Credit: Sim Chi Yin via Magnum

On an early September morning 10 years ago, the Chinese fishing trawler Minjinyun 5179 collided with a Japanese Coast Guard patrol boat in the East China Sea. The trawler had been fishing near disputed territory controlled by Japan known as the Senkaku islands, or Diaoyu in Chinese. Beijing had been increasingly hawkish towards numerous contested territories, but a long-standing animosity between the two countries made the Senkakus a particularly fiery flashpoint.

The Japanese Coast Guard detained the crew of Minjinyun, incensing Beijing and setting off a series of intense anti-Japan demonstrations across China. The diplomatic fallout outlasted the fishermen’s release when, in what many saw as a retaliation, Beijing blocked all exports to Japan of one of the most critical materials of the modern world: rare earths.

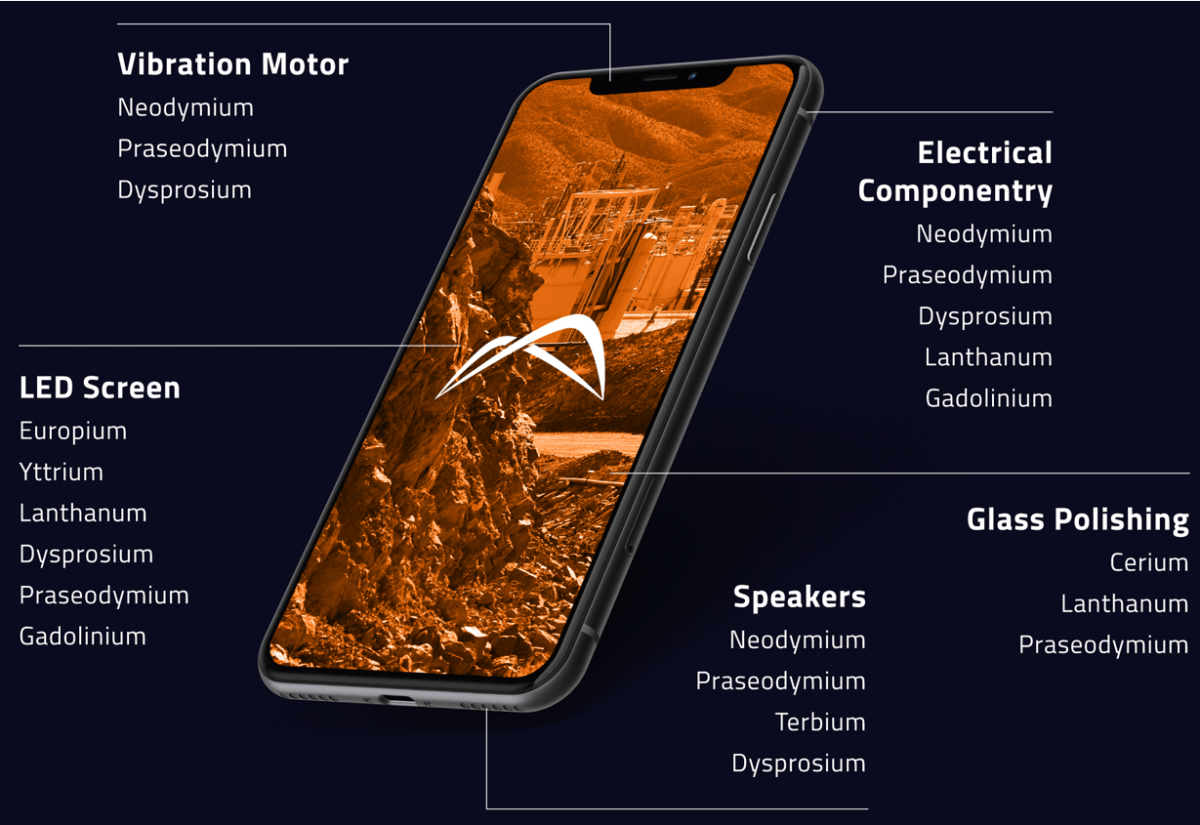

Rare earths are the pixie dust of modern technologies. With tongue-twister names like dysprosium, yttrium, and praseodymium, they comprise 17 elements on the periodic table, and go into everything from camera lenses to nuclear reactors. A single smartphone might contain 16 rare earths while an F-35 jet is said to consist of 920 pounds of rare earths. While the elements are found throughout the earth’s crust, they are considered rare because sizable deposits are found in just a few areas — namely, China.

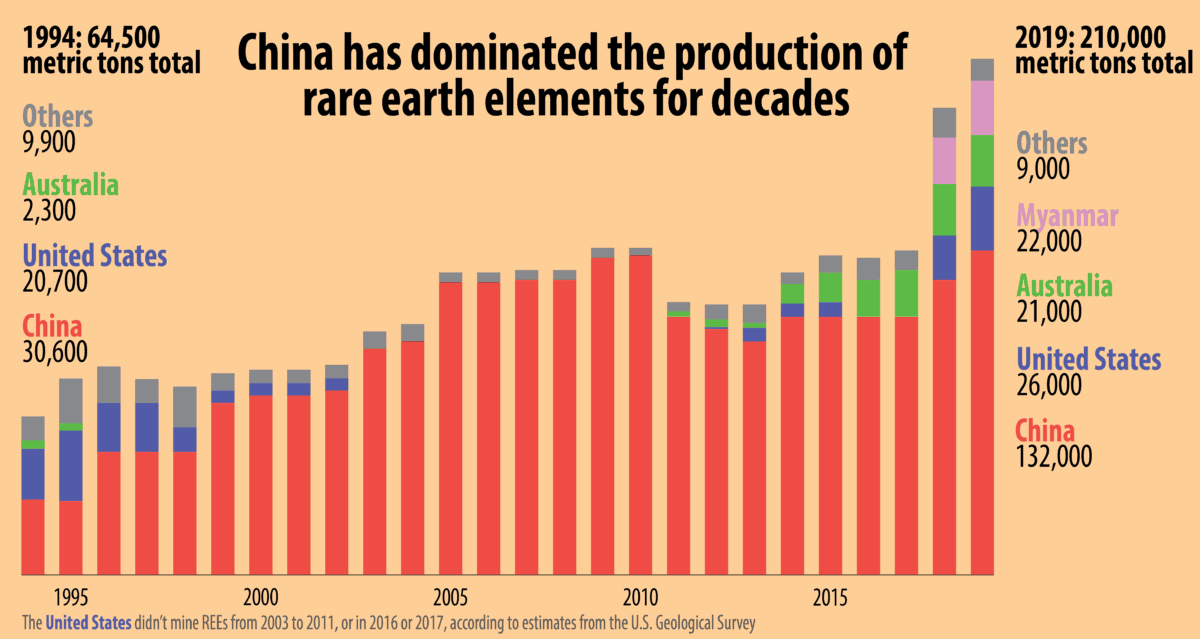

At the time of the export ban to Japan, China accounted for 97 percent of the global supply of rare earth elements, or REEs. And the incident demonstrated that China could — and would — suddenly turn off the tap1China denies it killed exports because of the incident. Markets panicked; one rare earth, dysprosium oxide, went from $200 a kilogram to $2,000 a kilogram overnight.

Credit: MP Materials

Washington panicked too. China, after all, had retaliated in geopolitical disputes using commodities before: blocking salmon imports from Norway and bananas from the Philippines, and closing South Korean department stores. Why couldn’t China do the same with rare earths, those critical ingredients of modern life and American national defense?

In September, the U.S. House of Representatives had passed the Rare Earths and Critical Materials Revitalization Act by a large, bipartisan margin. The alarm bell rang.

“The bottom line is this: China is cornering the market on rare earth materials and we are falling behind,” said Rep. Kathy Dahlkemper (D-PA), the bill’s sponsor, at the time. That is why we need to act now to begin the process of creating our own domestic supply of rare earth materials so the United States is never dependent on China — or on any other country — for crucial components for our national security.”

For the U.S., the threat from China went “right into the mix along with fears about selling off U.S. Treasury bonds or other potential ways that the Chinese could harm their adversaries,” says Scott Kennedy, an expert on Chinese technology at the Center for Strategic and International Studies.

For a decade, then — since the Senkaku affair — analysts and American politicians have argued that the U.S. should separate itself from Chinese rare earth supplies. But only recently has the potential stranglehold over rare earths translated into action by Washington. The turning point was May 2019 when, following the U.S. decision to blacklist Huawei, China released photos of President Xi Jinping visiting a rare earths magnet maker in Jiangxi Province. Xi’s subtext was clear: If you sanction us, we have our own cards to play.

Soon after, the Pentagon initiated funding to support building new processing facilities for REEs in the U.S. By last summer, lawmakers were arguing for tax incentives to encourage repatriation of the rare earths supply chain. And in September, President Trump signed an executive order to support mining, deeming the nation’s minerals reliance on “foreign adversaries” a national emergency. As recently as October, just before the U.S. election, Joe Biden told miners he would support efforts to boost domestic production.

With the U.S. still importing 80 percent of its REEs from China, Washington’s efforts to decouple the supply chain from China seem overdue. But can the U.S. really break its reliance on China? How might America pull it off?

A TALE OF TWO MINES

Rare earths were discovered in Sweden in 1787, but it wasn’t until the twentieth century that they were propelled to global prominence. In pursuit of color television, engineers discovered that they needed the rare earth europium to make the color red pop on a screen. Manufacturers started using europium in everything from TVs to computer screens, and lasers to fluorescent lights.

Fortunately for the U.S., its one and only rare earth mine — the Mountain Pass Mine in southern California, just an hour from Las Vegas — possessed an unusually large deposit of basanite, the rock containing europium. Before the advent of color TV, Mountain Pass’s ore had mostly been used to make flints in lighters, but the technology boom changed all that. For the next three decades, Mountain Pass reigned supreme in the REE world, and Molycorp, the owner of Mountain Pass, prospered through these golden years.

The Colorado company even solidified its dominance by finding new uses for rare earths, which were mostly processed in the U.S. at the time. From the 1980s to the 1990s, most of the mine’s cerium went towards the glass industry, its samarium to magnet manufacturers and its cerium, lanthanum and neodymium to producers of automotive catalytic converters. Production increased eight-fold from the 1960s to the 1980s, with the mine extracting up to 20,000 tons of REEs per year, a sum that met nearly all global demand.

Credit: Ricky Carioti/The Washington Post via Getty Images

On the other side of the world, China saw an opportunity. Bayan Obo, in Inner Mongolia, is the largest known single deposit of REEs in the world — 50 times larger than Mountain Pass. Chinese leaders recognized the potential. Deng Xiaoping compared China’s rare earths advantage to the Middle East’s oil advantage, and in the 1980s set about investing heavily in the industry, including educational opportunities for rare earth scientists and geologists.

The efforts paid off. Buoyed by state subsidies and a lack of environmental regulation, production of rare earths soared between 1979 to 1989. In the 1990s, it flooded the market with exports. The price of REEs plummeted, and many foreign competitors, like Molycorp, struggled to stay afloat.

Moreover, while China was ramping up production with little-to-no environmental oversight, the U.S. government cracked down on pollution. Though critical ingredients in green technologies like wind turbines and electric vehicles, rare earths are some of the most destructive materials to extract from the earth. Most of the mess is made in the separation process, which involves huge quantities of water, chemicals and acids. If not disposed of carefully, the toxic “tailings” can contaminate the earth and leach into groundwater. In 1998, a federal study found that 600,000 gallons of hazardous waste had flowed from Mountain Pass operations into nearby deserts. In 2002, saddled with debt and large clean-up bills from the EPA, the mine was shuttered for eight years.

Over the next two years, the United States imported more than 90 percent of its rare earth commodities from China.2 [Between 2005 and 2008, Chinese firms made three unsuccessful attempts to acquire Mountain Pass, one of which was blocked by Congress on national security concerns.]

“If you have state support and the environmental concerns are not there, constraints are not there, it means that your cost of production is next to nothing,” says Chris Berry, a rare earths consultant in Washington. “That is almost impossible for us here in the West to compete with.”

Indeed, China’s REE strategy was orchestrated from the top. In 1990, Beijing designated rare earths a “protected strategic material,” which barred foreigners from mining them and forced foreign investors to create joint ventures with Chinese companies to deal in the Chinese market.

China also consolidated the supply chain — from mining to processing to manufacturing — within its borders. The magnet industry, for example, requires large amounts of REEs, and one of the top producers of car magnets (which are used for both fuel and production efficiency ) used to be the American company Magnequench. In 1995, however, two Chinese companies partnered with a U.S. investment firm to acquire Magnequench, once a General Motors subsidiary. The U.S. government approved the acquisition on the condition the Chinese keep the company stateside for at least five years. The day after the deal expired the entire operation was relocated to China.

If you have state support and the environmental concerns are not there, constraints are not there, it means that your cost of production is next to nothing. That is almost impossible for us here in the West to compete with.

Chris Berry, a rare earths consultant in Washington D.C.

The market followed: In 1998, the United States, Europe, and Japan accounted for 90 percent of global magnet production; less than a decade later, most of the $20 billion industry was in China. The strategy worked just as President Jiang Zemin said it would in 1999: “Improve the development and application of rare earth, and change the resource advantage into economic superiority.”

DON’T CALL IT A COMEBACK

After being pummeled by lower-cost Chinese products, heavy investments and environmental violations, Molycorp, the company that ran Mountain Pass, found itself $1.4 billion in debt. The company filed for bankruptcy in 2015, and the mine sat unused for two years — even after the Senkaku Islands incident had supposedly set off alarm bells about America’s rare earths vulnerability.

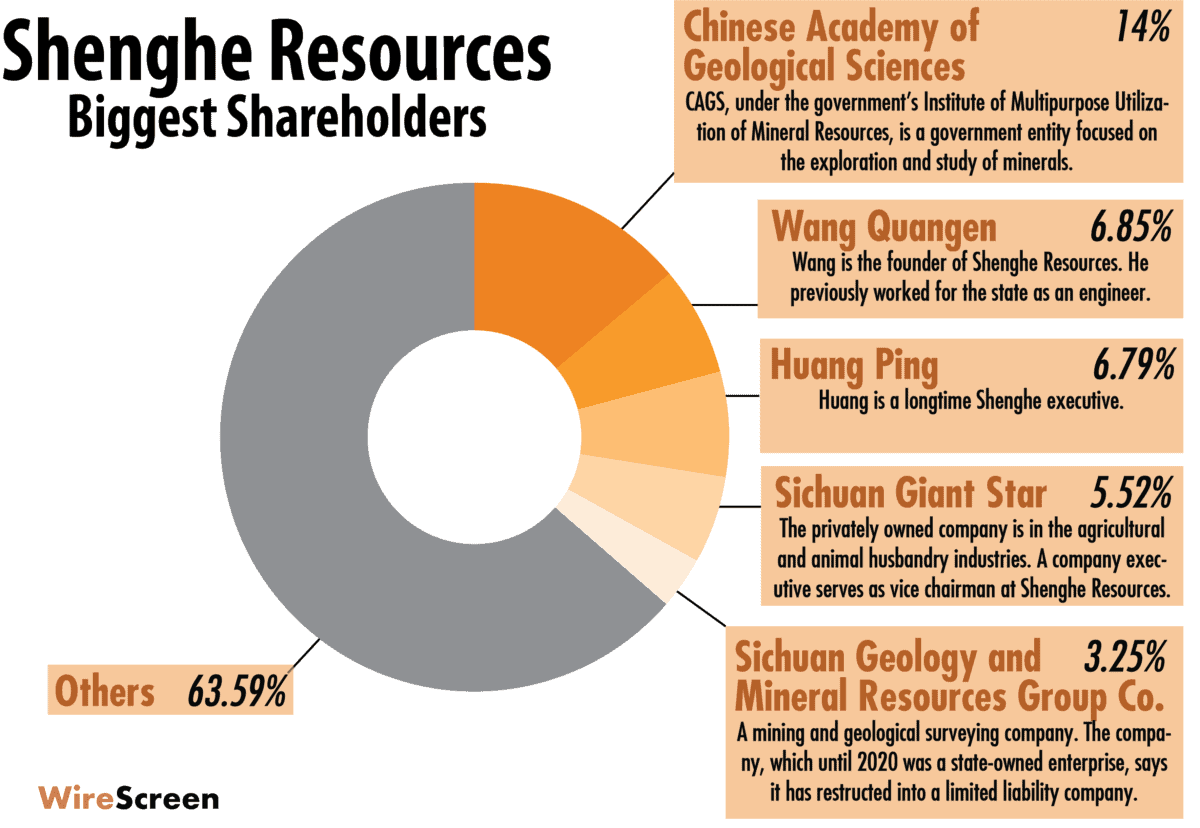

It wasn’t until 2017 that Mountain Pass Mine was sold at auction for $20.5 million to a group that included the Chicago hedge fund JHL Capital Group and a Chinese state firm called Shenghe Resources. A new consortium called MP Materials was formed to restart operations there. It went into overdrive, rapidly restoring operations at the idled mine. Today, Mountain Pass employs 270 employees and accounts for 15 percent of the global supply of rare earths. Its focus is mining the REEs used in industrial magnets for technologies such as electric vehicles, smartphones, wind turbines and defense applications.

While there are several confirmed rare earth deposits in the U.S. — the Wet Mountains in Colorado, Bear Lodge in Wyoming, and Elk Creek in Nebraska — Mountain Pass remains the largest and only functioning American REE mine. It would take at least a decade, experts say, for any other U.S. location to be operational, making the California mine the best hope to decouple from dependency on Chinese supplies.

“Our mission is to restore the full rare earths supply chain to the United States of America and we are years and billions ahead of any other producer,” says MP Materials president James Litinsky.

Credit: U.S. Geological Survey

But while Mountain Pass is productive again, the U.S. has not made up for its decades-long absence in the REE supply chain. Mountain Pass relies on Chinese expertise to process its rare earths to marketable quality and Chinese buyers account for all of its $100 million annual revenue. Mountain Pass ships 50,000 tons of concentrate to China for refining every year, with most purchased and separated by its Chinese partner, Shenghe.

Hoping to change that stranglehold, the Pentagon recently awarded MP Materials $9.6 million in funding to modernize its separation facility, which when completed in 2022, will be the only such facility in the western hemisphere. The Pentagon also provided funding for Australia’s Lynas Corp, which owns a rare earth processing facility in Malaysia — the only one outside of China — to construct a similar facility in Texas with Blue Line Corp, a private firm. Urban Mining Company, a rare earths recycling firm in Texas, received $29 million in Pentagon funding. The Pentagon has a great stake in rare earths, after all: a Virginia-class submarine, for example, requires 9,200 pounds, according to a congressional report.

Indeed, rare earths are so vital that the Trump administration has earmarked $209 million in public funding and a bipartisan group of Texas lawmakers is hoping to create a tax incentive program to encourage U.S. based investment.

All of this is good for business at Mountain Pass, which went public on the New York Stock Exchange this week thanks to a merger with Fortress Value Acquisition Corp., a special purpose acquisition company.3According to Quartz, Fortress is controlled by Japan’s SoftBank Group. MP Materials has been criticized by some insiders because Shenghe — MP’s biggest customer — owns 9.9 percent of its non-voting shares. The investment from China raised eyebrows and even paused the Pentagon’s investment before a third-party review for the Pentagon cleared the transaction.

Data: WireScreen

But even MP Materials acknowledges the “risks related to MP Materials’ arrangements with Shenghe” in a recent IPO release, and observers see potential problems. For example, if MP’s new processing facility faces hurdles — and given how complex and multi-tiered the separation process is, hurdles are likely — “Shenghe will just be waiting in the wings, saying, ‘Send it back to us because we already know how to separate it,’” says Berry.4According to an SEC filing, MP Materials recently paid Shenghe a $66.6 million one-time “settlement charge” to restructure the original arrangement.

“The real key to unlocking Chinese dominance of the supply chain is the separation of the rare earths and that’s what Shenghe has been doing for MP Materials for years now,” he adds.

Litinsky cites the company’s board, which includes Richard Myers, the former chairman of the Joint Chiefs of Staff under President George W. Bush, as proof of its patriotism.

“It amazes me that this is even a question,” he says. “Look at this facility. How could you lift this up and move it to Beijing?”

When its processing facility is completed, Mountain Pass expects to produce 5,000 annual tons of separated neodymium and praseodymium oxides, lanthanum and cerium oxides and “heavy” rare earths concentrate. 5“Heavy” is more profitable compared to their current “light” concentrate capabilities.The Pentagon uses less than 5 percent of a domestic REE consumption of around 13,000 tons.

But given the complex stages of the rare earths supply chain, to say nothing even of the environmental costs, analysts say it would be unwise for the U.S. to put all its eggs in one basket.

“It’s a reasonable deposit, but I wouldn’t say it’s a world-beating deposit by any stretch of the imagination,” says Berry. “They can probably help contribute to U.S. defense needs, but I wouldn’t say that single mine could make the United States self sufficient.”

“This cannot be done by just giving a few million dollars in seed money,” adds Sophia Kalantzakos, a professor at New York University. “It requires a major transformation.”

THE SEARCH FOR SOLUTIONS

Today, China accounts for 80 percent of global supply of rare earths, down from 90 percent a decade ago. Part of the reduction was purposeful on environmental grounds. In Jiangxi Province, for instance, where nearly all of the world’s dysprosium is mined — a commonly used REE for high-power magnets — the farmland surrounding the mines was poisoned beyond use, according to the book The Elements of Power. Only 0.2 percent of the mined clay there contains REEs, leaving 99.8 percent to be discarded in tailings that have been carelessly dumped only to seep into groundwater through streams, lakes and rivers. Around Bayan Obo, in Inner Mongolia, villagers suffer skin rashes, osteoporosis, cancer and respiratory diseases that have been traced to the noxious chemicals left behind by the mine.

But China shows no signs of backing off rare earth mining. Beijing’s Made in China 2025 strategy, a plan to update Chinese manufacturing with a focus on high-tech industries, calls for an “intelligentization” of the rare earths industry.

Environmental concerns, says Kalantzakos, are “at the top of the government’s preoccupations.” Beijing has cracked down on illegal mining, recycling and black market smuggling. The state has tightened control over trade as well, with the industry now consolidated under six state-owned mining groups with production quotas.

No matter what the U.S. does, analysts say China’s dominance is likely to continue. “There is no other example of one nation having such a stranglehold on the supply of a vital element as is the case with China and rare earths,” writes Kalantzakos, in China and the Geopolitics of Rare Earths.

The United States just cannot rejigger rare earths supply chains on its own. It just wouldn’t be economically feasible.

Martijn Rasser, an analyst at the Center for a New American Security and former foreign technology analyst at the Central Intelligence Agency

Others say developing an alternative supply chain involves more than just money and facilities. Beyond the infrastructure of mining, processing and manufacturing, the U.S. lacks the intellectual know-how — the rare earths professionals that China invested in during the 1990s.

“It’s not the smarty-pants PhDs and professors like me, who we’ve got plenty of,” says Mark Johnson, the Director of the Center for Advanced Manufacturing at Clemson University. “It’s all the folks that have bachelor’s degrees in engineering and chemical engineering and have an expertise in how to make an actual rare earths process work.”

For this reason and others, Martijn Rasser, an analyst at the Center for a New American Security and former analyst at the C.I.A., says a “multinational coalition approach” on the part of the U.S. is not only preferable but necessary.

“The United States just cannot rejigger rare earths supply chains on its own,” he says. “It just wouldn’t be economically feasible.”

Indeed, alongside encouraging domestic production, the U.S. has also been seeking new rare earth deposits in friendly countries abroad, such as Australia and Greenland.6Shenghe has also invested in a large operation in Greenland. It is also ramping up efforts to find substitutions for rare earths.

The Department of Energy funds the $240 million Critical Materials Institute, a research consortium involving four national labs and seven universities working to cut rare earths out of the equation. And DOE’s REACT program is looking for solutions for clean energy technologies, such as electric vehicles, that are not heavily dependent on rare earths.

Mark Johnson, former director of the Advanced Manufacturing Office overseeing the REACT program, says it investigated new nanoparticles and nanostructured materials that could, in theory, give the same phenomena as rare earths.

“They showed some kind of laboratory-scale results,” he recalls, “but nothing that was a huge home run.”

Of course, the underlying assumption motivating these efforts is that China would weaponize its rare earth dominance in a future conflict with America or its allies. “In the near term, it would have significant impacts,” says Rasser, at CNAS.7The Center for New American Security “It takes time to restart these facilities and to set up the processing, anywhere from 18 to 24 months.”

But just because it could, analysts say, doesn’t mean it would. Rasser doesn’t see such a move being in China’s interest, as it would crater its credibility in the global market. “[Countries would think], if you’re willing to do this for rare earths, where else are you willing to do that?” he says. “Then you start having a lot of countries worrying about the reliability of China as an exporter.”

To Kennedy, at CSIS, China’s recent veiled threats of restricting rare earths is more an attempt at “psychological warfare” than a demonstration of intent or ability.

“They have never taken that kind of economic coercive step against the United States or other major powers,” he says. “Banning salmon imports from Norway is one thing; starting a high-tech war or escalating a high-tech war with the United States is something else.”

With the U.S.-China relationship not improving anytime soon, though, the U.S. may not want to wait another ten years to make progress. “If there ever was an optimal time to rethink these supply chains,” notes Berry, “it’s now.”

Brent Crane is a journalist based in San Diego. His work has been featured in The New Yorker, The New York Times, The Economist and elsewhere. @bcamcrane