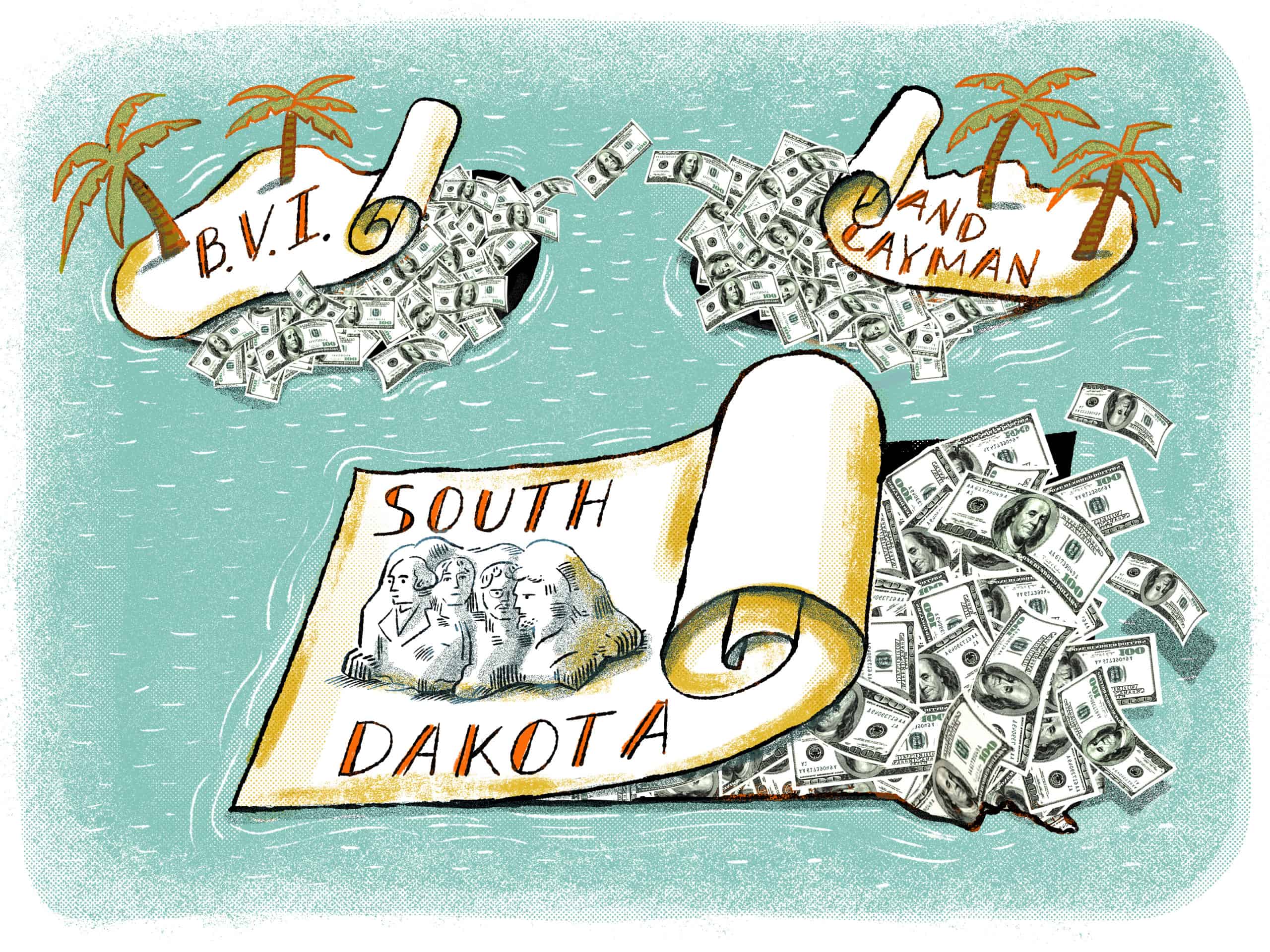

About a year and a half ago, the sleepy state of South Dakota found itself rudely awoken by the global spotlight. In a filing for his Hong Kong-listed company, Sunac, Sun Hongbin, the Chinese real estate tycoon with a net worth around $10 billion, disclosed he had just transferred his shares to the South Dakota Trust Company. To the surprise of most analysts, a small, two-story brick building in downtown Sioux Falls was the proud custodian of a chunk of shares that is now worth more than $6 billion.

What’s more, as Bloomberg News reported at the time, three other Chinese businessmen had moved billions to South Dakota trusts just weeks before Sun did. The incongruity was lost on no one, and many observers started to wonder what, exactly, was going on in South Dakota. Suddenly, the 97 trust companies licensed to do business in South Dakota felt the global gaze upon them.

“Are people here talking about it? No,” Jason Krause, a lawyer in Sioux Falls, says of the influx of Chinese money. “It’s the Midwest; everyone wants to pretend that we’re not dealing with that here, that there’s not this offshore investment happening.”

South Dakota, it turns out, has among the most generous trust laws in the world; trusts established in the state can benefit yourself (as opposed to a child or charity), exist in perpetuity, face no state taxes, and all records, including those from courts, are sealed. That means if you place money in a South Dakota trust, it can grow indefinitely, unencumbered by most taxes, and nobody — not even spouses or your children — will know about it unless you disclose it, like Sun did in a Hong Kong regulatory filing.

Credit: Sunac 2012 annual report

Sun was just doing what any savvy billionaire does: moving assets around the world to shield them from tax burdens and other impositions, such as litigious clients, creditors or even governments. But Sun likely had a more fierce desire to protect his wealth than your average billionaire. He, after all, had almost lost it all once before.

A native of Shanxi province and an engineering graduate from the prestigious Tsinghua University, Sun’s career had started well enough at Lenovo, the Chinese technology company. But in 1992, he was charged with embezzling nearly $20,000 from the company. He was sent to jail for almost two years. With his career and reputation seemingly in tatters, Sun got right to work rebuilding himself. He founded a real estate group in 1995, attended Harvard Business School for a management program in 2000, founded Sunac in 2003, and by 2010, he had gotten his conviction overturned, finagled Bain Capital financing, and taken Sunac public.1See this Bloomberg profile of Sun Hongbin in 2014.

He was back on track. But for China’s elite, nothing feels safe.

“In the U.S. or Europe, if your money is in the bank, you’re confident the government isn’t going to confiscate it. That’s not necessarily the experience of wealthy folks in China,” said William Vlcek, a professor at the University of St Andrews who specializes in offshore finance. Consider, for example, Xiao Jianhua, the billionaire who was apparently kidnapped from a Hong Kong hotel by Chinese authorities in 2017. His whereabouts are still unknown, and in July, Chinese authorities stripped Xiao’s Tomorrow Group of its assets, which were at one point worth over $100 billion, according to his aides.

Having been burned once already, Sun took extra precautions to get his money and even his legal self out of China: Sunac is incorporated in the Cayman Islands, Sun transferred the majority of his shares to Sioux Falls and, at some point, he even secured U.S. citizenship, despite continuing to run his company’s operations in China. (Sun could not be reached for comment.)

Offshoring — the legal process of moving assets overseas to take advantage of more favorable laws and taxes — is not unique to China, of course. Both businesses and the ultra-wealthy from all across the globe have long moved their money and assets around for a variety of reasons, ranging from the reasonable desire to diversify investments to the illegal pursuit of tax evasion and money laundering. For a time, it was mostly American and European elites opening Swiss bank accounts and sheltering funds offshore. But given the tumultuous history of modern China as well as the risks of doing business and amassing wealth in the supposedly communist country, China’s business elite have become particularly interested in offshoring.

“After five years of making a lot of money, people say, this is nice. But there is a risk we could lose it all,” says Roland Jones, the CEO of Axebridge Group, a wealth management firm in Barbados that helps Chinese clients with their offshoring needs. “So they diversify their investments in terms of industry, jurisdiction, and then in order to protect themselves from future lawsuits and creditors, they may diversify some of their family wealth outside of their country.”

And increasingly, analysts say, they’re looking to the United States as the preferred destination. The tide began to turn in 2016 when the rest of the world teamed up to crack down on the tax havens and financial secrecy exposed in the Panama Papers leak. The United States notoriously abstained from that effort, rejecting reforms outlined in the international Common Reporting Standard (CRS). The result is that a host of U.S. jurisdictions from Sioux Falls to Wilmington, Delaware, are now outcompeting the British Virgin Islands, Cyprus, the Seychelles, and Samoa for their promises of lots of secrecy, little scrutiny, low fees, and in some cases, no taxes.

“What’s the safest way to keep your money away from the scrutiny of the Chinese government and U.S. controls?” said Basil Hwang, managing partner of Hong Kong law firm Hauzen LLP. “The answer is: it’s America.”

This may be seen as a surprising development given the abysmal state of U.S.-China relations, not to mention the fact that states like South Dakota are overwhelmingly supportive of Donald Trump and his policies to “decouple” from China. But just like island nations, U.S. cities like Sioux Falls profit from the offshore business and the white collar industry of lawyers and bankers it requires. “From the U.S. perspective, we’re benefiting from all this Chinese capital flooding in,” says John Cassara, a Board Member of Global Financial Integrity and former Treasury Special Agent on the Financial Crimes Enforcement Network team. “People close their eyes to this.”

‘A NEW GAME OF CHESS’

China’s business elite, however, see exactly what is happening. Every year, executives and officials from the world’s biggest offshore destinations gather at the Grand Kempinski Hotel in Shanghai to meet with Chinese lawyers, accountants, and corporate service providers and discuss how they can help Chinese clients set up companies offshore, move wealth across borders, and even acquire new citizenship.

The conferences aren’t exactly subtle. In 2018, the theme was “Into a Transparent World Comes a New Game of Chess for the Globalized,” and that year’s sponsors were the financial services association from the British Virgin Islands (BVI) and a Hong Kong firm called Vistra that helps companies incorporate overseas. Since then the governments of Samoa and the Seychelles as well as firms from Liechtenstein and the United Arab Emirates have sponsored the event, hoping to help Chinese clients outmaneuver increasingly vigilant regulators. Industry awards like “Domestic Immigration Agent of the Year” are handed out with much fanfare at a nighttime gala, and consultants boast of how they can help Chinese clients avoid taxes or establish shell companies in faraway places. Evidently, figuring out how to do business in China is itself pretty good business.

This cottage industry of offshore advisors is relatively new for China. When the country’s economic opening began roughly 40 years ago, there was little private wealth or business in the country. Deng Xiaoping, the architect of China’s economic reform, famously said that a changing economic system would let some people get rich first. But as entrepreneurs and politicians tried to do that, they quickly ran into heavy bureaucratic constraints and political controls on business and private wealth.

“China is still a socialist country. There’s a political sensitivity to saying: ‘rich people can now become very rich, much richer than everyone else, and here are the political and legal structures to support that,’” said Hwang, the Hong Kong lawyer.

China’s business environment is thus inundated with bureaucracy; regulator approval is necessary for routine decisions such as adding a board member or issuing shares. But because China still wants the business, wealth, and foreign investment that brings development, it allows Chinese companies to incorporate offshore, make money in the global capitalist system, and, hopefully, bring it back home. Some state-owned enterprises even set up offshore — meaning that arms of the Chinese state have decided that exchanging Chinese rules for offshore ones can be good practice.2The Chinese government owns its majority stake in China Mobile, for example, through a British Virgin Islands subsidiary, and China’s state-backed semiconductor champion SMIC is incorporated in the Cayman islands.

Perhaps the best example of this migration can be found in capital markets. While companies that operate inside China are obligated to register or incorporate locally, the government now allows them to have offshore affiliates and subsidiaries, which helps them attract foreign capital and acquire overseas assets. As a result, the vast majority of Chinese companies listed on the New York Stock Exchange, the Nasdaq, and the Hong Kong Stock Exchange are now incorporated offshore.3See this article on how China “supercharged the offshore market. And most of them have chosen to domicile in the Cayman Islands, a trend first established in the 1990s when Western venture capitalists and private equity firms like Carlyle Group and KKR came to China and introduced the practice. (This practice, according to Matteo Maggiori, who teaches at the Stanford Graduate School of Business, has huge implications on how wealth is measured and tracked around the world.4Professor Maggiori and a group of colleagues and scholars have published a series of fascinating papers on the topic. Some of their work is here.) Today, for instance, Chinese internet giants like Alibaba and ByteDance, as well as state-owned behemoths such as China Resources Land, are incorporated in the British territory.5Companies that are incorporated in China need regulator approval to list overseas, which is why so many Chinese companies incorporate offshore. When you buy a share of Alibaba in New York, you’re buying a piece of a Cayman Islands company that has a relationship with the Chinese operating entities.

Credit: Kmanian345, Creative Commons

At the same time in the 1990s, many people in China started moving money through Hong Kong to the British Virgin Islands, a territory that shares an English legal heritage with Hong Kong. Some of these people offshored their money for a simple, if circuitous, reason: China gave benefits, such as tax breaks and cheap land, to foreign investors, so if Chinese investors could get their money to the BVI on paper, they would get preferential treatment when they invested at home.6The M.I.T. scholar Huang Yasheng found that during the 1990s, a significant chunk of foreign direct investment in China was actually money controlled by businessmen in mainland China, and dressed up as foreign capital to take advantage of generous tax breaks. But others were motivated by fear of the Chinese government’s grip: newly wealthy Chinese worried about China seizing their assets, and people in Hong Kong worried about what would happen to their money when the British colony returned to Beijing’s control in 1997. For decades, capital flight occurred under everyone’s noses.

A key ingredient in the successful development of offshore financial centers is persuading wealthy people in developing countries or authoritarian states like China that their money is better protected offshore than it is at home. And in China, it’s been a relatively easy case to make, since the government has been known to seize assets and lock up entrepreneurs without a trial. Having an offshore account thus doesn’t have the negative connotations in China that are often associated with them in the West. They are more commonly associated with what they find lacking at home: the rule of law and protection of private property. And, perhaps more importantly, it often helps Chinese get around something Americans can hardly understand: China’s capital controls, which limit what a citizen can send out of the country to $50,000 a year.

With such strict controls, paying tuition at expensive American colleges or buying a multi-million dollar condo in New York City requires clever workarounds. The most common solution, analysts say, is to set up shell companies. Taken together, setting up offshore vehicles, holding property overseas, and even acquiring second citizenships are hedges against risk at home. “This is partly driven by wanting to have money and assets out of the reach of the Communist Party,” says Fraser Howie, the Singapore-based financial analyst and the co-author, with Carl E. Walter, of Privatizing China: The Stock Markets and their Role in Corporate Reform. “They know they’ll have better legal protections offshore, and that they won’t be arbitrarily stripped of their assets.”

But after the Panama Papers — which blew the lid off the secret offshore dealings of the world’s elite, including the Chinese elite — were published, the winds shifted. The treasure trove of millions of leaked documents from Mossack Fonseca, a law firm that facilitated corruption and criminality by setting up secretive offshore shell companies, involved many members of the Chinese political and economic elite. In fact, nearly a third of Mossack Fonseca’s business came from mainland China and Hong Kong.

Data: S&P CapitalIQ, SEC and HKEX filings

In the wake of these revelations — which also involved leaders of Iceland, Saudi Arabia and Ukraine — the international community tried to clamp down on the murky offshore world. The founders of Mossack Fonseca were arrested for money laundering and a wave of political resignations occurred across the globe. Reforms cracking down on anonymous shell companies were passed, especially in Europe, and an international agreement — the Common Reporting Standard (CRS) — was implemented in 2017 in an effort to boost transparency. Developed and overseen by the OECD, the more than 100 countries participating in the CRS system agree to automatically share information from financial firms working within their territory in an effort to curtail tax evasion and boost transparency. For China’s elites, the CRS system makes it harder to keep money out of Beijing’s view in traditional offshore jurisdictions.

But, notably, one country didn’t sign onto the CRS: the United States. In 2010, Congress passed the Foreign Account Tax Compliance Act (FATCA), which requires foreign financial firms to disclose information about assets held by U.S. citizens; the United States thus saw signing on to CRS as both unnecessary for U.S. interests and also potentially troublesome because the U.S. would have to provide information to other countries — like China. But by not joining the CRS, the U.S. decided not to reciprocate reporting, making it possible for non-U.S. citizens to store their money in the United States with no transparency.

“It is an absurd and perverse situation, that pretty much the only country in the world where you can really hide your money today is the United States,” Philip Marcovici, a wealth management consultant and author of The Destructive Power of Family Wealth, said.

At gatherings like the offshoring conference at the Grand Kempinski Hotel in Shanghai, Matthew Sumner, director of China Offshore, which organizes the summit, says he has noticed that demand in the offshore world is shifting to the U.S. because it’s not participating in the Common Reporting Standard. “The banking world has changed,” he said. “In Hong Kong or Singapore, you could easily get a bank account for a BVI company or freshly minted Hong Kong company. But because of the Common Reporting Standard, there’s so much scrutiny…it’s unlikely a new bank account could be opened for a company from an offshore jurisdiction. In the U.S., opening accounts for newly incorporated Delaware companies and Foreign Grantor Trusts is still relatively easy.”

Ultimately, wealthy individuals will go to the country that most protects their wealth, and the U.S. is currently at the top of that list. “What we have created over the last 20 or 30 years is a relatively open legal framework whereby individuals can pick and choose the laws by which they wish to be governed,” Katharina Pistor, a Columbia Law School professor and author of The Code of Capital: How the Law Creates Wealth and Inequality, said. “So they go around, or their lawyers help them go around, and find the laws that best suit their needs. People will always pick the rules that are most beneficial to them, and they will be oblivious of the harm it might do to others.”

THE SOUTH DAKOTA VAULT

Many icons of China’s economic boom, it turns out, choose to be governed by laws outside of China. Zhang Yong, a former factory worker from Sichuan Province who turned his hometown cuisine into a billion dollar hot-pot chain called Haidilao, swapped his Chinese passport for a Singaporean one. Yang Huiyan, the heir to Country Garden real estate empire and the richest woman in Asia with a net worth over $20 billion, bought herself a Cyprus passport, which gives her visa-free access to the European Union. And, of course, Sun, the Sunac founder, acquired U.S. citizenship.

Taken together, Zhang, Yang, and Sun are symbolic of China’s extraordinary economic rise. Their new passports, however, are a reminder of the inherent contradictions in that newfound economic might.

Credit: Imaginechina via AP Images

While emigrating is not a new phenomenon, the Chinese demand for foreign citizenship has gone up in recent years, according to Micha-Rose Emmett, the CEO of CS Global Partners, an international legal firm advising clients on citizenship by investment programs. “More and more people are realizing that they need to diversify their citizenships. It’s like diversifying risk,” Emmett says. “People just want to have the option of knowing that they’ve got plan B.”

For many wealthy Chinese, Hong Kong used to be plan B; it served as a reliable entry and exit point for them to take their money overseas. But the new National Security Law means the territory is fully under the grip of Beijing, and many of China’s elite fear that they — and their money — will no longer be safe there.7After Xiao Jianhua was apparently kidnapped in Hong Kong and taken back to China, his family surfaced overseas, with his wife living in Canada. Xiao held multiple passports, including one from Canada. Indeed, those with offshore wealth may have reason to worry: according to a survey of the offshore services industry, there is a widespread belief that China will significantly increase its scrutiny of funds moved offshore to international financial centers. For those unable to secure a shiny new passport, the next best thing is a strong, well-hidden vault — like a trust in South Dakota.

According to John Christensen, chair of the board of the Tax Justice Network, trusts are the foundation of complicated offshore systems. “You might have an offshore company in British Virgin Islands doing real estate, you might have a company in Luxembourg which operates a bank account in Switzerland, but all these things belong to the trust,” he said.

Take Alphamab Oncology. The Suzhou-based biotech company is owned by a Hong Kong shell, then a BVI shell, then a Cayman Islands shell — which is traded on the Hong Kong Stock Exchange — and the largest chunk of those shares, worth over $750,000,000 today, are held by the CEO’s family trust in South Dakota, in the same two-story brick building that holds Sun’s fortune.

Today, South Dakota is home to 105 trust companies. Only 10 of those were around in 2000, and the vast majority were founded in the past decade. The state gained some notoriety since its trusts allowed people to protect their money from alimony or child support payments, and soon enough, people from across America — and all over the world — turned to South Dakota to shield their money for a variety of different reasons.

Credit: Maxpower2727, Creative Commons

Now, $367 billion are held in South Dakota trusts, according to the state’s banking division, but some analysts estimate the trusts could hold as much as $1 trillion in assets since not all the assets held have clear monetary values. The South Dakota Trust Company, for example, has over 90 billionaires and 300 mega-millionaires as clients — 15 percent of whom are foreign nationals, according to its website. It is the custodian for over $160 billion in wealth, and charges its customers low, flat fees.

The Wire requested comment from local and federal lawmakers in South Dakota, as well as trust companies and administrators. All declined to speak on the record.

Despite the trusts themselves not paying state taxes, some say the industry brings real benefits to the state. The economic impact is significant in terms of good local jobs and taxes paid by the trust companies, says Tom Simmons, a professor at the University of South Dakota Law School and member of the Governor’s Task Force on Trust Administration Review and Reform, “and it’s a very clean industry compared with say, bringing a new strip miner to town.”

Others note that the flow of Chinese money to a place like South Dakota is a sign of global trust in the United States. “The irony is that, even though many people would probably conclude from newspapers that the U.S. is not friendly to China, the Chinese people still tend to think that they have confidence in the United States,” says Shudan Zhou, an associate at the international law firm McDermott Will & Emery.

But while that confidence may be rooted in the U.S.’s rule of law or stable economy, it now also includes the American veil of secrecy. Joseph Field, Senior Counsel in Estates, Trust and Tax planning at Pillsbury Winthrop Shaw Pittman LLP, says that by not participating in the CRS, the lack of information exchange in the United States, can be “an attraction for Chinese clients.”

“For practitioners, you have to be extremely careful in dealing with people who are coming to the U.S. for CRS avoidance, because it is a crime under the laws of most European countries and many others to willfully assist clients to avoid the CRS regime.”

And as a leak of U.S. government documents published today by the International Consortium of Investigative Journalists shows, over the past decade, banks have moved trillions of dollars in suspicious funds with U.S. government knowledge.

The fact that China’s global treasure map increasingly points to Trump’s America, experts say, ultimately reveals the contradictions and inequities of the larger system of global capital. “Countries are competing to attract capital by giving them all sorts of tax incentives, regulatory incentives, and subsidies,” says Christensen. With so much capital moved offshore, shielded or hidden from both home and adopted governments’ reach, capital has become “totally transnational,” he says. “And the rules of the game allowed this to happen.”

Eli Binder is a New York-based staff writer for The Wire. He previously worked at The Wall Street Journal, in Hong Kong and Singapore, as an Overseas Press Club Foundation fellow. @ebinder21

Katrina Northrop is a journalist based in New York. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. @NorthropKatrina