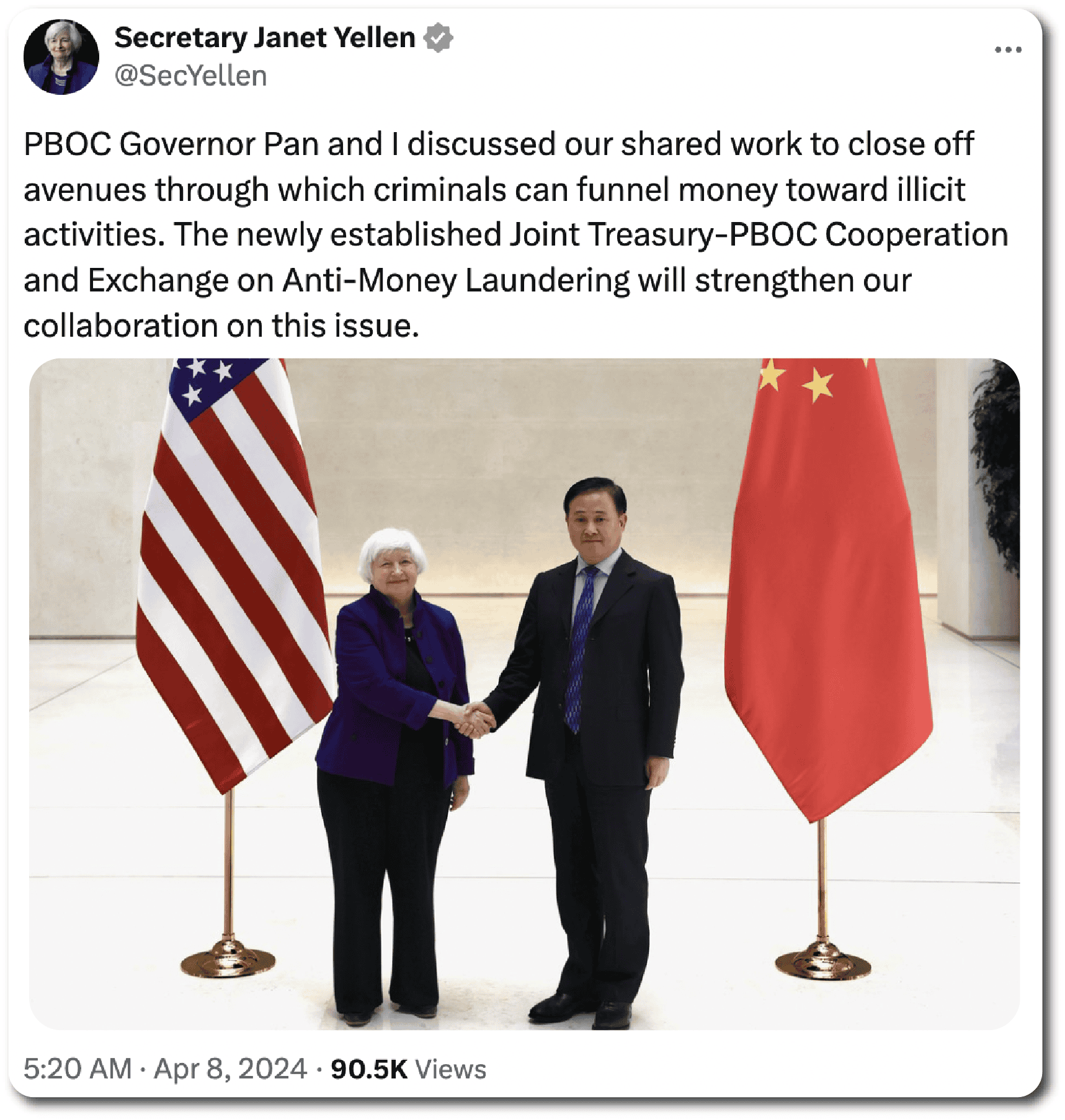

Janet Yellen’s April trip to China was, somehow, even more resounding a success than her first, the previous July, when Chinese netizens marveled at her choice to eat a rare and sometimes-hallucinogenic Yunnanese mushroom. This time around, the Treasury Secretary was praised for her chopstick mastery and modest style, which, observers pointed out, stood in stark contrast to Chinese officials’ flashy suits and entourages of umbrella-wielding apparatchiks.

But Yellen achieved more than just culinary diplomacy in April when she negotiated regular collaboration between the Treasury Department and the People’s Bank of China (PBOC) — an elusive feat for a bilateral relationship that has descended into verbal warfare. Standing in the garden of the U.S. ambassador’s residence, Yellen triumphantly announced a new initiative to fight money laundering and financial crimes. The “Joint Treasury–P.B.O.C. Cooperation and Exchange on Anti-Money Laundering” would establish quarterly meetings, enabling Chinese and American counterparts, Yellen said, “to share best practices and information to clamp down on loopholes in our respective financial systems.”

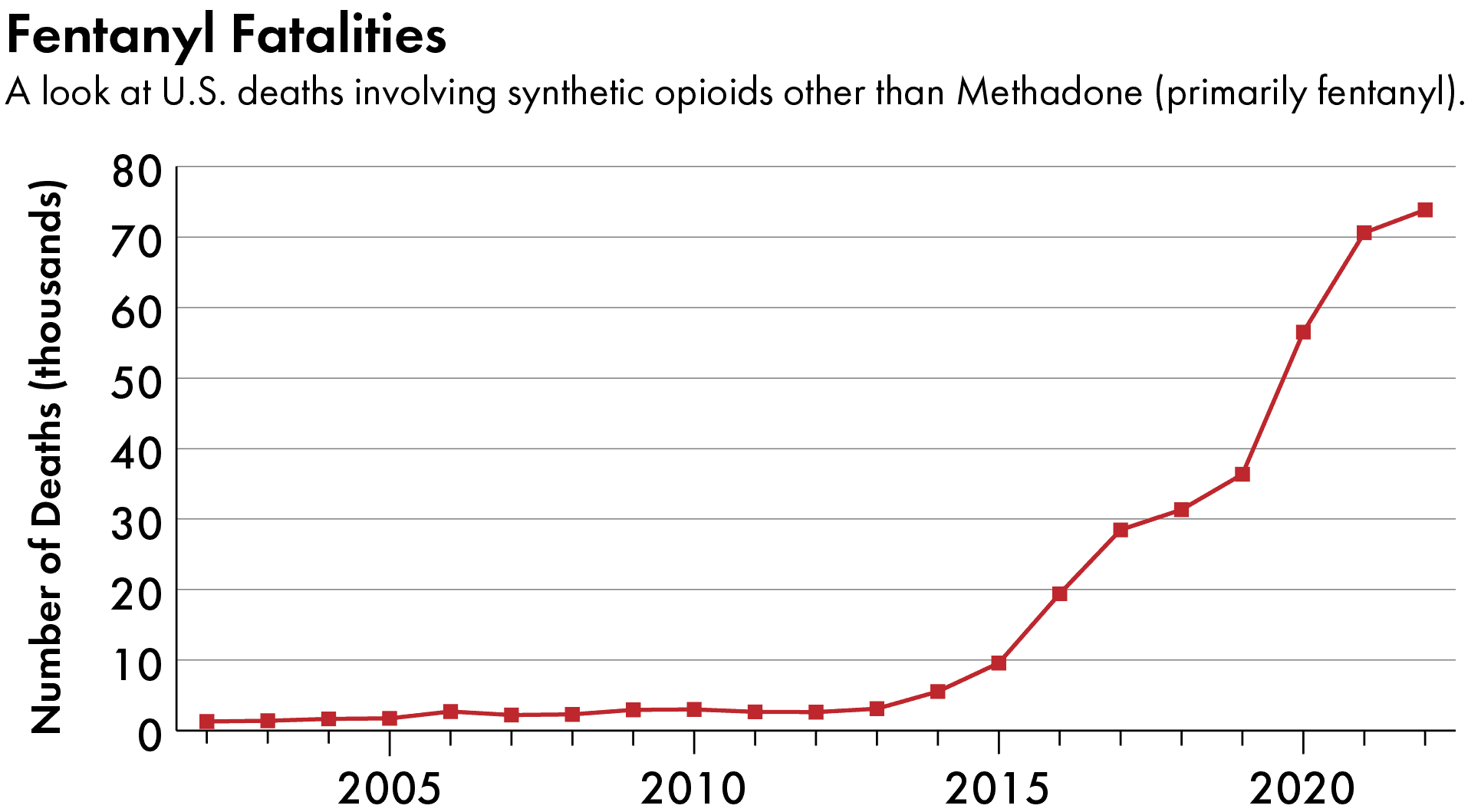

For the U.S., this was a chance to save lives. In recent years, U.S. law enforcement has woken up to the fact that Chinese money laundering syndicates are the partners-of-choice for violent Latin American cartels who flood the country with fentanyl, a synthetic opioid that causes around 80,000 deaths each year in the U.S. — more than firearms and car wrecks combined. The new exchange would, Yellen claimed, “help us disrupt the flow of illicit narcotics, precursor chemicals, and equipment.”

Left: Fentanyl pills seized by CBP at the Port of Mariposa in Arizona, November 6, 2023. Right: Fentanyl seized by CBP at the International Mail Facility in Illinois, November 28, 2017. Credit: CBP via Flickr

Almost all of fentanyl’s precursor drugs originate in China, and just two months after Yellen’s visit, it seemed her Chinese counterparts were taking the opportunity for collaboration seriously. Beijing proscribed 46 psychoactive substances and shuttered over a thousand webstores offering illicit drugs.

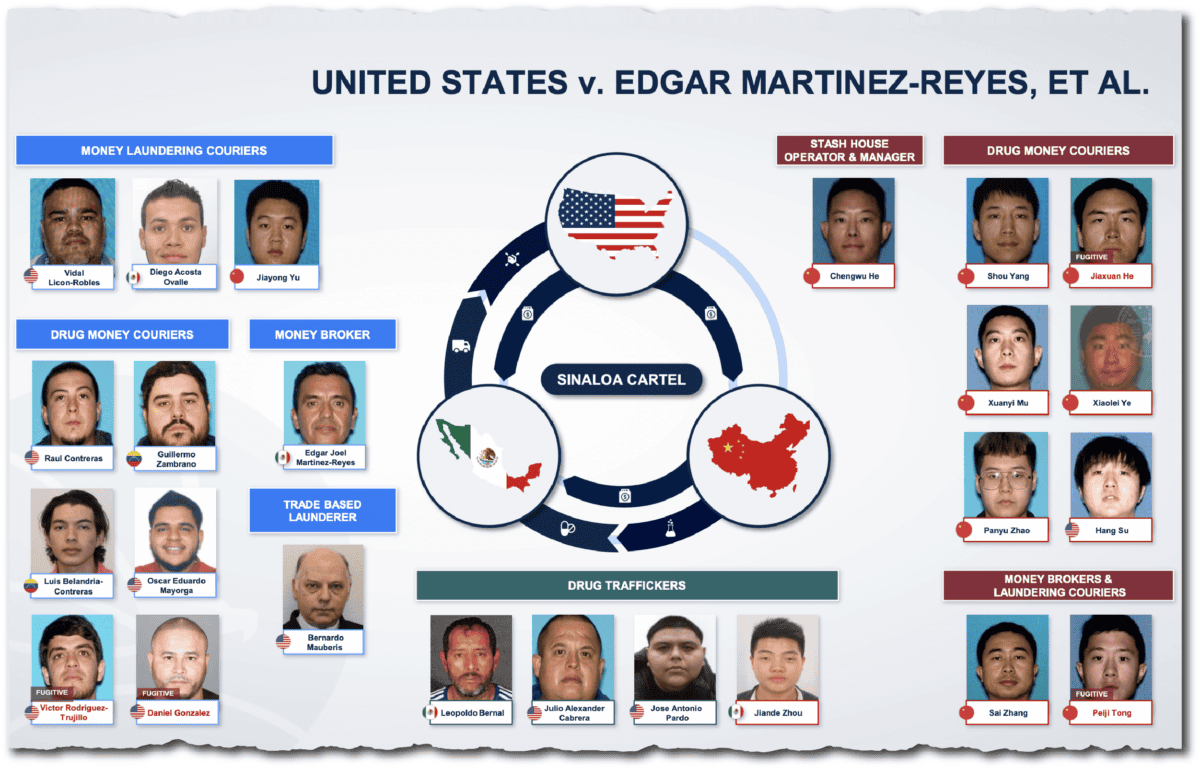

There also seemed to be forward momentum combating money laundering’s role in fentanyl trafficking. That same month, the Department of Justice (DOJ) announced the conclusion of Operation Fortune Runner, a yearslong investigation into a Los Angeles-based money laundering syndicate. Two-dozen defendants, the DOJ claimed, had used “Chinese underground banking” to launder more than $50 million in drug sales for the Sinaloa Cartel, the most powerful organized criminal group in the western hemisphere. “Laundering drug money gives the Sinaloa Cartel the means to produce and import their deadly poison into the United States,” said Drug Enforcement Agency (DEA) administrator Anne Milgram.

On the face of it, these would seem like an extraordinary series of wins. Experts have long singled out money laundering as a rare opportunity for low-stakes cooperation since the incentives seem to align: the U.S. wants fewer drug deaths and weaker cartels; China wants to stem corruption and capital flight that costs its economy hundreds of billions of dollars. Finally, it seemed, progress was being made.

And yet crimes, not least those worth billions of dollars and spread across the entire planet, are so infrequently solved by the simple swish of a diplomatic wand — or, for that matter, a chopstick. The Chinese launderers, says former CIA and Treasury agent John Cassara, “are very fast, very nimble, and they’re not bound by borders or lack of budget. We are always playing catchup. It is very hard — and it’s getting worse.”

Indeed, fentanyl is merely the deadliest chapter in a millennium-old story of informal Chinese networks that have capitalized on their nation’s extensive trade, embedded diasporas, and new technologies to drive a black market that shows no signs of slowing down. An increasingly fragile Chinese economy, deepening trade ties between China and Mexico, and the emergence of a retail craze called daigou have given Chinese money launderers new incentives and outlets.

So consummate has Chinese control of money laundering become that Elaine Dezenski, of the Foundation of Defense for Democracies, believes that many in the U.S. are barely grasping what’s at stake. “This is a money laundering crisis fueling a drug crisis,” she says. “Right now, fentanyl is one iteration of this problem. But next year maybe it’s something else we’re worried about coming in.”

‘FLYING MONEY’

Around 2 a.m. on June 6, 1993, a cargo ship named the Golden Venture hit a sandbank near New York’s JFK Airport. Most of its 268 passengers — undocumented migrants from China’s Fujian province — survived, but ten did not, drowning in their attempts to flee the stranded vessel.

The tragedy would precipitate the downfall of Cheng Chui “Sister” Ping, a Fujianese woman who, since the early 1980s, had smuggled over 3,000 Chinese into the United States. Ping made up to $40,000 per migrant, committing most to indentured servitude under threats of violence from an ethnic-Chinese Manhattan gang.

Amid the fallout of the Golden Venture’s sinking, investigators discovered that Ping operated not only a so-called “snakehead” smuggling network worth around $40 million, but also an “underground bank” that remitted cash to China for a commission that undercut the Bank of China’s local branch. At her Chinatown variety store, a worker would exchange his or her weekly cash earnings with Ping in return for a code number, which the worker would then relay to a relative in China. Ping would call or fax her contact in China, and within a day a bike courier would arrive at the door of the relative who, if they relayed the code, would receive their money in U.S. dollars.

The Chinese are constantly balancing the need to enforce the law with the need to ensure that the economy keeps growing.

Laurence Howland, who was Britain’s fiscal crime liaison in Beijing between 2010 and 2014

Two ‘mirror transactions’ had been made, but the money itself did not move — much less cross an international border. So popular was Ping’s underground bank that the Bank of China placed ads in Chinatown newspapers reminding residents that it was illegal. “There were always people there sending money,” one migrant told the reporter Patrick Radden Keefe, in his book The Snakehead.

Authorities arrested Ping in Hong Kong in 2000 and sentenced her to 35 years in prison. For years, she was the highest-profile example of a criminal using a method called fei ch’ien, or “flying money.” Other cultures knew it as hundi or, in the Arab world, hawala. But the practice began during China’s Tang Dynasty (618-907 AD). Merchants purchased a state certificate that, when presented at any provincial treasury, allowed them to withdraw the equivalent sum in cash. Both the state and merchants could therefore avoid carrying copper coins on long and dangerous journeys. These certificates are widely considered to be the world’s first paper money.

As Chinese traders ventured out across the world, brokers emerged to settle debts and remit cash back to the homeland. Many operated in Chinatowns in major cities worldwide via guanxi, an honor system that thrived in diaspora communities that were often insular and tight-knit. From the 16th to 19th centuries, Chinese underground finance split into two lanes: Piaohao, or “draft banks,” which facilitated international trade, and Chien chuang, or “money shops,” which were smaller and more local. Both functioned with full recognition of the Chinese government.

At the beginning of the 20th century, as foreign banks entered China, draft banks began to decline. Money shops endured until Chairman Mao’s nationalization of China’s banking industry snuffed out the private finance sector. But they both reemerged soon after to serve a newly mobile generation of Chinese expatriates, whom Deng Xiaoping’s 1978 economic reforms had freed to trade with all corners of the planet.

The U.S. Drug Enforcement Administration first connected Chinese underground bankers to drugs five years later, as cartels in Southeast Asia’s Golden Triangle dominated the global heroin trade. Chinese-run casinos in Thailand, Laos and Myanmar emerged as key facilitators of the industry. Chinese launderers also washed small amounts of the profits reaped by cocaine traffickers in Colombia, including Pablo Escobar. They kept almost no records, according to a 1990 Justice Department cable, and used coded messages, telephone calls and “chits” (small notes) to transfer money across international borders.

Yet by most accounts, Chinese shadow banks played a peripheral role for western-hemisphere narco traffickers. Asian gangs may have worked hand-in-glove with Hong Kong Triads and groups on the Chinese mainland, but Latin American narcos, whose chief powerbase had shifted by the late 1990s to Mexico, preferred to clean their money in-house, paying commissions up to 18 percent in the process.

That all changed in 2007, when China’s State Administration of Foreign Exchange (SAFE) began more strictly enforcing a rule that prevented citizens from exchanging more than $50,000 in foreign currency per person a year. For Beijing, the idea was to stem “capital flight,” the rapid exodus of large sums of money from China’s economy.

But for underground bankers, the decision had the effect of a key sliding into a lock.

Whether wittingly or not, the Chinese Communist Party (CCP) aligned a series of interests that would hand Chinese underground bankers a vital edge over their competition — one that Mexico’s most feared criminals could not ignore. Almost overnight, the Chinese had a “captive demand” of millions of compatriots looking to circumvent the controls, says Vanda Felbab-Brown, an expert of international crime at the Brookings Institution.

Chinese underground banks, she says, could “impose most of the fees on Chinese customers, while charging much less to their criminal clients.”

That March, Mexico City police discovered a two-ton mountain of cash totaling $207 million at the pink-walled mansion of Chinese-Mexican businessman Zhenli Ye Gon. Four months later, DEA agents arrested Ye Gon in Las Vegas on drugs and money laundering charges. Since then, claims the Washington, D.C.-based NGO Global Financial Integrity, “China’s shadow banking system has mushroomed into a $10 trillion obscure financial system.”

The use of underground banks accelerated even more with Xi Jinping’s ascension in 2012 and his pledge to purge the party of graft. As corrupt officials and elites scrambled to park their wealth outside China, the Chinese Central Bank estimated that around 18,000 officials left the country in 2011, taking almost $7 million each. Many used offshore bank accounts and investments in real estate or collectibles, but experts note that underground banks have a large role to play as well.

“The capital flight issue is front and center,” says Dezenski. “People wouldn’t have a need to buy dollars on the blackmarket [if it weren’t for Beijing’s capital controls].”

Are we going to see the dismantling of networks? Indictments of individuals laundering money, as part of that U.S.-China cooperation? Or in China itself? This is where the rubber will meet the road.

Vanda Felbab-Brown, an expert of international crime at the Brookings Institution

China’s zeal to prosecute financial criminals, however, has largely been confined to politically-driven cases. Bo Xilai, for instance, the commerce minister and Xi political rival, was arrested for bribery, embezzlement and abuse of power. China only has one unit dedicated to investigating financial crimes (the PBOC’s Anti-Money Laundering Monitoring and Analysis Center), and judges have historically avoided levying money laundering charges in favor of less politically sensitive offenses, such as illicit trading and illegally running a business. Those who are charged with money laundering are far likelier to face a fine than prison — diluting even further the operational risk for underground bankers.

Laurence Howland, who was Britain’s fiscal crime liaison in Beijing between 2010 and 2014, notes that authorities have little reason to prosecute these cases since China’s economic miracle very much depends on them.

“The Chinese are constantly balancing the need to enforce the law with the need to ensure that the economy keeps growing,” Howland, who is now director of risk and compliance at Buckles Solicitors, says. Black markets like counterfeit goods, illicit finance and fentanyl precursors can keep “whole communities afloat in areas [of China] that are still very third-world.”

Before fintech took China by storm with AliPay and WeChat Pay, China’s legal banking system was also so onerous and bureaucratic that an underground banker often meant the difference between sending money in moments and waiting in line at a bank for half a day or longer. As the fintech platforms streamlined legitimate finance, they handed underground bankers faster and easier ways to make money fly.

China’s stock market crash in 2015, for instance, precipitated a fresh wave of capital flight. No longer did citizens require coded messages or “chits” — they needed only to type “flying money” or “money shop” into WeChat to engage hundreds of underground bankers. Some used a method called “smurfing,” which recruited Chinese who hadn’t maxed out their $50,000 quota. Others used the accounts of foreign-based students. Because WeChat and Alipay are closely surveilled by the Chinese state, U.S. officials have accused Beijing of at best negligence and at worst complicity in these schemes.

The following year, in 2016, the number of fentanyl overdose deaths in the U.S. overtook heroin for the first time. New York regulators acknowledged the role of Chinese illicit finance in the crisis by fining the Agricultural Bank of China $215 million. The state-owned bank was accused of “alarming transaction patterns,” including clearing dollars for an Afghan Bank client who was known in the drug trade.

But the extent of cartels’ involvement with Chinese money launderers was most spectacularly exposed that same year, some 2,000 miles south of New York, when gunmen ambushed a Chinese-American gangster named Xizhi Li near his Guatemala City casino, peppering his armored Range Rover with over 20 rounds.

Li escaped unhurt. But, just as the Golden Venture had sparked Sister Ping’s downfall, the attack presaged a DEA sting against Li’s money laundering enterprise, whose casinos and tech-led transactions straddled the old and new worlds of Chinese money laundering. In late 2019 agents captured Li in Merida, Mexico, and in 2021 he was sentenced to 15 years imprisonment for laundering $30 million for the same groups that were now responsible for almost 74,000 fentanyl overdose deaths per year. Li used accounts “including but not limited to the Agricultural Bank of China and the Commercial Bank of China,” according to his indictment.

The case would help “to weaken the complex system the cartels rely on to continue their depraved business,” said DEA special agent Wendy Woolcock.

But only insofar as plucking a grain of sand makes a beach lighter.

Where Rubber Meets Road

Cooperating on fentanyl has become a way for Beijing to curry favor with U.S. counterparts — and forestall trade sanctions that would further damage China’s faltering economy. A 2022 campaign that is set to run until next year, for instance, has charged more than 2,300 people with operating fei ch’ien schemes worth several billion dollars. It seems as if Beijing is now “more willing, at least on the process part, to be more forthcoming than ever before,” says Felbab-Brown.

Yet getting from process to meaningful action, she says, requires a lot more. “Are we going to see important seizures of drug money,” Felbab-Brown asks. “Are we going to see the dismantling of networks? Indictments of individuals laundering money, as part of that U.S.-China cooperation? Or in China itself? This is where the rubber will meet the road.”

Indeed, while Beijing’s recent overtures will make “some difference,” says Neil Thomas, a Chinese-politics fellow at the Asia Society, “there’s not much in the way of a buddy-cop film to be made about U.S.-China cooperation on anti-money laundering.”

The next big hurdle, he predicts, will be when the U.S. finds more evidence that implicates politically-sensitive actors, like Chinese state-owned banks. “China won’t want to admit that these core institutions are closely involved, either wittingly or unwittingly, in these criminal networks,” he says. “The people who run these banks are often part of the Central Committee and fairly high-ranking officials.”

In the 2016 indictment against the Agricultural Bank of China, New York’s regulators accused it of obscuring the beneficiaries of transactions by sending codes via SWIFT, the global banking sector’s messaging network. The bank also violated sanctions regarding Russia, Iran and Yemen, and it had pressured its compliance chief into resignation. Regulators have also warned the China Construction Bank, another state-owned bank, to tighten its anti-money laundering compliance.

The involvement of state-owned banks makes it tricky for the U.S. to take decisive action. Both the Agricultural Bank of China and the China Construction Bank have more assets than JP Morgan Chase, America’s largest bank. They are two of China’s “big four” state-owned banks that are also the four biggest on earth, with assets totaling $21.9 trillion — over two-thirds of the entire U.S. economy. Penalizing them more seriously may kneecap the money launderers, but it could also have unintended ripple effects throughout the global economy.

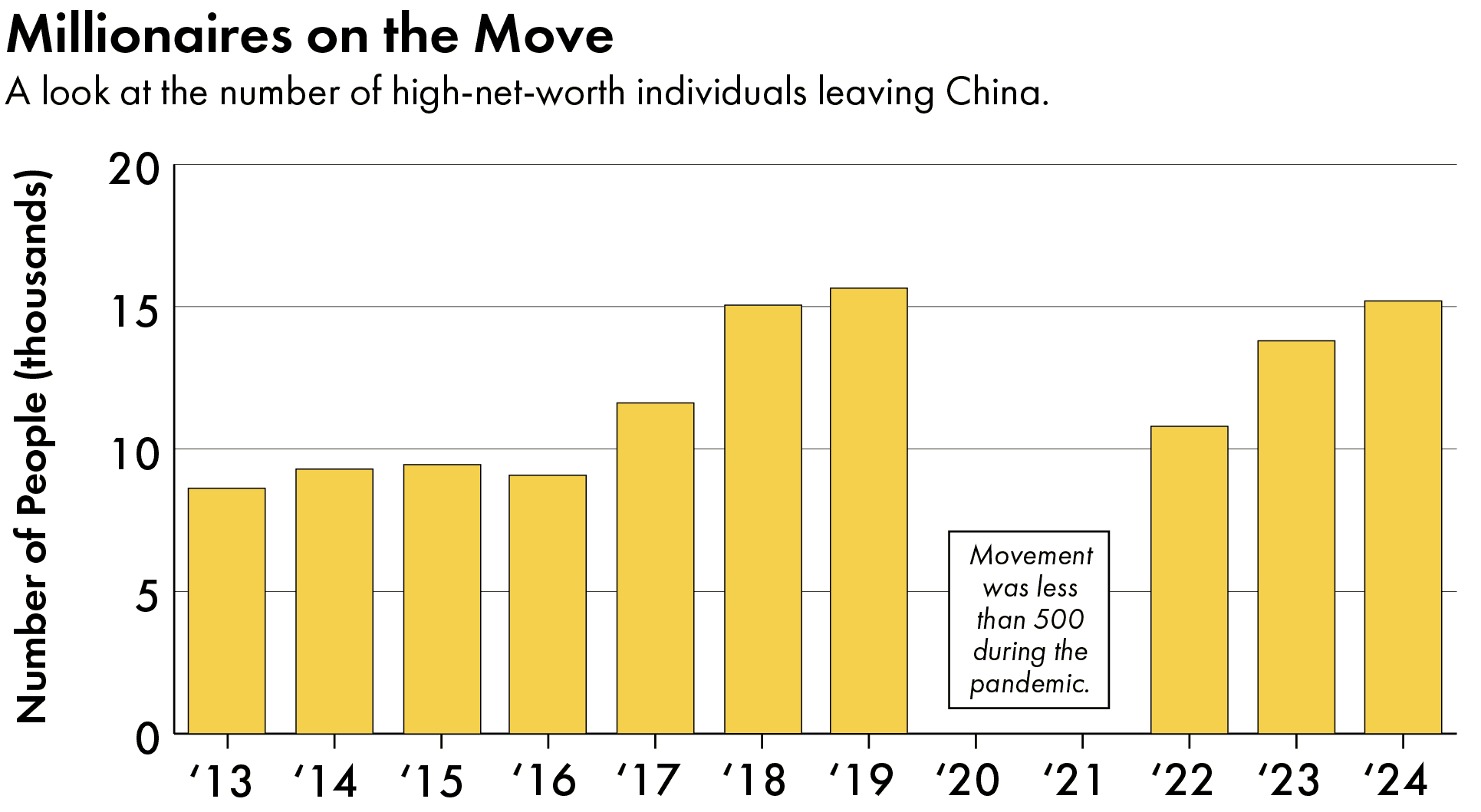

Some experts speculate that China and the U.S. don’t have enough motivation to solve the root problems of money laundering. From Beijing’s perspective, fentanyl addiction, however tragic, drains U.S. budgets, hobbles law enforcement and weakens social cohesion — outcomes no Chinese trade or intelligence operation could hope to achieve. Likewise, the U.S. has its reasons to encourage more capital flight from China. With Chinese indices and property prices down and growth slowing, real estate consultant Juwai IQI expects more than 700,000 Chinese will leave the country in the next two years. The accompanying capital flight could cost China’s economy hundreds of billions of dollars.

China’s money launderers, meanwhile, are devising new ways to stay ahead of the demand. Increasingly, for instance, they are piggybacking off of legitimate trade. After the Trump administration began its trade war with China, Chinese exports to Mexico surged 107 percent and reached an all-time-high of $114 billion. “Trade-based” money launderers might use legitimate transactions as criminal Trojan Horses by, for example, over-invoicing for goods, falsely describing goods and services, or by introducing unknown third parties to deals. In 2020, Mexico’s second largest cartel laundered drug proceeds by bulk-buying Chinese shoes.

The idea that we’re going to interdict the problem is totally wrong. We really have to just cut the ties that connect these players.

Elaine Dezenski, of the Foundation of Defense for Democracies

Trade-based transactions, notes Brookings’s Felbab-Brown, avoid international wires and money transfers across banking systems, thus evading most of the anti-money laundering systems that have been built. “The Chinese can offer enormously advantageous prices and avoid law enforcement attention,” she says, “because they can change money through trade with just about any place in the world.”

Money launderers have discovered another goldmine in daigou — roughly, “buying on behalf of” — a system whereby Chinese individuals buy products abroad then resell them domestically, often without paying customs tariffs. The system is particularly popular among those seeking high-end European brands; approximately 15 percent of luxury goods arrive in China via daigou. Narco money launderers can hijack the phenomenon just as they do legitimate trading.

Daigou has grown by 40 percent since 2019, according to reporting by Reuters, and is now worth an estimated $81 billion. For underground bankers, daigou is “an easy way of moving money,” says Howland. “It’s not intrinsically lawful, and it’s not intrinsically criminal.”

To close loopholes, increase transparency and tighten financial laws worldwide, the Financial Action Task Force, a global money laundering watchdog, recommends a raft of actions including national cooperation, the prioritization of asset recovery, company ownership transparency and tougher supervision of banks.

These recommendations — 40 in total — are “the golden standard,” says Julia Yansura, Program Director for Environmental Crime and Illicit Finance at the FACT Coalition. But while it doesn’t seem like rocket science, she says countries are not particularly good at implementing these reforms. It took U.S. lawmakers 15 years, for example, to mandate the disclosure of companies’ beneficial owners, a loophole that allowed money laundering via anonymous shell firms.

“These are things we know we’re supposed to do,” Yansura says. “But it’s hard, it takes time, and it might be politically difficult.”

It may also be the only option. In 2022 the ‘Chapitos’, an arm of Mexico’s vast Sinaloa Cartel, claimed to be reaping a profit margin on fentanyl “approximately 200 to 800 times” the cost of the drug’s precursors. One, $800 kilo of chemicals from China could be pressed into 415,000 fentanyl pills destined for U.S. streets, each one costing around $3. Cartels are said to be able to lose nine of ten shipments and still reap a tidy profit.

This reality, says Dezenski, means that no number of ‘drug busts’ will ever stem the tide of fentanyl on America’s streets. The only way to win the war on synthetic drugs, she adds, is to disrupt traffickers’ access to the commodity they crave the most: cash. Right now, that means stopping the Chinese money launderers.

“The idea that we’re going to interdict the problem is totally wrong,” she says. “We really have to just cut the ties that connect these players.”

Sean Williams is a British reporter and photographer based in New Zealand. His work has been published by The New Yorker, Harper’s Magazine, GQ, The Daily Beast, The New Republic, Wired, The Economist and more. @swilliamsjourno