Novo Nordisk is feeling good about China. In March, the pharmaceutical company behind the blockbuster diabetes-turned-weight loss drug Ozempic held its “Capital Markets Day” presentations and held a breakout session devoted to its strong showing and trajectory in China. As Maziar Mike Doustdar, head of international operations, put it “all of our competitors combined are not able to cover what we do.”

He had good reason to be cocky: Novo Nordisk’s sales of Ozempic in China doubled last year, propelling it to claim 77 percent of the market share, and in June, Chinese authorities cleared Wegovy, Novo Nordisk’s higher dose version of Ozempic, which will undoubtedly further boost revenues.

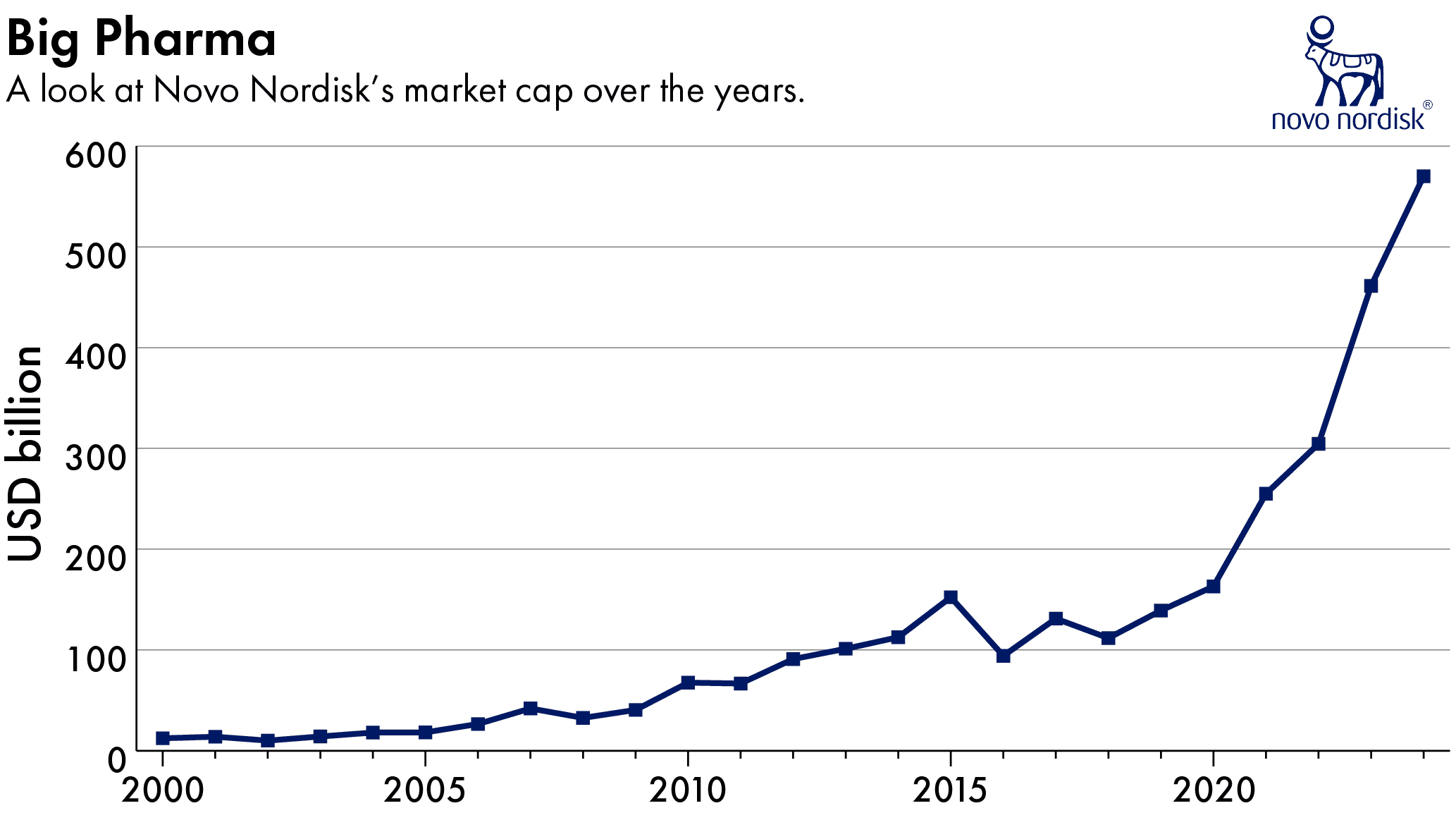

China is not unique, of course; Ozempic has made Novo Nordisk a global sensation. The Danish company is now worth more than the entire Danish economy, and it dethroned the French luxury group LVMH as Europe’s most valuable company late last year. In February, its market capitalization reached half a trillion dollars, making it only the second European company in history to achieve the feat.

But breaking into the China market as authoritatively as Novo Nordisk has done is not an easy feat. Doustdar himself noted that many observers have found it baffling that the relatively small company could have such an unusually large share of the Chinese market. Novo Nordisk, he added, has accomplished what giants like Apple, Google and Amazon have failed to do in their own sectors, and he attributed Novo Nordisk’s competitive edge to its long-standing presence in the country.

Indeed, Novo Nordisk first entered China in 1994, just as demand for its insulin drugs was booming, and it has maintained a laser focus on China’s insulin and diabetes market ever since. Today, there are around 140 million diabetic patients in China, about 10 percent of the population and a quarter of the global sum, according to The International Diabetes Federation. China is also home to the world’s largest population of obese people.

But despite Doustdar’s confidence and the clear need for drugs like Ozempic in China, Novo Nordisk faces an uncertain future in the Middle Kingdom.

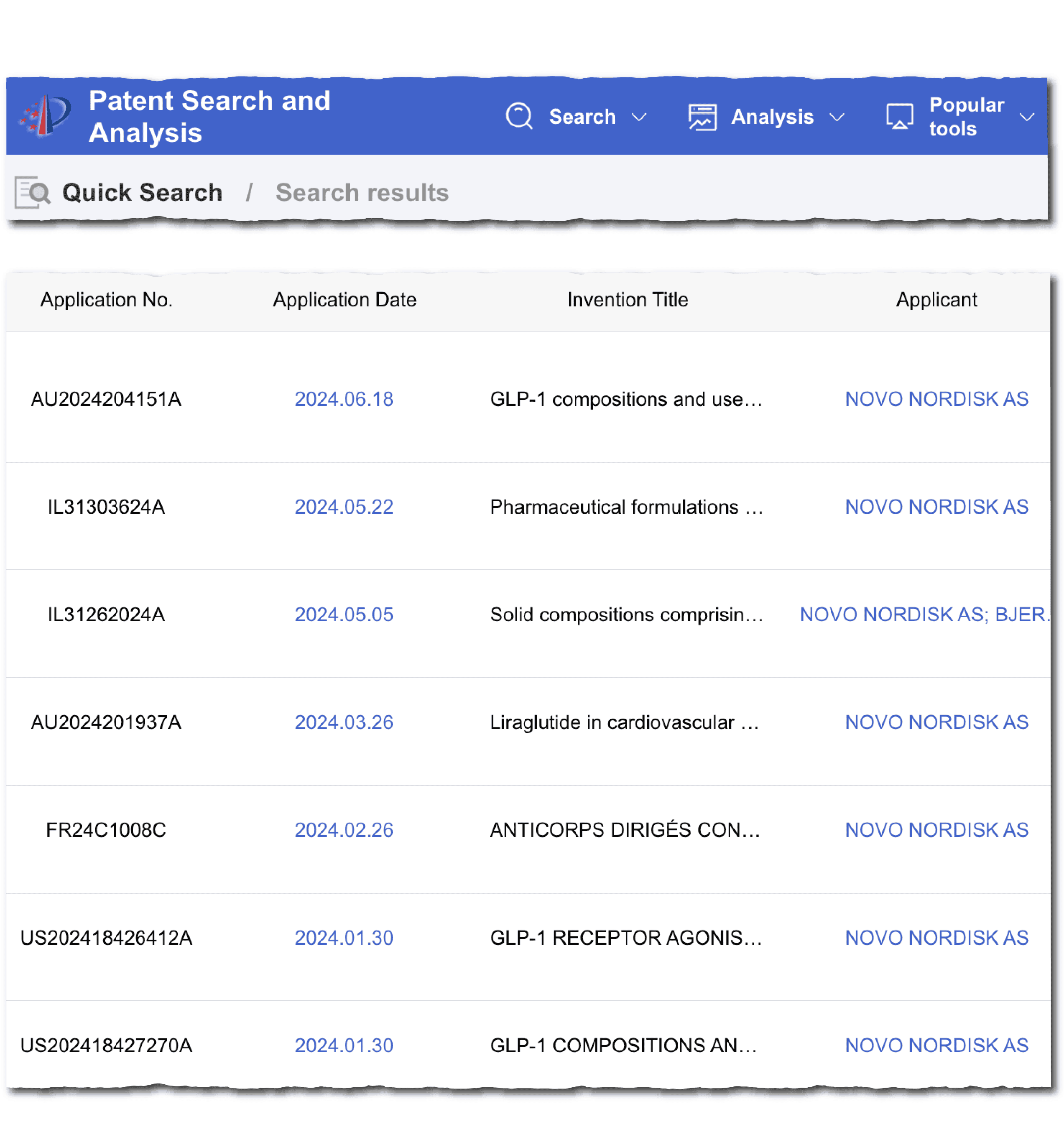

In July 2022, Chinese drugmaker Huadong Medicine successfully challenged Novo Nordisk’s patent, arguing that it lacked novelty. According to James Hou, founder of the Nanjing-based consultancy China Intellectual Property Consulting and Information, Novo Nordisk’s patent is rock solid: “It’s genuinely a remarkable technical achievement,” he says. But Huadong Medicine has a biosimilar, Jiyoutai, that it wants to enter the market, and Hou says the patent office’s decision was an example of the government favoring domestic generic drug makers.1Jiyoutai is developed by Jiuyuan Gene. Huadong Medicine is the largest shareholder of Jiuyuan Gene.

This is not a new trend: A study by scholars at Tongji University in Shanghai found that the success rate of invalidating drug patents in China between 2005 and 2022 was as high as 73.7 percent, while the rate in the U.S. was around 23 percent in 2018.

Still, Novo Nordisk appealed the patent office’s decision, submitting post-filing data to prove its case, and the Beijing Intellectual Property Court listened, overturning the patent office’s ruling last year. A final decision about Novo Nordisk’s patent is now in the hands of the country’s top court, and industry experts say the ruling will serve as an important test case for Beijing.

“The ruling will be a signal of how the system balances the interests of innovative biopharmaceutical companies with those of generic drug manufacturers, at a time when the Chinese government is focused on supporting the innovativeness of its domestic industry,” says Sandra Barbosu, a senior policy manager at the Washington-based think tank Information Technology and Innovation Foundation.

Every single multinational finds China hard. You may have three competitors in the U.S., but you may have triple that in China. It’s just a fact of the market here.

Helen Chen, head of the China life sciences and healthcare practice at L.E.K. Consulting

Novo Nordisk says it does “not comment on the expected timeline for court cases,” and declined to comment on its broader China strategy beyond saying the company has “a long-term commitment to China.”

Protecting patents is seen as key for fostering innovation, and a ruling in favor of Novo Nordisk could be seen as a ruling in favor of the many Chinese companies racing to develop the next generation Ozempic. China’s market for GLP-1 drugs (the type of diabetes and obesity medication that Ozempic falls under) is expected to grow faster than the global annual rate of 21 percent and reach $11.4 billion in 2033, according to Nomura, and Chinese companies could take up 20 percent of the pie in dollar terms. According to the consultancy Bain & Co, there are 99 Chinese GLP-1 drugs already in the pipeline, with 18 in late-stage trials last year.

“Every single multinational finds China hard,” says Helen Chen, head of the China life sciences and healthcare practice at L.E.K. Consulting, a global strategy advisor. “You may have three competitors in the U.S., but you may have triple that in China. It’s just a fact of the market here.”

What happens to Novo Nordisk in the country, then, is not just a test for Novo Nordisk but one for China’s larger pharmaceutical industry.

SUGAR HIGH

Only 1 percent of China’s population had diabetes in the 1980s, but the prevalence of the chronic, metabolic disease rose along with the country’s economy as people’s diet and lifestyle shifted. By 2014, the number grew to 10 percent, and patients were overwhelming clinics. It was such a pressing public health crisis that a leading scholar warned at the time the country was on track to become “the kingdom of dialysis.”

“The wealth that we’ve accumulated over the past 30 years will be wasted in the drains of our dialysis machines,” Linong Ji, director of the Peking University Diabetes Center, said at the time.

Indeed, a study by Chinese scholars put the economic burden of diabetes — including the health expenditure and the indirect costs of lost productivity — at $250.2 billion in 2020, accounting for 1.58 percent of the country’s GDP. The sum is estimated to nearly double in the next decade, growing at a faster rate than the GDP.

Concerned by these trends, China initiated a healthcare reform in 2015 and unveiled the Healthy China 2030 blueprint the next year. Central to the plan is encouraging innovation and scientific development, and experts say it was a pivotal moment for the industry.

“Before that, China was really aiming to restrict [multinational companies] as much as possible and keep more control over its domestic market,” says Jeroen Groenewegen-Lau, head of the Science, Technology and Innovation program at Berlin’s Mercator Institute for China Studies. In contrast, “we are now in a period where China wants its populations to have access to the best treatments on the planet, so there’s more incentive to allow foreign treatments to be sold on the Chinese market.”

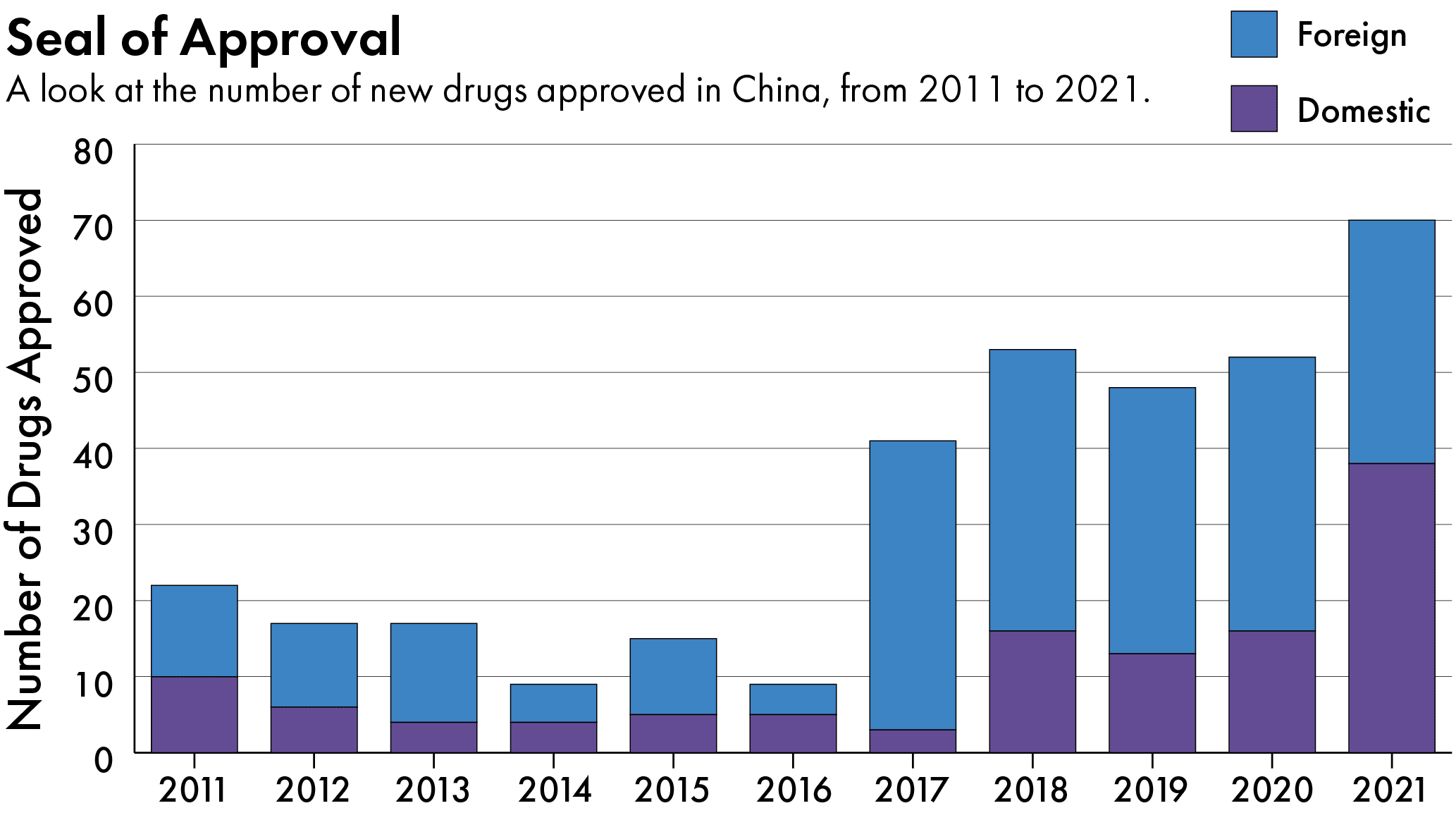

As part of the reform, China streamlined approval of drugs, giving priority to innovative medications. The median review times for new drugs fell from nearly 2.5 years in 2014–2016 to 13.7 months in 2021. To close the access gap with developed countries, China also welcomed more overseas clinical data and began allowing foreign companies to conduct local trials, opening its door to a flurry of foreign medications.

Global drugmakers took notice. China went from an afterthought to a “CEO-level priority.” Every drug that went into late-stage testing must have a China plan, an executive at AstraZeneca told The Wall Street Journal in 2018.

Novo Nordisk’s plan was to localize. The Danish drugmaker was already the first international pharmaceutical company to set up research and development as well as modern insulin manufacturing in China in the 1990s. In 2015, it doubled down by expanding domestic production and salesforce. “We hope to be seen over time as a Chinese company so that we can partake in the development of diabetes care in China,” Lars Rebien Sorensen, then chief executive, said at the time.

In recent years, China has also stepped up its IP protection, bringing its system more in line with the rest of the world. As part of the China-U.S. Economic and Trade Agreement in 2020, for instance, Beijing started allowing patent term extension and introduced a patent linkage system to help resolve potential patent infringements.

Taken together, the reforms didn’t just change the calculations for multinational corporations (MNCs); they also made it easier for domestic companies to take their products overseas, especially the U.S., where they could fetch premium prices and higher profit margins.

“It was the catalyst to China’s growth in biopharmaceuticals, partially because having to harmonize approval regulations with the rest of the world changed the incentive structure,” says Abigail Coplin, an assistant professor at Vassar College, who has studied development in China’s biotech industry.

Chinese biopharmaceutical companies moved from licensing rights to foreign drugs and developing biosimilars to debuting first-in-class therapies. In its annual report in 2020, Huadong Medicine, the Hangzhou-based company that challenged Novo Nordisk’s patent, declared that “the era of high gross profit of generic drugs has come to an end,” and noted the company needed to shift towards innovative drugs, which are more profitable.

This period also gave birth to companies like BeiGene, which, despite originating in China, considers itself a global company. For a brief moment, it felt as if China’s domestic pharmaceutical companies were on the cusp of challenging established MNCs outside of China.

If you go overseas, the key questions are: Can you run clinical trials in this market? And how much can you invest in the commercial capability. I don’t think [Chinese pharmaceutical companies] have the money or funding to expand overseas on their own these days.

Jialing Dai, founder of PharmaDJ, an industry intelligence firm

Then, of course, the pandemic and the larger “decoupling” trend between China and the West unfolded. Chinese companies now draw scrutiny on foreign soil, and in recent years, the U.S. has rejected a number of China-developed drugs on the same grounds Beijing once cited, taking issue with clinical trials done only or predominantly in China.

“The U.S. is doing what China did before Healthy China 2030: closing off the market and ironically citing some of the same arguments,” says Groenewegen-Lau.

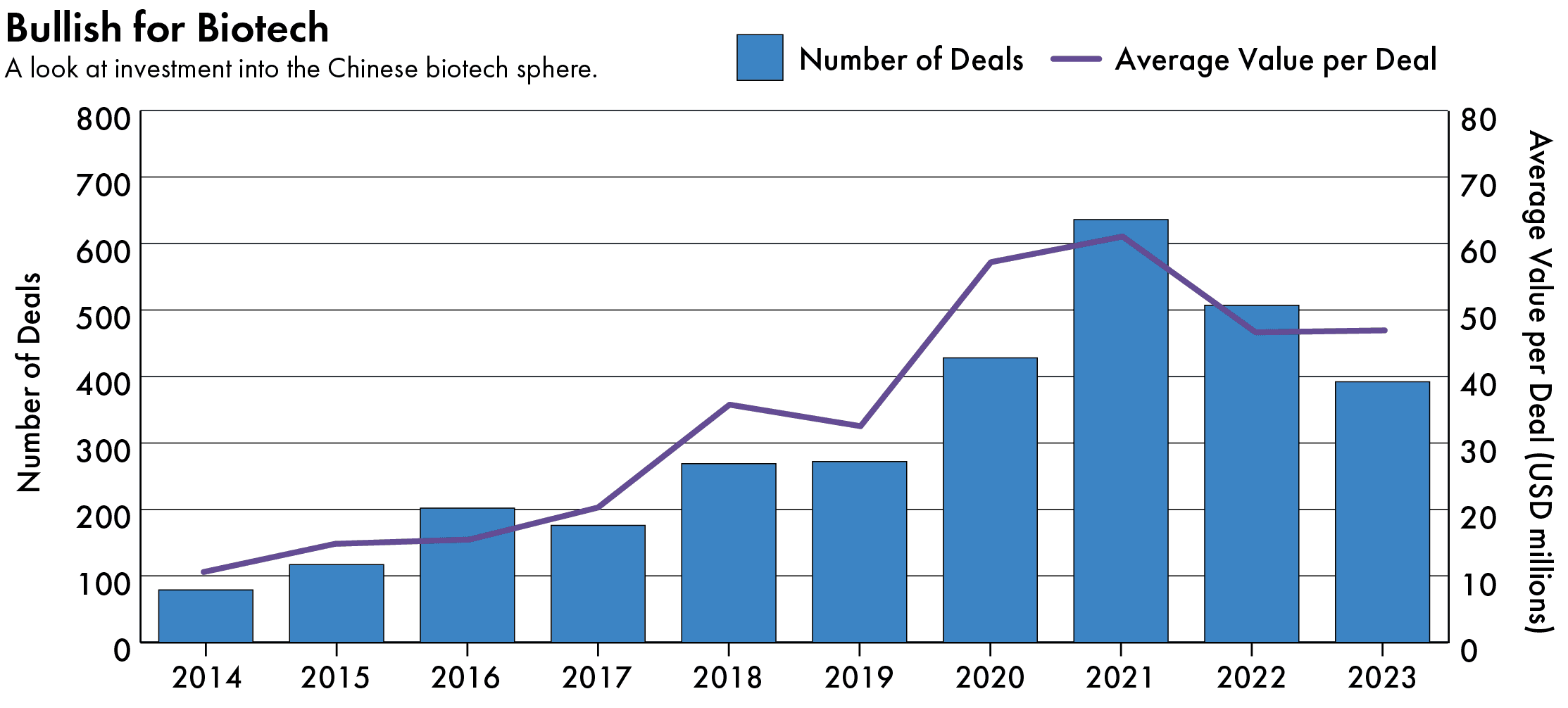

China’s capital market downturn also isn’t helping: Many Chinese pharmaceutical companies have seen their valuations halved since 2021, and investment is drying up. Few Chinese biotech companies have the cash flow to establish a presence in developed markets, such as the U.S. and Europe.

“If you go overseas, the key questions are: Can you run clinical trials in this market? And how much can you invest in the commercial capability,” says Jialing Dai, founder of PharmaDJ, an industry intelligence firm. “I don’t think [Chinese pharmaceutical companies] have the money or funding to expand overseas on their own these days.”

Beijing, of course, doesn’t want to rely on Western countries, especially the U.S., for their medicines, which guarantees a certain level of support and runway for the domestic pharmaceutical companies to develop. But as long as healthcare is a priority, China needs to keep its doors open and play nice with foreign firms.

Chinese vice premier Zhang Guoqing seems to have said as much last August during a one-on-one meeting with Lars Fruergaard Jorgensen, chief executive of Novo Nordisk. According to China Daily, Zhang vowed China’s support, saying it was “resolved to high-level opening-up and will continue to support the development of foreign companies, including Novo Nordisk, in China.”

Thanks to its strong name brand recognition in China and good standing with the Chinese government, Novo Nordisk certainly stands out from other big pharma companies in China. Plus, as a Danish company, it is less exposed to the turbulence between the U.S. and China.

But the company has pursued a unique strategy by building its operations in China from scratch rather than through acquisitions and partnerships with domestic firms. Given the evolving landscape, it’s not clear how long such a strategy can bear fruit.

“No one’s quite sure what’s going to pan out in terms of being the best strategy right now,” says Coplin. “But the Chinese government would prefer to see a domestic actor involved.”

TWO WAY STREET

This is the tack Eli Lilly is taking in China. The U.S. pharmaceutical company has chosen to pursue more strategic collaboration with domestic companies, including outsourcing the manufacturing of its active pharmaceutical ingredients to Chinese manufacturers and collaborating with a Chinese partner to develop multiple therapies, including a next-generation GLP-1 drug. Although the former has resulted in some controversy — WuXi AppTec, one of Eli Lilly’s manufacturers, was caught in the geopolitical crossfire between the U.S. and China — the latter could pay off in a big way.

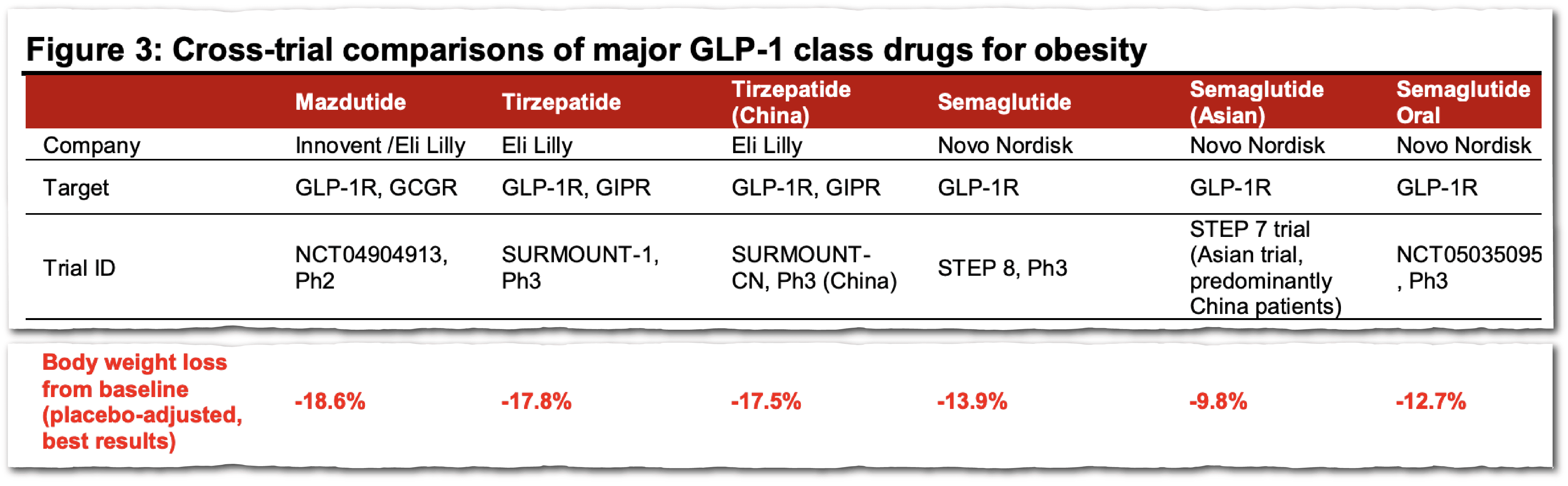

Since 2015, Eli Lilly has maintained a close relationship with Innovent Biologics, a biopharmaceutical company from Suzhou. Eli Lilly has its own blockbuster diabetes drug, Mounjaro, but in 2019, the U.S. company licensed a diabetes compound in mid-stage clinical development to Innovent, which in turn developed it into the drug Mazdutide. In clinical trials, Mazdutide had a better safety profile and yielded more substantial weight loss than Mounjaro and Ozempic.

By cultivating a Chinese partner, Eli Lilly not only secured a strong contender in the pipeline; it will also get an advantage navigating China’s huge and fragmented market when Mazdutide launches, which could be as early as mid next year.

“That’s where Innovent comes in handy,” says Brian Yang, an analyst with the industry intelligence provider Citeline. “Because it has its own local foot soldiers who can promote the products efficiently and reach the lower-tier markets, which a lot of MNCs have difficulties penetrating.”

Eli Lilly is also developing Mazdutide in parallel outside of China and is currently in phase 2 clinical trials. In an email to The Wire China, the company said it is “premature to comment on the commercial strategy.” But according to the estimates of GlobalData’s Pharma Intelligence Center, Eli Lilly stands to make $75 million from Mazdutide’s global sales outside of China by 2030.

Given that both Novo Nordisk and Eli Lilly are struggling to meet the skyrocketing demand in North America for their weight loss drugs, it can also make sense to partner with domestic companies that have strong supply chains. Some Chinese companies even see the bottleneck as their way in: “That gives us a big opportunity because we have no issue with supply,” says Xu Wenjie, chief commercial officer at Innogen, a Shanghai-based biopharma whose novel GLP-1 drug is one of the domestic frontrunners waiting to capitalize on the segment. Now under regulatory review, it is expected to be launched later this year under the brand name Diabegone.

There’s a belief on both sides that you protect your competitiveness by walling off your domestic sector, and that’s just not true. Biotech runs more on kind of a basic science model where you stay competitive by staying engaged.

Abigail Coplin, an assistant professor at Vassar College

Partnering up with MNCs is also considered a win for domestic companies like Innovent. Out of the dozens of innovative GLP-1 candidates currently under trial in China, few companies have the resources, funding and capability to even reach the finish line, says a Chinese biotech executive who requested anonymity as they were not authorized to speak to the media. And even if the domestic contenders do successfully launch their products, they will need to obtain enough market share to achieve economies of scale and turn a profit.

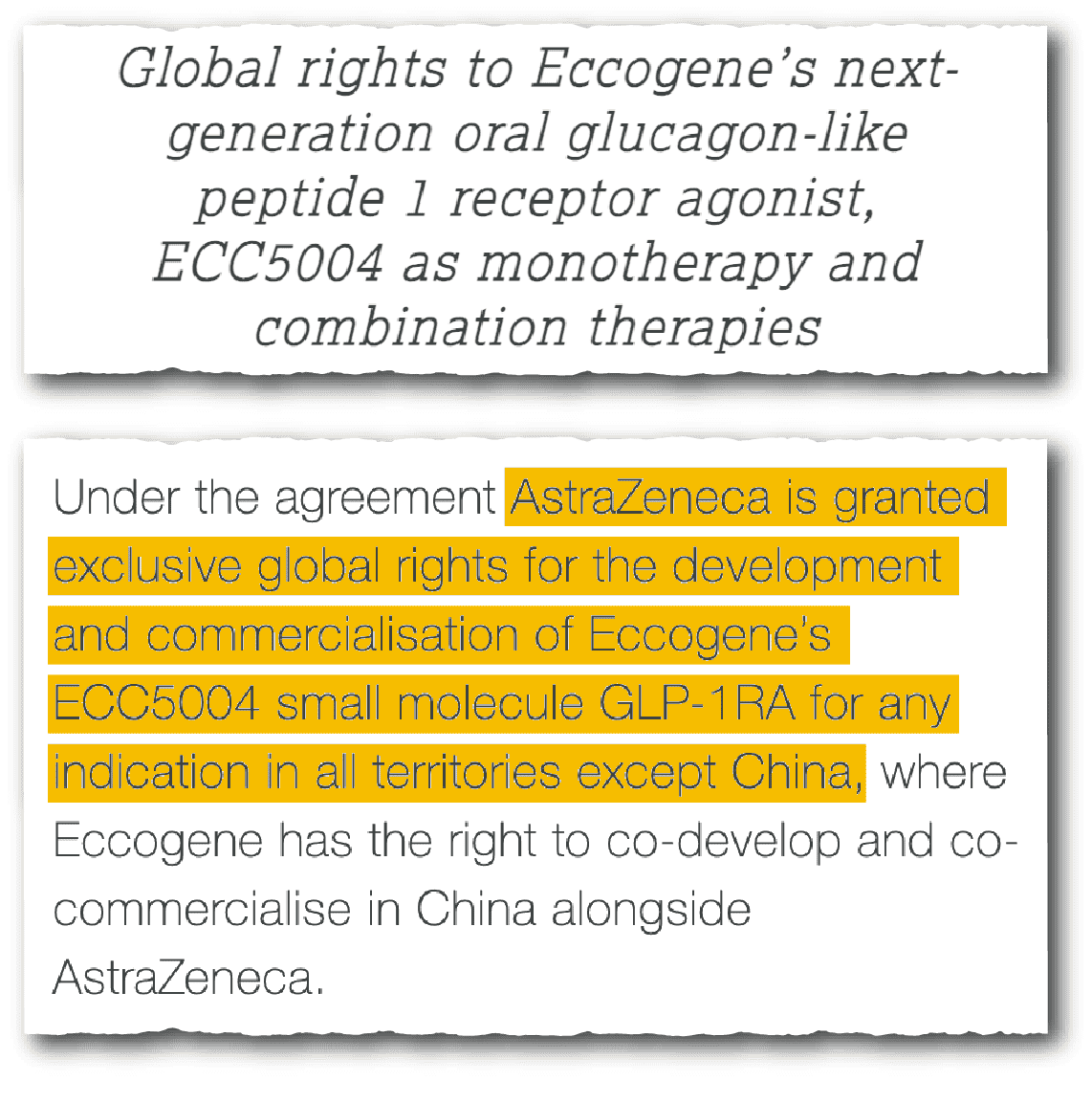

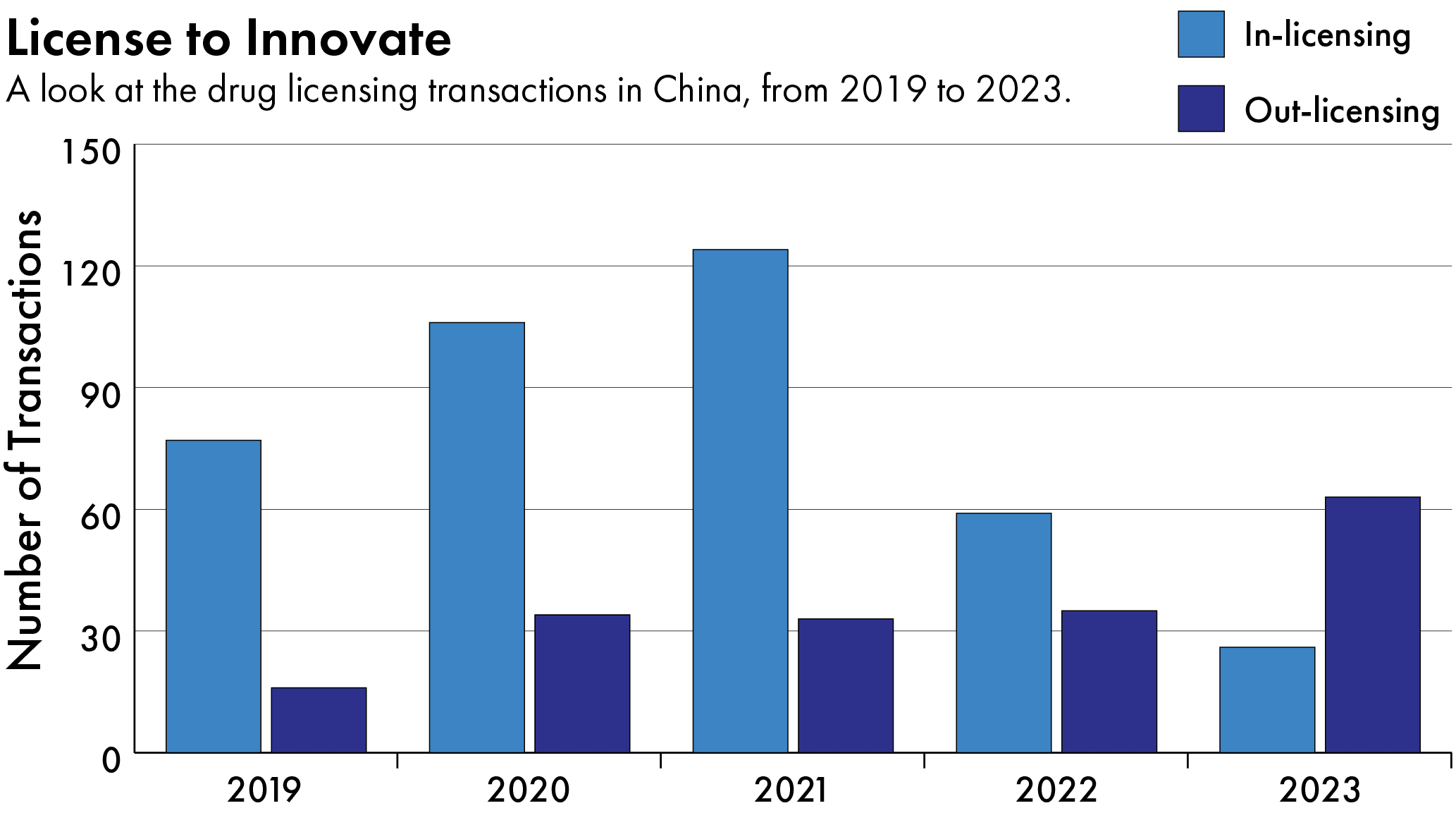

Chinese biopharmas are also eyeing opportunities to go global with MNCs. Instead of going it alone as BeiGene once did, many have opted to out-license their assets, selling the rights to commercialize their drugs outside of China in return for funds to continue their research. The Shanghai-based biopharmaceutical Eccogene, for instance, out-licensed its oral GLP-1 drug to AstraZeneca in November, leveraging the MNC’s resources to take its product overseas. It pocketed $185 million in upfront investment and stands to receive up to $1.8 billion in royalties on sales. Jiangsu Hengrui Pharmaceuticals, a leading pharmaceutical in China, also sold the global rights of its innovative GLP-1 portfolio to a financial consortium in May, giving itself a new injection of capital.

For Western pharmaceutical companies, this represents an opportunity to snap up promising assets at bargain prices and expand their portfolios. Such deals hit a record $44.1 billion last year, despite the geopolitical storm.

It is a bit of an irony, then, that despite the great “decoupling,” Western pharmaceutical companies and Chinese ones need each other like never before. Chinese companies especially, says Leon Tang, founder of the biotech consultancy, ISWT-BioAdvisory, have learned that to compete, you must first collaborate.

“That’s the biggest lesson for Chinese biopharmas in the past decade,” he says. “If you want to keep everything to yourself, no one will help you.”

“There’s a belief on both sides that you protect your competitiveness by walling off your domestic sector, and that’s just not true,” Coplin adds. “Biotech runs more on kind of a basic science model where you stay competitive by staying engaged.”

Some analysts even suggest that if Novo Nordisk wants to stay on top, it may have to up its game in China and look for domestic partners. Even if the top court upholds Novo Nordisk’s patent, it is still set to expire in 2026, at which point an avalanche of Chinese generics like Jiyoutai will be ready to compete at lower prices.

“In the next five to seven years, for sure, [Novo Nordisk] will face some difficulties in retaining its market share,” says Karan Verma, a healthcare research analyst at information services provider Clarivate. “That’s purely because once biosimilars start entering the market, in a country like China, it’s very easy for a domestic company to gain a foothold with its own supply chain and distribution networks.”

Another shift may come when there are sufficient generics in the market and China’s centralized procurement system finally kicks in. Under the program, drugmakers have to take steep price cuts in order to win contracts to supply the country’s hospitals, essentially trading price for volume. Most of the bids in the past have gone to Chinese companies, which can afford to offer lower prices, while MNCs may choose to stay with a smaller audience that pays out of pocket.

“In the future, you would probably have two markets in China: People who are cost sensitive and covered by insurance using a Chinese version, and wealthy consumers sticking with Novo Nordisk [and other foreign drugs],” says Tang.

In other words, while the pie is growing in China, the share for companies like Novo Nordisk may be shrinking.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.