Last year, the creditors of the world’s most-indebted real estate developer, Evergrande, gathered for a signing ceremony in Beijing where they agreed not to force the company to pay them their debt. A photo from the event shows Zhang Jindong, a Chinese tycoon and then-chairman of Nanjing-based retail giant Suning, standing next to his longtime friend, Evergrande’s chairman Xu Jiayin, and clapping unenthusiastically.

That day, Zhang helped his friend avoid a near-term cash crunch by waiving his right to collect a nearly $3 billion payment Evergrande owed to Suning. The timing of the decision couldn’t be worse — at the end of the third quarter last year Suning’s own debt was more than $6.6 billion. Suning Holding Group and its operating company, Suning.com, have local and offshore bonds worth $4.3 billion maturing soon, with the largest payment approaching in December.

Personal favors to Xu Jiayin notwithstanding, Suning seems to be making moves to get ahead of its debt. This spring, it was reportedly trying to find a buyer for its beleaguered soccer team, Football Club Internazionale Milano — often referred to as Inter Milan, or simply Inter — which is worth an estimated $1 billion. Then in July, Suning secured a bailout, selling a 16.96 percent stake of Suning Group and its other holding company, Suning Appliance Group, for $1.36 billion to a state-backed consortium that included the Nanjing municipal government, Alibaba Group Holding, Xiaomi and others. And in October, it was reported the company is mulling over whether or not to sell its controlling stake in Carrefour SA’s China business for a potential $800 million cash infusion.

But while these efforts will certainly help to chip away at Suning’s debt, some say the threat of Suning’s default has revealed larger, more systemic problems about the way private Chinese companies borrow, especially from foreign creditors.

“Chinese companies want offshore money. But they burn money,” says Carl Walter, visiting scholar at Stanford University and a co-author of Red Capitalism: The Fragile Financial Foundations of China’s Extraordinary Rise. “And on private transactions, when things go wrong, they can easily break their contracts. So, unless the foreign creditor has a powerful connection in Beijing, they have to be very careful.”

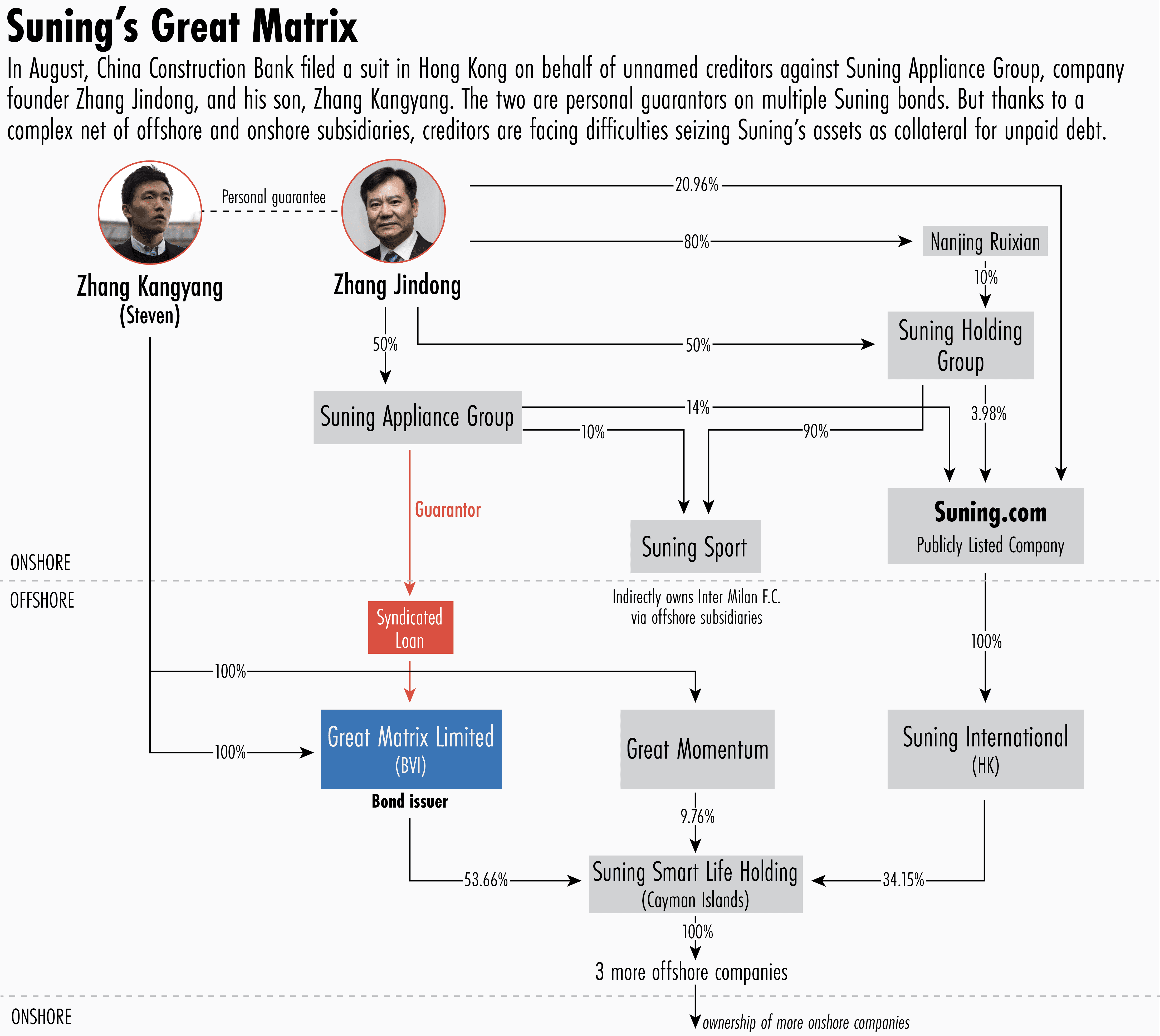

That may be starting to change, however. With such high-profile defaults rocking the Chinese corporate bond market, the legal rights and repayment priority of offshore creditors are being put before Chinese courts. On August 2nd, a state-owned enterprise, China Construction Bank Corp., filed a lawsuit in the Hong Kong High Court on behalf of unspecified offshore creditors, with Suning Appliance Group, Zhang Jindong and his son, Zhang (Steven) Kangyang, listed as defendants. Zhang Jindong and his son are personal guarantors on multiple Suning bonds, some of which have already matured. The bank is seeking to recover $255 million Suning Appliance Group owes the creditors — $165 million from loans and $85 million from a defaulted bond.

But even with help from one of the “big four” Chinese banks, offshore creditors still face an uphill battle. First, in this case, Suning Appliance Group is the onshore guarantor on the bonds, but the company that issued the bonds is called Great Matrix Limited and is registered in the British Virgin Islands. When looking at Suning’s web of subsidiaries, Great Matrix is removed enough from the onshore assets that it becomes extremely difficult for creditors to trace their way back.

“Overseas creditors face serious challenges when seeking recovery from distressed Chinese conglomerates like Suning, as their claims are usually structurally subordinated to those held by PRC onshore creditors,” says Jason Kang, China-focused litigator at Kobre & Kim. “As we’ve seen in our experience, they often need to deploy creative and aggressive legal strategies to seek recovery from the debtors’ overseas assets, which are often held in complicated cross-border holding structures involving layers of SPVs in the PRC and some offshore jurisdictions.”

The second challenge stems from the fact that, although the Zhang family has personally guaranteed many of these bonds, their assets will likely be kept out of reach of creditors. As of last April, Zhang Jindong was worth an estimated $7.4 billion. But analysts say that Chinese business people are well-versed at protecting personal assets through subsidiaries or even placing them under the names of family members and close friends. Untangling and understanding which assets to go after thus becomes a monumental task for offshore creditors.

“If an individual knows that there will be enforcement cases or actions against them, it will be very difficult to track down their assets,” says Melody Wang, litigator and investigations practitioner at Shanghai Lang Yue Law Firm, Allen & Overy’s joint operation firm in China. Wang is not involved in the Suning case, but says that in the cases she and her team have handled, “Often the individual will have no meaningful assets under their name anymore.”

Indeed, people familiar with the case told The Wire that the Zhang family reported being “stuck,” saying they didn’t have the money creditors claimed. If the family has moved assets for no other reason but to protect them from the creditors, it would be nearly impossible for plaintiffs and their attorneys to prove since Chinese courts don’t have a discovery mechanism — the means through which such information would be shared. The lack of a discovery tool also means that even if creditors do manage to locate assets they could potentially seize, those assets may already be promised to someone else.

“Their enforcement actions become less promising,” says Ran Chen, Wang’s colleague and litigation counsel at Lang Yue. Although Chen does not have personal knowledge of the Suning lawsuit, he says he has seen similar cases play out before. “Entering the enforcement stage, the foreign lenders will often discover that their assets have already been pledged [to someone else] by registering it with some local authorities. They will have no access or their priority will be behind other people’s.”

The task of repossessing assets in, say the United States or Europe, is theoretically easier, and sometimes creditors ask to have these assets pledged as collateral during the negotiations. Suning, for instance, has a very visible asset in Italy — the famous football club Inter Milan. But the Zhang family’s roughly 70 percent of the club is held through Suning Sports, an onshore subsidiary, which means that Suning Sports is covered by a policy that forces creditors to go to a specific local court, the Nanjing Intermediate Court, for any legal actions against it. Attorneys working on behalf of the the creditors don’t seem optimistic about those chances.

“The current suit is not moving anywhere,” says a source close to the matter, “so it is expected to be very difficult to pursue Zhang’s interest in the [soccer subsidiary].”

Analysts say that the risks of the Chinese corporate bond market have always been known: the system is designed for lending convenience, not the legal practicality of retrieving money if an issuer defaulted. But until recently the large profits outweighed those risks. Now, the potential default by Suning and other reputable companies has caused a crisis of trust.

WHEN THE MUSIC STOPS…

Before the current defaults by giants like Suning and Evergrande captured international attention, China’s corporate bond market was quite profitable.

After China joined the World Trade Organization in 2001, Chinese companies increasingly turned outwards in their search for capital. Since China’s banks are largely state-controlled, they mostly preferred lending to state-owned companies, making money for private companies hard to come by in the domestic market.

“Capital is a privilege in China. It’s really hard to borrow. It’s not as easy as it is in the U.S.,” says Patrick Eng, partner at The Sparkill Group, an investment firm focused on China. Eng says that with a high demand for capital, offshore creditors could charge Chinese companies higher rates for loans than they would have elsewhere.

Chinese corporate bonds, as a result, turned into a great investment.

For nearly a decade, the yield of Chinese corporate bonds was one of the most profitable in the world, with the average return hovering around 10 percent. At the peak of the global financial crisis in 2009, Chinese corporate bond returns went as high as 99 percent, according to ICE Data Services. For comparison, last summer, the average yield on U.S. high-risk bonds, also called junk bonds, was around 4 percent.

“You couldn’t get that kind of money anywhere in the U.S. or Europe,” says Walter at Stanford University. “The reason so many investors put their money in China bonds was the yield — it was as simple as that.”

And yet, for much of this time, China’s strict regulations and approval processes made things difficult. The foreign exchange regulator, for instance, didn’t allow private onshore companies to guarantee offshore bonds to raise cash. So, much like the VIE structures now rattling U.S. stock markets, the corporate bond market came up with a workaround: so-called Keepwell obligations. These, in essence, are gentlemen’s agreements: a Chinese company’s offshore subsidiary borrows money from foreign investors while the onshore parent company promises to maintain its financial backing and solvency. But the parent company itself doesn’t formally guarantee payments in case its subsidiary defaults. The only guarantee, in other words, is their good word.

“It isn’t a guarantee or a covenant to pay,” says Jonathan Leitch, a partner at Hogan Lovells, an American-British law firm that has a presence in China. “But what it does is it purports to give some comfort to a buyer that the parent company will actually step up. I think it’s more about convention rather than the people who are buying the bonds necessarily analyzing their legal rights.”

The Keepwell structure, which is unique to Chinese corporate bonds, started being used widely in 2012. Only 11 bonds with such provisions have been defaulted on by their issuing company in the past decade, but the Keepwell structure is estimated to be used in more than 16 percent, or roughly $100 billion, of all outstanding offshore bonds issued by Chinese corporations today. Some experts estimate that number could be as high as 30 percent. In other words, there is a large chunk of China’s corporate debt that might prove unenforceable in the case of default.

The contested Suning bonds do not have Keepwell provisions. They were issued in 2020, after which point China’s foreign exchange regulator allowed private onshore companies to guarantee offshore bonds to raise cash. But the basic setup is similar and the enforceability, analysts say, is only mildly improved.

“For the Chinese companies, there’s a benefit to this offshore structure,” says Leitch. “If the offshore subsidiary company that issued a bond defaults and is forced into liquidation, then all of its assets and subsidiaries below that issuer would then be controlled by the liquidator. But if it doesn’t own anything, then the only asset that the subsidiary will have is an intercompany loan,” he says.

Zhang Shuncheng, associate director of corporate research at Fitch Ratings, notes the offshore bonds are also useful for onshore companies to diversify their funding resources.

“They may go offshore to seek foreign currency denominated bonds, for instance,” he says. “Another factor could be the appreciation of Chinese yuan against the U.S. dollar: They can borrow U.S. dollars and then repay back by Chinese yuan. So, effectively, they will see a decrease in the actual cash they need to get out of their pocket to service that debt.”

Indeed, the system seemed to work well for everyone, even despite the legal disadvantage to creditors. That is, until recently.

“There really have been very few of these China situations that have blown up,” says Leitch at Hogan Lovells. “It’s only now that we’re starting to see a significant number of offshore defaults under these high yield notes. The music never stops until you get to the point where we’re at now, which is the market doesn’t believe what the companies are saying. There is no longer the window for these companies to obtain credit, particularly the real estate developers like Evergrande.”

The music never stops until you get to the point where we’re at now, which is the market doesn’t believe what the companies are saying. There is no longer the window for these companies to obtain credit, particularly the real estate developers like Evergrande.

Jonathan Leitch, a partner at Hogan Lovells, an American-British law firm that has a presence in China

Indeed, at the beginning of November, the yield on an ICE BofA index of Chinese junk bonds rose to its decade-high of 25 percent — a reflection of the market’s view of these bonds as extremely high risk. China’s total corporate debt, meanwhile, is estimated to be $27 trillion, with a debt-to-GDP ratio almost twice that of the U.S., according to S&P Global Ratings. All that borrowing helped fuel China’s incredible growth, but some say it could be the end of an era.

“Suning is representative of this Golden Age: they were just expanding like crazy and dreaming that the next expansion would be financed by the previous expansion,” says Jason Yu, general manager and board member of Kantar Group in China. “But once the credit support is tightened, and they are no longer able to borrow money cheaply, then, nothing is right. Plus, China’s economy is no longer humming as it was before, which adds to this big problem.”

#PRIORITIES

With more than $100 billion in offshore debt borrowed by Chinese companies coming due by the end of this year, the big question is if the music will pick up again. If it doesn’t, many observers say the effects could ripple across the global economy.

“We don’t know exactly the implications and the ramification of this situation. But it’s similar to the global financial crisis starting with the subprime mortgage crisis in the United States,” says Paola Subacchi, professor of international economics at the Queen Mary University of London and the author of The Cost of Free Money. “It started as a domestic problem, and nobody seemed to care. But then a year later it had become a global crisis.”

While it’s not clear to what extent the Chinese government would intervene to prevent such a crisis, it is clear to observers that the well-being of overseas companies would be far from the top priority for Beijing.

“When a company fails to pay the debt,” says Li-Wen Lin at the University of British Columbia, “the top concern for the government is: ‘Is there any risk of social riots? Is there any risk of social protests?’ As a result, they prioritize domestic creditors and vendors getting paid before offshore investors.”

So far, this approach seems to be playing out with Zhang Jindong. The courts have recently frozen 3 billion yuan, or $464 million, of his assets that were pledged as collateral for two onshore lenders. He is currently negotiating more time to pay the maturing bonds, and some observers think he will be required to sell off his overseas assets in order to bring more money back onshore.

“I wouldn’t be surprised if Beijing would expect or require indebted entrepreneurs like Zhang and his son to pay back their debts,” says Zhu Ning, deputy dean of the Shanghai Advanced Institute of Finance and an author of China’s Guaranteed Bubble. “Because if they do not, I am afraid that there might be a more serious outcome waiting for them.” Zhu points to the example of Chen Feng, the former chairman of HNA, the Chinese conglomerate that went bankrupt earlier this year. While the allegations against Chen were not specified, he was arrested in September and forced to sell off his overseas assets.

“The government eventually steps in,” Zhu says, “largely in order to placate the buyers. They don’t want any social instability.”

In the case of Evergande, for instance, Chinese authorities reportedly told Xu Jiayin, the chairman, to use his personal wealth to help the company avoid a worsening debt crisis.

“This is not a legal obligation at all. This is a political request,” says Lin. And in China, a political request could have much more weight than a legal decision.

Suning, meanwhile, is likely to survive, according to analysts — but it might be restructured along the way. According to Suning.com’s third quarterly statement, at the end of October, the company’s sales were down nearly 65 percent compared to the prior year. In the first nine months last year, Suning closed 1,000 self-owned stores around China, and in July, Suning.com appointed a new chairman: Huang Ming-Tuan, who sold his previous company, Sun Art Retail Group Ltd, to Alibaba in 2018. Some observers think the appointment is a sign that Alibaba, which has owned a 19.9 percent stake in Suning.com since 2015 and now holds a 24 percent stake in Suning’s two holding companies, is about to take a more active role in the company’s operations.

“Clearly there is a strong intention to integrate [Suning into Alibaba],” says Jason Yu at Kantar.

“It is very likely they are going to build a stronger connection with Suning so Suning is able to enjoy some of the benefits of scale and the logistics network that Alibaba offers.”

The belief that Suning will emerge unscathed — and that the Chinese government will do whatever it takes to avoid an internal crisis — makes some analysts optimistic that the current lack of trust in Chinese borrowers is only temporary.

“There is no bankruptcy threat,” says Eng, at The Sparkill Group. “It’s a poker game right now, a dance. Right now, the creditors are probably just holding out for more appealing refinancing offers. The problem is thinking you’ll get your money back. You usually don’t. You usually refinance — that’s how the music keeps going.”

It’s a poker game right now, a dance. Right now, the creditors are probably just holding out for more appealing refinancing offers. The problem is thinking you’ll get your money back. You usually don’t. You usually refinance — that’s how the music keeps going.

Patrick Eng, partner at The Sparkill Group, an investment firm focused on China

“It’s very natural in the financial industry that reward will usually come with risk,” says Jenny Huang, senior director at Fitch Ratings. “As long as the pricing [on bonds] reflects the potential risk that you will undertake, then investors are willing to enter the market.”

For those creditors who hope to maximize their chances of asset recovery, however, experts say more attention needs to be paid to the very beginning of the process.

“In my experience, the creditors do not do enough research at the time they do the transaction,” says Melody Wang, of Lang Yue. In one case Wang saw, an offshore creditor thought it was doing the responsible thing by asking for the overseas assets of a businessperson to be pledged as collateral. But by the time that person defaulted on payments, their assets outside of China were already gone.

“The current struggles of companies like Evergrande and Suning to pay their debt will be a good lesson for the creditors, especially internationally, that when they deal with mega companies in China, they need to be mindful of the risk,” says Wang. “These companies are very large and reputable, and they’ve been in the market for a very long time, but this episode will corroborate the fact that you need to be very careful when investing in China.”

Anastasiia Carrier is a staff writer at The Wire. Her work has appeared in POLITICO Magazine, Harvard’s Radcliffe Magazine and The Brooklyn Eagle. She earned her Master’s degree in Journalism at the Columbia University Graduate School of Journalism. @carrierana22