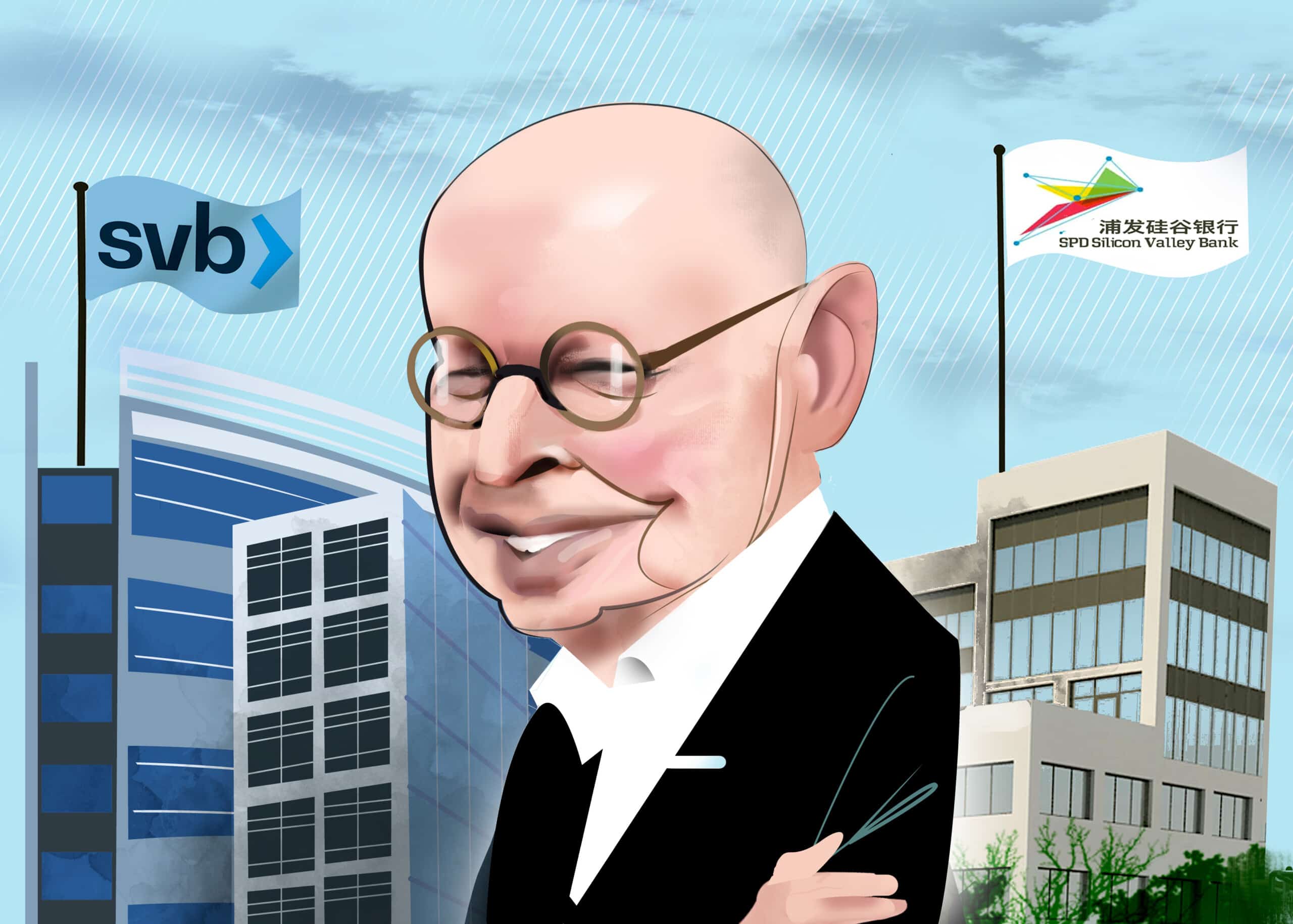

Silicon Valley Bank's former CEO reflects on the bank's challenges in China.

Illustration by Luis Grañena

In April 2011, I had just turned 63 and was supposed to retire after a 30-year career at Silicon Valley Bank (SVB), the final decade of which was spent as CEO. Somehow, things turned out a little differently.

Rather than pursue hobbies or get involved with nonprofits, my wife and I moved to China. SVB’s Board had asked me to found a brand-new bank: the Shanghai Pudong Development Silicon Valley Bank (SPD SVB), a joint venture between SVB and the state-owned Shanghai Pudong Development Bank.

Exclusive longform investigative journalism, Q&As, news and analysis, and data on Chinese business elites and corporations. We publish China scoops you won't find anywhere else.

A weekly curated reading list on China from Andrew Peaple.

A daily roundup of China finance, business and economics headlines.

We offer discounts for groups, institutions and students. Go to our Subscriptions page for details.

California-based Jupiter Systems sold high-tech wall screens to U.S. military and government clients. On June 14, The Wire China revealed how Jupiter was sold to a Chinese company in 2020 without the first Trump administration’s knowledge. Now Trump is back and on the case as Jupiter teeters on the verge of bankruptcy.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.