After years of state-backed plenty, China’s semiconductor industry is undergoing a reckoning.

Take Beijing Zuojiang Technology which, since going public in 2019, has touted its chips as a domestic alternative to U.S. giant Nvidia’s data processing units. Riding the AI boom, the company’s market cap reached a peak of $300 billion yuan ($41.5 billion) last July.

But that bubble burst when it emerged earlier this year that Zuojiang Technology has never found a buyer for the chips it claimed to have sold. China’s securities regulator announced in January that it was investigating the company for financial fraud and the company delisted from the Shenzhen stock exchange last month.

Zuojiang Technology’s debacle is not an isolated case. In June, the Chinese authorities barred Shanghai-based chipmaker S2C from listing within the next five years, after it found that the company had inflated its profits in 2020 by more than double. The same month, a Shanghai court ordered Shanghai Wusheng Semiconductor Group to liquidate; the startup, which built power semiconductors, owed suppliers and employees hundreds of thousands yuan and has since gone bankrupt.

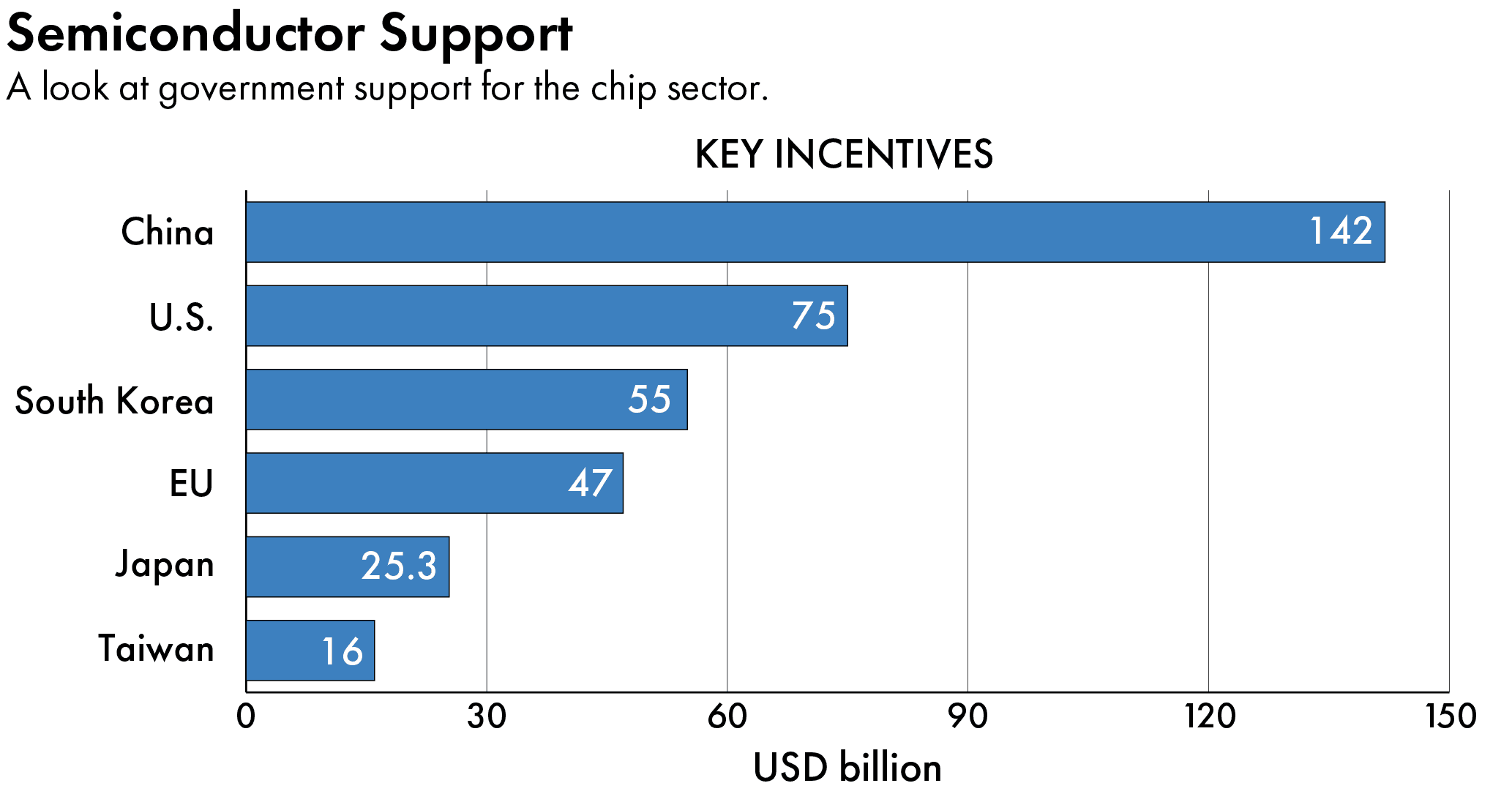

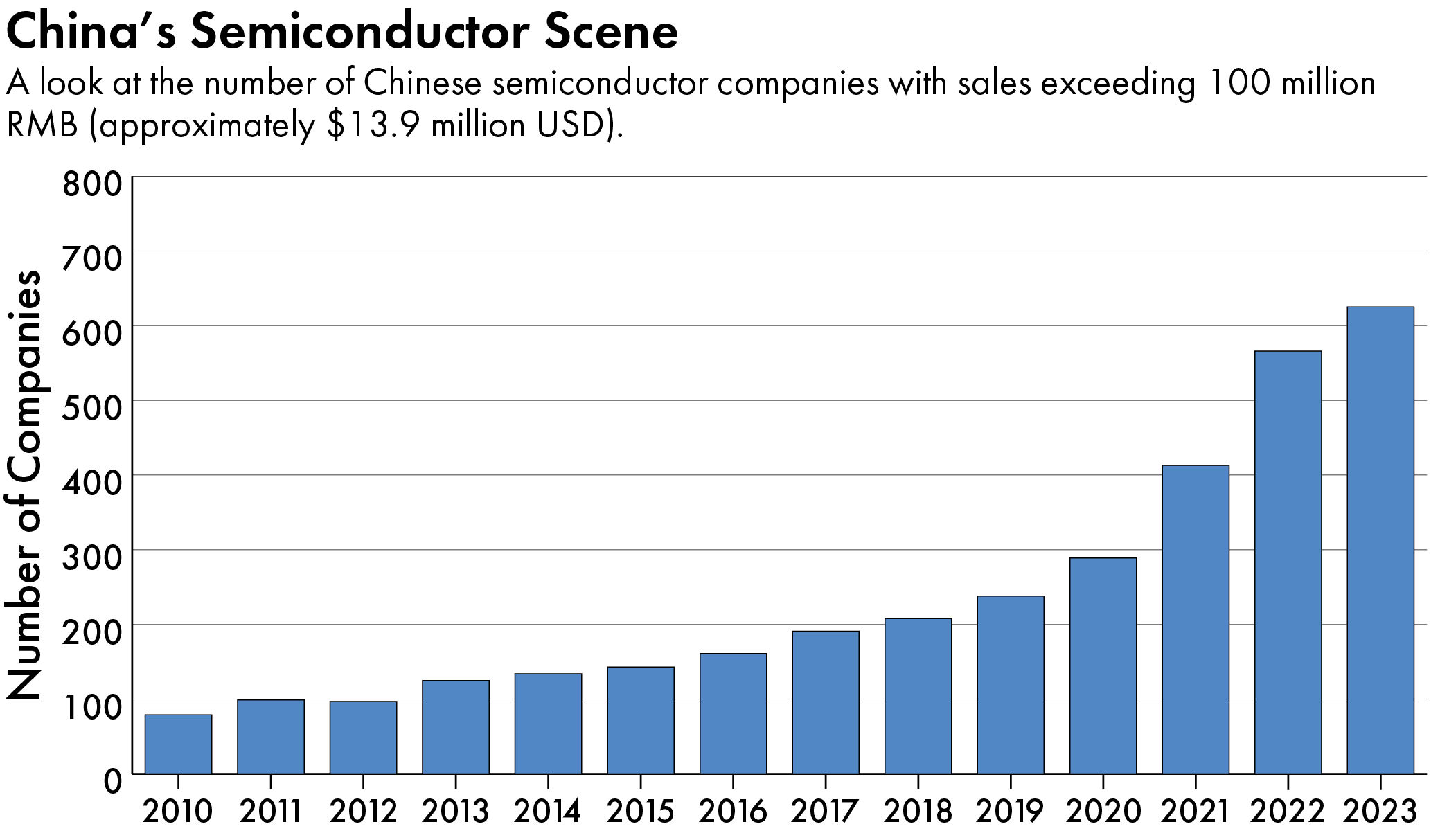

These companies’ downfall is part of a larger shakeup. To achieve its goal of self-sufficiency, Beijing has pumped $142 billion into grooming homegrown chip companies since 2014, according to an estimate from the Semiconductor Industry Association (SIA), a Washington-based lobbying group. Hundreds of companies jumped on the bandwagon backed by robust state support.

Now, though, the Chinese government is weeding out bad actors, all while becoming more selective about how it allocates its resources.

“There has been ongoing consolidation in the semiconductor industry, as industrial planners in Beijing have sought to ensure that semiconductor companies have real business models and are not just taking advantage of subsidies for a sector Beijing deems critical for future economic growth,” says Paul Triolo, technology policy lead at the Albright Stonebridge Group, an advisory firm.

The course correction stems in part from corruption scandals that have plagued the industry and high profile project failures, such as that at Wuhan Hongxin Semiconductor Manufacturing Co, which received millions of dollars worth of support from local government in Wuhan before going belly up in 2021.

“China is keen to let underperformers die outright or merge,” says Woz Ahmed, a former semiconductor executive and managing director of the consultancy Chilli Ventures. “Some were shells created to get local government funds. Others were more legitimate, doing research and development, but didn’t sell a single thing and were simply kept alive by government grants.”

A record 10,900 semiconductor-related companies in China were terminated last year, a 90 percent increase compared to the year before, Chinese media outlet TMTPost reported, citing information from the Chinese business database Qichacha. Meanwhile, 36 Chinese semiconductor companies withdrew their initial public offering applications in the first half of the year, mainly due to higher government scrutiny and disappointing financial results, according to JW Insights, a Chinese consultancy.

The setbacks in China are part of a larger downturn that dealt a blow to global semiconductor sales last year. And while China’s domestic supply of chips has surged in recent years, demand for end products such as consumer electronics and electric vehicles remains weak amid the country’s economic slowdown. Semiconductor sales in China fell by 14 percent last year, the steepest drop among all major markets, according to SIA.

The Chinese ecosystem excels at creating a lot of startups in a very short time, but at some point, it’s simply not sustainable… [Consolidation] is a necessary step to achieve economies of scale and to be more cost effective.

Jan-Peter Kleinhans, head of global chip dynamics at the European think tank Interface

The gloom has extended into the first half of this year and impacted established players as well, though analysts say there is cautious hope for a gradual recovery this year.

Shanghai-based foundry Hua Hong Semiconductor saw a 79 percent drop in its profit in the first quarter, compared to the same period last year, although its revenue increased by 1 percent compared to the quarter before. Similarly, state-owned Semiconductor Manufacturing International Corporation (SMIC), the Chinese industry leader, saw its revenue grow by a fifth in the first quarter, although its gross profit plunged by 69 percent.

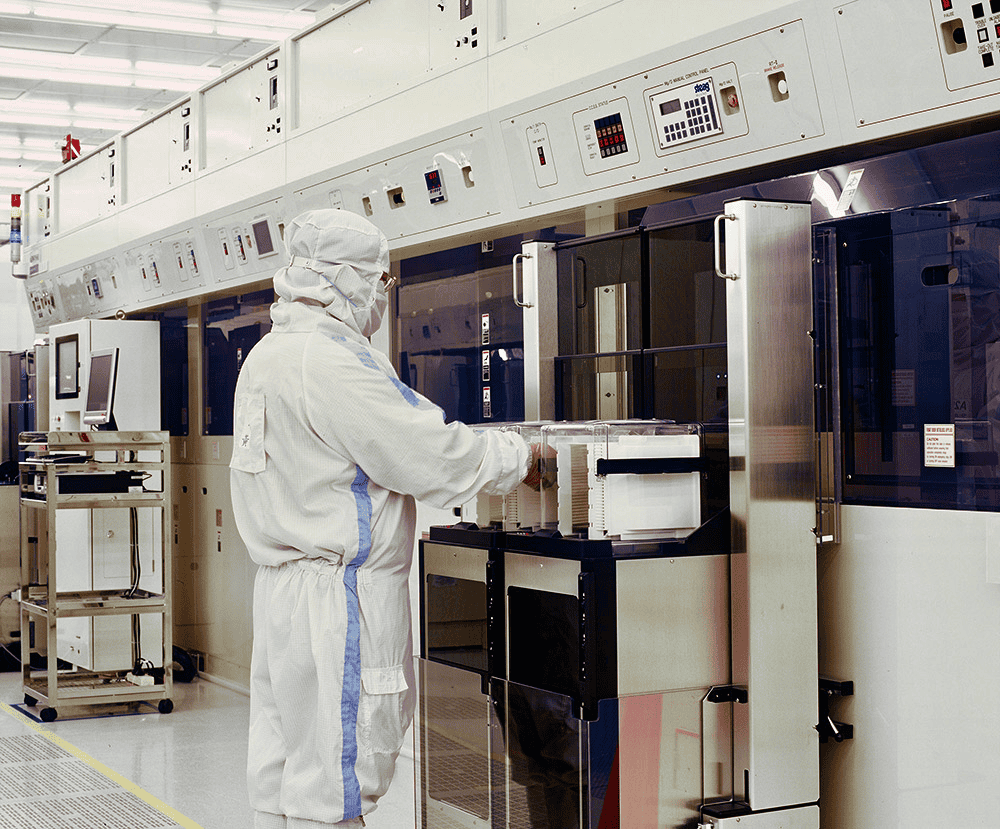

A worker in a Hua Hong cleanroom (left) and an SMIC cleanroom (right). Credit: Hua Hong, SMIC

“As China’s local new capacity continues to come online, competition in the industry has been increasingly fierce,” said Haijun Zhao, a co-chief executive officer, during an earnings call in May.

The strategy of Chinese foundries like SMIC is to prioritize utilization rates over earnings, says Adam Chang, an analyst at Counterpoint Research. “They do very aggressive price cuts to try to gain share from Taiwanese foundry players such as UMC or TSMC, and they are also benefiting from China’s semiconductor localization policy.”

Experts say eliminating poor performers is healthy for the sector in the long run.

“The Chinese ecosystem excels at creating a lot of startups in a very short time, but at some point, it’s simply not sustainable” says Jan-Peter Kleinhans, head of global chip dynamics at the European think tank Interface. “If you look at what happened to the semiconductor industry globally, in any sector that is maturing, you see consolidation. This is a necessary step to achieve economies of scale and to be more cost effective.”

In other markets, for instance, each area of the semiconductor supply chain tends to be dominated only by a handful of players. China, however, is still far from that situation.

“The number of Chinese semiconductor companies is still growing. The size of many companies is still growing. We’re still in the boom period,” says Dylan Patel, chief analyst at the consulting firm SemiAnalysis, who expects a bigger wave of consolidation only when Beijing fully turns off the tap.

A still more urgent question for China is how it can break the U.S.’s stranglehold and produce more sophisticated semiconductors on its own. The Biden administration, which has limited exports of advanced chips and chip-making tools to China, is mulling further restrictions on China’s access to AI memory chips, according to Bloomberg. It is also planning a new rule to prevent some Chinese fabs from sourcing equipment from countries such as Malaysia and Singapore, Reuters reported last month.

To that end, China has taken a more cautious approach with the third phase of its Big Fund, which it rolled out in May, directing the $47.5 billion it raised towards critical bottlenecks and more promising ventures.

“Beijing is putting most of its effort behind companies like Huawei and SMIC with proven track records, large numbers of qualified personnel, and clear business models, rather than subsidizing a larger number of smaller firms with little chance to make breakthroughs in key technology bottlenecks,” Triolo says.

As part of new measures unveiled in June to promote innovation, Chinese regulators are also encouraging mergers and acquisition in the tech sector, which analysts say will accelerate integration in the semiconductor industry and hopefully pool resources in more capable hands.

How well this new formula will work remains to be seen. “There is a certain risk that China gets stuck in mediocracy,” says Kleinhans, of Interface. And if it fails to close the gap, “the pain of the Chinese industry will be felt more acutely with every single year that passes.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.