Jason Bedford is a veteran analyst of China’s financial system with over two decades of experience. He spent ten years in Beijing in auditing and financial analysis roles at KPMG before joining UBS in Hong Kong, where he led research into China’s shadow banking and banking sector. During that time he correctly anticipated the wave of bank failures that began in 2019. In this lightly edited Q&A, we discuss the role of the state in China’s banking system, its strengths, and its key vulnerabilities going forward.

Illustration by Lauren Crow

Q: You have focused on China’s banking system for many years. What got you into this area to start with?

A: What got me to China in the first place was an interview with the Canadian Embassy. I had to tell a little white lie that I was living in Beijing because they wouldn’t interview overseas applicants. So I flew out to Beijing from Vancouver. I unfortunately did not get the job at the embassy, but not too long after that I joined KPMG: they put me onto banking projects, and I then developed a deep interest in them.

If I had applied to KPMG in Vancouver, it would have been a very quick no: I have a degree in political science. But at that time, if you had some Mandarin language skills, you had a job at KPMG in China. We were perpetually understaffed in those early years. These were labor-intensive projects and audits that needed accounting skills that few people had in this part of the world. I did have some Mandarin, but where it got very good, particularly reading, was when I became aware that if I couldn’t do this work in Chinese, I would not have the job for very long. They were fun days auditing Chinese banks in the mid-2000s — it was a unique experience.

How easy is it to get the data you need to do your research, especially now you are based in Singapore?

| BIO AT A GLANCE | |

|---|---|

| AGE | 46 |

| BIRTHPLACE | Salmon Arm, Canada |

I always hear that China is opaque and information access is getting worse. There is some truth to that in the top-down data, like the youth unemployment figures. But the bottom-up data is incredibly transparent. My problem has never been a lack of information, but absorbing the amount of information in front of me: what Chinese companies publicly disclose in their financial statements always astounds me. It’s often this bottom-up data that tells you what you need to know.

To go back to basics: What are the key differences between the U.S. and Chinese banking systems?

They are very different. China’s banking system is almost three times the size of the U.S. banking system. But that’s because credit in China effectively begins and ends with a bank balance sheet. Not only is it dominated by banking, but that dominance has been increasing over time. So the vast majority of economic activity, and financing activity in the country, is purely through a bank balance sheet. If you want to understand the economy in China, you just need to understand what’s happening in the banking system.

One of the strengths of American banks is that they look at how much money is actually needed by a customer or company and then lend that amount. The Chinese bank just looks at how much collateral you can give them, and rarely asks the question “why does this small shop need such a huge loan?”

That is not true for the United States, where a minority of corporate finance comes from the banking system — the vast majority comes from deep capital markets, private credit, equity markets, bond markets etc.

| MISCELLANEA | |

|---|---|

| FAVORITE BOOK | Guns, Germs, and Steel: The Fates of Human Societies |

| FAVORITE FILM | Sin City |

| FAVORITE BAND | Radiohead |

| MOST ADMIRED | Lee Kuan Yew |

What’s the role of the state in the banking system?

China has three policy banks and then the “big six” state-owned banks. Let’s start with the Big Six [Bank of China, Industrial and Commercial Bank of China, Agricultural Bank of China, China Construction Bank, Bank of Communications, Postal Savings Bank of China]: in my experience, they have always been very commercial, perhaps excessively so. Back in the mid-2000s, in some ways China’s banks didn’t manage risk as much as they just avoided it, and over the long term that’s not a great way to run a banking system.

Credit efficiency has improved dramatically since the 2000s, but they’re still risk-averse. These big state-owned banks finance big initiatives: if the government tells them to finance real estate developers on the white list [referring to projects eligible for financial support], or refinance some local government financing vehicles (LGFVs) [structures set up by local governments off their balance sheets, which typically borrow heavily to fund investment projects], they will. But crucially, they are very risk-averse when making a loan that they know is bad, and will charge a commercial rate for it. I’m fond of saying that the Chinese banks are everyone’s best friend, because they never say no unless you ask them to lose money.

Credit: China Daily via China Development Bank

When the government wants money to go to something and it’s concerned about the commerciality of that lending, then that’s where the policy banks come in. They have these incredibly deep balance sheets which can finance a wide range of things at incredibly low costs. They also have the lowest net interest margins in the system because they lend at such incredibly low rates. But to be clear these things are enormous. China Development Bank (CDB), the largest of the three, is the world’s largest development bank and over five times the size of the next biggest development bank.

Just as a side note on LGFVs, I always hear them referred to as “hidden debts”. They’re actually quite transparent: we know how much LGFV debt is out there. They just aren’t on the local governments’ balance sheets. [Economists estimate the total amount of off-balance sheet borrowing to be 50-60 trillion yuan as of 2023, roughly $8 trillion. The government has since announced a plan to reduce “hidden debt”].

What role do regional banks play?

In some ways, regional banks are the most important banks in the country from an economic efficiency perspective. Until fairly recently, most small and medium-size enterprise (SME) finance came out of the regional banks. From my perspective, the best bank in China is a regional bank, namely Taizhou Bank [in Zhejiang province]. Equally, some of the worst banks in the country are regional banks. Many of them are in rough shape, but what you have is regions in trouble, and by virtue of that, regional banking systems that are in trouble.

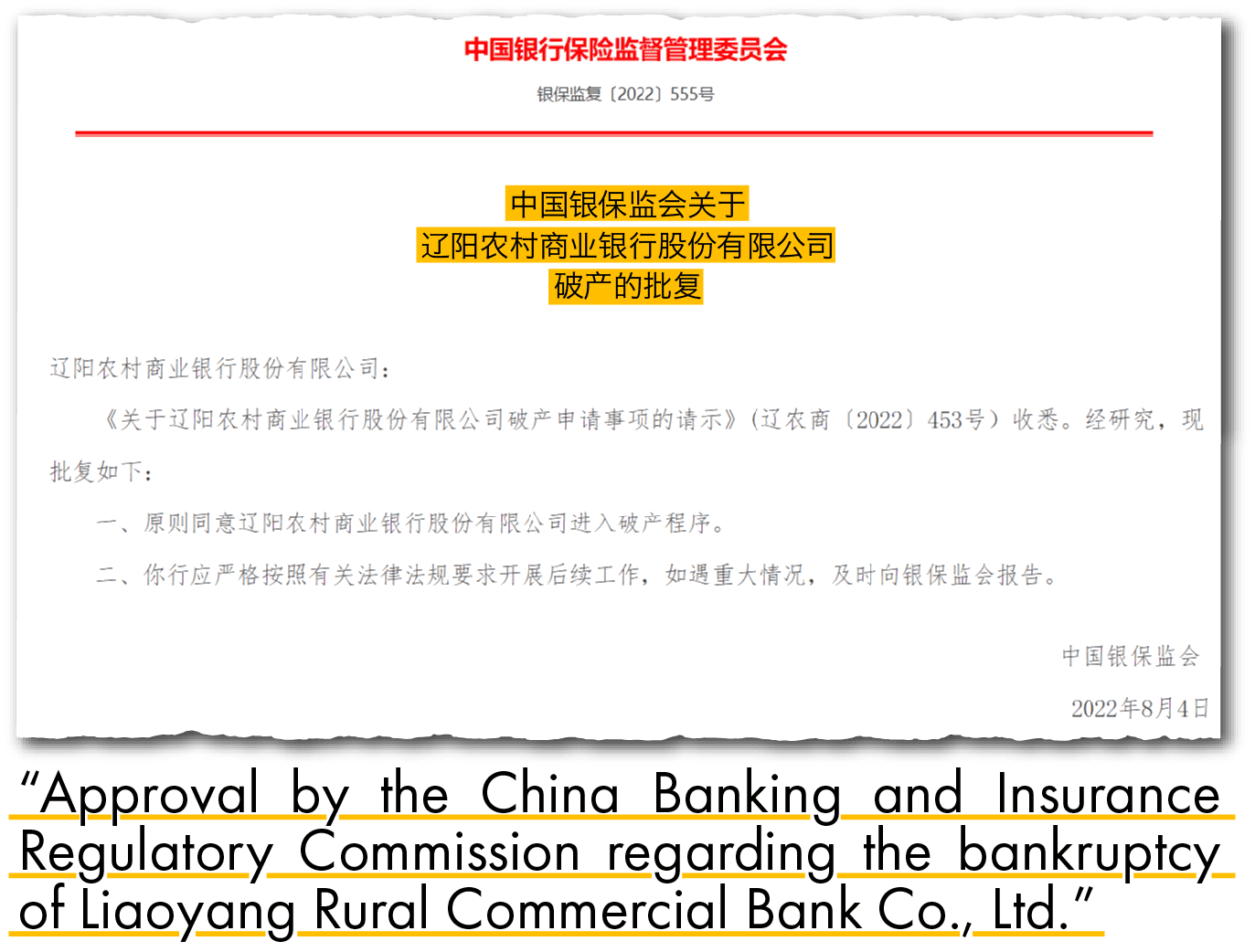

The worst example is Liaoning Province, where seemingly every single bank in the province, bar one, is either technically insolvent or undergoing a restructuring. Inner Mongolia and Tianjin are also troubled economies with highly-levered banking systems. Compare that to, for example, Guizhou. It is an economically troubled region, but you don’t have quite the same issues with the banks, because they’re small relative to the province’s GDP.

So what are the system’s major strengths and weaknesses?

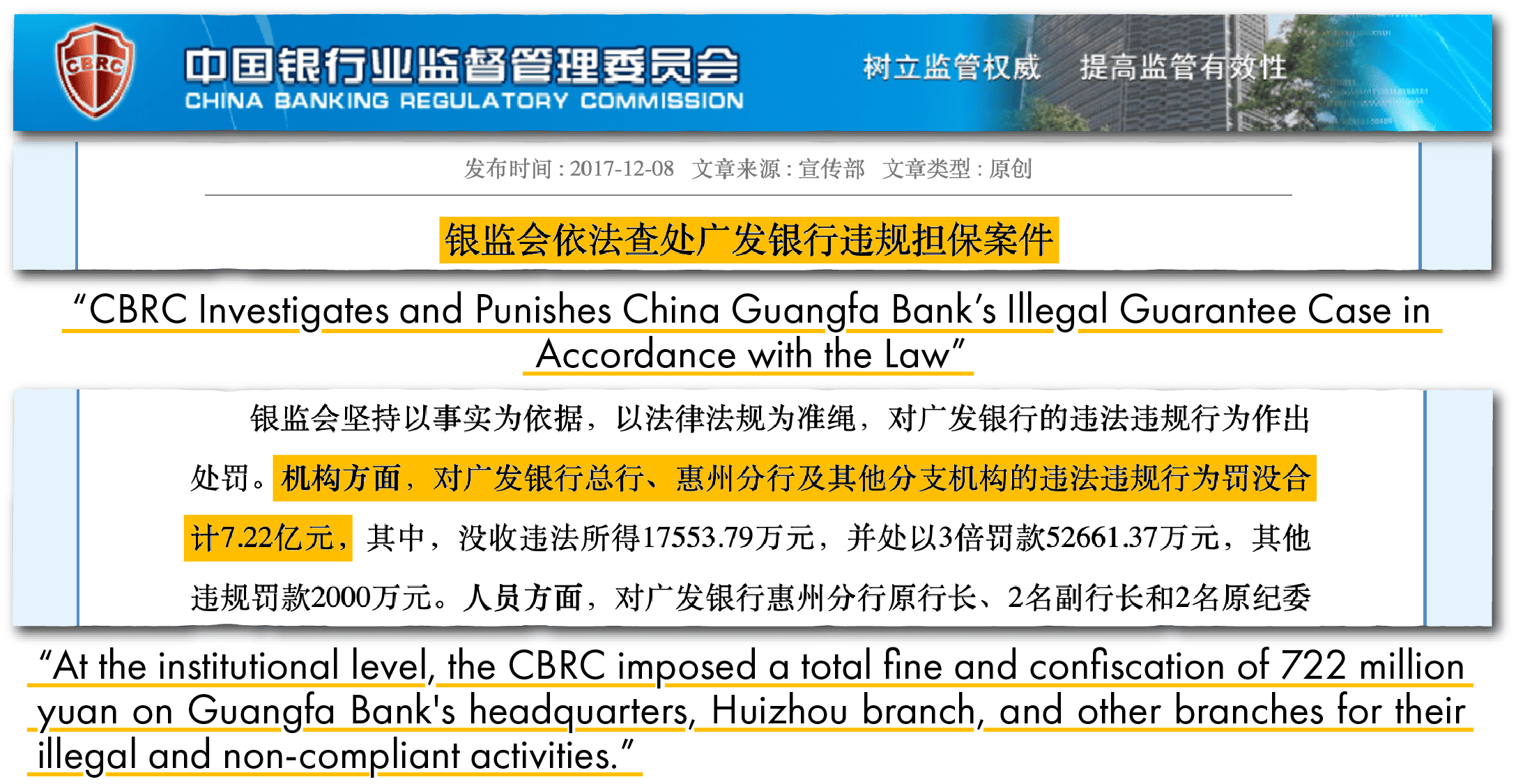

There is a very strong risk management culture, which always surprises people. The quality of the audit process with respect to banks is much better in China than it is in many other countries around the world, including the U.S.. It’s because they’re very labor-intensive audits: The banks insist on the auditors doing deep dives into their local branches, because the auditors are very good at uncovering branch-level issues, which are typically where most issues tend to occur within the banking system [for example, this fraud case in 2017].

There are still some weaknesses though. They don’t tend to do a great deal of needs-based testing. One of the strengths of American banks is that they look at how much money is actually needed by a customer or company and then lend that amount. The Chinese bank just looks at how much collateral you can give them, and rarely asks the question “why does this small shop need such a huge loan?”

The collateral management processes are very good. These institutions are not very trusting: one of the universal truths of Chinese banks is they don’t trust Chinese people. That’s why the level of collateralization in China is high, though in recent years, you’re seeing much more of a push into uncollateralized, unsecured lending, particularly for SMEs.

How does shadow banking fit into all of this?

The problem with the term shadow banking is it sounds like a terrible thing. Actually, it’s not bad in and of itself. It is alternative finance, and was incredibly important in the 2000s and the 2010s, when you still had a banking system that struggled to finance the broad economy.

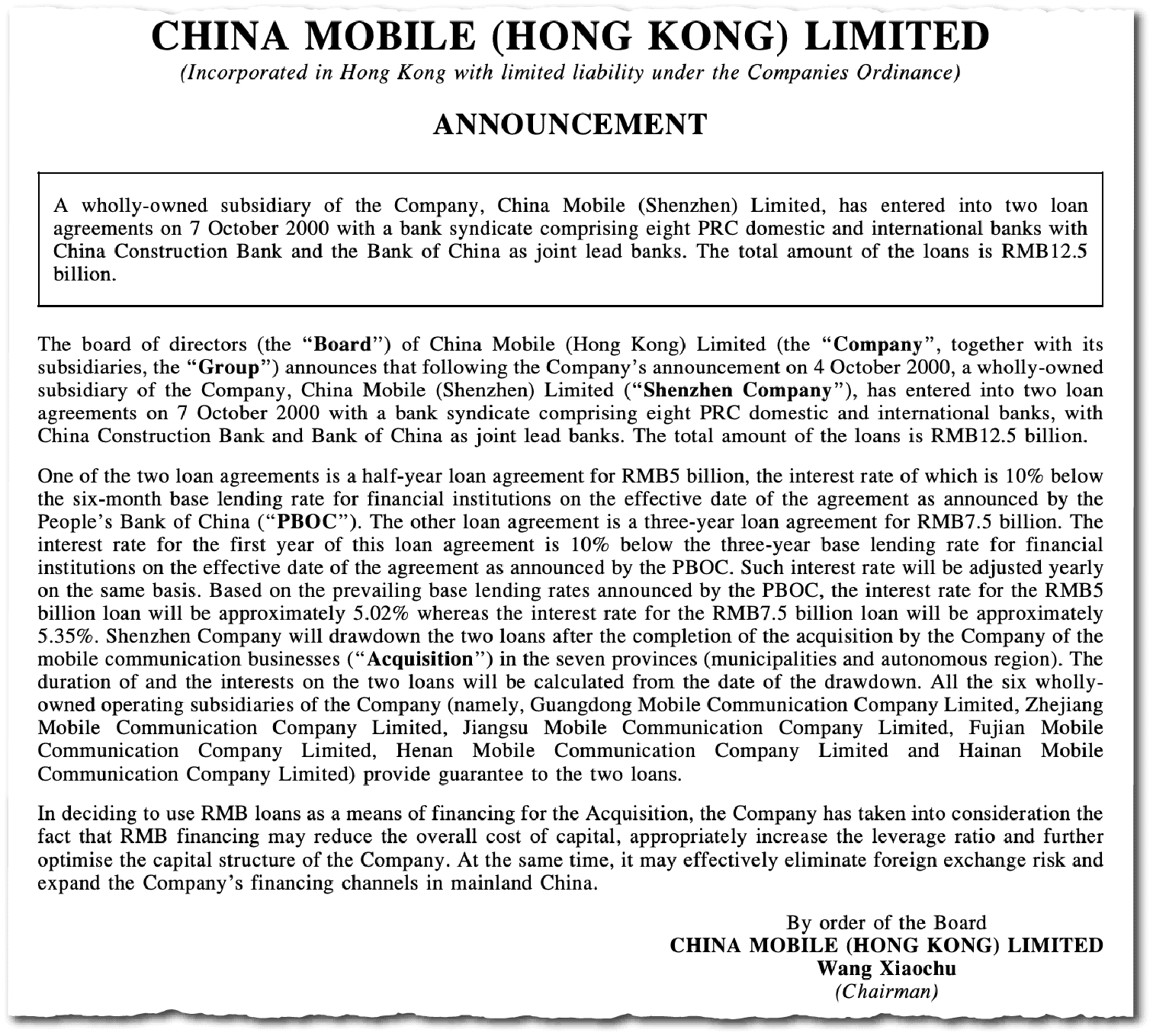

Shadow banking was, for a long time, actually encouraged in China. In the 2000s you had this situation where a major state-owned enterprise like China Mobile was being offered far too many loans by state-owned banks, but all these private, often more entrepreneurial, companies around the country couldn’t access any debt financing at all. I remember being shocked when I first arrived in China, doing due diligence and seeing these company balance sheets that were purely financed by cash flow, not debt. They couldn’t access debt when they needed it, so they went to the shadow banking system.

Back then, China had both a formal and informal shadow banking system. There was the informal network of underground lenders — pawn shops, micro-credit companies — and they would lend at crazy interest rates: sometimes 20-40 percent. Then you had the regulated shadow banking system — the auto-finance industry, the trust sector, the credit guarantee sector. These institutions are regulated, but they are not subject to the prudential banking regulations that constrain bank lending in the name of financial stability. They played a very important role in getting credit to bits of the economy that were struggling to access it. Some of their financing structures were very innovative: they would offer these structured, flexible finance terms which you could not get from a bank.

Shadow banking today is much smaller. A lot of shadow banks operated as counter-cyclical lenders, targeting industries suddenly cut off from lending. Historically, it made them outrageously profitable institutions. This time around, they lent into the deeply troubled real estate sector and got the math wrong. After the government imposed the three red lines policy for real estate [in 2020 to restrict debt among property developers], if a lender were to keep giving a ton of money to real estate developers, it didn’t end very well, and that’s why you see a lot of bankruptcies [in shadow banks]. By my estimates, nearly a third of the trust sector is likely to go under or need to be bailed out.

There often seems to be talk of a crisis in China’s banking sector, with analysts predicting some kind of collapse. Are those predictions justifiable?

I’m asked multiple times every single year when the banks are going to implode. The one year where it was a very legitimate question was in 2016. You had this incredible build-up of on balance-sheet, special purpose vehicles called trust beneficiary rights (TBRs) — products from 2012 [which used intermediaries to mask risky loans on balance sheets as low-risk investments, thereby evading a range of regulations]. They were filled to the brim with non-performing loans (NPLs), and the TBRs and similar instruments were sometimes bigger than banks’ actual loan books. It was easy for me to see that quite a number of banks were going to blow up — and they did.

Think of it this way: If I make a loan, under the rules, it becomes bad if there is no payment for 90 days or more. But back then there was no such criteria for investments. So the banks would set up these investment products into which they put their bad loans. I recall one bank where they disclosed that 87 percent of these investments were non-performing. Did that hurt the bank? Not really. When it comes to loans, banks in China are subject to very conservative rules. The issue was that these rules didn’t apply to non-loan assets, meaning there was no immediate profit impact.

What happened in 2016 is that the government reached the same conclusion as me: this banking system was in a lot of trouble. The head of the regulator was changed, and there was a big cleanup. People didn’t notice this banking cleanup, and for good reason: cleanups are typically in response to a crisis. But China didn’t do it that way, it was a proactive cleanup of the system before it could turn into a crisis. From 2016 to 2021, the banks disposed of bad debts equal to about 14 percent of GDP, according to my bottom-up research of 230 banks’ balance sheets which account for over 90 percent of the system’s assets. It’s not completely done, but the big banks and many regional banks were cleaned up very thoroughly. I think the narrative of a perpetual leveraging cycle and banks bloated with bad debts misunderstands that.

There’s a second big misconception floating around. I keep hearing about how real estate’s going to bring down the system. Now, a real estate blow-up in 2016 would indeed have been very problematic. The main problem would not have been the scale of losses on developer debts. It’s rather that so many of the loans were backed by land and property: you can’t clean up the banking system if all the collateral on the loans you’re about to dispose of suddenly becomes illiquid because property prices keep dropping.

Problems in the real estate sector that started emerging in 2021 and 2022 did hurt the banks. About 6.8 percent of their total loans went to real estate developers, according to my figures.

But my view is we don’t have a systemic threat to the banking system from real estate unless we have a threat to mortgages or if a whole bunch of property collateralized loans suddenly need to be resolved. In the U.S., during the 2008 crisis, people would often declare bankruptcy if the value of their property was underwater. That is not an option in China: there’s no personal bankruptcy. There is no way for consumers to formally expunge a debt commitment. Moreover, the system is very punitive towards defaulted individual debtors: they get placed on a blacklist that prohibits them from doing things like taking high-speed rail, reducing their social credit scores, leaving the country, etc. The result is that defaults on a mortgage only ever occur because of true inability to repay, not unwillingness to repay.

I think it’d be a pretty tough job right now to be the head of a Chinese bank. Chinese banks don’t have the right to reject deposits, so they have huge deposit inflows which they want to lend out, but credit demand has fallen.

And so when you look at mortgages, the banks’ non-performing loan levels are ticking up but still they aren’t in any real trouble. Of course, there’s also a very large amount of real estate developer debt, but it’s the offshore bond market and the shadow banking system which bear the full brunt of that [Many of China’s largest real estate developers financed themselves by selling bonds to overseas investors].

Where did these bad debts cleaned up after 2016 go? Who bought them?

Well, a lot of them were dealt with by the banks directly. The banks massively ramped up their in-house asset servicing capabilities, whose job was to chase after bad debtors to ensure repayment or sale of collateral. I remember some of my old colleagues at the Big Four accounting firms were complaining of staff shortages because people kept getting poached by bank restructuring teams. You also had reforms in the legal system, which made it much cleaner and easier for banks to enforce their rights as creditors.

So most of the bad debts were resolved. The way that a bad debt is typically resolved is that you seize collateral, sell it, take the borrower to court, and force repayments. A lot of it was done in-house. There are still some bad debts, but it’s a fraction of what it was in that peak year in 2017.

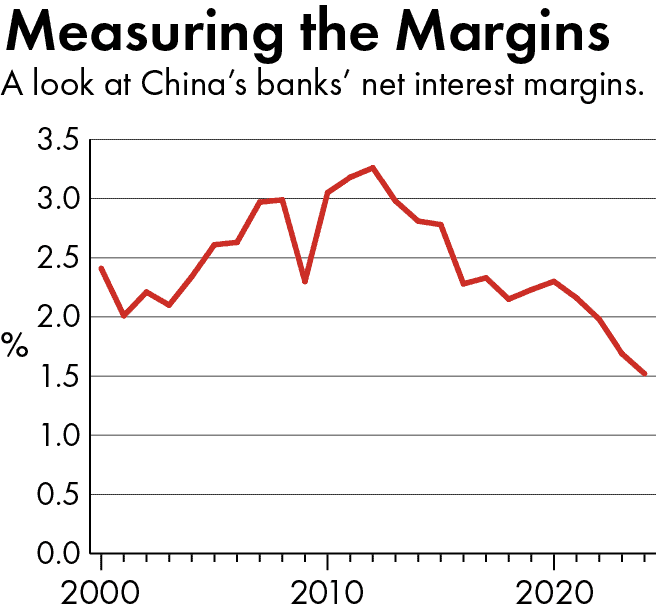

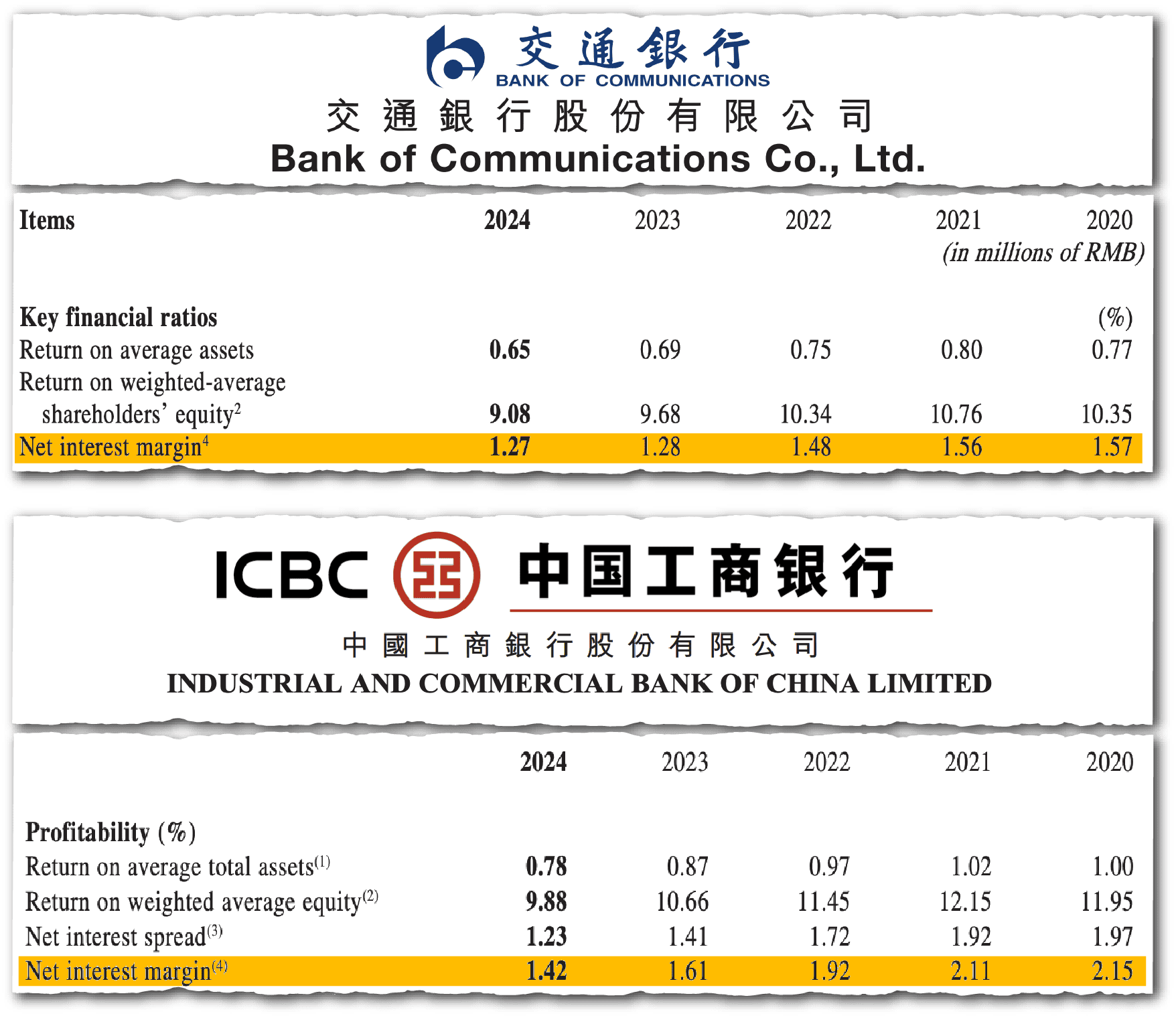

Why are banks’ net interest margins now collapsing? [This margin is a key measure of bank profitability — the difference between what banks earn on the loans they make and what they have to pay on the deposits they take in.]

That’s when I start to sound a bit more negative. Historically, China had a managed rates environment, which means when the interest rates on loans go up, the rates on deposits go up and vice versa. This beautiful fixed margin made Chinese banks incredibly profitable, especially in the 2000s and early 2010s.

But the model broke when banks started to aggressively ratchet down loan rates in response to policy pressure. Mortgage rates nearly halved while huge numbers of LGFV loans have undergone restructuring, typically for longer tenures at lower rates. There was also the ‘Two Increases’ Policy — brought in in 2018 but not rigorously enforced until the pandemic — which mandated that banks rapidly expand SME lending while perpetually cutting the rates they charge on SME loans. SME loans, in my view, are the single most mispriced asset class in China. Between mortgages, LGFV loans and SME loans, these are big chunks of bank loan books that have been repriced.

Historically what would have then happened is that the interest rate on deposits should have gone down by a similar amount [keeping bank profits at the same level]. They did fall: people weren’t really buying property and were nervous about other asset classes like stocks, so deposits just flooded into the banks. In 2016, 13 percent of net new deposits into the system were retail term deposits [fixed-term consumer deposits]: that number grew exponentially from 2022 as households became risk averse and started to pour everything into term deposits. In 2023, that figure was 66 percent. A similar thing happened with corporate deposits. Overall, in 2023, 99 percent of net new deposits were fixed-term deposits.

But the problem was the huge growth in these more expensive liabilities combined with relatively modest cuts to deposit cuts until the first quarter of 2024. The net interest margin is the gap between average interest-earning assets and average interest-earning liabilities. Fortunately, the government responded appropriately in early 2024 causing that gap to narrow.

Why is it such a problem if banks are less profitable?

The Chinese banking system is heavily reliant on interest income for its profitability, rather than fees income [which typically form a big part of the income of U.S. banks]. When you look at the capital base in the bank, historically China’s banks organically recapitalize. In other words, their profits go straight into their capital base, after they pay out their dividends.

You have a system that doesn’t like to raise capital [from investors]. Restrictions aiming to prevent dilution of state holdings in banks make it difficult for banks to raise capital in primary and secondary capital issuances. As a result, the banks have to build up their core capital from their profits.

Banks and their regulators assess whether they have enough capital using a measure called a capital adequacy ratio. It’s basically calculated by dividing the bank’s capital by its so-called risk-weighted assets — that is, its assets adjusted for how risky they are.

In China, the banks and economy are still growing, so the banks’ assets are still growing. Basic math tells us that a bank’s capital needs to grow as fast as its risk-weighted assets to keep its capital adequacy ratio at a certain level. That’s no longer happening because of the drop in net interest margin, which means the banks’ capital is growing slower in proportion to their assets. I’m even seeing some banks with net interest margins of less than 1 percent, while the system as a whole is at 1.53 percent. According to statements from the government, the system needs a minimum net interest margin of 1.8 percent to ensure organic recapitalisation of the banking system.

Capital adequacy was already quite low because of the bank cleanup after 2017. In theory, what should have happened was you had a massive rally in Chinese bank stocks [in 2021] because the cleanup was done. But the pandemic hits, and then you see this rate cycle, which is the opposite of what probably would have happened if not for Covid.

So now, who’s going to put fresh capital into the banks? Given that China’s banking system is over three times the size of the economy, it would be difficult [for the government] to recapitalize the banks. That would represent a very burdensome financing commitment. But right now there seems to be a recognition in comments from officials that the net interest margins are a problem, and that’s great.

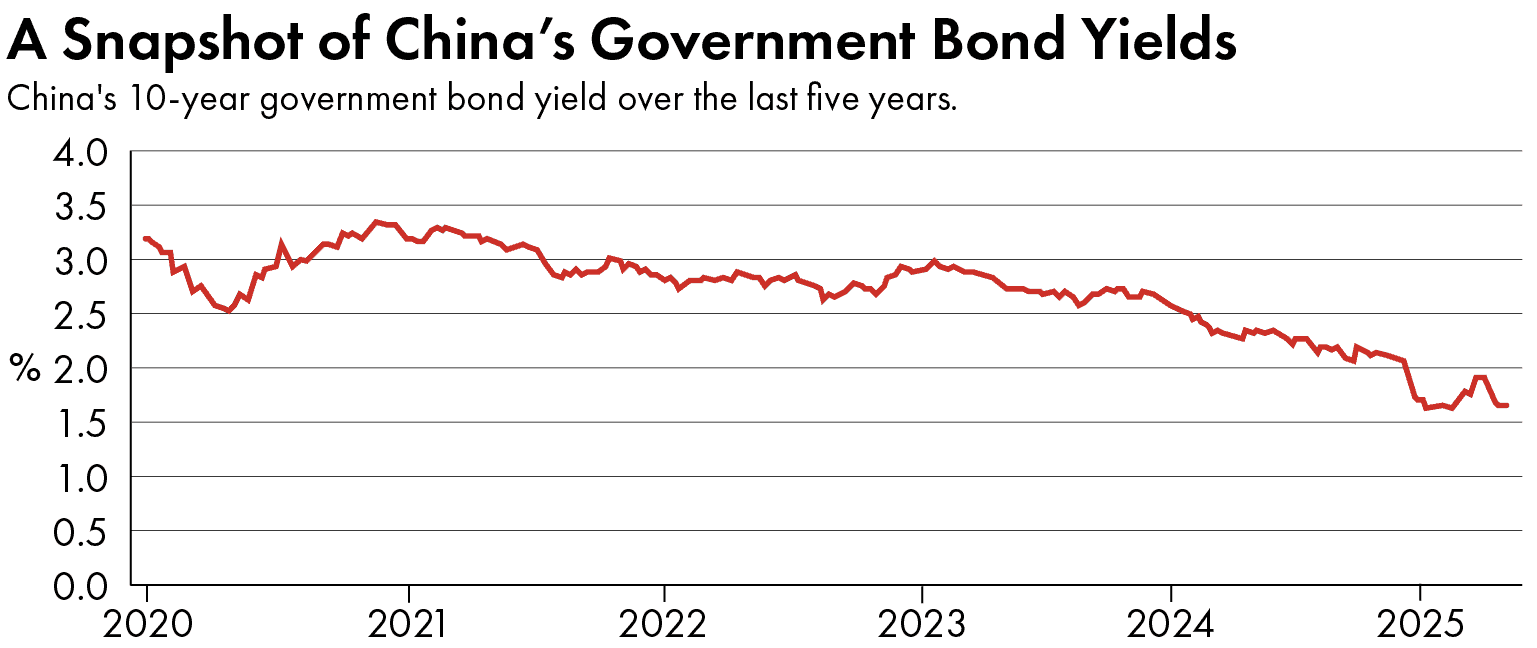

And on a related subject, what’s your read on falling government bond yields in China? [Yields have started to tick up since this interview took place but remain well below the 5 year average. Bond yields fall as the price of bonds rises].

I think it’d be a pretty tough job right now to be the head of a Chinese bank. Chinese banks don’t have the right to reject deposits, so they have huge deposit inflows which they want to lend out, but credit demand has fallen.

Here’s a figure from the banks I cover, which account for 90 percent of banking system assets. In 2016, two-thirds of all net new lending from banks went to Chinese households, mostly as mortgages. In 2023, household lending was less than 1 percent of net new loans and in the first half of 2024 it actually turned negative (about a 1 percent contraction). Households are de-leveraging, and corporate China is borrowing a lot less than before.

So what do the banks do? They start to use these new liabilities coming in to buy Chinese government bonds as quickly as they can [because bonds at least offer banks a way to earn interest].

Just a final comment, this perpetual decline in profitability is not a given. What happened most particularly in 2023, but also in 2022, was a sharp collapse in net interest margins due to a precipitous decline in asset yields (i.e. loans) without a commensurate decline in deposit rates. This NIM contraction came to an end after the first quarter of 2024, as the government made the difficult yet smart decision to sharply cut deposit rates while also trying to improve the stock market in a bid to get households to shift more of their wealth away from deposits.

However, what is ultimately needed is a rebound in NIMs, not a flatlining (assuming that China’s GDP growth is positive going forward). If they stay at the current level then bank capital will gradually be eroded and, eventually, they will need to be recapitalized. That will be painful: the banking system is nearly 3 times the size of China’s GDP.

Paddy Stephens is a freelance tech and energy journalist based in Taipei. He has written for The Economist, Financial Times, and Sinification newsletter, and is the author of The New Space Race Substack.