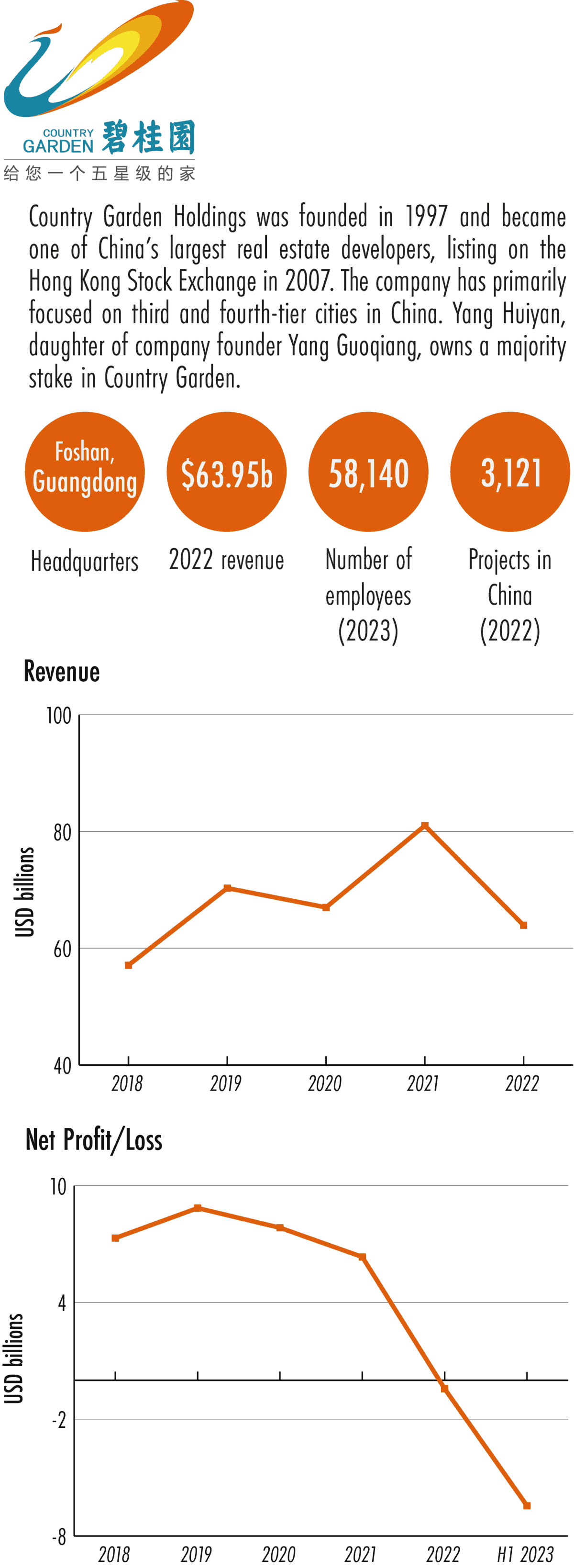

Few companies are more synonymous with China’s long property boom than Country Garden, whose rise to become the country’s largest real estate developer mapped the market’s long expansion.

Late Tuesday, however, Country Garden entered the annals of Chinese corporate ignominy, after failing to make a $15 million coupon payment that was due on a portion of its $10 billion of dollar-denominated debt held by global investors.

This week, The Wire looks at the rags-to-riches — and back to rags — story behind Country Garden, and examines whether it has a path out of its present predicament.

BECOMING A BILLIONAIRE

Country Garden’s origins lie in the southern Chinese city of Foshan in Guangdong, which became an industrial heartland during China’s era of market reforms. In 1994, amid early moves to reduce the state’s role in the property market, the local municipal government asked budding entrepreneur Yang Guoqiang if he would acquire a development project then under state ownership.

Yang, a former construction worker who was then the general manager of the project, convinced four business partners to join him in investing 80 million renminbi ($9.66 million) in Shunde Sanhe Property Development. The group went on to establish Country Garden in 1997, according to former chief financial officer Wu Jianbin, who documented the company’s early years in his book: My 1,000 Days at Country Garden.

“Particularly in property, local government is key, because they’re the ones who are ultimately finding you the land blocks,” says Fraser Howie, an independent analyst and co-author of the book Red Capitalism.

“If you were operating a property company in the early 1990s, in some ways you’re almost a decade ahead of the field,” Howie adds.

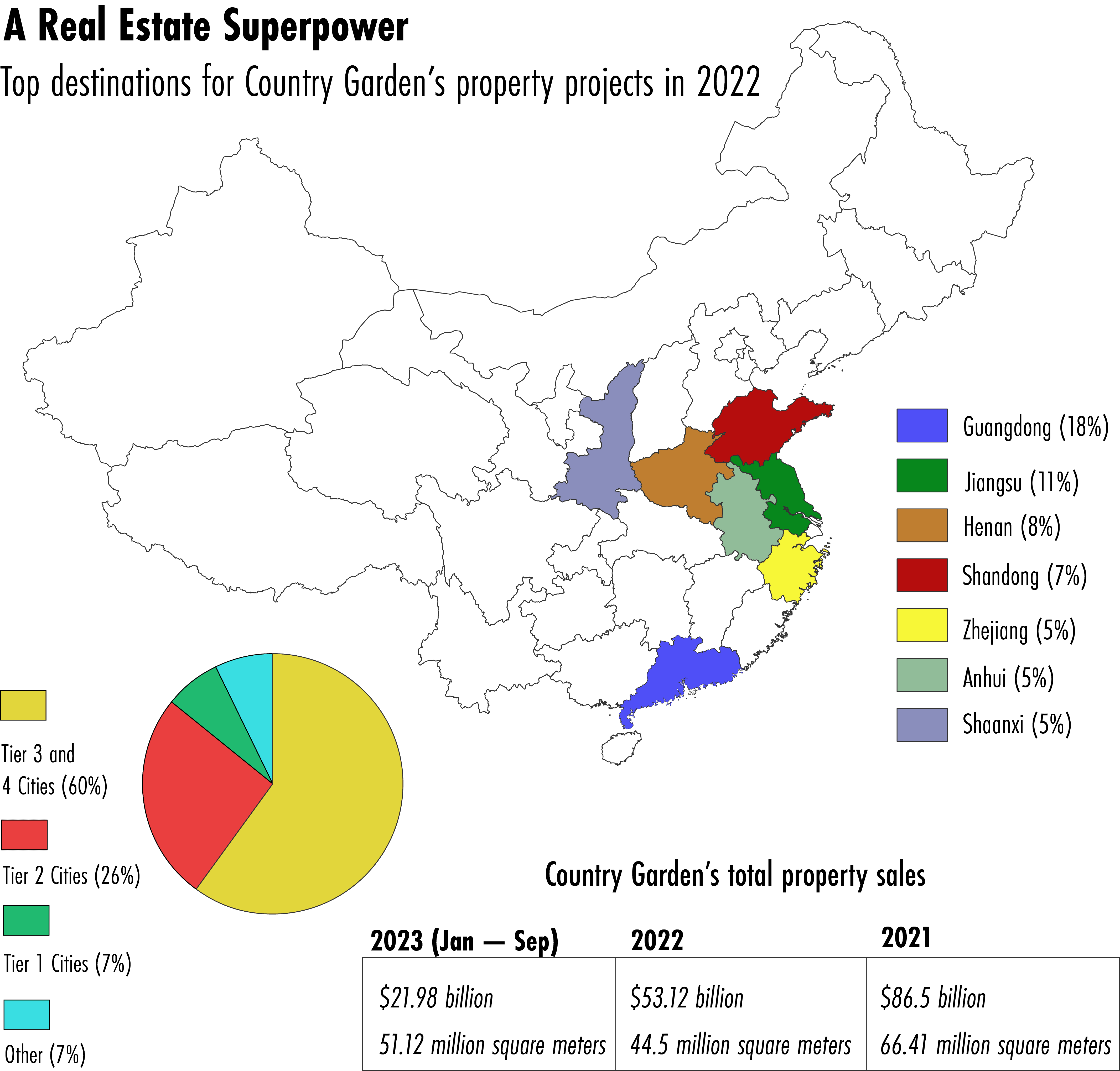

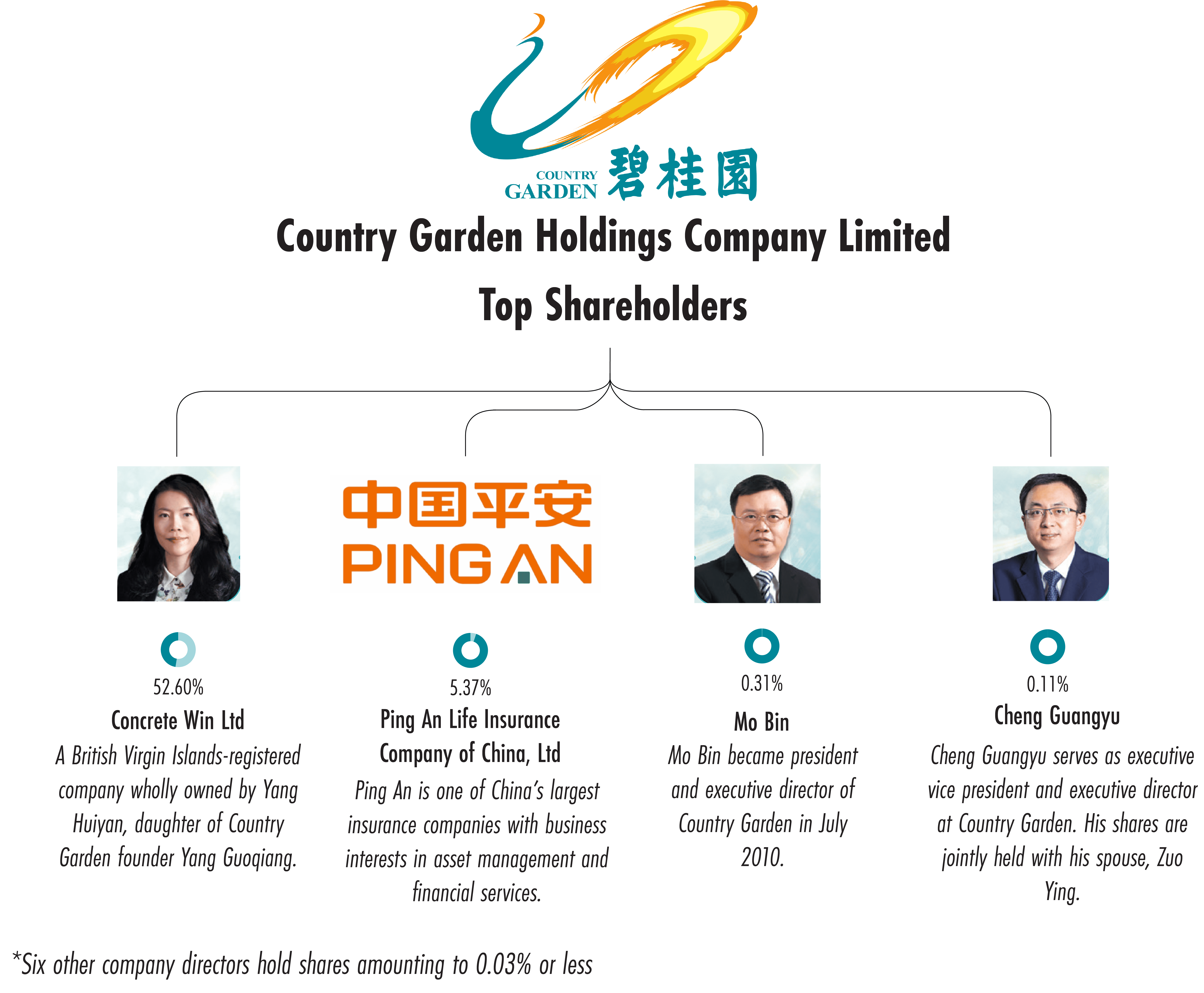

Country Garden’s subsequent growth followed the trend of urbanization and development across China. The company based the majority of its construction projects in third and fourth-tier cities, as well as in suburban areas outside major cities. In 2005 and 2006, Yang and other senior executives transferred a 70 percent stake in the company to Yang’s daughter, U.S.-educated Yang Huiyan, intending to train her as his successor in the family business.

“That stood out because it’s China, and very seldom are you coming across a woman CEO or billionaire,” says Howie.

In 2007, Yang Huiyan became the world’s youngest female billionaire when Country Garden raised $1.65 billion from its initial public offering in Hong Kong. At age 26, she had a fortune of $16.2 billion on paper, according to a Forbes estimate from 2007. As of October 16 this year, Forbes estimates that fortune has dwindled to $3.6 billion. 68-year-old Yang Guoqiang retired in March this year, citing his age, leaving Yang Huiyan as Country Garden’s sole chairperson.

TROUBLE IN PARADISE

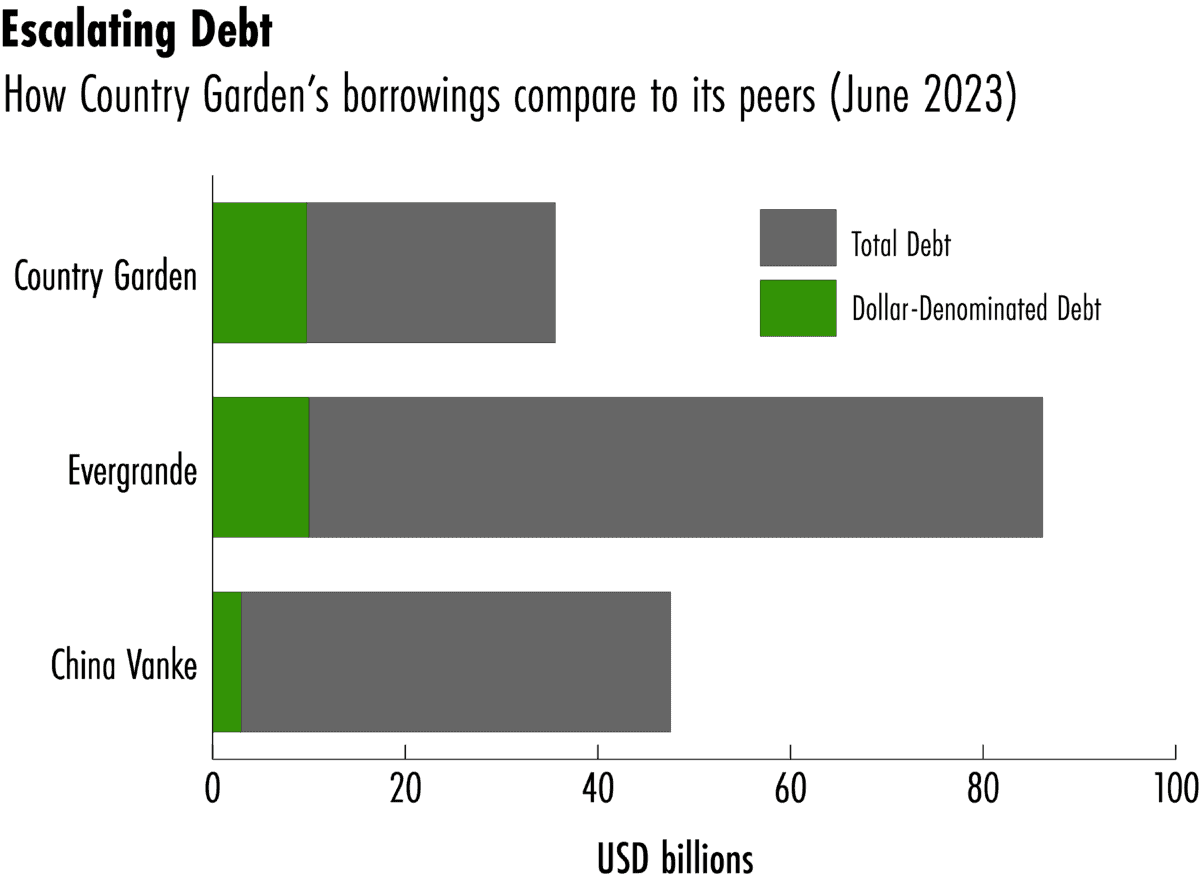

Country Garden became China’s largest private developer by total sales in 2017, when its contracted sales reached 550.8 billion renminbi ($84.7 billion), ahead of its closest rivals Evergrande Group and China Vanke. While its debt had reached $33 billion by that stage, it was only about one-third the level of Evergrande’s.

“The leveraging for Evergrande was always a lot worse than that of Country Garden,” says Victor Shih, director of the 21st Century China Center at the University of California in San Diego. “Country Garden was seen as generally a lot healthier because they had a rule of trying to sell their properties as fast as possible.”

Despite this, a storm of regulatory challenges was imminent.

During that same year, Country Garden’s largest overseas development project, Forest City on the southern tip of Malaysia, hit a setback when China abruptly imposed controls on its citizens moving their wealth out of the country to buy property abroad. The restrictions meant the $100 billion megaproject, a signature component of the Belt and Road Initiative in Malaysia, would have to rely on non-Chinese buyers. The project’s goal of housing 700,000 residents by 2035 is now riddled with uncertainty.

PRECARIOUS PRIVATE POWER

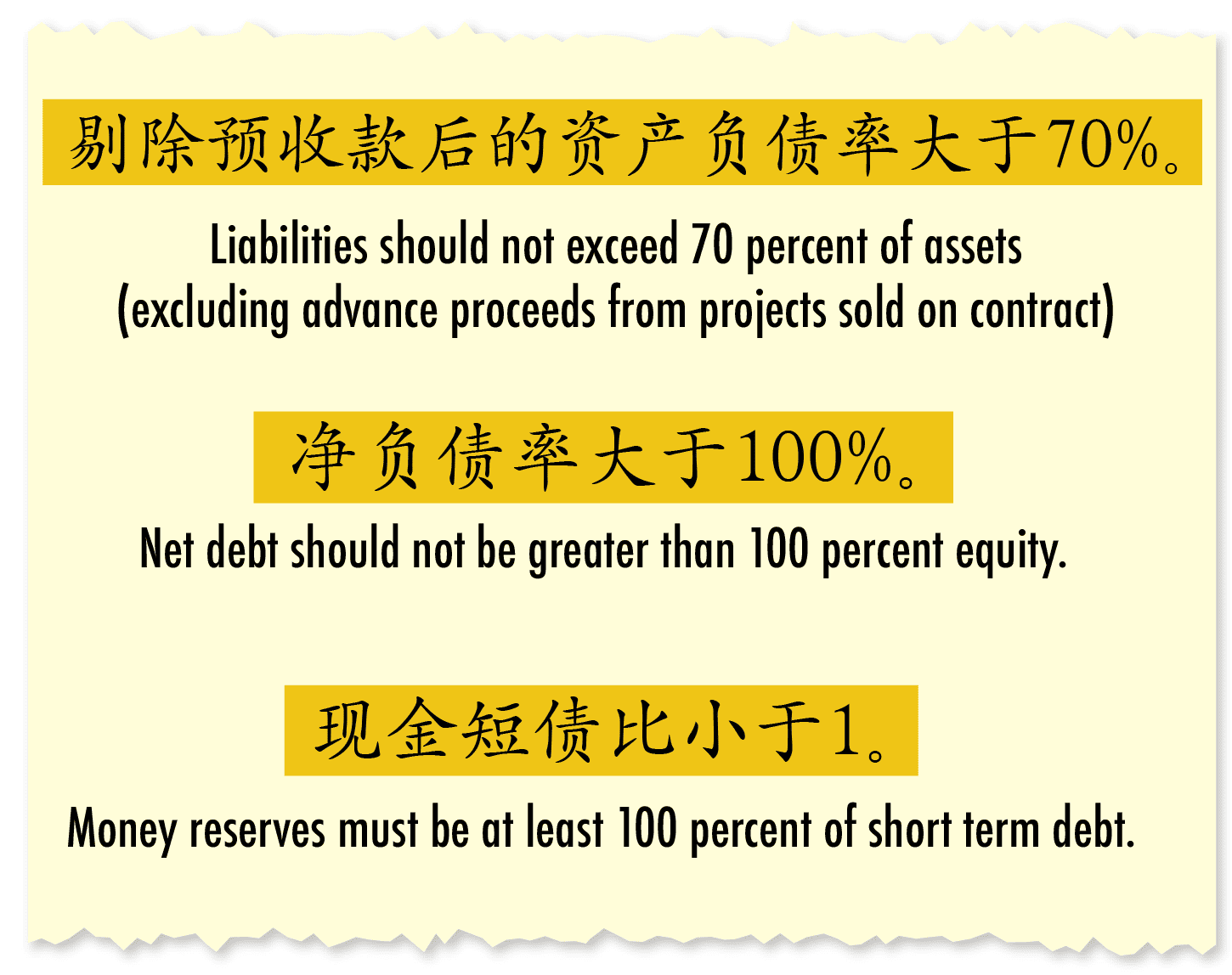

In 2017, Xi Jinping declared that “housing is for living in, not for speculating on,” a catchphrase often repeated during the following years as property developers’ debt levels became an increasing concern for the Chinese government. In August 2020, this principle evolved into the “three red lines” policy, which sought to rein in private developers by limiting the amount of debt they could accumulate relative to their equity. Country Garden was not immune to the consequences.

The limitations on developers’ ability to borrow forced them to rely more on pre-sales — selling homes before they are ready for occupants to move into — for cash flow. This came at exactly the wrong time, as the pandemic inhibited prospective buyers from moving ahead with purchases.

“Demand was going to weaken anyway because of demographic issues, then there was COVID, so sales plummeted at the same time that the developers’ ability to roll over their debt was highly constrained,” says Shih from UCSD.

On October 10, Country Garden said its revenue from contracted sales for September had plummeted to 6.17 billion renminbi ($876 million), down 81 percent from the same month in 2022.

“That’s what killed Country Garden — other doors being shut: financing, banks, onshore bond markets, and the fact that the pre-sales, which became the one and only mechanism to finance projects, died out because of zero-COVID policies,” says Alicia García-Herrero, chief economist for the Asia Pacific at investment bank Natixis.

If Evergrande can fail, then so can Country Garden. If they too can fail, then almost anybody in the sector can fail.

Fraser Howie, an independent analyst and co-author of the book Red Capitalism

By the end of June, Country Garden’s total debt had risen to $36.5 billion, of which around $10 billion is denominated in dollars and issued offshore — that is, outside China, according to research firm CreditSights. The company has recently managed to reschedule some of its onshore debts. But in its October 10 statement, Country Garden admitted it would “not be able to meet all of its offshore payment obligations when due or within the relevant grace periods.”

Although the prospect of a debt default raises the question of a government rescue, analysts expect few moves in this direction from Beijing.

“There has been some relaxation of real estate policies, but because this policy of ‘housing is for living and not for speculation’ is a very well-known policy of Xi Jinping, they cannot roll back the policy, they can only relax it gradually,” says Shih from UCSD.

Instead, others predict a larger role for state-owned developers in the future.

“It’s going to be much tougher for any private developer to have the leverage and the position that they once had,” says independent analyst Howie. “If Evergrande can fail, then so can Country Garden. If they too can fail, then almost anybody in the sector can fail.”

Aaron Mc Nicholas is a journalist based in Washington DC. He was previously based in Hong Kong, where he worked at Bloomberg and at Storyful, a news agency dedicated to verifying newsworthy social media content. He earned a Master of Arts in Asian Studies at Georgetown University and a Bachelor of Arts in Journalism from Dublin City University in Ireland.