Dalian Wanda spared no expense when it built Wanda Reign on the Bund, an opulent hotel that opened on Shanghai’s famous waterfront in 2016. It hired British architect Norman Foster’s studio to design its modern exterior and fashion designer Laurence Xu to create the staff uniforms. The works of celebrated Chinese artists like Huang Gang and Shi Qi graced its walls.

Just eight years on, the Chinese conglomerate has sold the luxury hotel to Indonesian tycoon Sukanto Tanoto for less than half of its $516-million investment. Singapore-based Pacific Eagle Real Estate, controlled by Tanato, acquired the property for as much as $234 million, real estate intelligence firm Mingtiandi reported earlier this month.

The knock-down sale comes as part of Wanda’s efforts to offload some of its prized assets in China amid a liquidity crunch. The company, headed by China’s former richest man Wang Jianlin, has been on a global retreat since China started tightening credit conditions in 2017. But the unwinding of its empire has intensified amid the broader downturn in China’s real estate sector, where developers can no longer rely on high-leverage financing to fund their growth.

“A lot of developers and real estate investors were very used to the China market only really going in one direction,” says Michael Cole, founder and chief analyst at Mingtiandi. “The one thing that Wanda has in common with the residential developers is that it took outsized risks. It borrowed money on high-risk bets and when those high-risk bets did not work out, it very rapidly got into trouble.”

The story of how Dalian Wanda first fell into financial difficulty is well known: the conglomerate, whose interests once spanned entertainment and media to sports and yachts, saw its fortunes reverse after its founder Wang Jianlin fell out of favor in Beijing, amid Chinese leader Xi Jinping’s tightening grip on the private sector. But while Wanda may have faded from the headlines, the recent deepening of its difficulties demonstrates the ripple effects of China’s property market and economic downturn.

For a while, Wanda seemed to have fared better than its counterparts such as Evergrande, once China’s largest real estate developer. Wanda’s diversified portfolio to some extent insulated the company from market shocks last year even as China’s property sector collapsed.

A major problem for the company in the last year has been with its efforts to hive off Zhuhai Wanda Commercial Management Group — an entity controlled by Wanda’s commercial property arm Dalian Wanda Commercial — through an initial public offering in Hong Kong that, it was hoped, would raise up to $4 billion. Zhuhai Wanda manages over 494 plazas across 227 cities in China, making it the world’s largest operator of shopping malls.

All four of Wanda’s efforts to take the unit public on the Hong Kong stock exchange since late 2021 have lapsed — the latest application, submitted in July, expired last month — due to weak market conditions and regulators’ concerns over the company’s past operational reporting. The Chinese authorities have also asked Wanda for assurances the IPO proceeds would not be used in property development, a sign Beijing is worried about sending mixed signals that could contradict its desire to tame the country’s real estate sector, says Shen Meng, a director at Beijing-based investment bank Chanson & Co.

“Figures reported in [Zhuhai Wanda’s] prospectus are also overly optimistic, which leaves little room for growth after its listing,” he says. “In which case, Chinese regulators would also be cautious.”

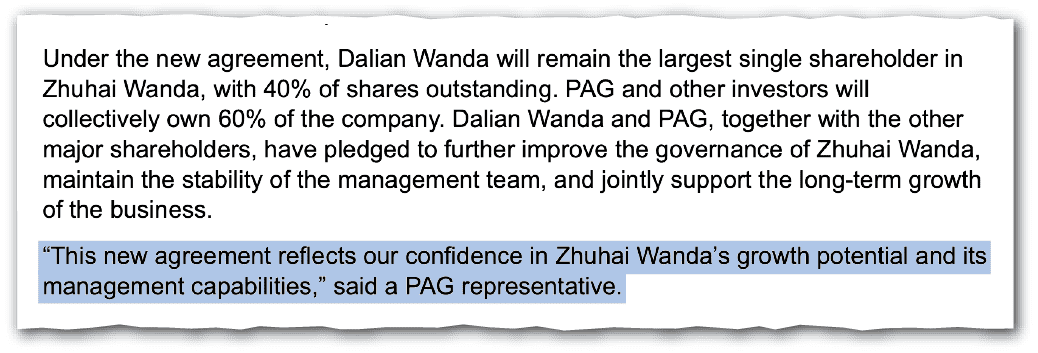

The unit’s failure to list threatened to breach an agreement made with a group of investors including private equity firm PAG, run by industry veteran Shan Weijian: The group had invested some 38 billion yuan (US$5.9 billion) in Zhuhai Wanda in 2021 on condition it would IPO by the end of 2023. Dalian Wanda cut a deal with the investor group in December to forestall having to repay that amount, but only by ceding control of the business, lowering its stake in Zhuhai Wanda to 40 percent.

That new agreement has bought the company some time. It is also hoping creditors will soon agree to extend the repayment of a $600 million bond issued by another subsidiary, Wanda Properties International, that had been due later this month – to December this year. But the crisis at Dalian Wanda is far from over.

“The deal with PAG has removed certain obligations with the pre-IPO investors. Nonetheless, Wanda Commercial still has 11.5 billion yuan’s ($1.6 billion) worth of bonds maturing in the next 12 months,” says Chloe He, director of Asia-Pacific Corporate Ratings at Fitch Ratings.

To ease the strain, Wanda has been offloading other assets. Founder Wang Jianlin has sold his remaining 51 percent stake in Wanda’s film unit to the Tencent-backed entertainment company China Ruyi for an undisclosed sum, according to a stock exchange filing in December, spelling an end to his dream of building an Asian Hollywood.

Wanda’s Acquisitions… and Sales

ACQUIRED FOR: $2.6 billion

ACQUIRED FOR: $500 million

ACQUIRED FOR: $365.7 million

ACQUIRED FOR: $54 million

ACQUIRED FOR: $1.1 billion

ACQUIRED FOR: $650 million

ACQUIRED FOR: $3.5 billion

ACQUIRED FOR: $82.7 million

Between 2012 and 2016, Dalian Wanda expanded globally, primarily into movies and sport. Above are selected acquisitions, with Wanda’s investment amount as well as the current status. Source: Wanda and media reports

Moreover, Dalian Wanda sold at least nine signature plazas in high-value areas, such as Shanghai and Guangzhou, in the second half of last year and one earlier this month, according to Chinese media reports. The company has also been searching for investors to take over the Swiss-based Infront Sports & Media, a marketing agency it acquired for $1.2 billion in 2015, Reuters reported in August.

Dalian Wanda’s scrabbling to offload assets is a typical strategy for Chinese conglomerates struggling to stay afloat, says Anne Stevenson-Yang, co-founder of J Capital Research, a stock research company.

In this day and age, those [connections] are more likely to be liabilities than they are assets for [Wang] to try to save his business.

Rick Carew, a private investor and a visiting scholar at the National Cheng-Chi University in Taipei

“They [Dalian Wanda and other real estate companies] have way too much debt. And in order to keep their heads above the water and meet some upcoming obligations, they’ll sell off an asset. They scrape together enough cash to roll over,” she says. “It’s the story of the whole Chinese real estate sector, just scraping by and in order to keep from a big public crash. But basically, the real story behind this is not good.”

Yet according to ratings agency Moody’s, the assets sales can only partially mitigate Wanda Commercial’s liquidity needs, given its cash on hand has reduced sharply over the past year.

“The execution of asset disposal plans entails high uncertainty in view of the weak market conditions,” a spokesperson from Moody’s told The Wire China.

In another sign of trouble, Ding Benxi, a retired president of Dalian Wanda and a non-executive director of its hotel arm, has been out of contact since September, according to a stock exchange filing. His disappearance came a month after three senior executives were placed under investigation, Chinese outlet Caixin reported. In February, Qu Dejun, another former executive who previously led Wanda’s fintech business, went missing and was assisting authorities with a probe related to Wanda, according to Caixin.

“Wanda has been the target of a series of probes over the years and there has been this kind of dance with officials about not letting the company go bankrupt and not going after it in the same way they went after HNA or Anbang or companies like that,” says Meg Rithmire, an associate professor at Harvard Business School who studies China’s political economy.

But while Wang’s wits and political ties have helped his company sail through previous clampdowns on corporate leverage and the private sector, analysts agree the situation looks bleaker this time.

“In this day and age, those [connections] are more likely to be liabilities than they are assets for him to try to save his business,” says Rick Carew, a private investor and a visiting scholar at the National Cheng-Chi University in Taipei. “There’s really been a pushback from the bureaucracy and Xi to say these private sector high flyers are no longer welcome.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.