A non-resident senior fellow at the Harvard Kennedy School, Paul G. Clifford has worked in China since the early 1980s, with stints at The First National Bank of Chicago (now JP Morgan Chase), consultancy Oliver Wyman, and the U.S. network company Cisco Systems respectively. He profiled Huawei in his last book, The China Paradox: At the Front Line of Economic Transformation (2017). He co-wrote his newest book, China’s Logistics: From Laggard to Innovator, with industry veteran Christopher Logan, drawing from his experience advising state-owned firms on their restructuring and foreign firms on market entry into China.

Illustration by Lauren Crow

Q: Logistics isn’t an industry that gets a lot of attention, but as you point out in the book, it’s the backbone of any economy. Why is it so important, and what role did it play in China’s rise?

A: There’re a lot of good reasons why China’s logistics are incredibly important and why the government realizes that. The first is it increases economic efficiency and productivity and drives towards a better GDP. China’s logistics still account for about 15 percent of GDP, compared with 7 percent in the U.S., so there’s massive room for improvement. China is a heavily manufacturing-oriented country, which probably should have more logistics costs, but that gap is still very large.

The other thing that stands out is the ability of logistics to address the green agenda. This is a big opportunity because transportation of goods, whether it’s trucks, air cargo, or container shipping, accounts for an awful lot of green-house emissions. Thirdly, a big aspect of logistics is that the capabilities of China-owned logistics firms power the trade that flows through the Belt and Road, but also into the broader economy. And that cannot be underestimated.

| MISCELLANEA | |

|---|---|

| FAVORITE BOOK | Frantz Fanon, The Wretched Of The Earth |

| FAVORITE FILM | All We Imagine As Light |

| FAVORITE MUSICIAN | Bob Dylan |

| MOST ADMIRED | Nelson Mandela |

And then, of course, the Chinese economy under the Mao years was actually poorly integrated because of the dysfunctional centrally planned economy. The workaround was to create lots of sub-scale capabilities at the local level. What’s happening with modern logistics is that it’s enhancing the integration of the nation, while also addressing the well-being of the Chinese people by bringing some of the poorer people into the economy. Those are some of the things that make the government realize that China’s logistics improvement is a priority.

How did you first get involved in the industry and what’s the vantage point from which you wrote this book?

I studied in China during the Cultural Revolution, but I started working in China in the early ’80s, just as the reforms were beginning. I worked with countless foreign firms seeking to establish manufacturing facilities. The most challenging and intractable issues were the dismal state of Chinese logistics, whether it was getting inbound materials and parts or getting the finished product out into the market.

Even around 2000, when I was working with a series of state owned enterprises, such as Sinotrans and the land-based business of COSCO Shipping, to help them restructure, we found that China’s logistics still were not really meeting the demands of the new post-reform economy. I was also elected as the executive director of the China Federation of Logistics and Purchasing, so I got to see it very close up at that time.

I wanted to share with people what is really a rather under-explored subject. Logistics isn’t very fashionable. It’s seen as rather dirty and grimy, but actually it’s a very interesting industry with a lot of innovation going on. This industry is also an example of how China has a hunger to embrace foreign ideas and concepts. China really took this on board very completely.

On social media, you can often see viral clips showing robots sorting and moving packages at Chinese warehouses. Is that level of automation the norm? What kind of innovation is happening in the Chinese industry?

Those clips you saw are an example of the cutting edge of what’s going on, and much of that is amongst e-commerce and the private companies running that. That is the area where China is out-innovating the rest of the world — firms like UPS, FedEx and DHL. In the technology deployment, China has caught up very fast, and is now, in some respects, innovating.

IT systems sit at the very core of the logistics firms, integrating the flow of goods and representing a key factor for competitive success. Chinese logistics firms have their own proprietary IT platforms, including transportation management systems, which control a wide range of functions, including using AI algorithms for transportation scheduling.

Some of the robots you’ve seen online are in smart warehouses. These warehouses can reduce labor costs by 70 percent. And robots and AI allow them to adjust all the time and improve without human intervention. These robots are assembling products, packaging, sorting, palletizing, stacking, and retrieving goods.

There are plenty of smart warehouses in the rest of the world. But in China, the warehouses used to be appalling, wet and damp. There were rats, lots of theft, and they were very inefficient. So China has come a long way. UPS handles about 5.6 billion packages in one year. China’s e-commerce logistics firms handle over 1 billion packages on Singles Day [an online shopping festival every year on Nov. 11]. That puts it in perspective.

Who are some of the notable Chinese players? How are they shaking things up and are they doing it elsewhere as well?

China’s logistics firms in the international market are mostly focused on serving Chinese clients. None of them have emerged as full global players like the German firm, Kuehne + Nagel, or FedEx. It’s difficult for them to establish themselves in Europe and North America due to a range of issues, such as knowledge of local regulations, market conditions, their reputation, branding and recruitment. Interestingly enough, some of those issues that they face outside of China mirror the issues that foreign logistics players face in China.

But there are Chinese firms trying to create a footprint in the rest of the world, and they’re doing it through acquisition. Sinotrans, for instance, has made a major acquisition in Europe, and China’s sovereign wealth fund CIC has acquired a large warehousing company in Europe called Logicor.

Getting to the companies that you’re really interested in: In 2013, Alibaba’s Jack Ma established Cainiao with the daunting goal of fulfilling e-commerce orders in China within 24 hours and the rest of the world within 72 hours. Today Cainiao has a turnover of around $11 billion. And actually about $8 billion of that isn’t even with Alibaba. It’s with other customers. The 24 hours within China is a reality. The 72 hours is not there yet, but they have logistics hubs in Liege in Belgium, and Kuala Lumpur [in Malaysia]. And they handle about 4.5 million cross border items daily. So they’re going overseas already.

SF Express is another really great company that we looked at. They want to create a global reach and they took a big step forward in 2012 when they spent over $2 billion to acquire Hong Kong’s Kerry Logistics. They said, ‘frankly, we don’t have a global footprint at this moment. We are in about 20 percent of the countries that DHL and FedEx are in.’ So they knew they weren’t there yet. SF Express has done bold acquisitions, alliances and heavy investments in aviation and air freight. Just like FedEx, which invested heavily in a fleet of aircraft, SF Express has invested heavily in an air cargo fleet, which now has over 87 aircraft flying on 10 international routes and 50 domestic routes. And they also have China’s first professional freight airport, which they actually own and run, which is unusual since other airports are mostly government-owned in China.

So Chinese companies are making progress in their global expansion. Do you see them becoming a formidable competitor for the likes of FedEx and DHL? And vice versa, are these foreign companies also gaining ground in the Chinese market?

Chinese logistics companies in China are quite capable of meeting the needs of multinational corporations. That’s new. But in the rest of the world, they are primarily — not exclusively — serving Chinese manufacturers and shippers. There are very few large Chinese multinationals all over the world in the way that American and European multinationals operate. They don’t have that reach around the world with global customers in the way that DHL and FedEx do. So they are still relatively limited in their focus.

The issues that Chinese companies have in the world mirrors what’s going on in China for firms like DHL and FedEx. China was very late in opening up to foreign direct investment into logistics. That may be because transportation is viewed as highly sensitive in terms of national security. But also, the Chinese government valued manufacturing more than logistics, so they missed out on doing this early on. It took four years after WTO accession for China to permit foreign companies to own 100 percent of a logistics firm in China. That forced foreign firms to form joint ventures. FedEx, doing cross border business, had to partner with a Chinese firm. And in 2007, it cost them $400 million to buy out their Chinese partner and gain control. So this was painful.

…the large multinationals and the logistics firms that work with them have great vested interests in the existing supply chain. There’s a lot of inertia around that supply chain, which they’ve constructed over decades. And while there will be some changes, it will be partial.

And in the domestic market — the intra-China market — foreign firms find it very hard to negotiate bureaucratic red tape and legal or illegal tolls, charges levied on trucks and things like that. Chinese firms face those complications too, but for foreign firms, it’s even worse.

A good example of a foreign firm doing well in China is DHL. In 1986, it formed a joint venture with Sinotrans in cross-border logistics and that firm is still running very successfully and profitably. DHL also formed other types of joint ventures in China to address the domestic market, and those ones did not succeed. So there are positive examples, but it’s much harder for foreign firms than it is for Chinese firms, which have great local advantage.

The use of air freight by Chinese e-commerce companies like Shein and Temu is quite controversial. People have described it as a logistical nightmare. There’s a lot of criticism about its sustainability. How do you think this will play out?

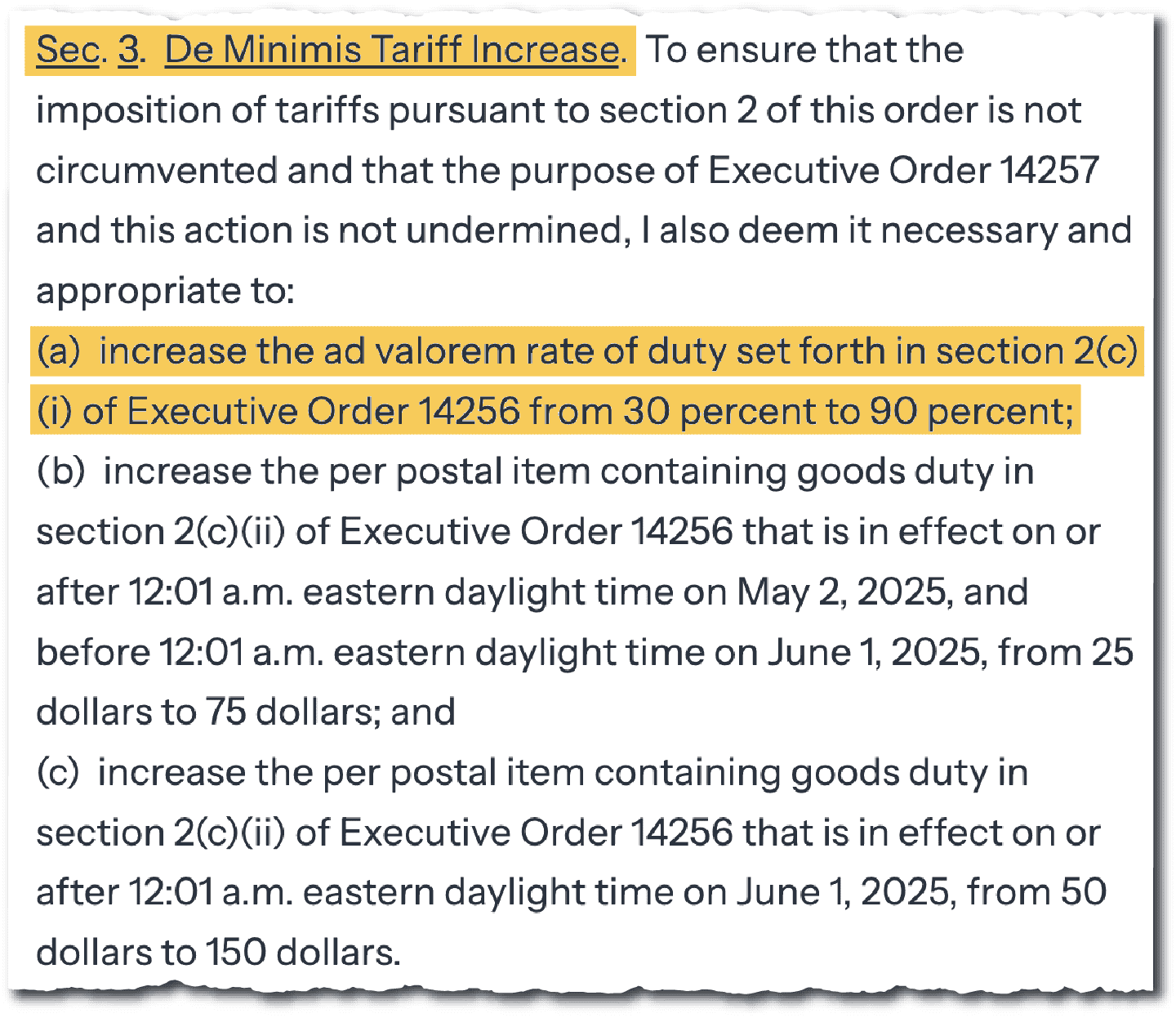

Most large garments importers tend to import large volumes and then break them up into smaller shipments over here [in the U.S.]. What Temu and Shein are doing is that they have vast numbers of small suppliers in China, and those suppliers produce packages already labeled for the UK or the U.S., which are then sent as small packages. And some players who are competing with them, who import large volumes of garments and pay duty on them, have serious complaints, because under the de minimis rule, if a package is worth under $800 in the U.S., it doesn’t get charged duties. And in the UK, the threshold is £135, and in the EU it’s around the same amount. So these packages are coming in without attracting duty.

There will likely be import duty levied on these packages. The question is how do you do it practically? Shein and Temu are already thinking of ways of charging money from their customers and suppliers to cover import duty. All this may undermine their performance to some extent, but there is an expectation that they will continue to deliver very low prices, an attractive product selection, and market appeal. So they’re not out of the game.

What does the ongoing trade war mean for the global logistics network? Some Chinese goods now pass through other countries before they arrive in the U.S. or elsewhere. How will the network change?

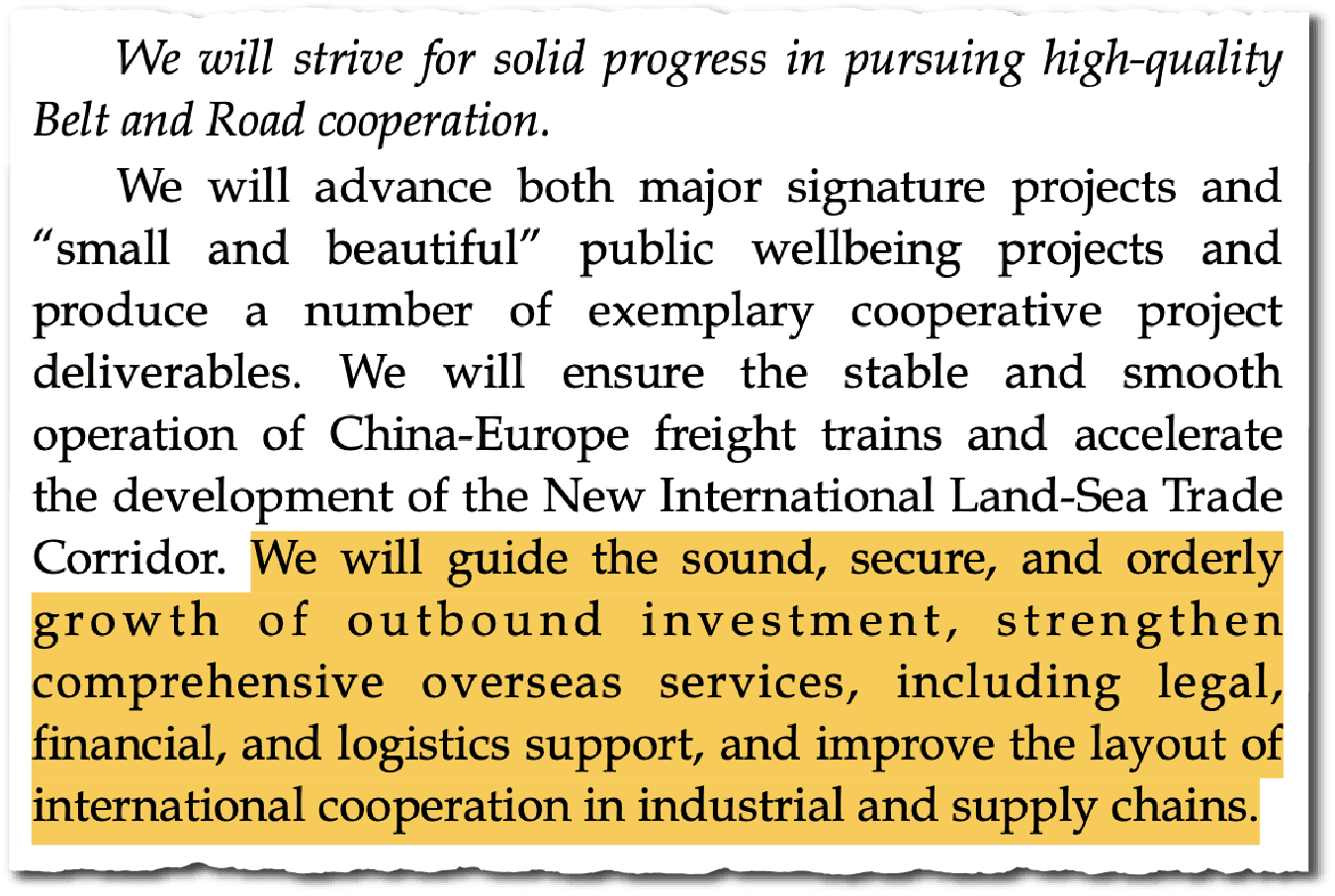

China is hedging its bets by forging new trade relations with the Belt and Road and through numerous free trade agreements. That being said, there’s strong evidence that China has no intention of pulling away from the global economic order. We’re very blunt about the new uncertainties in global trade, and particularly the U.S.-China trade. But the economic world order and supply chains will probably be quite resistant to political pressures. There will inevitably be some decoupling or de-risking. But the interesting thing is that the large multinationals and the logistics firms that work with them have great vested interests in the existing supply chain. There’s a lot of inertia around that supply chain, which they’ve constructed over decades. And while there will be some changes, it will be partial.

A lot of logistics firms are adapting to meet those needs. It reflects a big trend, not so much complete decoupling, but more regional approaches. The idea of everything being integrated across the whole world is seen as quite risky. For instance, a car manufacturer may now be thinking of integrating its components supply chain only within Asia.

As you pointed out in the book, China’s logistics network first emerged under central planning in the ’80s. What way has that legacy affected its development or held it back?

When I first started working in China, for decades it was really difficult. It was hard for foreign companies to get their components in and their products out. Just in a practical sense, the foreign firm had to position somebody at the local rail bureau to pay bribes to get products onto the railway. Trucks were underpowered, with a tarpaulin pulled over to shield the goods from the elements. When they passed into a new province, they often had to pay illegal tolls. Local firms hadn’t grasped the principles of modern logistics, and were incapable of delivering an integrated service across the nation. 20 years later, it was still bad. We did a survey of China’s logistics in 2000 and we interviewed many shippers, foreign and Chinese, and found that there were a lot of unmet needs.

That has to do with the legacy of central planning, where logistics were not thought through in a very creative way and it certainly wasn’t integrated across China. There was no national logistics you could count on, whether it was railway or roads. But there has been incredible progress in the last 40 years.

It took until late 2022 for the Chinese government to issue its first comprehensive five-year national plan on logistics. That plan is a milestone in planning, which is very important because the Chinese government plays a key role in driving China’s logistics upgrade. And the Chinese government admitted that after 40 years of reforms, China’s logistics still lagged the rest of the world massively. They stated that China’s logistics are “large, but not strong.” That was pretty honest. When you admit a problem, then it’s easier to fix it.

So what needed fixing?

I can go through a long list. Even today, China’s logistics is fragmented and there was an absence of scale. There are too many small companies, and they can’t meet the needs of the market. The other thing is that as the centrally planned economy melted away in the ’80s and ’90s, Chinese manufacturers couldn’t rely on the logistics that were around, and they chose to create their own inhouse capabilities, such as trucks and warehouses. They were extremely reluctant to outsource to what we call third-party logistics providers (3PLs), so China has been slow to follow the rest of the world in doing that.

Chinese firms feel the need to own assets because customers don’t feel that they have enough control. They want to see some skin in the game. They want to see the [third-party logistics provider] actually owning some of the transportation and warehousing. Otherwise, they don’t have enough confidence to outsource to them.

Because these logistics firms are often quite small, not technically sophisticated, and poorly differentiated, they compete mainly on price. It drives down the price, and as a result, the levels of services are very poor. And without the profits, they can’t invest in transportation and warehousing, and particularly the IT systems needed.

Also, Chinese logistics firms are often forced to invest heavily in the actual transportation and warehousing. This is unlike the rest of the world, where 3PLs are asset-light, which means they can reduce capital expenditure, financing needs and balance sheet pressure, while providing business flexibility. Chinese firms feel the need to own assets because customers don’t feel that they have enough control. They want to see some skin in the game. They want to see the 3PL actually owning some of the transportation and warehousing. Otherwise, they don’t have enough confidence to outsource to them. They want to be sure the goods will arrive at their destination safely and on time, and be tracked during the process.

What are the reforms taking place now and what is the progress so far?

China’s new logistics plan stresses that the market leads, government guides, and that sums up where we are. The Chinese government’s extraordinary high level of support for the development of logistics manifests itself in a number of ways. They have the detailed state plan we’d mentioned. They are guiding the allocation of capital. And it’s not just bank loans, it is also access to equity markets, such as allowing IPOs by Chinese companies. The Chinese government’s intervention goes well beyond just transportation infrastructure. It is investing heavily in logistics parks and zones alongside business. A lot of this is coming from local governments. Usually, cities are competing against each other to attract capital, jobs, revenues, and that’s happening even when cities are burdened by a lot of real estate issues. Despite that, they are still investing in these hubs. And the government’s forcing consolidation across this sector.

You brought up the example of Sinotrans, a state-owned company. How did it transform itself?

I had the pleasure of working with them as a consultant around the turn of the century. It’s a great example of how an old state firm overcame the legacy of central planning and became a world-class logistics firm. They were founded around 1950 under the foreign trade ministry, and for 30 years, they had a complete monopoly on China’s cross border freight forwarding. So when you wanted a product moved across the border, the company would contact Sinotrans and organize it. But in the late 1990s, everything was changing. The domestic monopoly they had was over, and moreover, they were going to face increased competition from foreign firms after WTO accession. Premier Zhu Rongji told firms like Sinotrans bluntly: reform or prepare to fade away.

Today, Sinotrans has annual revenue of $16 billion. It is China’s largest logistics firm. But in 1999, its future looked far from secure. We did a diagnostic of this firm, which showed that several lines of business were in a death spiral. So it had to recapitalize itself through listing on the stock market. That occurred in 2003. But that path to restructuring was painful and complex. They decided that the healthiest parts of the firm would first be listed in a new entity in Hong Kong.

And the Chairman, Luo Kaifu, correctly and courageously said that the new listed entity needed to be attractive to those that might buy the stock. Even though he was a rather traditional communist, he argued the case for a massive reduction in the bloated workforce, and they had to think about the organizational structure. A lot of large state owned companies at the time looked like they had a strong network across the nation, but really it was just a series of autonomous legal entities at a local level. So what they had to do was create a firm that could deliver an integrated service. And the ownership of these companies had to be painstakingly changed to permit centralized control.

Then they had to refocus the business. They had trucking, shipping and warehousing. They were no longer going to be standalone businesses. They were only to be retained and grown to the extent that they supported the core business, which was freight forwarding and modern integrated logistics. And then they started specializing in auto, fast-moving consumer goods, electronics, and they upgraded the workforce, much of which had never gone beyond lower middle school education.

Today, Sinotrans is a transformed company. It’s been consolidated, now part of China Merchants Group. It’s become a national champion. It has its own proprietary IT platform. It’s now specializing in cold-chain. It can meet the needs of foreign multinationals in China. It has a long-standing and highly profitable joint venture with DHL, and it’s been very prominent in developing the containerized rail routes from cities such as Chengdu out into the Belt and Road, and on to Europe, and Southeast Asia.

What I would say is that it hasn’t made its mark in e-commerce. It finds it hard to compete against private firms such as JD Logistics and SF Express. But it does show that state owned companies can be effectively transformed and revitalized, and that they can step up to the plate where needed.

Are there lessons here for other countries?

There are good reasons why it is not feasible for China to export its hybrid economic model to other countries. That being said, in the U.S., Europe and Britain, while governments play a very important role in developing transportation and in some cases, ports and warehouses, they don’t intervene in the way that the Chinese government does. There may be a role for the U.S. and European governments further downstream to help foster change and efficiency in logistics.

When it comes to the adoption of technology and particularly AI in e-commerce, it illustrates the value of being a late arriver, and thus being able to leapfrog some of the established players, like UPS.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.