In 2012, an investigation by The New York Times’ David Barboza — now The Wire’s editor-in-chief — into the hidden riches of the family of China’s then-premier, Wen Jiabao, revealed that they controlled assets worth at least $2.7 billion. Their holdings included stakes in property companies, banks, jewelers, telecommunications and finance. One investment stood out for the substantial windfall it netted the family: a stake in Ping An Insurance, one of the world’s largest financial services firms.

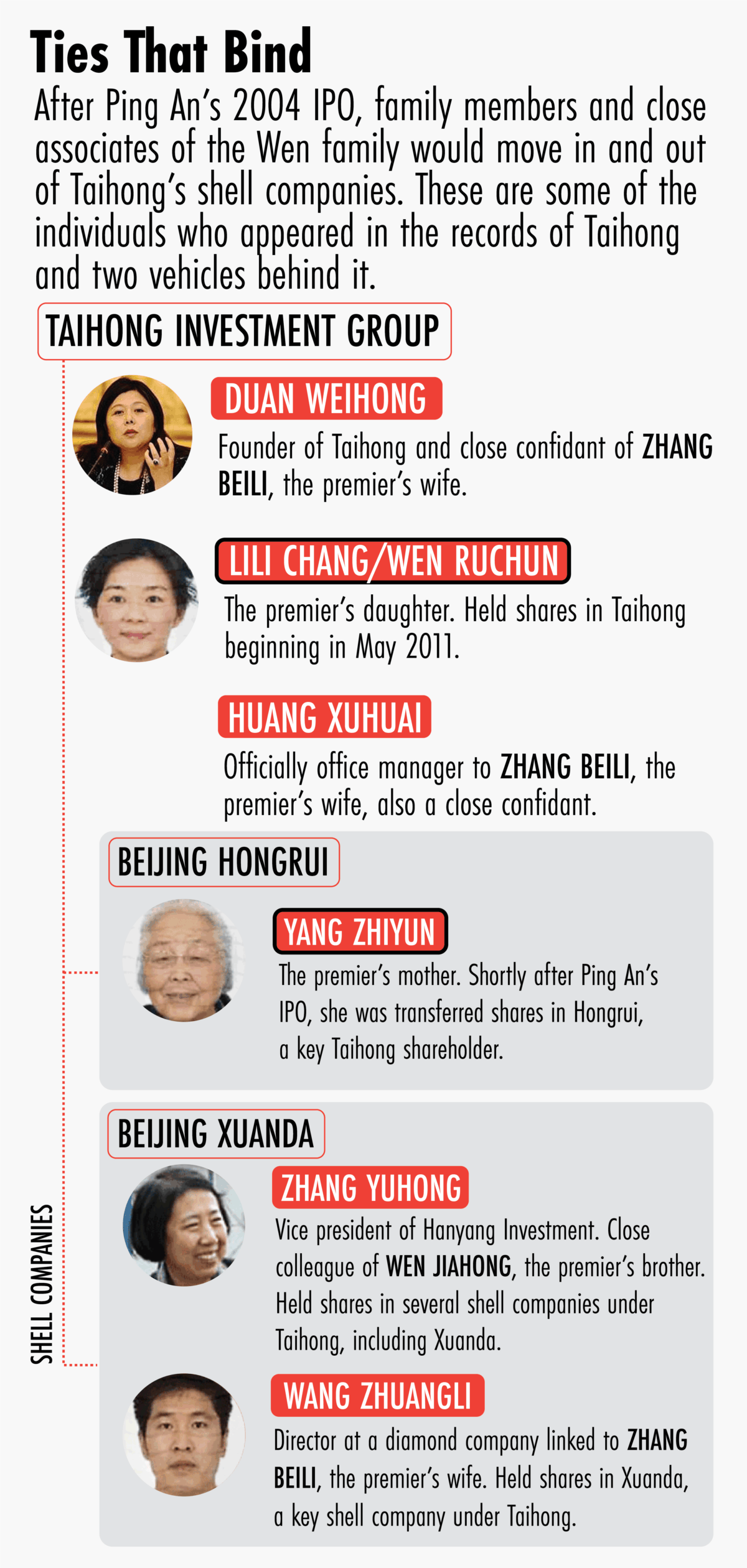

By examining corporate records, The Times found that Wen’s relatives and their close associates controlled shares in Ping An that would have been worth as much as $2.2 billion in 2007, the year the company listed its shares on the Shanghai Stock Exchange. A large portion of their Ping An holdings were held indirectly and concealed behind one company: Taihong, which was controlled by Duan Weihong, a wealthy businesswoman and confidant of Premier Wen’s wife, Zhang Beili.

After Wen retired in 2013, China’s top leader, Xi Jinping, announced a sweeping anti-corruption campaign that subsequently brought down former Politburo members Zhou Yongkang and Sun Zhengcai. Then, in September 2017, Duan Weihong disappeared from Beijing. She was believed to have been detained as part of a corruption investigation but Chinese authorities have not said publicly that she was detained or charged with any crime.1Duan made a phone call to her ex-husband Desmond Shum a few weeks ago saying that she had been detained but has not yet been charged and has been released.

Last month, about four years after Duan’s disappearance, her ex-husband and business partner, Desmond Shum, published Red Roulette, a tell-all book about the couple’s life and business dealings with China’s political elites. In it, Shum confirms that he and his ex-wife helped the relatives of China’s prime minister gain a stake in the financial services giant. This week, The Wire revisits the Ping An deal, tracing the steps Taihong took to bring in the relatives and associates of the Wen family, and details who was involved and how their stake was concealed.

THE PROSPECTUS

Ping An Insurance was founded in 1988, and evolved with financial backing from the government and private investors. It was one of the first Chinese financial institutions to attract foreign investors, most notably Morgan Stanley, Goldman Sachs and HSBC. The company went public in June 2004 on the Hong Kong Stock Exchange, with one of the biggest stock offerings of the year. And yet the company’s IPO prospectus gave no indication that a portion of the company was owned by the relatives of Wen, who as premier had oversight over the financial services industry.

Details from Red Roulette explain how the Wen family came to hold an indirect stake in Ping An. In 2002, the Chinese shipping giant COSCO was looking to sell a 3 percent stake in Ping An. Shum says that his ex-wife, Duan Weihong, approached Wei Jiafu, the chief executive of COSCO, with an offer to buy the shares. According to Shum, the purchase went through and two-thirds of the shares in Ping An went to Zhang Beili, Wen’s wife, and one-third went to Duan and Shum.

COSCO sold its shares to the investors for about $36 million, according to Shum. Duan and Shum’s stake was secured via a bank loan, while the stake held by the Wen relatives was financed with the help of Zheng Jianyuan, a businessman linked to Hong Kong-based New World Development, the property developer controlled by Cheng Yu-tung, Shum said in an interview with The Wire. (Zheng could not be reached for comment.)

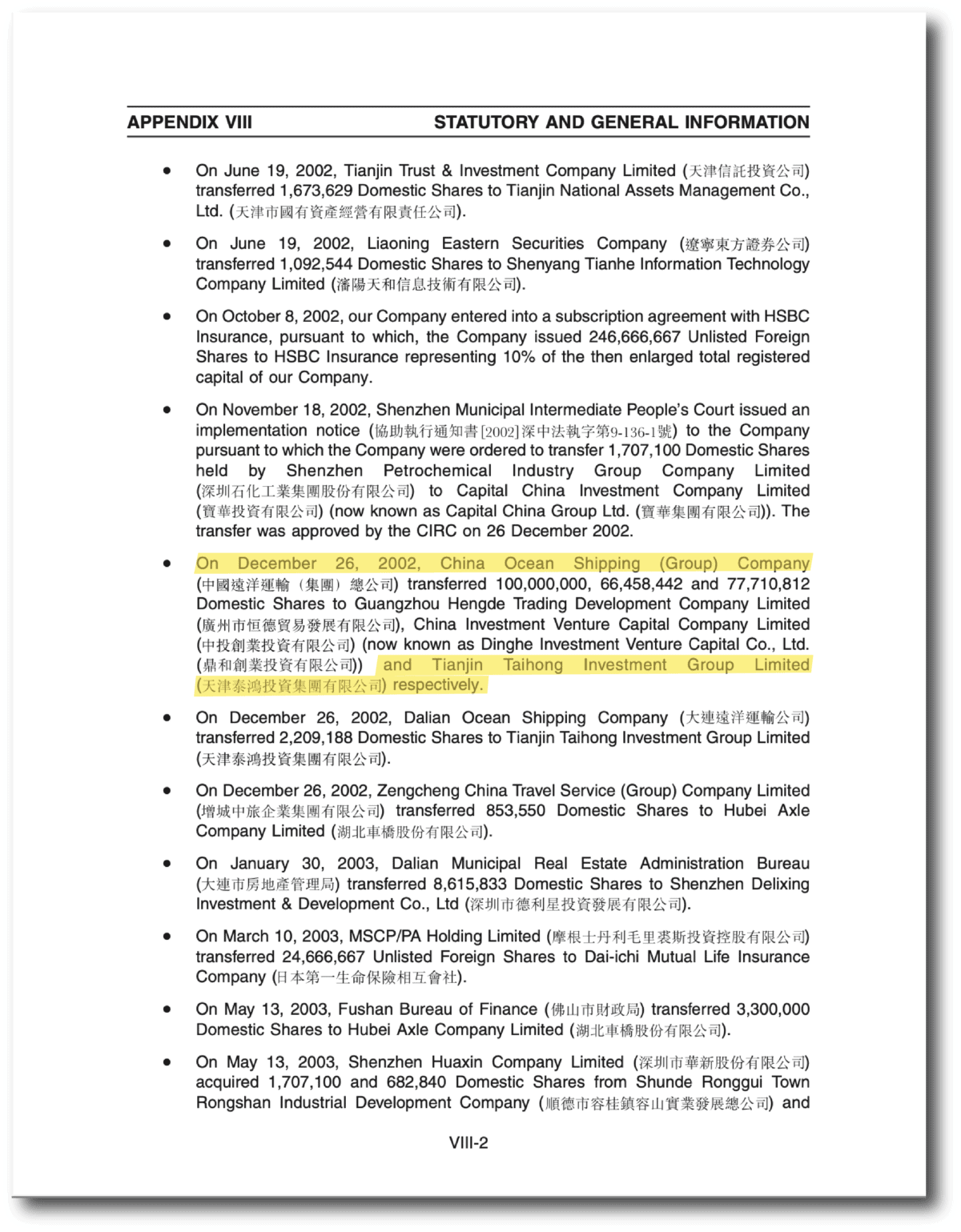

Ping An’s prospectus records the transfer of 77,710,812 domestic shares from COSCO to the Tianjin Taihong Investment Group in December 2002. Taihong’s effective 3.24 percent stake made it Ping An’s 13th largest shareholder at the time of the 2004 IPO.

But to an observer reading the prospectus, it was far from clear who owned Taihong, and therefore held the 77 million Ping An shares. The Times investigation into the corporate records of Taihong revealed that the ultimate beneficial owners, shielded by as many as five layers of shell companies, were largely the Wen family and their close friends and business associates. The files suggest that associates of Zhang Beili may have served as so-called “white gloves” for the Wen family, holding stakes on their behalf, a practice Shum describes as widespread among China’s political elite.

WHO OWNED TAIHONG?

The following graphic depicts the structure behind Taihong in July 2004, one month after Ping An’s Hong Kong IPO.

Design by Hiram Henriquez

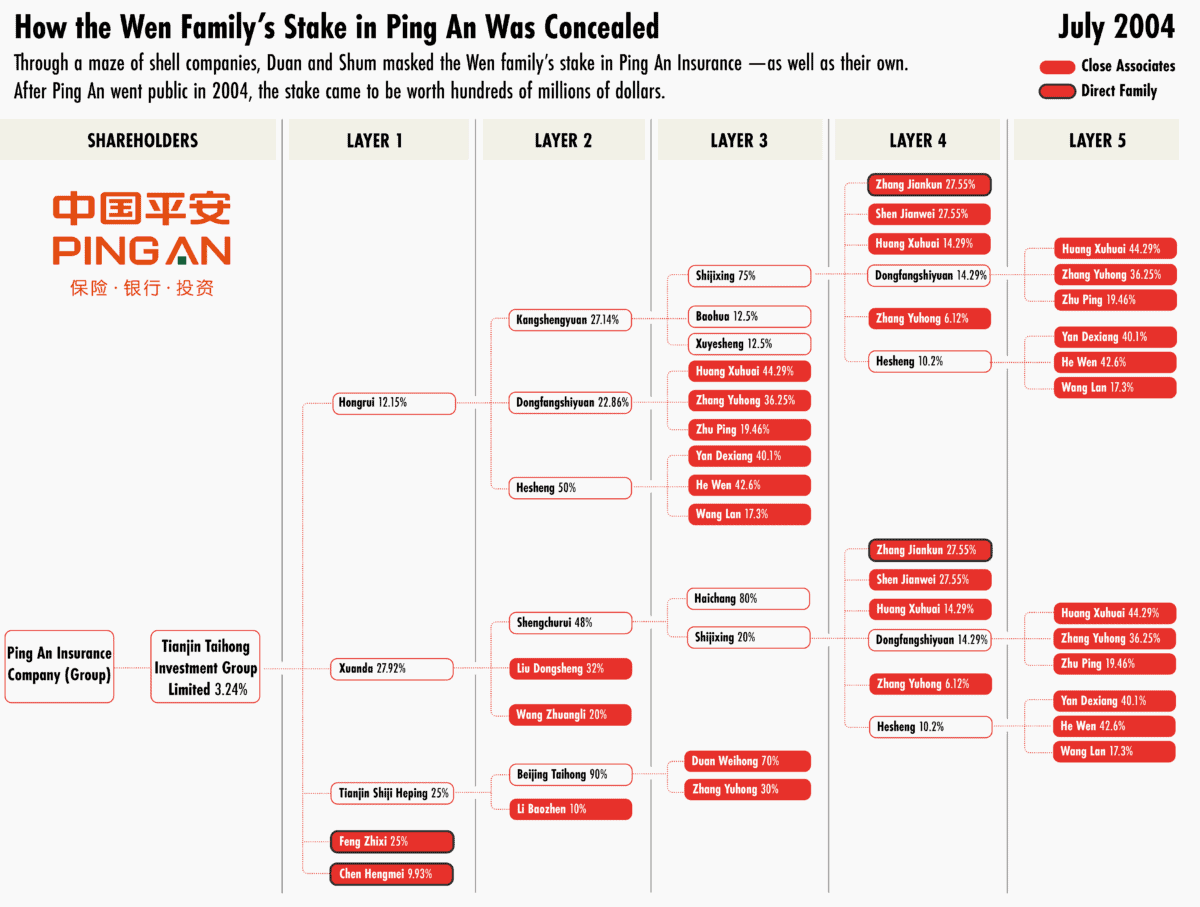

While few members of the Wen family are directly named as owners of Taihong, several of the family’s close associates can be identified. One is Huang Xuhuai, a close aide of Wen Jiabao’s wife, Zhang Beili. While officially titled “Office Manager to Madame Wen Jiabao,” he was also her personal confidant, according to Shum. Another is Wang Zhuangli, who alongside many of Taihong’s other beneficial shareholders, worked at one point with Zhang Beili at a state-controlled diamond company, according to corporate filings.

Zhang Yuhong is also listed in corporate filings as a Taihong shareholder. She was a business partner of the premier’s daughter, Wen Ruchun, and the premier’s brother, Wen Jiahong. At one time, Zhang served as vice president of Hanyang Investment, a firm run by Wen Jiahong. Zhang Yuhong also helped run Fullmark Consultants, a firm co-founded by Wen Ruchun that did consulting work for JPMorgan, according to another New York Times investigation in 2013.

As ownership of the shell companies tied to Taihong changed hands in the years after Ping An’s IPO, links to the Wen family became increasingly clear. A key revelation came from the corporate files for Beijing Hongrui, one of the direct shareholders in Taihong.

Ten months after the Ping An IPO, shares of Hongrui were redistributed, with one stake transferred to Yang Zhiyun, the mother of Premier Wen. A retired schoolteacher with a government pension, she was brought into Hongrui when Wen’s wife grew concerned that a large portion of her stake in Ping An was held by Duan’s companies, according to Shum.

That move, Shum wrote, would prove to be a “fateful mistake” because it tied the Wen family more directly to Ping An. The Times would later estimate Yang’s shares in Ping An to be worth $120 million.

Ping An would also list shares on the Shanghai Stock Exchange in 2007, allowing Duan and Shum to cash out that year — China’s capital controls had previously prevented the couple from selling their shares on the Hong Kong market, which was considered offshore. Six months after the Shanghai IPO, the couple sold their stake for a profit of more than $300 million, twenty-six times their initial investment, according to Shum.

It is unclear when members of the Wen family and their associates sold their shares in Ping An. After Duan and Shum sold their stake, ownership of Taihong changed hand several times, and in 2011 a 14 percent stake in the company was transferred to Lili Chang, also known as Wen Ruchun — Premier Wen’s daughter.

Besides the premier’s mother, brother, and daughter, other Wen family members identified by The Times as having held Ping An shares included the premier’s two brothers-in-law, a sister-in-law, daughter-in-law, and the parents of his son’s wife. The byzantine network of shell companies may have provided cover for individual shareholders who were frequently swapped in and out, making it difficult to see the extent of the ties between Taihong and the Wen family at any given moment in time.

PING AN’S CURRENT SHAREHOLDERS

Duan Weihong and Desmond Shum had long since sold their shares in Ping An when the Times’ investigation was published in October 2012. It’s less clear what happened to the Wen family’s stake, however. Premier Wen’s wife told Duan and Shum that the family had donated all of their assets to the state in exchange for immunity from prosecution, Shum says in his book, Red Roulette.

In December 2012, Charoen Pokphand Group (CP Group), a conglomerate controlled by Thai billionaire Dhanin Chearavanont, bought a 15.6 percent stake in Ping An from HSBC for about $9.4 billion. At the time, HSBC said that it had sold the shares as part of a strategy to sell off non-core assets.

Today, CP Group remains the largest single shareholder in Ping An, though it has reduced its stake, most recently in September. While Ping An’s market value is close to $130 billion, its stock has fallen by more than 40 percent this year, falling further in recent weeks due to concerns about its exposure to Chinese real estate stocks amid a liquidity crisis at Evergrande Group. Ping An recently said that it has no exposure to Evergrande.

A look at Ping An’s top shareholders shows that among global investors it remains one of the most widely held Chinese stocks.

Ping An did not respond to multiple requests for comment.

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen