Earlier this month, China’s economic tsar, Liu He, took the stage at the World Economic Forum in Davos like a salesman delivering a carefully practiced pitch. With thinning gray hair and reading glasses, the 71-year-old Harvard graduate methodically laid out for the audience how to better understand the Chinese economy.

“Entrepreneurship is a key factor for wealth creation of a society,” Liu said. “Therefore, entrepreneurs, both Chinese and foreign, will play an important role as the engine driving China’s historical pursuit of common prosperity. If wealth doesn’t grow, common prosperity will become a river without source or a tree without roots.”

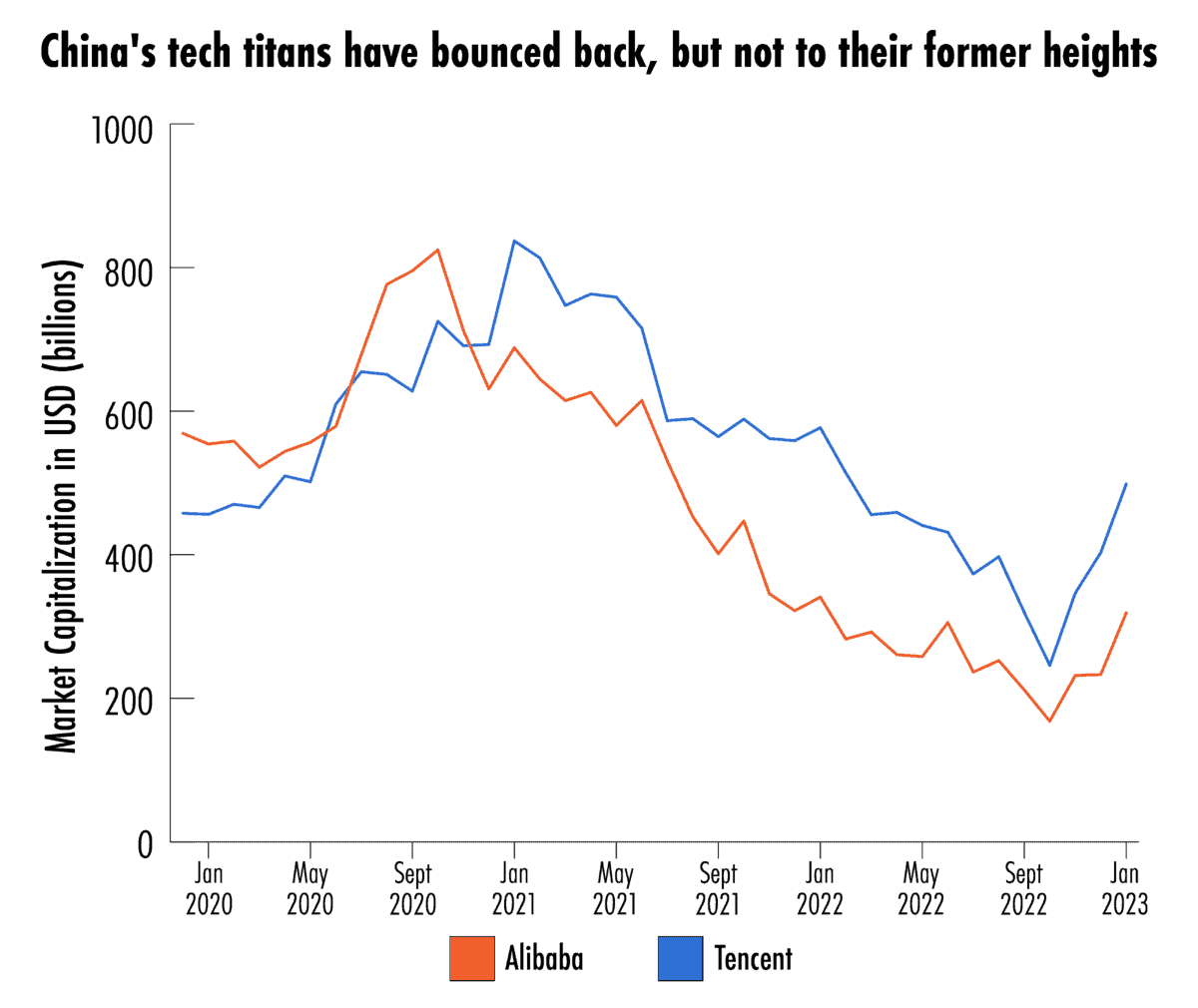

The message — that China is open for business — likely caused some head scratching in the Davos audience. As Xi Jinping’s right-hand-man on the economy, Liu himself oversaw the “tech crackdown” of the last three years, which decimated the value of some of China’s biggest internet companies, including Alibaba and Tencent. In the wake of Beijing’s intervention, several of China’s most prominent entrepreneurs have quietly stepped down from their founder-CEO roles, or even emigrated to live in semi-exile.

Alibaba founder Jack Ma, for example, is rumored to be living in Tokyo while learning about sustainable farming practices from around the world. Zhang Yiming, the founder of Tik-Tok parent company Bytedance, is using Singapore as a base since resigning from his leadership roles, according to The Information. Colin Huang, the founder of agritech giant Pinduoduo, stepped down from the CEO role in 2020, and relinquished his chairmanship in 2021. And in 2022, Richard Liu resigned as CEO of JD.com, although he remains chairman.

This entrepreneurial exodus, observers say, is at odds with Liu’s pitch and is reflective of a larger problem in China’s economy: the fear factor.

Inflamed by the regulatory crackdowns, China’s strict zero-Covid measures, and the perception that Xi Jinping is seeking greater control over the economy, the fear factor is evident among both global investors — who pulled a net $9 billion out of China’s equity markets between January and October 2022 — and among Chinese entrepreneurs in younger, more dynamic digital industries.

“Entrepreneurs have lost faith in the government’s ability to govern in a balanced manner that could drive innovation and risk-taking,” says James Zimmerman, a partner in the Beijing office of law firm Perkins Coie LLP, where he helps clients navigate China’s regulatory regime and complex business environment. “Why take chances? Why be creative? Business now takes the view that politics trumps entrepreneurship.”

David Lesperance, managing director of tax and immigration advisory firm Lesperance and Associates in Ontario, says he advises a lot of Chinese entrepreneurs and has noticed the change.

“The world that today’s founders find themselves in is fundamentally different than when people like Jack Ma or Pony Ma began their companies. Requirements to give the CCP board seats and golden shares, plus the ever present threat of another tech crackdown and the hesitancy of foreign investors, make China an unattractive place to start the next Alibaba, Ant or Tencent,” he says. “Today’s founders are looking internationally to establish their companies.”

Liu’s measured Davos address, experts say, was clearly part of a larger effort to stop this entrepreneurial brain drain. Recently, Beijing has reversed its stance on “zero Covid,” signaled an end to fintech crackdowns, allowed the ride-share company Didi to sign up new users for the first time since 2021 and loosened restrictions on property developers.

A CGTN video highlighting remarks made by Xi duirng a symposium attended by entrepreneurs from China and abroad, July 21, 2020.

This hot-and-cold relationship between the Chinese Communist Party (CCP) and China’s private sector is nothing new, of course. But many experts say the current environment represents a step change from previous swings, and that Beijing’s efforts to woo back China’s entrepreneurial spirit might be too little, too late.

“For many years, China managed a balance between control and innovation,” says Christopher Marquis, a China expert at Cambridge University’s Judge Business School, and the author, with Kunyuan Qiao, of Mao and Markets: The Communist Roots of Chinese Enterprise. “But under Xi Jinping, the pendulum has swung in the ideology and Party control direction much further than it has in the past, which really undermines the economy and entrepreneurship.”

The timing of this particular swing is problematic: China is facing economic headwinds and an increasingly hostile, protectionist geopolitical environment. It needs the trust of entrepreneurs who can spur growth and innovation, especially in the tech industry — otherwise, as Liu noted, “common prosperity will become a river without source.”

“For a lot of the Party’s objectives, it ultimately still needs a tech industry,” says Victor Shih, an expert on Chinese elite politics at the University of California San Diego. “If China is going to have any kind of global influence in technology, especially in the software side, it will need these internet platforms.”

The CCP is undoubtedly sending positive signals to the cowering tech sector. Senior local officials have met with tech CEOs in recent weeks, showing that, for local Party leaders, “cooperating with these companies is not the potential liability it was seen as six months ago,” says Tom Nunlist, a senior analyst at Trivium, a China-focused policy research firm. Plus, January announcements from the People’s Bank of China and the State Administration for Market Regulation painted a brighter picture of the year ahead for China’s tech platforms. Those signals, combined with China’s opening up, have contributed to a rally in Chinese tech stocks over the last few weeks.

Beijing is projecting the message that, with the ship now righted, China’s entrepreneurs and global investors no longer have anything to fear: China wants the private sector to thrive, so long as it is working towards Party ends. This, after all, has always been the deal between the CCP and China’s so-called capitalist class.

But many experts say it’s naive for Beijing to think the recent bumps in the relationship will smooth out quickly — especially since China’s wealthy have been eyeing the exit and planning their exodus for years.

… under Xi Jinping, the pendulum has swung in the ideology and Party control direction much further than it has in the past, which really undermines the economy and entrepreneurship.

Christopher Marquis, from Cambridge University’s Judge Business School

“Entrepreneurs are moving their bodies and families abroad now,” says Meg Rithmire, a China expert at Harvard Business School. “But the huge movement of assets happened before that, and it was a warning sign to the CCP.”

IT TAKES TWO TO TANGO

Liu’s about-face at Davos harkened back to another prominent example of CCP cognitive acrobatics: Jiang Zemin’s 2001 address to the nation on the 80th anniversary of the CCP’s founding — a speech that elucidated his “Three Represents” theory.

Less than 12 years earlier, in his first year as China’s General Secretary, Jiang had overseen the ban on private businessmen obtaining Party membership in the wake of the Tiananmen Square protests. But on July 1, 2001, Jiang took to the podium in Beijing’s Great Hall of the People to declare that entrepreneurs were “working to build socialism with Chinese characteristics.”

“Under the guidance of the Party’s line, principles and policies, most of these people in the new social strata have contributed to the development of the productive forces and other undertakings in a socialist society through honest labor and work or lawful business operation,” Jiang told the audience in his trademark oversized glasses.

It was a stunning admission, but one that fit China’s pattern of “accommodation and reprisal,” as Rithmire puts it.

From the anti-capitalist “Five-Anti Campaign” in the 1950s, to the Cultural Revolution and its purging of “capitalist roaders,” to the renewed suspicion of private entrepreneurs in the wake of the 1989 Tiananmen Square protests, the state has always been quick to suppress — often violently — an increasingly powerful capitalist class. At the same time, however, entrepreneurs have been co-opted by the Party, when required. Prominent businessmen — like the original “Red Capitalist,” Rong Yiren — grew accustomed to being persecuted and then parachuted into important economic roles in Beijing.

“It was like a dance between, ‘We are a communist country,’ but also, ‘We need your skills, creativity, innovative capacity, managerial capacity … we need someone who knows how to run a factory,’” says Harvard’s Rithmire.

To many, the 1990s seemed to fundamentally change China’s relationship with private business. The fruits of economic liberalization under Deng Xiaoping’s reforms had resulted in booming private business activity and a rapidly improving standard of living for the Chinese population. Entrepreneurs were an undeniable force in China’s future trajectory, and were already being informally — and at that time illegally — co-opted into the Party by regional officials.

The years following Jiang’s 2001 speech seemed to cement this new status and a more permissive approach to capitalism in China. That year, China joined the World Trade Organization (WTO) and the opportunity arose for the burgeoning private sector to meet global demand for cheaply produced manufactured goods.

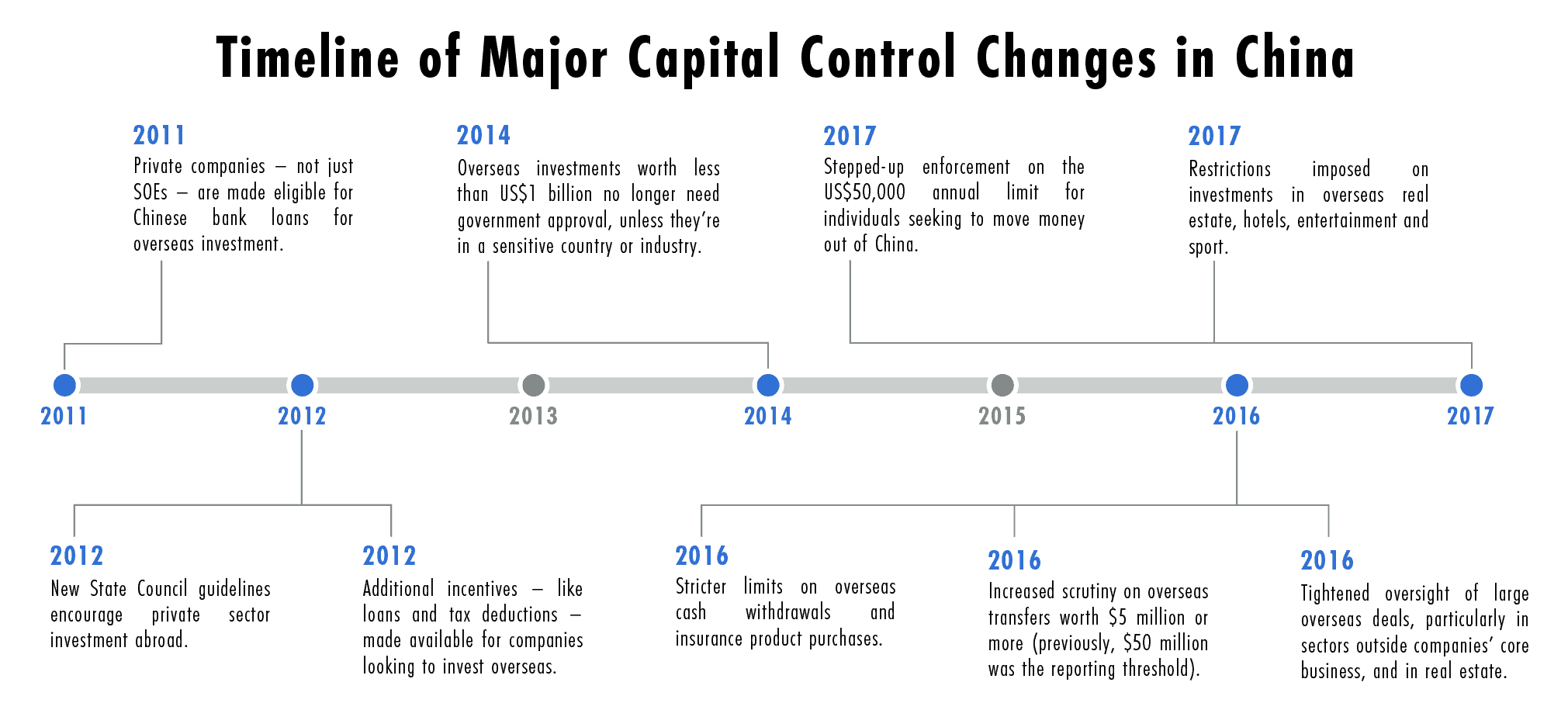

Beijing also instituted its novel “Going Out” policy in 1999, which encouraged companies to invest in strategic sectors abroad in order to secure inputs like natural resources for economic development at home.

In retrospect, “Going Out” marked a turning point in China’s complicated relationship with its entrepreneurs. Initially, it was seen as a way to make use of China’s ballooning foreign currency reserves (thanks to its large trade surplus) and was dominated by state-owned enterprises (SOEs).

But with the door now open, it wasn’t long before the private sector walked out as well — which it did swiftly once the 2008 financial crisis hit and there were deals to be found. For the first time in the CCP’s history, capitalists were encouraged to buy assets abroad, therefore moving their money outside the country.

Prior to 2015, there was a period — even during Xi’s rule — when China had such large foreign exchange reserves that it encouraged domestic investors to invest overseas.

Victor Shih, from the University of California San Diego

China’s currency, the renminbi (RMB), is tightly controlled by the state through its foreign exchange reserves. Historically, Beijing was concerned with suppressing the currency’s value to maintain China’s export competitiveness. In the early 2010s, outward flows of RMB — that is, RMB converted into U.S. dollars or other currencies — weren’t of much concern, insofar as they helped with the mission of suppressing the RMB’s value.

“Prior to 2015, there was a period — even during Xi’s rule — when China had such large foreign exchange reserves that it encouraged domestic investors to invest overseas,” says Shih, from UCSD. “It was very easy to take billions out of China as long as you had some kind of excuse.”

The nature of Chinese overseas investments during this period, however, show that the private sector was not always following the intent of Going Out, or even the infrastructure-centric Belt and Road Initiative, which was launched in 2013. A significant proportion of post-2010 overseas investment flowed into North America and Europe. And some of the most high profile investments of the period were not in strategic sectors at all, but in real estate, hospitality and entertainment.

For example, Fosun, a now-embattled conglomerate, paid $725 million for One Chase Manhattan Plaza in 2013. Insurance giant Anbang — now overtaken by the Chinese government — snapped up the iconic Waldorf Astoria hotel in New York for $1.95 billion in 2014.

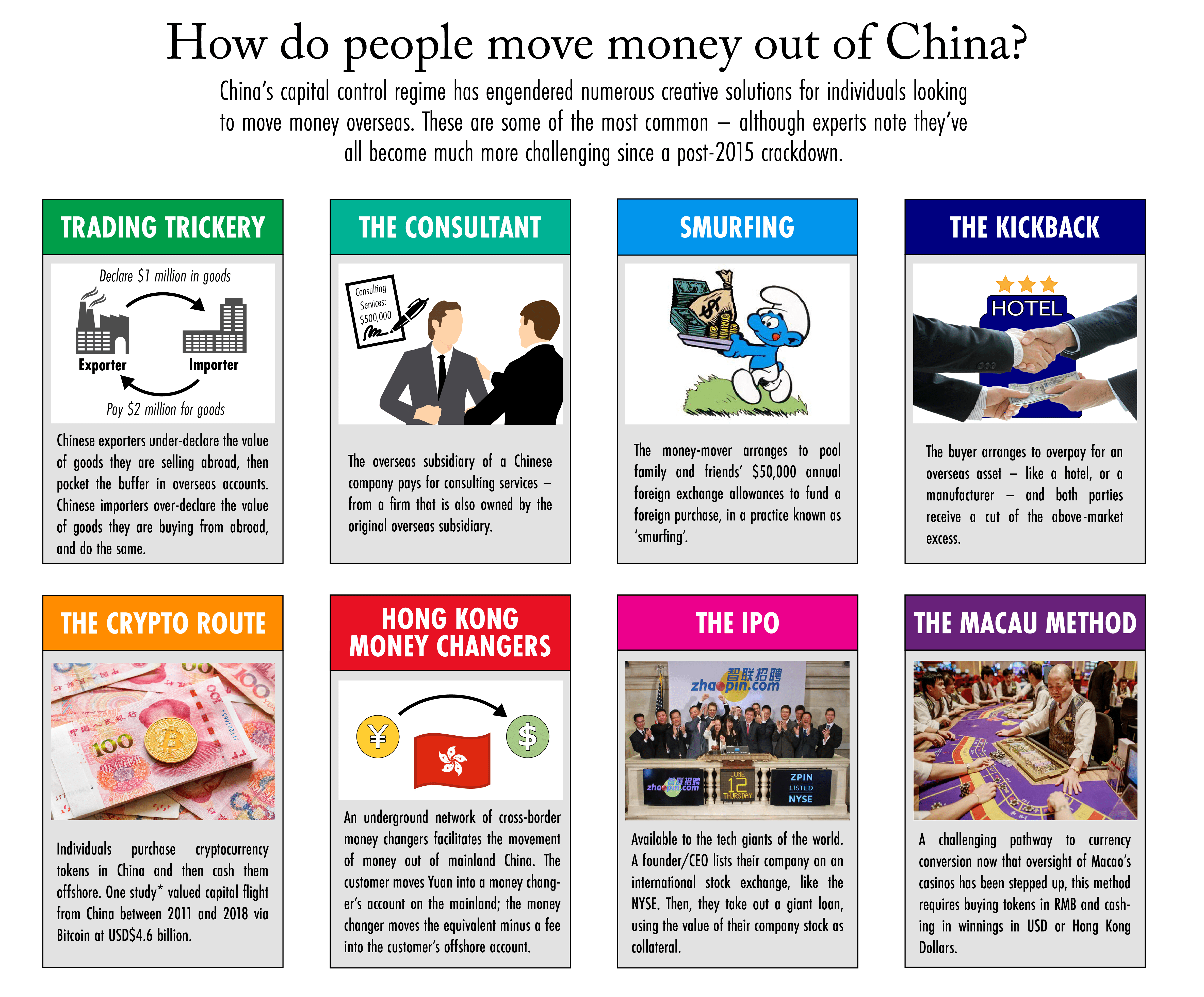

Moreover, in most years since 2009, every dollar that left China as outbound foreign direct investment has been approximately matched by a dollar in unexplained outflows. Experts say this trend of unexplained RMB leaving China — captured in the ‘errors and omissions’ line of China’s official Balance of Payments statistics — was likely driven, in part, by Chinese individuals finding unofficial and even illegal ways to move money out of China.

Rithmire, from Harvard Business School, says that while it’s hard to disentangle legitimate, commercially motivated investments from capital flight, the nature of the foreign assets being purchased and the political environment in China at the time — Xi Jinping launched his anti-corruption campaign in 2012 — suggests China’s wealthy were looking for ways to get their money out of the country.

“Ironically, the anti-corruption campaign seems to have accelerated this kind of behavior,” Rithmire says. “You almost get incentives to even more quickly borrow money while you have access to it, and invest it in Europe while you still can.”

In other words, China’s entrepreneurs, familiar with the CCP’s erratic dance, saw an opportunity to switch partners.

By 2015, China’s total outward foreign direct investment stock hit $1 trillion for the first time, according to Chinese official statistics, up from around $56 billion in 2008, with about half of that coming from the private sector.

Click here to read another cover story by Isabella Borshoff on Germany’s relationship with China.

For those trying to move money out of China, however, the music stopped shortly afterwards. Faced with a wobbling stock market and slowing economic growth, Beijing tried to contain the fallout with a managed devaluation of the renminbi — making Chinese exports relatively cheaper for buyers. But this move triggered fears of further currency depreciation, and thus capital flight, as holders of renminbi rushed to get rid of it.

To stave off a disastrous hollowing out of the country’s foreign exchange reserves, Beijing put in place a host of policies to limit capital outflows.

Although experts note that the focus of these regulations was managing the valuation of the renminbi, the byproduct was that moving money out of China suddenly became much harder for wealthy Chinese. It was difficult timing for China’s capitalist class: the structurally at-risk Chinese economy was slowing down, Xi’s government was clamping down on overleveraged conglomerates, a trade war with the U.S. was brewing, and Beijing would soon crack down on pro-democracy protests in Hong Kong.

Henley and Partners, a London-based investment migration consultancy, told The Wire that they first noticed a significant uptick in migration of Chinese “high net worth individuals” around 2018. The message to the capitalist class was clear: China is a risky place to keep one’s millions.

A NEW BREED

The Covid-19 pandemic stalled this exodus, but initial signs point to its enduring appeal: in the three weeks since December 28, when China first signaled the easing of travel restrictions, Henley and Partners says that inquiries by wealthy individuals seeking to emigrate from China and Hong Kong shot up 600 percent compared to the prior three weeks.

Analysts are quick to note that China’s brain and capital drain doesn’t spell an end for private business in China. China, after all, remains a massive market where big bets can still generate big returns.

But they do say it will take a while for entrepreneurs to warm back up. And when they do, it might take a different breed to succeed.

“Private entrepreneurs have got the message now: They need to be paying more attention to government relations,” says Neil Thomas, an expert in Chinese elite politics at Eurasia Group, the political risk advisory and consulting firm. “Because the Party will be scrutinizing your every move, and if you make political mistakes, it’s going to put you in a position of incredible risk.”

In such a draconian environment, everyone is okay until they’re not okay.

Zeren Li, from Yale University

Those willing to accept this risk will also have to be okay with the fact that the ceiling for their growth has been lowered and the pace of their innovations has been slowed. The main impetus for the tech crackdown, many note, was that the industry moved too fast in areas the Party has historically maintained monopoly control over — like finance and media.

To prevent that from happening again, Beijing has empowered various regulators.

“The whole bureaucratic structure has transformed,” says Xin Sun, an expert in Chinese business at Kings College London. “In the past decade, administrative and regulatory power has been reshuffled from local governments to the central government. Central departments and agencies will have a strong incentive to use their newly gained power, such as by issuing new policies and regulations and exercising them with discretion to advance their own bureaucratic interests, which will worsen the business environment.”

In other words, the added red tape will likely slow private businesses down. But it could also discourage them altogether. At best, says Martin Chorzempa, a senior fellow at the Peterson Institute for International Economics, there might eventually be “a shift towards normalized supervision — an environment where the rules of the game are clear and consistent over a long enough period that [entrepreneurs] feel comfortable launching a product or business.” But, he notes, “there’s no way of going back to the freewheeling era.”

The question, then, is whether the CCP can finally figure out how to strike that balance — incentivizing entrepreneurship while laying clear boundaries — without resorting to the wild swings of its past. Zeren Li, an expert in Chinese government-business relations at Yale University, isn’t holding his breath.

“There’s a joke I heard that the government is making policy like Chinese pancakes: this year we put the policy on this side, and flip it and do the opposite next year,” Li says. “It really hurts confidence and trust in the system. In such a draconian environment, everyone is okay until they’re not okay.”

Isabella Borshoff is a staff writer based in London. Previously, she worked as a climate policy adviser in Australia’s federal public service. She earned her Master’s in Public Policy at Harvard’s Kennedy School. Her writing has been published in POLITICO Europe. @iborshoff

{kind=link}