Tony Hisgett, Creative Commons

China’s effort to acquire resources and technology from abroad has been hampered by its economic slowdown at home and growing hostility to the country’s investments in other parts of the world. And the impact of the Covid-19 pandemic is likely to further dampen Chinese outbound investments for a lengthy period of time, analysts say.

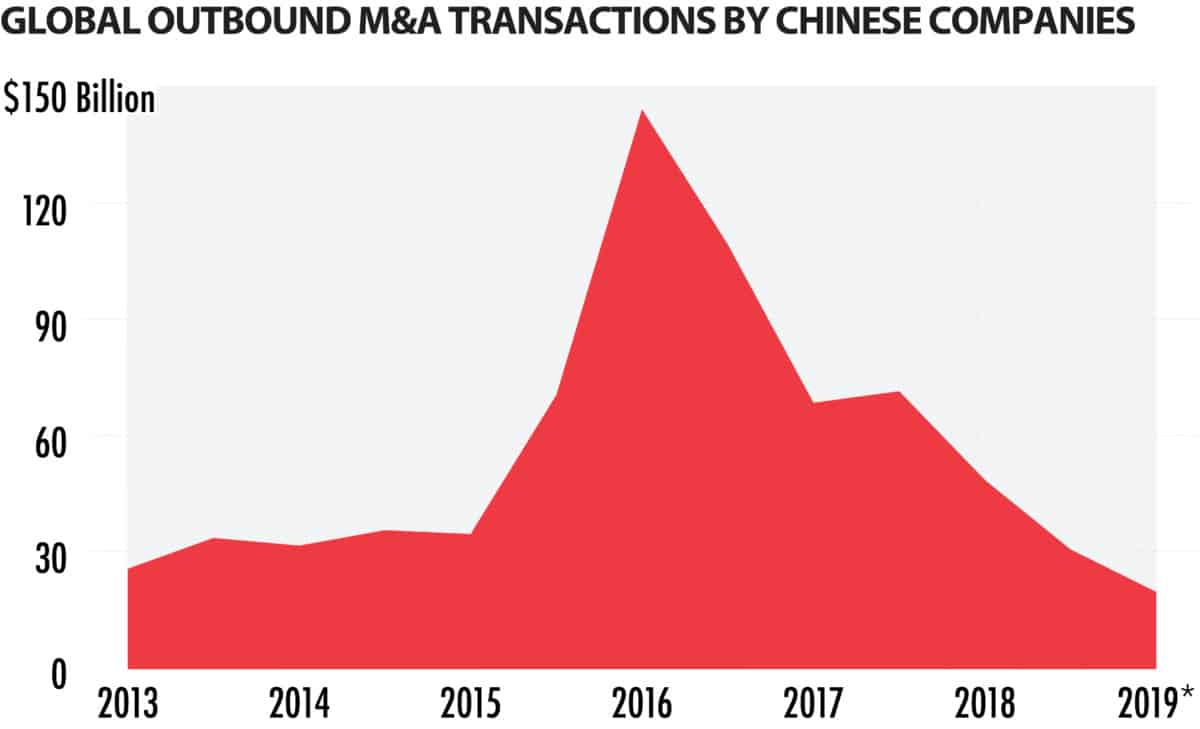

China’s global buying spree scooped up icons like New York’s Waldorf Astoria Hotel as well as stakes in Sweden’s Volvo and Wall Street’s Morgan Stanley. At its peak in 2016, outward investment crested at $196 billion. But foreign investment dropped by about 8 percent to $120 billion in 2019, according to the most recent data released by China’s National Bureau of Statistics. It was the third straight down year, signaling a major slump in the country’s overseas ambitions.

The decline in Chinese capital flowing into Europe and North America was even more pronounced, off 37 percent last year, data from the New York-based Rhodium Group showed.

“China was in the major leagues for several years, in terms of global investing, but this drop raises a question: Are they going to stay there?” said Derek Scissors, a resident scholar at the American Enterprise Institute in Washington. In the past eight months, “there hasn’t been a lot of investment,” he added.

Includes all announced M&A activity by mainland Chinese companies irrespective of resulting stake.

Data: Rhodium Group

The downturn has significant implications for the world energy markets, the pricing of global assets, and Wall Street. It’s also a barometer of China’s rise as a global power. Beijing has sought to use its money and clout to challenge American supremacy, build overseas alliances, influence regional policy, and source the energy and resources it needs to power the world’s second-largest economy.

Often backed by the government and state policy lenders like the China Development Bank, Chinese companies now own Smithfield Foods, one of America’s biggest pork processors and one of the companies hit hardest by Covid-19. Chinese firms also have a stake in Italian tire maker Pirelli, controlling stakes in a major port in Greece and a huge oil sands operation in Canada, and they operate huge construction and mining operations in Sudan, Angola and South Africa. But for the past three years, China’s deal-making has slumped.

The chill is broadly felt

Even before the global pandemic, the country’s investment slowdown was felt last year everywhere from the Americas, Europe and Australia to the dozens of countries that comprise the so-called Belt & Road Initiative, a massive China-backed program of infrastructure investment and development.

Large, outbound Chinese investment deals of at least $95 million plunged 41 percent in 2019, according to the China Global Investment Tracker, a survey of major deals by American Enterprise, a conservative Washington-based think tank. In Europe, Chinese investment fell to its lowest level since 2013, according to a study by Rhodium and Baker & McKenzie.

The drop was particularly acute in the United States. Venture capital deals involving China-based firms plummeted 51 percent in 2019, according to Rhodium, while mergers and acquisitions also dropped.

The causes were two-fold. In 2016, Beijing put new controls on outbound capital in the hopes of tempering what the government deemed to be reckless deal-making by Chinese companies, said Thilo Hanemann, a partner at the Rhodium Group. Chinese authorities worried about growing debts weighing on the country’s banking sector, and suspected that the frenzied deal-making was done partly to spirit money out of the country. China has strict capital controls on money flows crossing its border in either direction.

Then, the mood in Washington darkened and Chinese money ran into new obstacles.

The United States has long viewed China as a strategic rival for resources, technology and global influence. But after taking office, President Trump hardened America’s positions on China. He threatened, and later imposed, stiff tariffs on Beijing over trade practices; his aides accused Chinese firms of stealing intellectual property from American firms and blocking access to China’s own market. The White House also put up roadblocks aimed at preventing Chinese companies from investing in American businesses deemed essential to national security, such as semiconductors, robotics and artificial intelligence.

In 2017, for instance, the Trump administration blocked a Chinese-backed firm from acquiring Lattice Semiconductor. In early March, the White House ordered a Beijing firm to unwind its 2018 deal to acquire StayNTouch, an American software company that specializes in hotel guest data.

Amid a grinding trade war with China, the U.S. Congress in 2018 passed a law that effectively expands the power of the Committee on Foreign Investment in the United States (CFIUS) to screen foreign investments, including minority stakes, in American companies on national security grounds.

“The U.S. is worried about China’s emergence as a technology competitor,” said David Dollar, a senior fellow at the Brookings Institution, in Washington.

It hasn’t been just the U.S. that has sought to restrict Chinese investment. Australia and Canada have also moved to block Chinese investment in various sectors. European countries, including Germany and France, have grown concerned about China’s economic influence and their own industrial competitiveness, and have expanded the scope of what is legally reviewable under their foreign investment screening.

It hasn’t been just the U.S. — Australia and Canada have also moved to block Chinese investment and the European Union Commission now refers to China as a ‘strategic rival.’

The European Union Commission now refers to China as a “strategic rival.” Public opinion polls in Europe have turned negative on China, and politicians have moved to slow China’s deal-making on the continent.

In developing countries, Chinese companies completed fewer deals, too. According to data released by China’s Ministry of Commerce, Chinese companies’ direct investment in 56 countries in the Belt and Road Initiative was $15 billion in 2019, down 3.8 percent from 2018. There are indications that investments aimed at Africa, Latin America and southeast Asia may also be slowing, partly because China pumped billions of dollars into these regions during the past decade.

In Latin America, for instance, China’s state policy banks made loans of about $20 billion in 2015 to governments and state-owned companies in the region. In 2019, that figure dropped to $1.1 billion, according to a report released in March by the Global Development Policy Center at Boston University.

“Lots of countries already have lots of Chinese loans, and there’s a lot of power plants in production coming up down the line that haven’t even been done yet,” said Kevin Gallagher, the director of the policy center. “Some of those countries are undergoing debt distress, so they can’t borrow any more.”

The Chinese firms that emerged as major bidders for resources and advanced technology in the 2010s were virtually unknown in the global markets in the 1990s.

According to the United Nations Conference on Trade and Development, China’s foreign direct investment was $10 billion in 2000. By 2016, China was on par with the U.S., the United Kingdom, the Netherlands and Japan as one of the world’s biggest global deal-makers.

Licence Art Libre

In 2016 a state-owned company called ChemChina made a $43 billion bid to acquire Syngenta, the Swiss agricultural and biotech colossus, in the largest acquisition ever by a Chinese company. It gave government-run ChemChina access to one of the food industry’s most valuable assets: genetically modified seeds and technology, much of which had been banned from use in China.

By that time, Chinese conglomerates were acquiring office towers in London, landmark properties in New York City and pushing into Hollywood, with the acquisition of AMC, which operates the second-largest cinema chain in North America. The Dalian Wanda Group, which made the acquisition in 2012, even pledged $20 million to the Academy of Motion Picture Arts and Sciences — the organization that runs the Oscars — to help build a Los Angeles museum.

The AMC deal panned out poorly for Wanda, which has sold off much of its stake as streaming services and the Covid-19 pandemic have pounded box-office receipts. With its cash squeezed, AMC has been drawing down its credit lines recently as its stock fell.

Despite such reversals, China’s still-considerable holdings abroad have raised concerns for foreign governments over the exploitation of workers in developing countries, the expanded political influence that local holdings give Beijing around the world and the use of that influence as part of its geopolitical strategy.

“China is aggressive all over the place, trying to reorient the world away from the U.S.,” said Rob Rosenberg, a non-resident fellow at the Stimson Center, a Washington-based think tank focused on security issues. “Beijing doesn’t look at things from a return on investment perspective. They look at it as part of a national strategy.”

One of the Chinese government’s boldest moves was the 2016 creation of its own multilateral development bank, the Beijing-based Asian Infrastructure Investment Bank, a possible challenge to the World Bank. The government positioned the AIIB as a vehicle to engage in funneling loans to projects, many of them tied to Belt & Road and its ambitious infrastructure construction in the developing world.

Despite the current slump, China’s outsized economy and its ambitions have convinced many experts that the country will continue to be a huge global investor, particularly if it succeeds in reforming its financial system and loosening capital controls.

The short-term trend “is really hard to predict because the virus is having a big effect in China right now,” said Mr. Dollar, from Brookings. “But once you get past the virus, mostly, I would expect the long-term trend for Chinese outward investment to be up, mostly because this is still going to be an economy growing faster than the advanced economies.”

David Barboza is the co-founder and a staff writer at The Wire. Previously, he was a longtime business reporter and foreign correspondent at The New York Times. @DavidBarboza2

Shen Lu is a writer whose work has appeared in ChinaFile, the Columbia Journalism Review, The New York Times, and The South China Morning Post, among other publications. @shenlulushen