For private equity in China, it’s a case of paradise well and truly lost.

That much was clear from the mood at a major industry gathering held in Hong Kong this week. Nearly every talk at the annual China Private Equity Summit began with an admission that the outlook is grim.

Fund managers used to placing one-way bets on a rising Chinese economy and Beijing’s support grumbled about how tough it’s become to raise money for investment both at home and abroad, as high interest rates and bubbling geopolitical tensions bite. Many complained of the difficulty in offloading their investments, amid higher scrutiny of Chinese companies’ initial public offerings on both local and international markets.

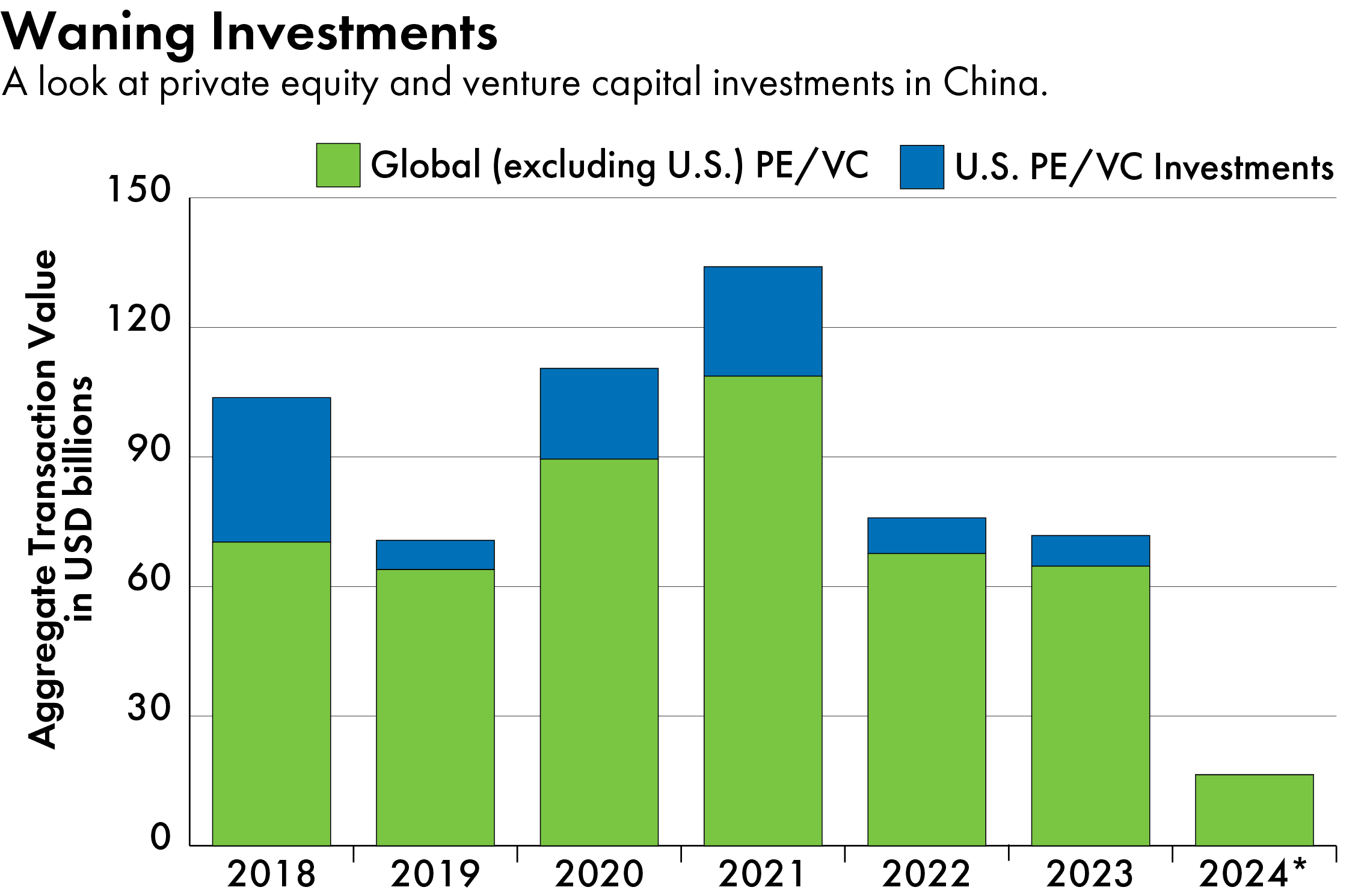

The figures bear out the gloom. Global private equity and venture capital investment in mainland China sank to $68.8 billion in 2023, a 52 percent plunge from the peak in 2021, according to S&P Global Intelligence.

That negative sentiment has persisted into this year as China’s real estate crisis and protracted consumer slowdown continue, alongside the lingering effects on entrepreneurs of a sweeping regulatory storm earlier this decade.

Total funds raised by Chinese private equity and venture capital firms in the first quarter hit a three-year low at 353 billion yuan ($49.7 billion), data from the Beijing-based market research firm Zero2IPO shows. Meanwhile, both the number of investments they placed and their value plummeted by 36.7 percent and 22.2 percent respectively, compared to the same period last year.

While investors have made double or even triple digit returns by betting on China in the past decade or more, they know those days are behind them, said Cate Ambrose, chief executive of the Global Private Capital Association.

“There will not be another time or place in the world where those types of returns are going to be made,” she said during a panel discussion at the event, organized by the Hong Kong Venture Capital and Private Equity Association.

We’ve already hit the bottom last year and we’re coming back. But this comeback doesn’t mean we’ll go back to 2019, pre-COVID [levels]. There will be a new normal…

Robert Chang, founder of GenBridge Capital

Yet despite the numerous reasons not to be cheerful, several fund managers who spoke during the conference and to The Wire said they had grounds for cautious optimism. The question uppermost in their minds is whether they can adapt their playbook to the new environment in China.

“People should give up on the hope that we can go back to the good old days,” said Yifeng Wang, head of China at Avenue Capital, a firm that trades in distressed debts, during one panel on private credit. “But against that backdrop, let’s think about how we can make money with lower liquidity, where the price is not going back and where public offerings are not available anymore.”

Part of the adaptation underway is a reassessment of the role the government is playing in China’s economy under Xi Jinping’s leadership.

“In the past, we just took it for granted that government policy supports growth,” said Rebecca Xu, managing director of Asia Alternatives, a private equity fund-of-funds. But, she added, the clampdown on sectors from tech to private education since around 2020 has underscored how sudden and unexpected policy changes can now be a significant risk.

In response, many investors are now betting on industries like artificial intelligence, clean energy and electric vehicles, which seem to be most aligned with government priorities.

Some are also spotting potential in more resilient segments of the consumer market. “We’ve already hit the bottom last year and we’re coming back,” Robert Chang, founder of GenBridge Capital, told The Wire. “But this comeback doesn’t mean we’ll go back to 2019, pre-COVID [levels]. There will be a new normal: In the consumer business, there will always be some companies winning.”

GenBridge, which focuses on companies in the consumer staples sector, raised $400 million for a new fund last June, according to Pitchbook, making it one of few China-focused funds to successfully close last year.

Other investors see a silver lining as Chinese companies try to find new markets overseas. “The mainstream vision is today Shanghai, tomorrow the world. [Chinese startups] want to build a product, a platform, a business that is not only catering to the domestic market, but also the global market,” Ian Goh of Shanghai-based early stage venture capital firm 01VC told The Wire.

Chinese private equity firms are also changing their approach to raising money, in part because of issues obtaining funds from American investors who increasingly see China as too risky. Many have flocked to the Middle East, home to some of the world’s largest sovereign wealth funds and numerous other wealthy investors. Still, building long-term relationships with investors from that region can take time, while many are also looking for more than just high financial returns.

“Very often my conversation with [Middle Eastern investors] includes whether you can bring some of the portfolio companies to [their] region and set up production facilities here,” said Yu Ren, a managing director at the alternative assets manager CDH Investments, speaking at one panel.

For some Chinese firms, the biggest pivot has been towards raising more funds in renminbi, where the dominant source is state-affiliated capital — be it from government guidance funds or state-owned enterprises. Taking care of these investors comes with its own set of challenges, however.

“While local and provincial governments have extensive funds, these frequently come with strings attached, such as pressures to invest in certain regions or even firms,” Josh Lerner, a professor of investment banking at Harvard Business School told The Wire in an interview.

Private equity firms have also tended to shy away from state-backed capital sources in China over concerns about political interference in decision-making, changing government objectives and a lack of professionalism, according to a recent study published in the Journal of Political Economy.

Supporting a domestic limited partner requires a team that is double or triple in size in order to handle day-to-day services and other non-investment related work, said Piau Voon Wang, managing director of Legend Capital, which manages over $10 billion in assets.

No one is counting out China in the long run. But there is going to have to be a reset in terms of how the industry is scaled.

Cate Ambrose, chief executive of the Global Private Capital Association

But with foreign investment dwindling, Chinese fund managers may be left with little choice but to look for more capital domestically, alongside having to refocus their investment strategies.

“What’s required in China is a complete reinvention of the model,” said Ambrose, of the Global Private Capital Association. “No one is counting out China in the long run. But there is going to have to be a reset in terms of how the industry is scaled.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.