During the 2017 Chinese New Year, late at night, a well-connected Chinese-born businessman named Xiao Jianhua was abducted from his apartment in the Four Seasons Hotel Hong Kong, apparently in coordination with Chinese law enforcement. The bewildered billionaire was placed in a wheelchair, covered in a blanket and rolled away. Later, he reappeared in Shanghai, where last year he was sentenced to 13 years in prison on corruption charges.

But Xiao’s plainclothes captors had been breaking the law too: The Chinese security agents were not authorized to operate in the city.

On paper, Hong Kong is a “special administrative region.” Its semi-autonomy had been eroding for years at the time of Xiao’s arrest, but the erosion had been felt largely at the street-level, among pro-democracy agitators and outspoken booksellers. For the city’s shielded rich, the dramatic seizure of one of their own sounded a shrill wake-up call.

Soon came other alarms: the 2020 National Security Law; the freezing of bank accounts tied to political undesirables; the defanging of the press; Covid Zero. Since 1949, Hong Kong had been considered a free and glitzy refuge from the Chinese Communist Party. Suddenly, it wasn’t.

“For my clients, the wildfire [of CCP intrusion] was getting too close,” says David Lesperance, an immigration lawyer focused on wealthy Chinese. “They were smelling smoke.”

Now, seeking refuge from Hong Kong, many have turned to another Asian, postcolonial port city: Singapore. In recent years, wealthy Chinese from both Hong Kong and the mainland have been flocking to Singapore in large numbers. The Singaporean government does not release country-based immigration statistics. But one metric that’s been used to measure the migration is the number of new family offices, an investment vehicle popular with wealthy Chinese.

The wealthy class of Chinese has seen the writing on the wall. Xi Jinping’s China is not a safe place for them or their money.

Clyde Prestowitz, economist and author

Between January 2020 and April 2022, registered family offices (FOs), which require a minimum fund of $7.3 million and a net worth of $400 million, rose from 400 to 843; Chinese FO founders accounted for up to 44 percent. Recent founders include the Hong Kong magnate Li Ka Shing, one of the wealthiest businessmen in the world, and Zhang Yong, a Chinese hotpot billionaire.

“Founders of family offices pick ‘Singapore Inc’ because everything works,” says Kia Meng Loh, a senior partner with the Singaporean law firm Dentons Rodyk & Davidson. “Entrepreneurs find it easy to register a company in a matter of hours. The government dishes out incentives and tax cuts for investors.”

Indeed, in an era of increasing capital controls and “common prosperity,” rich Chinese emigrants view the orderly island foremost as a haven for their private wealth. But they also see Singapore as a stable bastion of competent governance, relative freedom and pro-business bonafides with tension-free ties to southeast Asia and the west. The new catchphrase among Chinese netizens is “runxue,” or “run philosophy,” meaning to flee China in search of a better life.

Before the Xi Jinping era, Hong Kong fit this bill.

“[Wealthy Chinese] used to set up family offices in Hong Kong,” says Ryan Lin, director of Singapore-based Bayfront Law. “But with what’s happened between Hong Kong and China, more are coming directly to Singapore and bypassing Hong Kong.”

“The wealthy class of Chinese has seen the writing on the wall,” adds Clyde Prestowitz, an economist and author of The World Turned Upside Down: America, China and the Struggle for Global Leadership. “Xi Jinping’s China is not a safe place for them or their money.”

For the Chinese upper-class, Singapore’s brand is increasingly attractive. Under Singapore’s global investor program, people who invest at least $1.8 million in a fund, family office or company can apply for permanent residency. It makes Singapore competitive with other “golden visa” programs in the Caribbean, Europe and America. In an authoritative ranking of the world’s fastest growing ultra high-net-worth populations (people with $30 million or more), Singapore moved from eighth place in 2019 to third in 2022. Of the country’s ten richest residents, five are Chinese-born permanent residents.

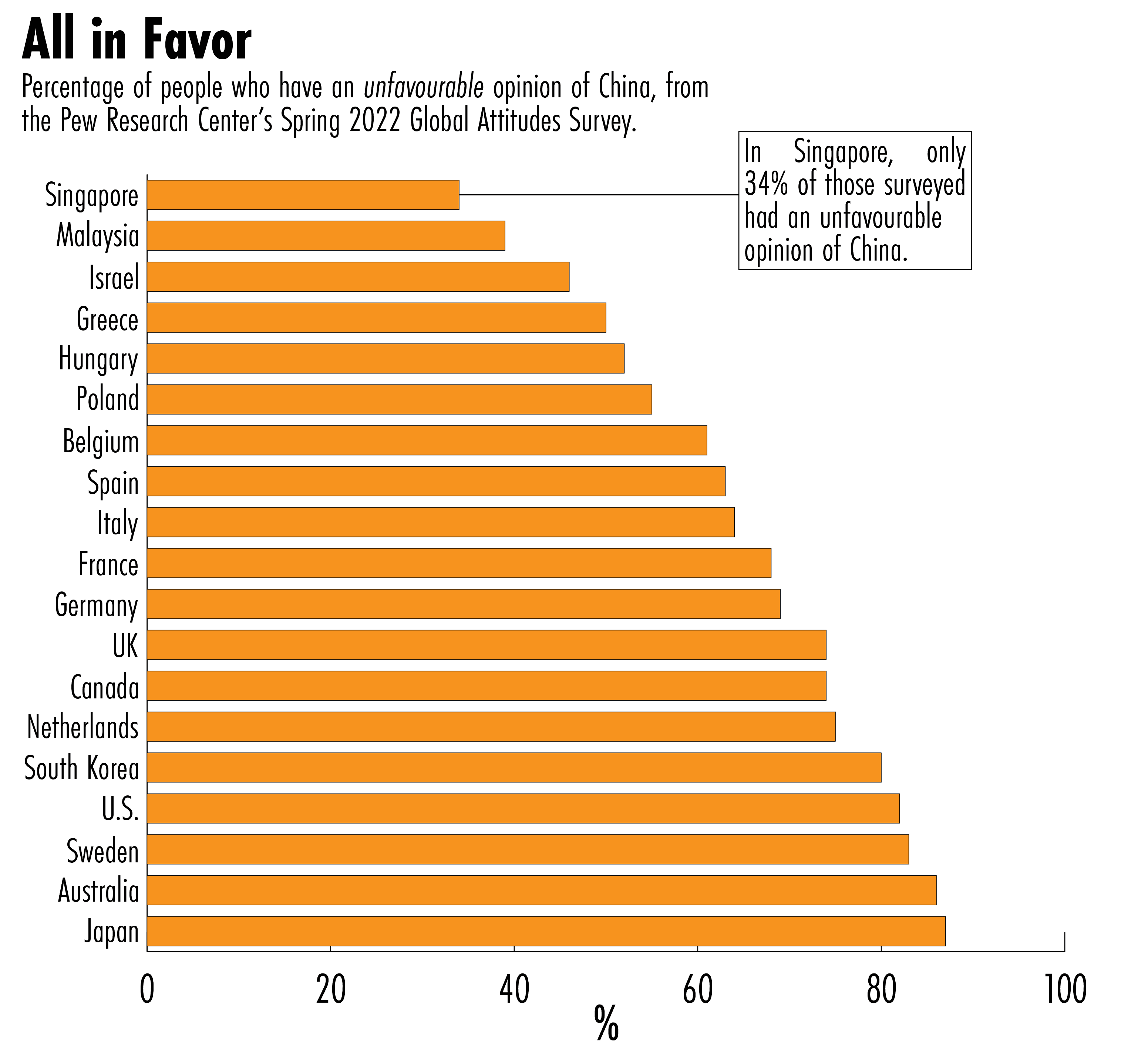

It also helps that nearly three-quarters of Singapore’s 5.6 million citizens are ethnically Chinese and that 67 percent of Singaporeans view China favorably, according to a recent Pew survey.

“It just ticks all the boxes,” says Dominic Volker, an executive with Henley & Partners, a high-end immigration consultancy, which saw inquiries surge 600 percent last month following the end of Covid-zero in China. “We spend most of our time with Singaporean wealth management companies and private banks and they are all having record years. A lot of that flows from China and Hong Kong, with all the geopolitical tensions there.”

Companies are shifting focus to Singapore too. In 2022, around 500 firms from Hong Kong and the mainland expanded their operations in Singapore. Many hail from the much-embattled Chinese tech sector — like online clothing giant Shein, the electric vehicle maker Nio, and TikTok parent company ByteDance — as well as Chinese crypto firms and even multinationals, like the VF Corporation, which owns The North Face, Timberland and other brands.

A video of NIO’s listing on the Singapore Exchange.

For the Singaporean government, both the influx of business interest and the migration play into long standing plans to attract top-notch human capital and foster a start-up culture.

“The government likes that it gets to build up Singapore’s wealth industry, but it also wants to attract entrepreneurs to build up entrepreneurship,” says Grace Tang, executive director at Phillip Private Equity which manages one of two global investor program funds in Singapore.

Hong Kong, meanwhile, has been bleeding out. In 2022 alone, over 130,000 residents emigrated — to Singapore but also places like Canada, England and Australia. There have been three straight years of population decline, according to government statistics. Nearly half of all European companies in Hong Kong have plans to relocate, according to a recent study by the European Chamber of Commerce. Firms that remain complain of a crippling brain-drain and a struggle to recruit workers.

So far, the city has only modestly attempted to blunt the exodus. Recently, it made it easier to acquire permanent residency cards, and the Hong Kong government now offers work visas to mainlanders who have graduated from prestigious institutions without the need for an employer’s endorsement.

Taken together, the changes in both cities have led to a general sense that Singapore is the new Hong Kong. Last year, as Hong Kong’s GDP shrunk by 3.2 percent, Singapore’s expanded by 3.8 percent. And in a 2022 comparative study between global financial hubs, Singapore replaced Hong Kong as the third top financial center in the world, behind New York and London.

“Hong Kong is losing its status as Asia’s most prime financial center and Singapore is on the rise,” says Xin Sun, an expert in Chinese business at King’s College London. “In the future, Chinese companies who want to go global will be more likely to register their headquarters in Singapore than in Hong Kong.”

But not everyone is so bearish on the Fragrant Harbour, as Hong Kong is called. As Covid Zero ends and the city reopens, some are predicting greener pastures. In terms of sheer wealth, Singapore pales in comparison to Hong Kong since Hong Kong boasts something Singapore never will: close proximity to one billion Chinese wallets. Reflecting this easy access to Chinese capital, the value of companies on the Hong Kong Stock Exchange dwarfs Singapore’s: currently, the market value of companies listed in Hong Kong is close to $4 trillion compared with less than $500 billion for the Singapore Exchange (SGX).

For companies in search of equity, this is a strong advantage.

“Network effects just make it very hard to compete because of the size and depth of capital markets in Hong Kong,” says Low. “The Singapore stock exchange has not been competitive for a very long time.”

The gap may widen still. According to a recent Bloomberg survey of 12 economists, Hong Kong’s growth rate this year is expected to exceed Singapore’s, thanks largely to its close proximity to eager mainland capital. In 2023, the city’s IPOs by deal value could triple to about $40 billion (most Hong Kong stock exchange listings are mainland companies). The Chinese economy, too — although hobbled by debt, a housing crisis and low consumer confidence — is still set to expand 5.2 percent this year, according to the International Monetary Fund’s latest forecasts.

Hong Kong’s economy still works quite differently to mainland China’s and still has better legal protections for business matters. It’s just that who Hong Kong is for is changing.

Neil Thomas, a China analyst for Eurasia Group

Moreover, Singapore has a dull reputation. “It is the conventional wisdom that Singapore is boring,” notes Rui Ma, a consultant focused on the Chinese tech space. Among mainland Chinese, one popular nickname is “Singaboring.”

Though less free, Hong Kong is decidedly not boring. Plus, finance workers there make on average 55 percent more in total compensation than those in Singapore, according to eFinanceCareers, a recruiting research group. And its effective tax rates are lower.

Despite its political problems, some argue, the mountainous metropolis remains robustly competitive.

“Hong Kong’s economy still works quite differently to mainland China’s and still has better legal protections for business matters,” says Neil Thomas, a China analyst for Eurasia Group. “It’s just that who Hong Kong is for is changing. It’s not for international business anymore, it’s for Chinese business.”

Even Singaporean prime minister Lee Hsien Loong insists the two cities aren’t in competition with each other. When asked last spring by a reporter if his country benefited from Hong Kong’s duress, he replied, “[I]t is not to our advantage to have Hong Kong languish. They thrive, we thrive. We will make a living, and so will they. It is not Hertz or Avis.”

The leader’s witty reply was a characteristic display of Singaporean tact. But it also reflected an important truth: Singapore needs Hong Kong to prosper. With the sudden windfall of Chinese wealth and talent, Singapore is facing unprecedented challenges of its own, including rapidly widening economic inequality and exceedingly delicate foreign policy choices. The relationship between the two financial hubs is far more complicated and consequential than rental cars.

NATION BUILDING

Pax Britannica, that “imperial century” when Britain ruled the seas, birthed Asia’s two wealthiest island cities. After the Qing dynasty ceded Hong Kong to the Crown in 1842, British colonialists remade the sleepy island into a modern and mighty financial titan. Throughout Hong Kong’s rise, mainland China withered in warlordism, civil war, Japanese brutalization and communist misrule.

Singapore, too, prospered under the Union Jack, transforming from a malarial hideaway into one of Asia’s busiest trading ports. After the British finally departed in 1968, their cultural and legal remnants set Singapore on a fortuitous path.

But it took the steely shepherding of Lee Kuan Yew (1923–2015), Singapore’s founding prime minister, to take full advantage of his infant country’s few advantages. Despite everything standing against Singapore, he remarked in 1979, “we have to fight our way out of [pessimism]. You have to show a credible, plausible way that we can keep our head above water.”

Lee’s “little red dot” proved a hardy swimmer. From 1965 to 1990, Singapore GDP per capita expanded from $500 to $13,000, surpassing Portugal, Israel and South Korea; it has since reached $72,000. “We are pragmatists,” Lee once remarked about Singapore’s development model. “We don’t stick to any ideology.”

Lee saw Singapore balanced on a knife-edge, perpetually at risk of economic implosion or societal unrest. “Precisely because it had no past as a nation, there was no assurance it would have a future; its margin for error thus remained perpetually close to zero,” writes Henry Kissinger in Leadership: Six Studies in World Strategy, which profiles Lee.

Despite lacking land, natural resources or even reliable drinking water, Singapore prospered to a remarkable extent. Capitalizing on its strategic position at the southern end of the Strait of Malacca, a major global sea lane, it has become the world’s second largest port. It also thrived by aggressively courting multinationals, nurturing a dynamic manufacturing industry.

By 1972, half of the Singaporean labor force was employed by multinationals, which accounted for 70 percent of its industrial production. A year later, Singapore became the third-largest oil refiner in the world.

All the while, the Singaporean government invested heavily in education — for several years, up to one-third of the national budget went towards it — rapidly moving its workforce up the value chain. “Emphasis on the quality of life turned into a defining aspect of Singapore’s style,” Kissinger wrote.

Today, Singapore tops virtually every regional quality of life index, and its GDP of $397 billion is larger than neighboring Malaysia’s, a resource-rich country nearly 500 times its size. In a region plagued by government and corporate corruption, Transparency International rates it as the fourth-least-corrupt country on earth. It is the richest city on the equator by far.

But despite succeeding against all the odds, the recent surge of Chinese money has been somewhat destabilizing for Singapore. From real estate to automobiles, everyday prices are rising, as are already-high inequality metrics, due in part to the migration. Last year Singapore was ranked the priciest city in the world, alongside New York, by the Economist Intelligence Unit. In a recent speech, the Singaporean prime minister acknowledged that the swelling costs of living were at “the top of everyone’s minds.”

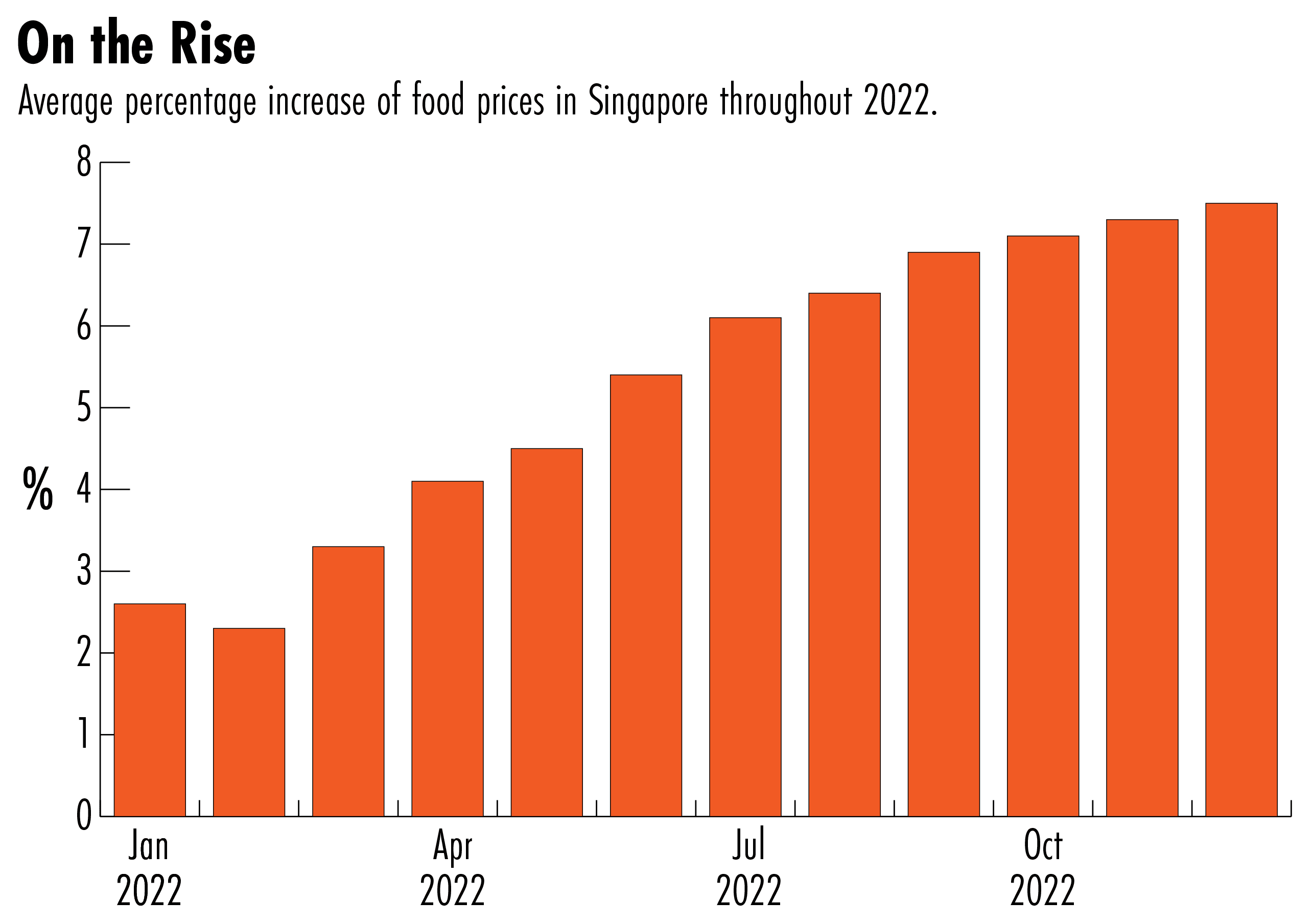

The numbers paint a picture of shrinking opportunity for the middle-class. Between 2021 and 2022, the average cost of rent shot up 36 percent to $3,500 a month for a 1,000-square-foot condo apartment, according to 99.co, a property portal. Home prices have gone up 8 percent. Last year, license costs to drive a car rose by almost 40 percent, while food costs are rising from inflation; hawker stall prices, Singapore’s average joe mainstay, have gone up nearly 8 percent. Parents are finding private schools more competitive than ever. Even golfing is pricier: the cost of a membership to the exclusive Sentosa Golf Club more than doubled since 2019.

Moreover, in a multiethnic country with a history of racial strife, there are whispered concerns of Chinese enclaves forming and old ethnic resentment bubbling up. Kher Sheng Lee, co-head of the Asia Pacific Alternative Investment Management Association in Singapore, says a popular shirt in Singapore that reads, “I’m Singaporean, not Chinese.”

“Because they’re coming in such large numbers, they tend to congregate amongst themselves,” says Kelvin F.K. Low, a law professor at National University of Singapore. “They use WeChat rather than WhatsApp. They’re more comfortable speaking Mandarin [than English, Singapore’s de facto main language].”

“It’s not just high-profile Chinese industrialists and property developers moving to Singapore and buying fancy houses in Sentosa,” adds Drew Thompson, a visiting senior research fellow at the National University of Singapore and former U.S. defense official. “There’s a lot of angst and consternation about immigration that this really touches on.”

Singapore has managed this balancing act fairly well. The Singaporeans very much hue to the dictum that nations don’t have friends, only interests.

Sebastian Strangio, author

Singapore has taken small steps to soften the Chinese surge. Recently, the conditions required to open a family office were tightened. And there has been an additional duty placed on foreign real estate buyers, most of whom are mainland Chinese — though it hasn’t had much effect.

“For a lot of the wealthy Chinese, particularly after the Shanghai lockdowns and the collapse of the Chinese property market, they don’t mind paying the additional buyer’s stamp duty,” says Low, who specializes in real estate law. “They’re just finding ways of preserving wealth.”

Perhaps most consequentially, the Chinese migration could roil Singapore’s delicate foreign policy. The Chinese-majority country has long taken pains to distance itself from accusations of undue PRC influence while still engaging heavily with China. As Gideon Rachman, the Financial Times columnist, has said, Singapore is the only nation in the world “to have a special relationship both with the People’s Republic of China and the United States.”

China is Singapore’s largest trade partner, and Singapore’s manufacturing industry has benefited enormously from Chinese growth. Moreover many Singaporeans have lived or worked in China. But as a bulwark against Chinese power, Singapore has quietly but firmly supported a strong American presence in the region, regularly hosting U.S. Navy ships and sending its own troops stateside for training.

“Singapore has managed this balancing act fairly well,” says Sebastian Strangio, author of In The Dragon’s Shadow: Southeast Asia in the Chinese Century. “The Singaporeans very much hue to the dictum that nations don’t have friends, only interests.”

With U.S.-China relations deteriorating, however, Singapore’s wiggle room between Beijing and Washington could be further restricted. As Singapore continues to lure away wealth and talent from China and Hong Kong, for instance, it may attract unwanted attention from its powerful and often vindictive northern neighbor.

“The Chinese government in the long run would certainly hope to exert more political influence on Singapore,” says Sun, of King’s College. “Down the road, things could become a bit trickier.” For example, he adds, Beijing might seek more cooperation from Singapore on the extradition of criminals and fugitives.

If U.S.-China relations were to dramatically rupture — in the case of an invasion of Taiwan, say — Singapore’s surge of wealth and business from China may well become a torrent.

“If worse comes to worse and war breaks out across the straits, then you’re going to see sanctions fly,” says a longtime senior business executive in Hong Kong who requested anonymity because they are not permitted to speak to the press. “All of that would be really important news for Singapore. You’d start seeing a lot of private money in Hong Kong leaping to Singapore.”

Still, this wouldn’t mark a win for the Lion City. In the case of war, the region as a whole “would suffer a huge geopolitically-induced recession,” says Thomas, of Eurasia Group.

If worse comes to worse and war breaks out across the straits, then you’re going to see sanctions fly. All of that would be really important news for Singapore.

an anonymous business executive in Hong Kong

Lee, the Singaporean assets manager, calls the prospect of war “the elephant in the room” of the ongoing Chinese exodus. “If there’s a war across the strait then all bets are off,” he says.

Beyond that extreme scenario, most analysts expect both Hong Kong and Singapore to continue serving as vital business hubs. But both cities have undoubtedly changed. Indeed, it’s not Hertz and Avis. It’s looking like Hertz and Car, Inc. — one of China’s largest rental car companies.

“The days of Hong Kong as a world finance center are gone,” says Joseph Fan, a finance professor at the University of Queensland in Australia, and who spent decades in Hong Kong. “The main investors and clients will be replaced by Chinese companies, especially state-owned enterprises. It’s already happening.”

Brent Crane is a journalist based in San Diego. His work has been featured in The New Yorker, The New York Times, The Economist and elsewhere. @bcamcrane

{kind=link}