Nicholas Borst is director of China research at Seafarer Capital Partners, a California-based investment adviser focused on emerging markets. Previous to that, he was a senior analyst at the Federal Reserve Bank of San Francisco covering financial and economic developments in Greater China and the China Program Manager and a Research Associate at the Peterson Institute for International Economics. His new book, The Bird and the Cage: China’s Economic Contradictions, explores the tensions between state control and market forces in China.

Illustration by Kate Copeland

Q: Let’s start with the bird and cage metaphor that inspired the title of the book. What is its origin, and what does it mean?

A: It’s a quote that goes back to Chen Yun, one of China’s most important reformers at the start of the reform and opening period, maybe second only to Deng Xiaoping. It stuck with me for a long time as a powerful metaphor to understand China’s approach to managing its economy — this country, led by a party that calls itself communist, that is embracing various types of market reform, permitting private enterprises alongside a continued strong role for state-owned enterprises, and lots of government intervention across the economy.

For me, the bird in the cage metaphor shows that the Communist Party understands the power of markets and the need to utilize elements of capitalism to achieve China’s own national goals; but at the same time sees markets as a potentially very dangerous tool that could have all kinds of negative side effects on the economy or their own rule.

There’s always been this constant balance of trying to utilize the market while also trying to control it. The bird represents the economy and market forces needing space to grow and to fly: you can’t grip it too tightly or you could crush it. But at the same time, you can’t let the bird escape freely, because that would have negative economic and social consequences that the party wouldn’t like. It’s an illustrative metaphor of an approach that has persisted across multiple decades and multiple Chinese leaders.

To use the same metaphor, where is China right now? We know Chinese President Xi Jinping has been reasserting state control, but at the same time, his meeting with private entrepreneurs earlier this year was seen as a sign of change.

There is a bit of a recalibration going on right now. The cage almost crushed the bird in 2020 and 2021, with all the different crackdowns on tech and real estate, and broader retrenchment for the private sector. It got to a point where it had a major impact on growth. So we are seeing a rebalancing, to some extent, by Xi and the party more broadly, where they’re talking more positively about the private sector and the importance of entrepreneurs.

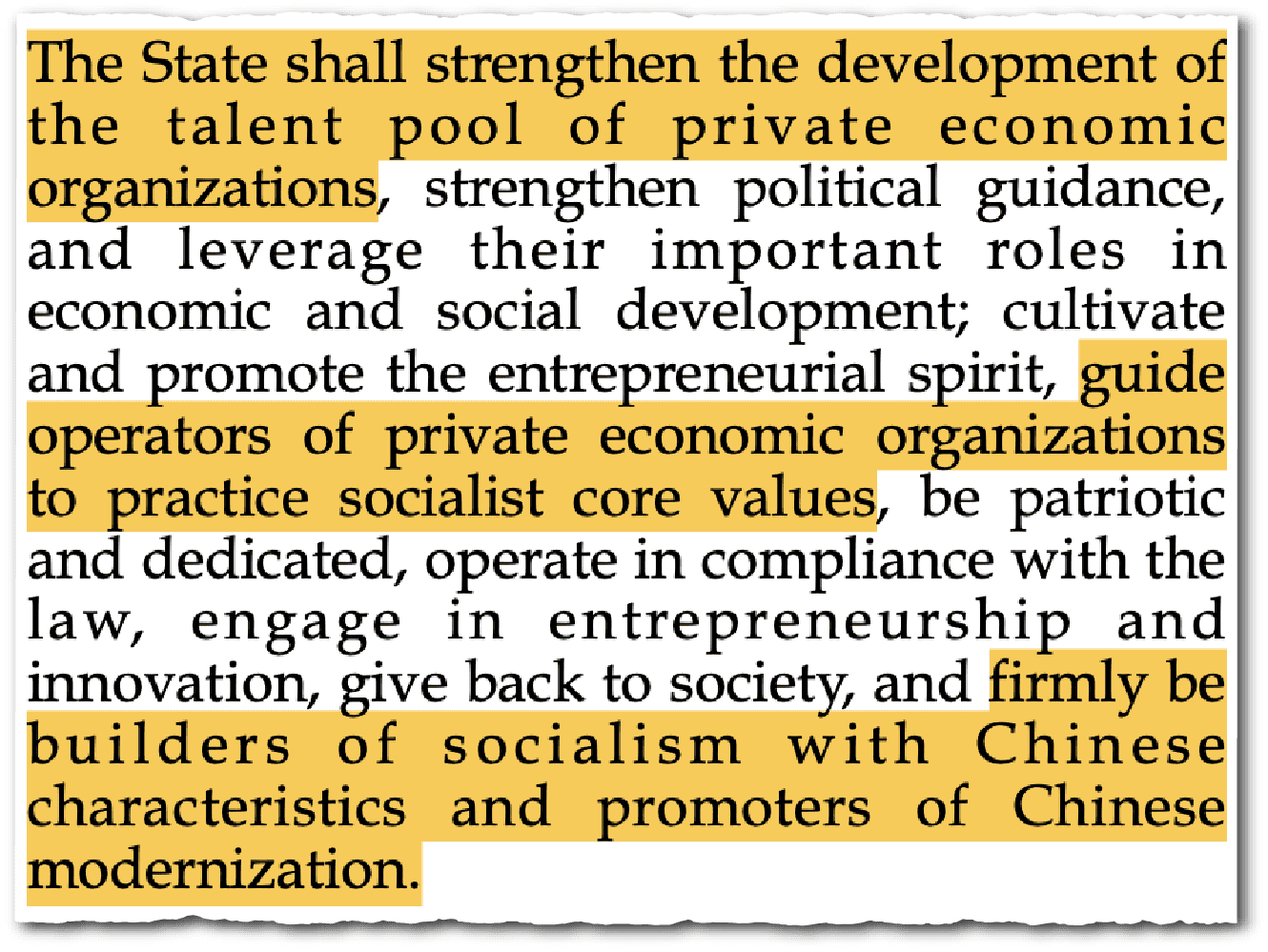

But it is much more of a tactical rebalancing, not a fundamental shift. A lot of the issues that the private sector was complaining about ten years ago are the same today. The government is doing things like the private sector promotion law, which is a step in the positive direction. But I don’t see any fundamental shift from the view that the private sector needs to be guided by the party, the direction of the economy needs to be set by the party, and that companies and entrepreneurs who push against that direction are going to face Beijing’s wrath.

What is Xi’s vision of the economy and in what ways is it different from the readjustments his predecessors had made?

A lot of this comes back to the third plenum in 2013, which was such a central event. It was the first time we heard Xi’s economic agenda. There was so much hope and excitement about a new generation of Chinese leaders, one that was more cosmopolitan and had worked in the coastal provinces where all the reforms that had been going on. When the third plenum agenda came out in 2013, many of us, including myself to some extent, got it wrong.

We saw in the third plenum what we wanted to see, focusing on the new reforms that were being announced, and we tended to minimize the statements about the necessity of the government to guide the economy, and of having strong state owned enterprises that play key roles in the economy’s commanding heights. That event, and the misinterpretation of that policy agenda, in some ways set the course for where we are now. There was this sense of almost a whiplash, when [Xi] turned out to be much more state focused than anticipated. It led to this fundamental sense of imbalance among a lot of China analysts, and to people asking: did we get China wrong?

Part of the motivation for this book was to go back and see if I was looking at these announcements with rose-colored glasses, or whether I was actually reading and understanding what Chinese policy makers were saying. I found some really important through lines to back up this ‘bird in the cage’ framework of a government that has recognized the importance of economic reforms and the market, but also never gave up its intention of controlling and guiding the economy. That through line runs from Xi all the way back to his predecessors.

Where does that leave the private sector in China right now? How is sentiment and what are the main issues companies are facing?

There’s been a shift towards more positive rhetoric around private companies and at the margin, that’s good. But it doesn’t change the fundamental issues that private companies are facing, which is a very uneven playing field when they compete with state owned enterprises. State owned enterprises have regulatory advantages, and other advantages in access to capital and government support.

One of the examples that has been talked about for a decade is just getting SOEs to pay private companies on time. SOEs have all these suppliers that are private companies, and they basically refuse to pay them, or they do so in an extremely delayed manner. It sounds small and trivial, but it gets to a very core issue of whether there is rule of law in China. Can a small private company take a big SOE to court and get a judgment enforced for payments of arrears? A lot of the evidence shows that that’s still very difficult in China. Otherwise the authorities wouldn’t have to be constantly telling SOEs to pay their bills and having rules related to this constantly come out.

If a company like DeepSeek is given a runway, they’ll have the potential to do amazing things. But if they start doing things that make Beijing feel like it doesn’t have as much control as it wants, or Beijing perceives as creating economic and social instability, then you would see the cage come down.

A second issue is when private companies get too big or too influential, when does the cage come for them? At what point will they face pressure to set up a party committee within their company? At what point do they have to talk with regulators about actions they may be taking? There are all these different tools that Beijing can use to clip the wings of private companies that are getting too big.

So there’s a dual problem for private companies of having to compete with SOEs at a disadvantage; and then even when they succeed, still facing this government scrutiny. Even though the private sector is now the largest part of the Chinese economy and the dominant source of growth, it’s still being restrained by government policies from what it could be.

How about the SOEs themselves? There have been attempts to reform them. How have those efforts panned out?

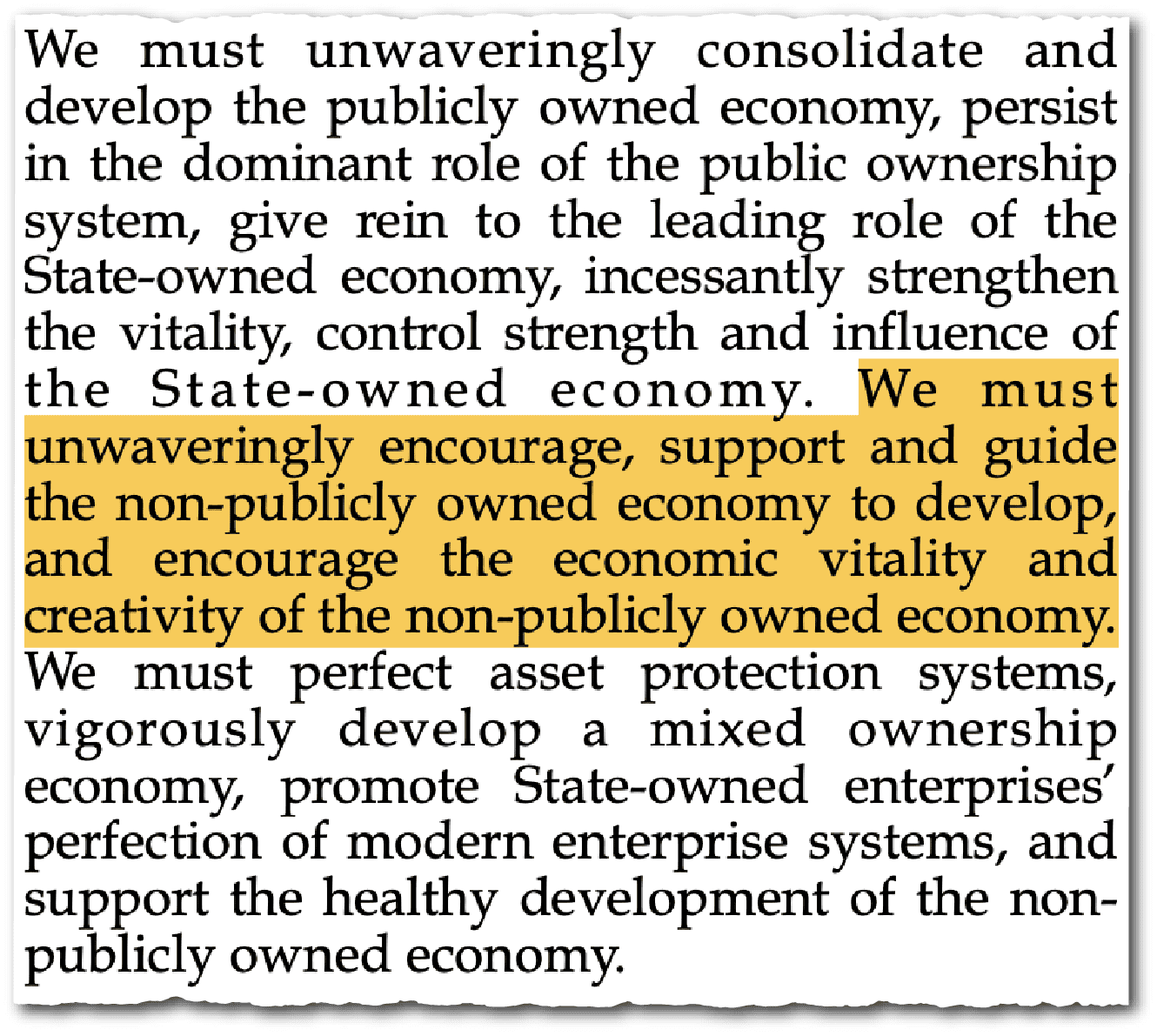

There is a recurring issue, particularly with Xi’s SOE reforms in 2015, of a real reluctance from the government to allow SOEs to go out of business, or be displaced by private firms. In response to SOEs struggling and being inefficient, there’s been a series of different campaigns meant to improve them and have more market-oriented practices put in place. But when the rubber hits the road, a lot of what we actually see is the authorities taking a weak SOE and merging it with a stronger one to make an even bigger conglomerate. Across industries where SOEs dominate, that has been the mode of action — making SOEs bigger, better, stronger, to basically avoid them being utterly displaced by private companies. If all these amazing private companies were able to compete on a level playing field, they would probably mop the floor with a lot of these SOEs, and the SOEs would be pushed out.

These government interventions are intended to prevent that from happening, because SOEs are still seen as very important implementers of government policy. When policies like the Belt and Road Initiative come out, or the semiconductor push, SOEs are often the most enthusiastic supporters. SOEs are also important stabilizers. When the economy is volatile, they don’t fire large numbers of employees. They will spend counter-cyclically, and so they are viewed as a crucial lever of control for the party over the economy.

In a recent blog entry about state-owned companies’ performances, you crunched the numbers. What did you find from that?

China now has a vast number of listed companies. The data they produce is pretty good, especially relative to other sources of Chinese data.

Left: Alibaba’s debut on the Hong Kong stock exchange, November 26, 2019. Right: Tencent Music Entertainment rings the opening bell to mark its NYSE listing, December 12, 2018. Credit: HKEX, NYSE

What can we learn when we look at it? It was very surprising to me that even after this tremendous growth of the private sector, to see how entrenched SOEs remain, particularly in several industries. The metric I was using was profits. If most of the profits in an industry are being captured by state owned companies rather than private companies, that’s a good proxy for an industry where there’s not a lot of competition between private companies and SOEs. There are still many major industries, whether it is real estate or finance or energy, where the vast majority of profits are still being claimed by state companies.

As you mentioned in the book, another constant calculation for the Chinese government is between the need for innovation and the need for control. How have we seen that play out?

It’s fascinating to watch because China has so many innovative companies. There are brilliant Chinese scientists, entrepreneurs, and a whole list of different Chinese companies that may have started out as copycats, but then have quickly progressed up the value chain, started developing their own technology and IP, and are competing globally.

The problem, though, is that they often run smack into controls imposed by the government. It’s not universal. There are many sectors that are not so important or strategic. Beijing is not particularly concerned about developments in the textile industry, other than to the extent it may impact employment. But there are other sectors, such as media or finance and payments, which are key channels for the flow of information or capital, and so these sectors have become very sensitive.

There are a series of examples of private companies that got too influential. Ant Group and Tencent, for instance, are innovative firms that were developing new financial ecosystems built around payments, but were also extending into micro credit, lending to SMEs, and credit ratings. They even started offering financial products that were direct competition to the state controlled part of the financial system.

Beijing has a different approach to managing its economy than the U.S. does. And that’s the heart of the conflict between the two countries. The ability for us to actually force China to change is pretty limited.

This was a clear example of private players competing directly with the state banking system, taking market share from the state banks, essentially reducing them to peripheral players — and as a result, Beijing did not have as much transparency into the financial flows as it would have liked. That all fed into a direct, very draconian intervention from the authorities to bring these firms back into line. They were called before regulators, forced to essentially engage in self-criticism, investigated, forced to restructure their businesses and in some cases, sell off parts of their companies. In some cases, the ownership table had to completely change, and at the end of the day, these companies faced dramatically reduced scopes of business and freedom of action. They’re still doing cool and innovative things, but their ability to actually change the status quo within the financial system has been substantially reduced.

An example of DeepSeek’s chatbot in action.

Has the rise of Chinese AI company DeepSeek forced Beijing to recognize afresh the importance and innovativeness of private companies?

DeepSeek is an example of China’s capacity for innovation, even in the face of technology transfer restrictions from the U.S. and others that were designed to slow down and potentially hinder China’s ability to develop AI. DeepSeek showed a lot of innovation, getting around those restrictions and making more from less.

It will be very interesting, though, to watch what happens to DeepSeek — a private company growing very quickly and operating in a very sensitive sector within China. To what extent does Beijing try to insert its levers of control over the company? Given it’s an unlisted company, we won’t get as much transparency about what happens to Deepseek. But it would be fascinating to know if they’ve been asked to set up a party committee and if it receives more attention from regulators.

That’s the key dynamic that’s at play — how far do they get to run? What is the scope for private companies to grow and expand and disrupt things? If a company like DeepSeek is given a runway, they’ll have the potential to do amazing things. But if they start doing things that make Beijing feel like it doesn’t have as much control as it wants, or Beijing perceives as creating economic and social instability, then you would see the cage come down.

Some argue that China’s top-down approach might be better suited to areas where you need long-term investment, such as quantum computing and nuclear fusion. Does that give China an advantage in innovation?

There’s a lot of literature on this and many people have acknowledged the advantages that come from the ability to plan and allocate funds long term and to clear away obstacles in the way that Beijing can when it’s motivated. Those are certainly quite significant advantages, but in terms of the economic impact, there’s really no substitute for the experimentation and flexibility of private companies who are taking ideas and running with them, developing new products, transforming whole industries, creating lots of disruption, but ultimately, driving forward economic growth and innovation.

It’s that latter part where I’m less convinced that China has huge advantages. The problem is that Beijing is so antithetical towards that type of disruption and private influence within the economy that they frequently hamstring private companies from reaching their ultimate potential. China certainly has some advantages, but the dynamism and creative destruction that’s necessary for true market-based innovation is facing a lot of resistance from the government.

Isn’t the rise of Chinese EVs in the domestic market and around the world a sign that they’re doing something right?

A lot of people would point to the Chinese EV industry and say that’s a success. From the perspective of wanting to reduce dependence on foreign automakers, to develop domestic brands, technology, and supply chains, they have done that. That’s quite commendable.

But this gets into another contradiction — that this push for self-reliance comes with some trade offs. The aggressive, determined approach to develop the domestic EV industry — which saw large amounts of subsidies and tax preferences and regulatory favoritism towards domestic companies — has produced a backlash globally, not just in the U.S., and Canada, but also Brazil, Turkey, the EU and India. Countries are basically saying, we want to put up some barriers to Chinese EVs because they were frustrated with the level of industrial planning and state intervention in the economy that created this great EV industry.

It’ll be very interesting to see how that works out because the Chinese EV industry is great, but it’s also facing some significant problems in terms of overcapacity. Many firms are not profitable. There’s going to be some real industry consolidation. One of the solutions is exporting to foreign markets, but they’re facing this backlash in large part because of the way the industry was created through industrial policy. The harder China pushes for self-reliance, the more it’s going to face a global backlash that threatens its ability to continue to trade and invest with the rest of the world.

Would it be accurate to say the core contradiction within China’s economic policy is that, on one hand, it wants and needs economic growth, and on the other hand, it also needs political control?

That’s exactly it. You can look at the entire reform and opening period as a constant adjustment between these two competing goals of wanting strong economic growth but being very worried about letting the market run wild. And so there’s constantly a kind of give and take, of relaxing for a period, allowing more reforms, and when that starts to produce some negative consequences, there are restrictions imposed and retrenchment of reforms. That’s a very important cycle that puts a lot of different Chinese economic policies in perspective.

What does all this mean for China’s economic trajectory?

That cycle of the ebb and flow of reform has broken down recently, where the relaxation that we might have expected to see after Covid, and after the tech crackdown, has come in much more slowly and at a smaller scale.

It really comes down to geopolitics. There’s a view held by Xi, and probably pretty prevalent throughout the entire party, that as long as China and the U.S. are in this protracted strategic competition, the tolerance for any type of risk, any type of challenge to the party’s control, any dependency on foreign countries for technology or resources, that all has gone down dramatically. There’s a much greater desire to focus on greater control, and much less willingness to relax restrictions and to let the economy and the private sector recover.

It comes down to the competition we’re seeing between the two superpowers and until that dynamic changes, it will have a major impact on the Chinese economy, where the government is leaning so hard into these goals of stability, control and self reliance that it is reducing the country’s growth rate significantly and pushing China onto a slower, less innovative, less globally integrated trajectory than it was even five years ago.

How does this affect China’s role in the global economy?

That is currently being debated openly. There’s this fundamental paradox between China wanting to be increasingly self-reliant, yet remain connected in the global economy, continuing to be the world’s largest trader and to access resources and technology from the rest of the world. Many countries, but most notably the U.S., are saying the current structure of the relationship is not working for us — we want you to rebalance your economy, we want to see less control over industries, we want a greater role for foreign companies within the Chinese economy, and we want freer flows of capital and information.

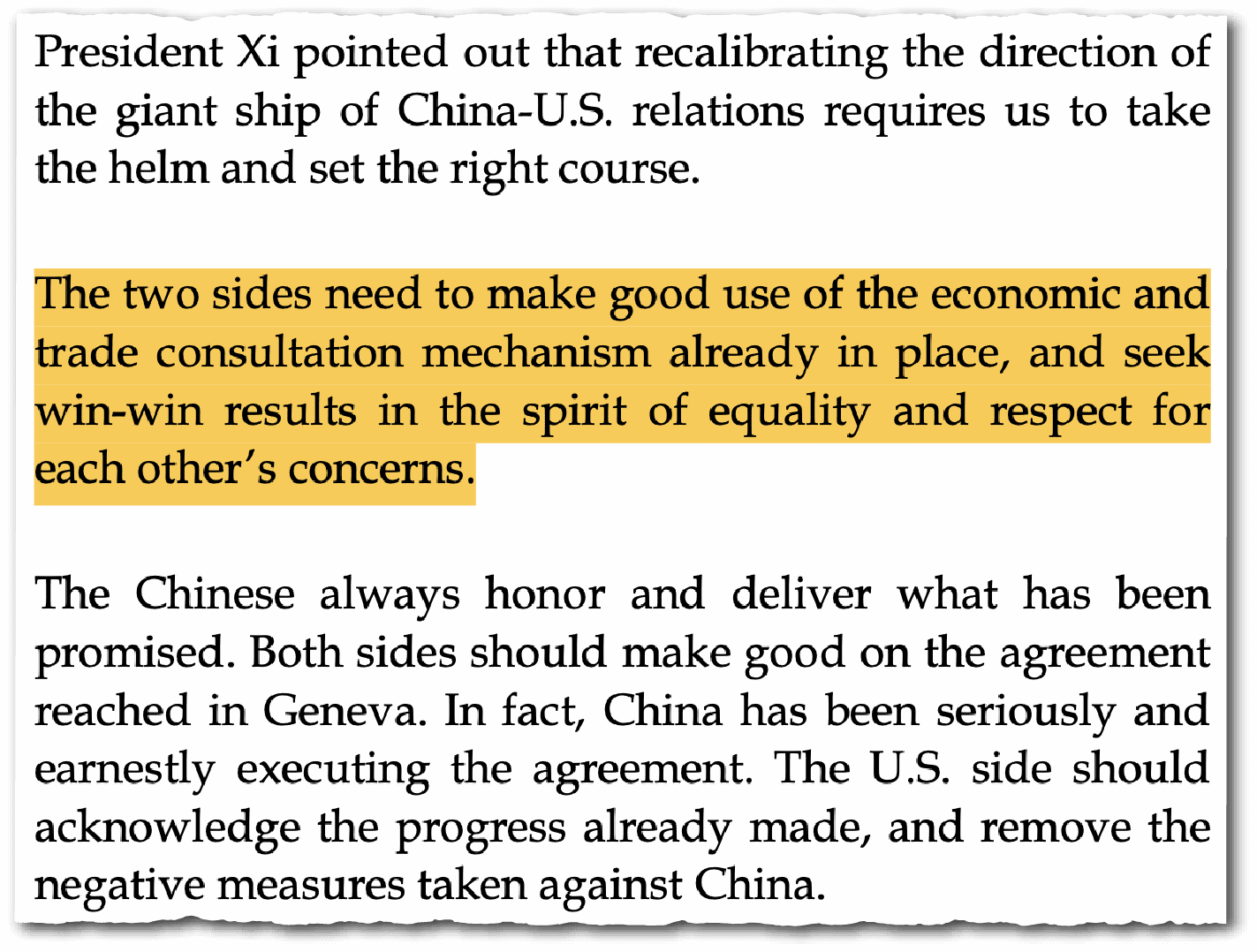

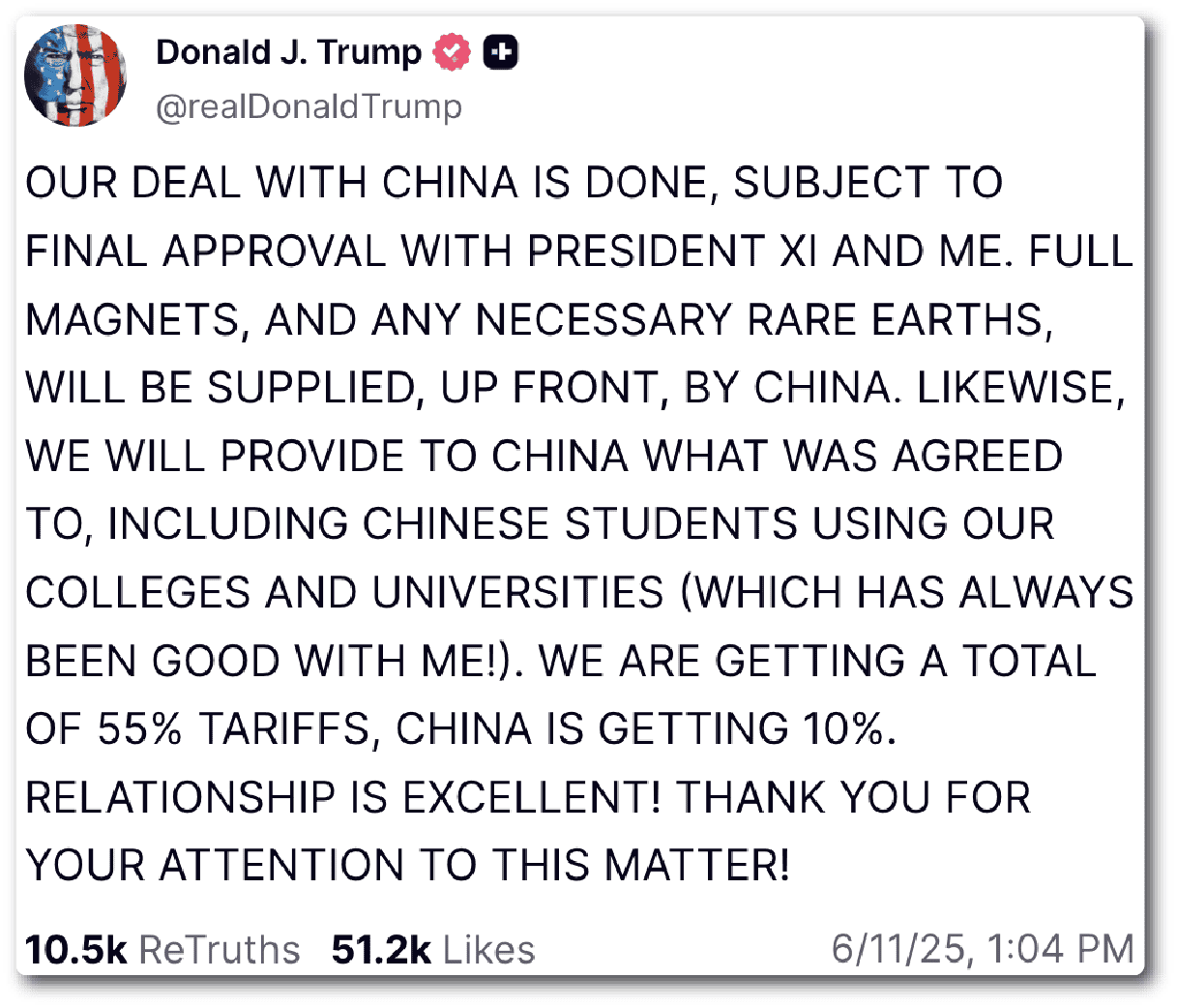

This is one of the reasons why it’ll be fascinating to watch the trade negotiations between two countries. Because the core conflicts that shape the U.S.-China economic relations are very difficult for Beijing to adjust course on. And in fact, Beijing may be looking at the most recent series of events and saying, we actually need to be more self-reliant: look at the types of pressure the U.S. can put on us when they want to, and how unpredictable and fickle U.S. policy can be.

It’ll be important to watch what is being negotiated — is it relatively superficial and technical things about trade barriers and market access? Or is it really getting to the much more structural problems that are at the heart of the current conflict — the way Beijing manages the economy and the level of intervention it has across different industries?

Is the trade war an inevitable result of China’s economic policies, and how do you expect China to respond over the longer term?

I don’t know if it’s inevitable, but it was predictable that the two sides would be on a collision course. Beijing has a different approach to managing its economy than the U.S. does. And that’s the heart of the conflict between the two countries. The ability for us to actually force China to change is pretty limited. This approach to managing the economy goes all the way back to Deng and so it’s decades and decades of consistent thinking about the importance of maintaining state control over key parts of the economy. That doesn’t mean that there can’t be any policy recalibration by Beijing, in a way that perhaps doesn’t settle all of our disputes and conflicts with China, but that may ease some of the more acute points of tension between the two countries.

That’s possible, but perhaps unlikely in the current environment, given the real lack of trust between the two countries. To have Beijing do a 180-degree turn and essentially pull back and give more play to the market seems like a tall ask. Even if that outcome is unlikely, it makes sense for the U.S. to try to negotiate for it because the alternatives of ever escalating economic conflict between the U.S. and China hurts both sides, and the potential for that economic conflict to spill into other types of conflict is even worse.

There’s a need for the U.S. to take action where it makes sense, to address its complaints about Chinese trade and investment patterns, to protect industries that are important in terms of national security, but also to give space for China to recalibrate its own policies, and to see if the balance between economic restriction and reform might shift again and help put the economic relationship between the two countries on a better path.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.