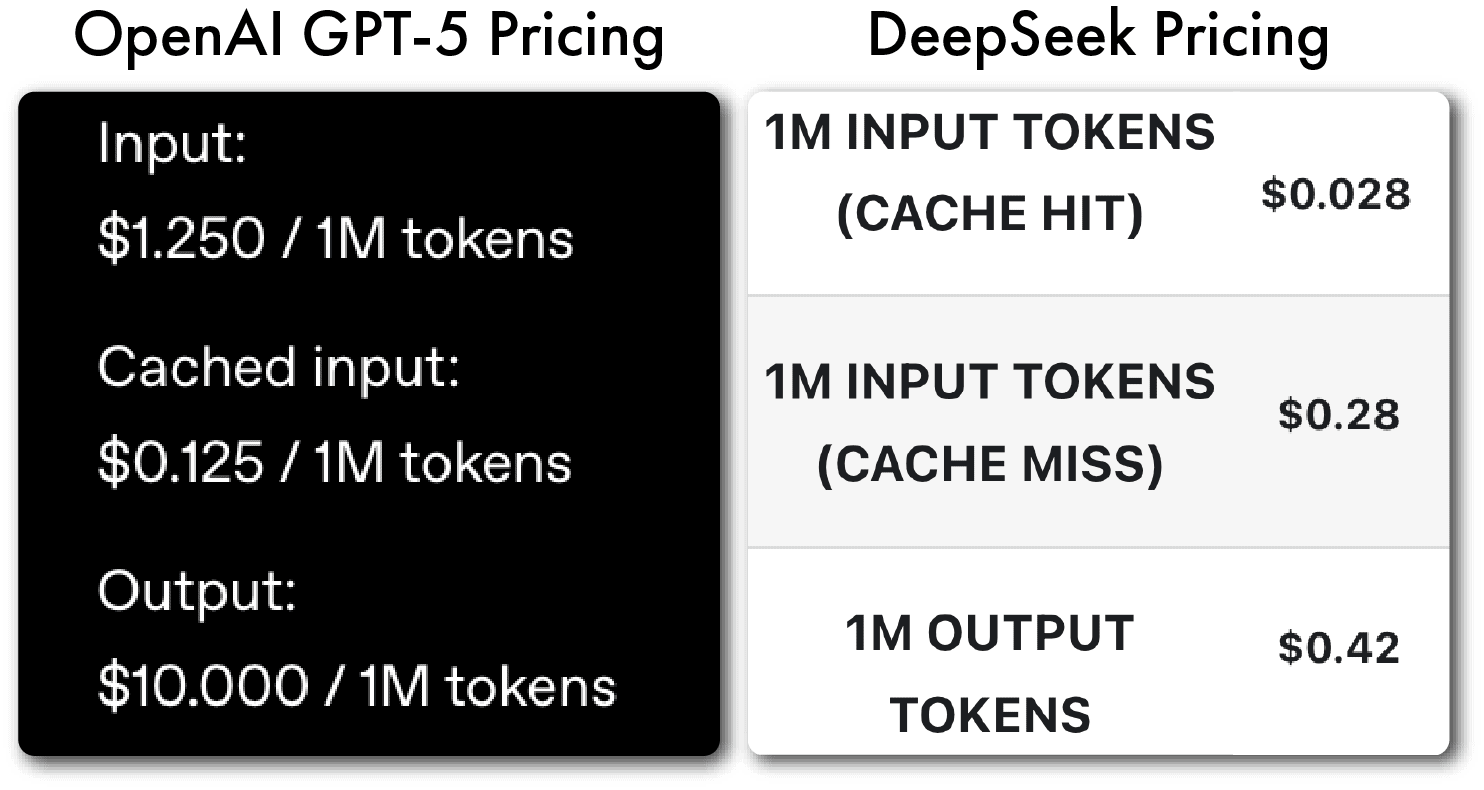

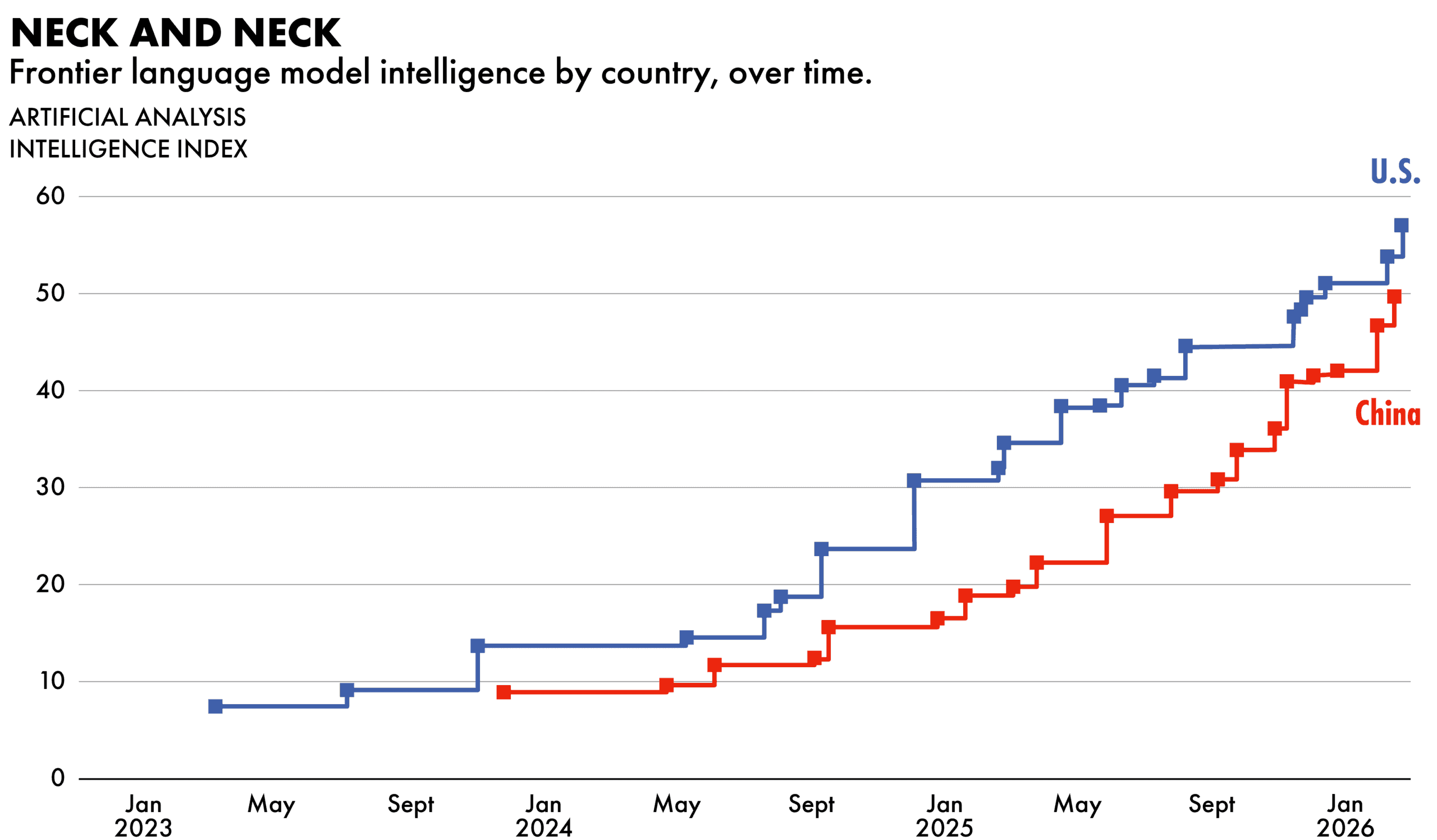

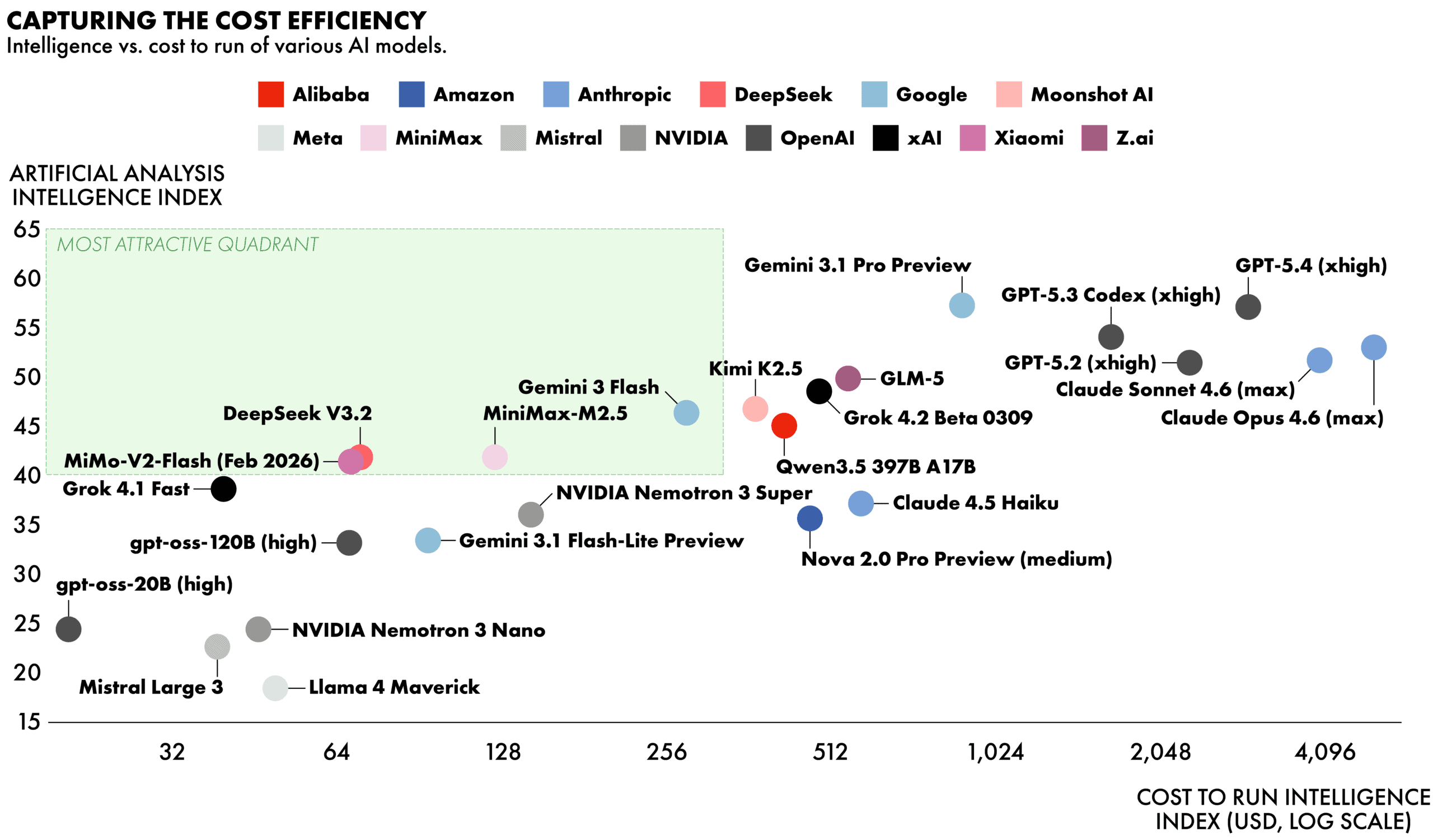

In spite of the relative chip scarcity, Chinese companies have several tricks up their sleeves. DeepSeek flipped the script last year with the launch of a model trained at a fraction of previously assumed costs. It made algorithm advances that allowed it to train smaller models more efficiently — an approach other Chinese AI startups are also adopting.

“The idea is to squeeze more performance out of limited compute power to get good enough models that don’t cost as much on the inference side either,” says Jeffrey Ding, an assistant professor of political science at George Washington University.

OpenAI and Anthropic have also recently accused Chinese companies, including DeepSeek, of “distillation” — a technique that involves training a new model on the output generated by another more sophisticated model. It allows DeepSeek to “free-ride on the capabilities developed by OpenAI and other US frontier labs,” OpenAI alleged in a memo to the Congressional Select Committee on China last month.

“That is partly why we see that China is not quite at the frontier, but they are at least keeping pace, maybe three to six months behind,” Pilz says.

Chinese companies are also competing on price. They generally charge less than leading companies in the U.S. for usage and subscriptions to proprietary models.

In addition, they have doubled down on open source models, which users can download for free and run on their own computers. The open source approach has helped Chinese ecosystems develop quickly and is contributing to the rapid adoption of Chinese models around the world.

“The open question is whether it will translate into revenues,” says Ding. “The bet on open source is that you build a community of people who are invested in your approach, and then eventually you offer paid integrations.”

This is an urgent challenge for Chinese AI companies, which are under pressure to generate tangible returns and justify their outlays. Junyang Li’s recent departure from Alibaba has highlighted the tension between technical and commercial goals. Li, a star researcher, was a powerful advocate of the open source strategy.

APPLICATIONS

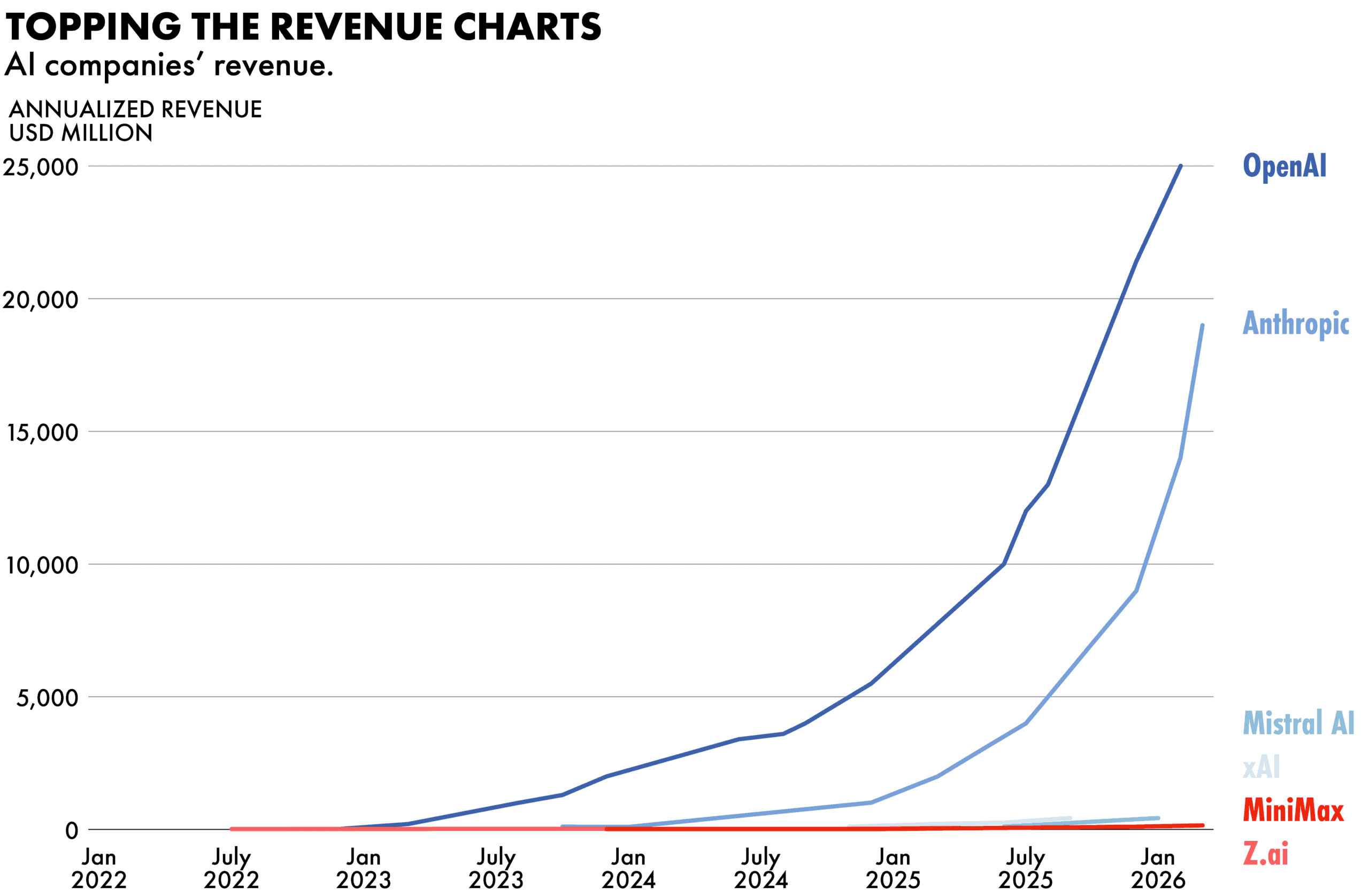

On OpenRouter, a U.S. platform that makes large language models available to millions of developers, Chinese companies in February surpassed their American rivals in terms of token consumption, which measures the amount of data processed by AI models. It is one indicator of the growing popularity of Chinese AI models.

However, U.S. companies continue to dominate in terms of revenues generated as they have more enterprise clients and other paying users.

As AI becomes a general purpose technology similar to electricity and the internet, what matters most is its macroeconomic impact and contribution to productivity growth, Ding says. “So the [best] adoption metrics are — regardless of where the technology is coming from — who is actually integrating and deploying AI across different sectors at scale.”

It appears that China is embracing AI with more enthusiasm than the U.S. and many other countries. Surveys have found that Chinese users are more optimistic than their global peers about the future of the technology. In recent weeks, for instance, people across major Chinese cities rushed to install OpenClaw, an open source AI agent, on their devices even as authorities warned of cybersecurity risks. The craze lifted the stocks of Chinese AI companies such as MiniMax and Zhipu, which are supporting the deployment of OpenClaw and have also launched their own AI agents.

The key is whether such phenomena can lead to sustainable adoption that boosts productivity. Ding argues that China’s ability to promote widespread AI use trails behind that of the U.S., citing metrics such as the much lower adoption rates of cloud computing and industrial software.

“Diffusion is about the spread of a technology across the entire country, not just what’s happening in Beijing, Shenzhen and Shanghai,” Ding says. “Can those frontier advances from top firms and universities travel to the small business in Qinghai province? That path is going to be more difficult in China than it is in the U.S.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.