In 1999, a frustrated young entrepreneur wrote a letter to then-Premier Zhu Rongji. Huang Wenyun had made a small fortune for herself by capitalizing on Shenzhen’s manufacturing boom and selling educational toys, but her business had hit a wall: Her products were so successful that the market was being flooded with cheap knock-offs, eating up a chunk of her profits and delivering a major blow to her business.

Not one to sit around, Huang had gone on a hunt for solutions to what she saw as a broader problem in China’s business landscape: unfair competition. The 42-year-old toured eight U.S. cities and interviewed experts in business before concluding that a credit rating system would be instrumental in leveling the playing field.

“Maintaining fair competition would have an incalculable impact on the manufacturing industry and ensuring it could drive new economic growth,” Huang wrote to Zhu, advising him to build China’s own personal credit management system. “I am determined to contribute my knowledge and wealth in this regard.”

Remarkably, the Premier not only read Huang’s letter but also approved of her idea. At the time, China’s government was struggling to deal with the corporate scandals and financial scams that accompanied the country’s breakneck industrialization. Beijing had a lot on its hands: Triangular debt was threatening its economic growth; legal enforcement and regulatory compliance were weak; and infrastructure for credit reporting and market supervision all had to be built from scratch.

But Beijing didn’t see these economic challenges through only a financial or legal lens. There was also a growing perception of a moral crisis. A credit management system, leaders believed, could not only help good business people like Huang recover from unexpected hurdles, but also restore trust and guide the market. “The absence of credibility distorts economic relations, increases social transaction costs and corrupts public morals,” top policymakers wrote in a State Council report in 2001. “This has grown into one of the most outstanding problems that hinder the healthy operation of our national economy at present.”1From Financial Supervision to Morality Construction: Political Narratives of the Social Credit System Policy Process by Pierre Sel, a researcher at University of Vienna.

With Zhu’s blessing, Huang invested 300,000 yuan ($42,270) from her own pocket to fund a research group under the Chinese Academy of Social Sciences, recruiting among other scholars Lin Junyue, a U.S.-educated sociologist. Armed with the full texts of 17 credit-related U.S. laws, Lin went on to pioneer the idea of a “social credit system,” wherein businesses would be judged on how trustworthy they are. The logic, he recounted in 2019, is that “if every company is honest and trustworthy, it would improve the order of the market economy and reshape business ethics.”

By 2002, as Chinese leader Jiang Zemin proposed the concept of “rule of virtue” to complement the rule of law, he also officially announced the construction of a social credit system. And from that moment on, says Marianne von Blomberg, a research associate at the University of Cologne, “trust became a main governance paradigm.”

Indeed, two decades on, China is now home to a sprawling social credit system with hundreds of different versions. It has so many evolving components and goals that scholars have debated over the years how to best characterize it. It’s been described as an enforcement tool, an extension of the law, a surveillance system, a mere user interface for criminal records — and all of the above. While the details of how these various systems work — or don’t work — together are messy, the basic idea is that regulatory agencies share information and then add people and companies to blacklists for non-compliance.

But aggregating compliance data is just the first step. To create a wider dragnet, authorities not only impose joint punishment on bad actors, but also often publicly name-and-shame the blacklisted entities in order to encourage the market and the public to boycott them.

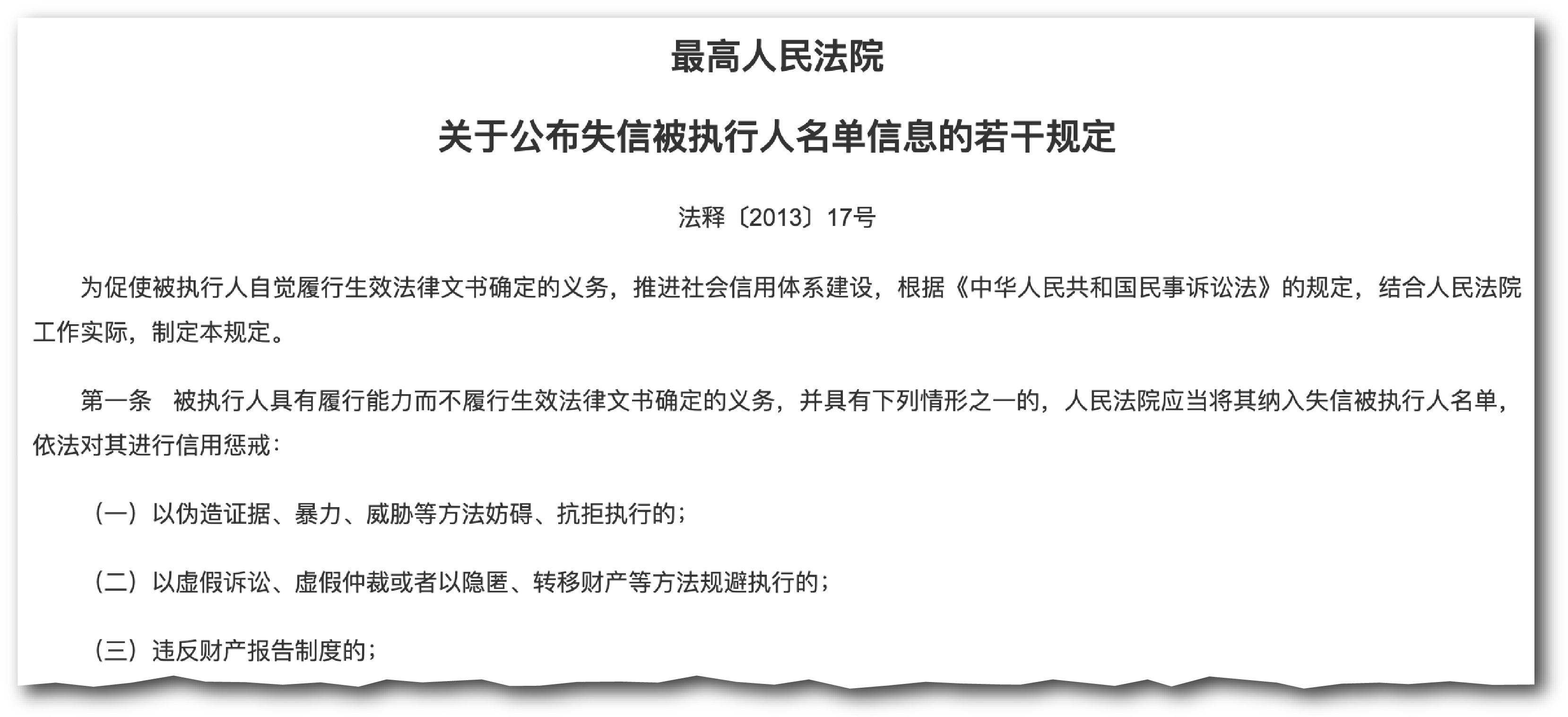

The most powerful blacklist today, for example, is the Supreme People’s Court’s List of Dishonest Persons subject to Enforcement, under which defaulters (often called laolai, meaning deadbeats) are barred from sending their children to private schools, traveling by plane and buying properties, among other restrictions on luxury spending. According to official statistics, from its promulgation in 2013 to the end of 2018, nearly 13 million individuals have been placed on the List of Dishonest Persons. Some local governments put the squeeze on defaulters by airing their personal information in public, and some developers even created apps to show users if a laolai is in their vicinity.

“The aspiration is that within 10 or 20 years, by virtue of these mechanisms, you will gradually weed out the bad eggs,” says Alexander Trauth-Goik, a researcher at the University of Vienna. “And eventually you get a self-correcting, more cohesive, trustworthy, market-based environment.”

In the interim, however, China got comparisons to Big Brother.

Not surprisingly, Beijing’s efforts to promote “trustworthiness” in society were quickly characterized in foreign discourse as a tech-driven panopticon that monitors and rates citizens’ every move. In a 2018 speech, former U.S. vice president Mike Pence famously described it as “an Orwellian system premised on controlling virtually every facet of human life.”

“The West considered it a ‘big data’ thing,” says Fan Liang, an assistant professor at Duke Kunshan University’s social sciences division. “They thought there was a centralized system and everyone was constantly being monitored.”

But, as it turns out, neither the West’s interpretation of, nor Beijing’s original goals for, the social credit system have borne out. Even for an authoritarian state known for its ability to harvest vast amounts of data from its citizens, the social credit system’s implementation over the past 20 years has been surprisingly mundane, incohesive and, in many aspects, more dysfunctional than dystopian.

Local governments in China have a very high capacity to get things done. But even for them, setting up an individual scoring system of their citizens is almost impossible.

Genia Kostka, professor of Chinese politics at the Free University of Berlin

In fact, China’s grand experiment with a social credit system appears to be at a standstill, if not fizzling out entirely. Local governments have run into deep-rooted problems in their efforts to make social credit systems operational, including data silos, inconsistent standards and bureaucratic pushback. And many local pilot schemes have strayed so far from the initial conception that Beijing has had to issue a series of high-level documents in recent years to rein in overzealous and wacky applications.

The whole idea of a social credit system in China, says Adam Knight, a researcher at Leiden University, “has had a lot of the energy taken out of it. From a central government perspective, things have cooled off a lot.” China is now in a “post-social credit era,” says Knight, with a lot of the local schemes either significantly altered or shut down entirely.

China is hardly any closer to creating an honest society or one where, as the government motto puts it, “the untrustworthy are unable to move a single step.” And yet, ironically, the post-social credit era might finally deliver what Huang set out to do: improve market regulation and corporate governance.

CREDIT CHECK

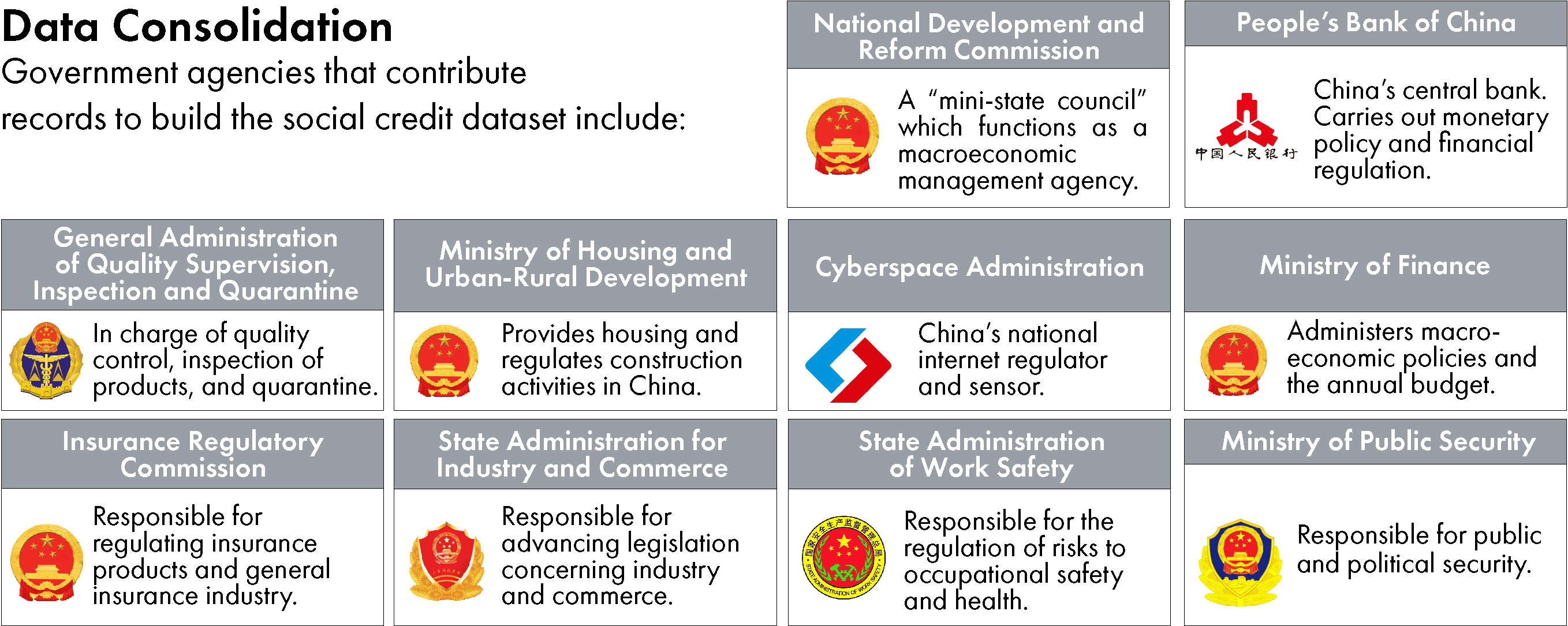

Despite Beijing’s early enthusiasm for the idea, China was slow to get the social credit ball rolling. In 2006, the People’s Bank of China launched the Credit Reference Center — a national commercial and consumer credit reporting system — but apart from that, the field was largely stagnant for years. But that all changed in 2014, when Beijing issued a planning outline for social credit systems and kicked off a race among localities and ministries to build the best system.

The idea was deliberately flexible: Beijing established a framework, but different authorities could decide how it would be implemented on the ground, including how or what data to collect.

“This was a conscious policy of experimentation on the government’s behalf. It essentially set out the broad parameters of what social credit should and shouldn’t do. But it didn’t lay out any of the details as to how this is actually going to work,” says Knight. “What that means is you get hundreds of different versions of social credit, all slightly different from each other.”

Between 2007 and 2019, the number of central agencies and departments involved in constructing a social credit system jumped from 15 to 46, and municipalities around the country launched initiatives that often went far beyond determining just one’s financial profile and credit risk. According to Knight’s research, at the social credit system’s peak, around 2019, the central government was actively tracking about 650 different city schemes and monitoring their performance.

One of the most extreme versions was in the coastal town of Rongcheng, Shandong, which in 2014 started giving each of its 738,000 residents not just a social credit grade, but also a score. Integrating data from dozens of local departments and deploying grassroots officials and volunteers with clipboards to take copious notes, it calculated the score of its residents based on 391 indicators. According to its standards assessment in 2019, a person’s score would be deducted five points for jaywalking, ten for extravagant weddings and 50 for spreading negative information on WeChat, while good Samaritan acts and blood donation added to their score.

The accumulated score decided their grade, which came with preferential treatments in public services as rewards or suspension of subsidies as penalties.

| ACTION | SCORE |

|---|---|

| Providing false materials, concealing the truth, harming the order of social management and the public interest | -30 |

| Plagiarism, Copying, and other academic misconduct | -40 |

| Fraud, cheating, and falsification in a unified examination | -40 |

| Fraud in academic research, professional title evaluations, and other such work | -40 |

| Employing illegal methods to fraudulently obtain honors or programs | -50 |

| Obtaining administrative permits, administrative confirmations, administrative payments, and related operations by improper means such as deception or bribery | -50 |

| ACTION | SCORE | LIMIT |

|---|---|---|

| Returned between 100 – 1000 RMB | +2 | Max 10 points per year |

| Returned between 1001 – 5000 RMB | +3 | |

| Returned between 5001 – 10,000 RMB | +5 | |

| Returned more than 10,000 RMB | +10 |

Source: China Law Translate

Rongcheng’s system was often showcased in media reports, but according to experts, it was unique among local governments. While Beijing’s 2014 plan did motivate local governments to devise systems, very few were actually adopted.

“Local governments in China have a very high capacity to get things done. But even for them, setting up an individual scoring system of their citizens is almost impossible,” says Genia Kostka, a professor of Chinese politics at the Free University of Berlin who has tracked public support for the social credit system since 2018. One of Kostka’s studies looked at 62 pilot projects and found that only half were developed enough by 2022 to track individuals as well as companies. Kostka’s survey respondents were also largely unaware of the systems’ existence in the first place.

“It’s almost like [the local government’s] symbolic display to the upper government level — just to say we are doing something, but they didn’t really full-heartedly invest in it,” she says.

When it comes to rating companies, many local governments also had trouble devising meaningful differentiation. Of 531 Chinese listed companies in Zhejiang, which has one of the country’s most advanced social credit systems for corporations, 90 percent received a good or excellent score. Only 6 companies, meanwhile, received a poor rating.

“You make this huge, time-consuming system for something you already knew from the beginning,” Kostka says. “They calculated the scores basically by looking at who pays their taxes and complies with regulations. But if you’re trying to weed out the bad apples, you don’t need this second, parallel system. You could just make sure you enforce existing laws and regulations better.”

According to Liu Chuncheng, a sociologist who has studied social credit systems since 2018, many local systems were shelved because they could not even get past the first bureaucratic step: sharing data among departments. “Most of the local credit systems failed because they cannot build this centralized data infrastructure,” Liu says.

By trying to do too many different things, you end up doing nothing at all. You turn this big data into dumb data.

Vincent Brussee, author of Social Credit: The Warring States of China’s Emerging Data Empire

Indeed, one state media report offered a glimpse into the painstaking negotiation that can go on behind the scenes: “To collect a broad, diverse range of data, we have to write up a list and go to individual departments,” Chen Lei, a government official responsible for data aggregation in Shandong province, told People’s Daily in July. “Many also complained to us that their data is on paper and in order to aggregate and feed it to our platform, they would have to enter it into a computer manually, which is time and energy consuming.”

With many municipalities dragging their feet, it was the heavy-handed “success stories” like Rongcheng that stood out — and sparked debate among legal scholars and policymakers. According to Knight, Chinese policymakers and legal scholars were “horrified” by what they saw in Rongcheng. “Many of these behaviors, frankly, are not illegal,” he says. “So, there was no legal basis for what they were punishing people for.”

Moreover, the overreach seemed to undermine the government’s original goals.

“By trying to do too many different things, you end up doing nothing at all. You turn this big data into dumb data,” says Vincent Brussee, author of Social Credit: The Warring States of China’s Emerging Data Empire. The pushback from both legal scholars and local communities, he says, “made the Chinese government realize that if they continued in this way, they would harm the goals that the social credit system set for itself.”

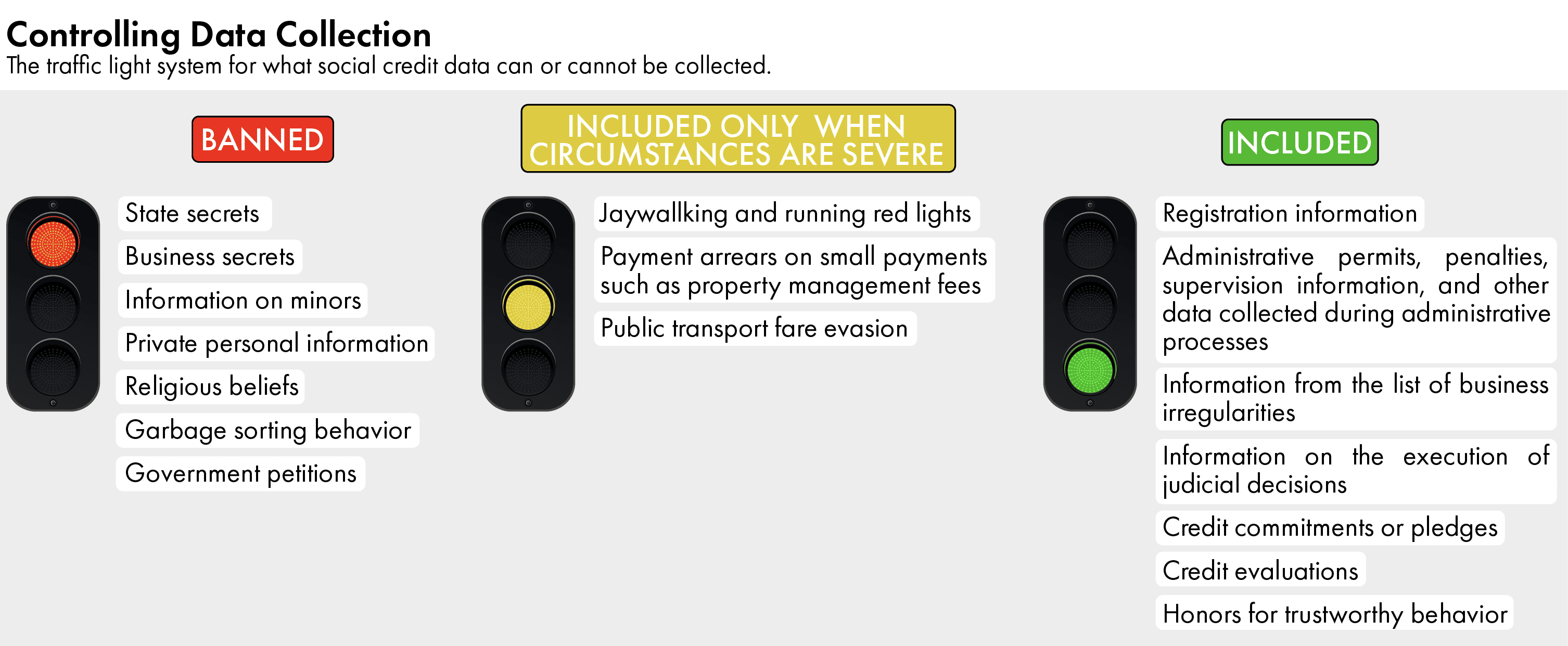

Beginning in 2019, the State Council issued a raft of guiding opinions that effectively throttled schemes like the one in Rongcheng. The documents standardized the type of information that can or cannot be logged under the scope of social credit as well as the range of disciplinary measures. All penalties must also have a legal basis in national legislation, and only serious violations can be blacklisted.

To comply with the new rules, Rongcheng quickly made a U-turn, turning their schemes into opt-in programs without penalty for low scores.

Though the reform is a step in the right direction, analysts say it did not resolve a fundamental problem with the system. Clement Yongxi Chen, a lecturer at the Australian National University College of Law, argues social credit has created a new system of punishment based not on the legal liability of individuals, but on the fictional notion of trustworthiness. “Many laws and regulations have been amended to incorporate this rather ambiguous notion,” he says. “It basically creates a mechanism for the Party and the State Council to leverage when they consider it necessary or convenient.”

Such as when there is a public health emergency.

DUE CREDIT

Despite Western characterizations of the all-seeing, all-knowing Orwellian system, the vast majority of Chinese society wasn’t really aware of social credit systems for much of the 2010s. The systems, according to researchers, rarely and barely impacted everyday life.

But the Covid-19 pandemic changed all that.

“Since the beginning of this project, the social credit system has been viewed as a catch-all — kind of like a Swiss Army knife solution to a lot of different problems,” says Trauth-Goik. “Effectively all local governments and agencies needed to do was create a new regulation, open a social credit website, and then implement a new blacklist — and that’s exactly what we saw during Covid.”

To punish noncompliance with Covid measures, for instance, Shanghai introduced a blacklist and recorded 96 infringements in less than a month. Weihai, a coastal city in the eastern province of Shandong, deducted points from office workers who were found working without their masks on.

Hangzhou went even further, attempting to replace the health code with a system that rates residents’ health on a scale of 0-100 based on their lifestyle. For example, a 1.5 point deduction for consuming 200 ml of alcohol; a 3 point deduction for smoking 5 cigarettes; or a 1 point bonus for sleeping 7.5 hours a day. The proposal drew such a huge backlash that authorities backtracked four days after announcing the initiative.

“Suddenly, everyone in the country was concerned with these questions of proportionality that the legal community had been warning about,” says Brussee.

Including some of the system’s original architects. In a series of essays on Caixin, Wang Lu, a former official at the central bank’s credit rating department, lambasted local officials for “hijacking” the concept of personal credit and turning it into a basket, in which they dump all their governance issues. The widening notion of personal credit, he warned, was “a bullet running wild.”

By the end of 2020, the central government decided the grand experiment may have run its course and started ‘re-centralizing’ the social credit system. At a press conference on Christmas day, Lian Weiliang, deputy director of the National Development and Reform Commission (NDRC), the macroeconomy planning agency that spearheaded the policy alongside the People’s Bank of China, admitted that some local initiatives were not well-established and meted out penalties without proper legal grounds. “These issues have affected the rights of individuals and market entities, and undermined the long-term development of the social credit system,” Lian said.

Following a series of restrictions on social credit, the NDRC and the central bank together released a draft for national social credit legislation in 2022. The goal was to define the system, give it a legal framework and ideally, a future direction, but experts say the draft law didn’t answer much. Most importantly, it was still plagued by social credit’s original sin: the bundling of moral behaviors and regulatory compliance with financial creditworthiness.

“The idea was that legal compliance in one area would help predict legal compliance in other areas,” says Jeremy Daum, a senior fellow at Yale University’s Paul Tsai China Center. “But once you start trying to make it into a useful system, you suddenly realize that these areas aren’t necessarily as linked as you thought.”

The social credit experiment did a lot to advance the state’s capacity and understanding of how to use data and information for governance. But it’s not a societal thing anymore.

Adam Knight, a researcher at Leiden University

A person’s ability to pay back loans, after all, has little to do with their proclivity for skipping bus fares — and even less with their willingness to wear a face mask during a pandemic. But the draft law, which Daum calls a “Franken-Law,” was still trying to stitch disparate areas together.

Going forward, some scholars say there are signs that China may finally be learning from social credit’s flaws and letting go of the idea of regulating trust.

Since 2015, for example, the NDRC has poured a staggering amount of information into a master database, called the National Credit Information Sharing Platform, to help monitor corporations and market entities. By aggregating data from 46 different government agencies — including tax arrears, annual reports, public utility payment history and red and blacklist records — the platform would offer a cohesive view of a corporation or a market entity’s behavior.

“There’s no comparable credit system in the world that integrates such a broad perspective of compliance and behavior,” says Mirjam Meissner, a managing partner with the China-focused research consultancy, Sinolytics.

But progress has been slow and difficult to track. Meissner notes that data integration and sharing remains a problem as does transparency. “There’s not a go-to page [for the platform], and the information is not systematically shared to the [public-facing] Credit China platform,” Meissner says. “Companies need to go to very specific, local platforms, or sometimes even reach out to local authorities to get their ratings.”

Having watched these challenges over the years, the State Administration for Market Regulation (SAMR) is now building a database of its own — and taking it in a very different direction.

First created in 2018, SAMR combined different market regulators, thus overcoming the data silo problem. By mining government data as well as public opinion online, SAMR determines an entity’s “credit risk.” Crucially, says Brussee, “it’s not trying to assess the moral trustworthiness of a company based on a thousand meta-factors; it’s just about how likely is a company to commit a regulatory violation and how severe will the impact be if it does.”

In addition to having a more focused goal, von Blomberg says SAMR has also sidestepped the legality problem by tying its results to soft measures, such as a higher rate of inspections, instead of punishments. The initiative, which ran as a trial in Shandong province in 2021, is set to be operational across the country by 2025, and the hope is it will enhance bureaucratic efficiency and improve corporate performances.

“It’s almost like they’re going back to the beginning a little bit,” says Knight. “The social credit experiment did a lot to advance the state’s capacity and understanding of how to use data and information for governance. But it’s not a societal thing anymore. It’s in the commercial space.”

China’s commercial space, however, is currently facing a very different economic environment than it did in the 1990s, when social credit was first conceived, and some analysts note that the post-social credit innovations could end up constraining Chinese businesses at a delicate time. The big question going forward is how much additional pressure Beijing wants to put on its companies.

“It’s possible that the government is losing interest,” says Brussee, “especially since social credit is no longer this fancy enforcement tool for every other problem in society. We’re really at a standstill for the system. And it’s at risk of stalling altogether.”

Click here to read another cover story from Rachel Cheung on the race to regulate AI.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.