One of the most surprising and potentially important stimulus policies the Chinese government has announced in recent months was its pledge to recapitalize large banks using so-called special purpose bonds. While the total amount of the recapitalization has not yet been revealed, several news outlets have reported a figure in the range of 1 trillion renminbi ($138 billion). The announcement harkened back to the late 1990s when the entire banking system was struggling under high levels of bad debt. The Ministry of Finance (MoF) then issued special government bonds to boost the capital levels at China’s four largest state-owned banks — the start of a widespread and expensive banking sector cleanup that lasted for many years.

The fact that regulators would propose using this tool again was particularly surprising because, on paper, China’s large banks — such as ICBC and Bank of China — appear in good health and are not undercapitalized. According to official statistics, these banks have capital levels well in excess of their regulatory requirements, and non-performing loan (NPL) ratios are reasonable.

However, looking beyond these indicators reveals that large banks face growing pressures and that more capital may be needed to preserve financial stability. So while the plan to issue special purpose bonds might seem like a technical matter, it is effectively an acknowledgment by the Chinese authorities that behind the scenes, the system is weaker than they have to date admitted. They are acting now to prevent growing pressures within the financial system from escalating to the point of causing a systemic crisis.

Distressed Lending

The first source of pressure on large banks is directed lending to distressed borrowers. As China’s economic problems have grown, the authorities have directed banks to continue lending to troubled borrowers and industries to prevent financial disruption.

Chinese banks, eager to avoid reporting bad loans, are restructuring loans at a growing rate. While restructuring avoids recognizing a loss, it makes a bank less liquid as repayment is pushed into the future.

The most prominent example is the White List for real estate projects. Starting in January 2024, local governments across China have identified more than 5,000 different property projects to which banks are “encouraged” to lend. Many of these projects are stalled-out construction projects where the developer is in financial distress. This directed lending is intended to provide developers with the funding necessary to restart construction and complete these projects. The government has also directed banks to lend to troubled small and medium enterprises and local government financing vehicles (LGFVs).

While reported NPLs have remained low, write-offs and other methods of bad loan disposal have skyrocketed, eating into bank capital. In addition, loan restructuring is becoming more common. In one infamous example last year, banks agreed to lower interest rates and extend loans to a struggling LGFV in Guizhou province for twenty years, including no principal repayments for the first ten years.

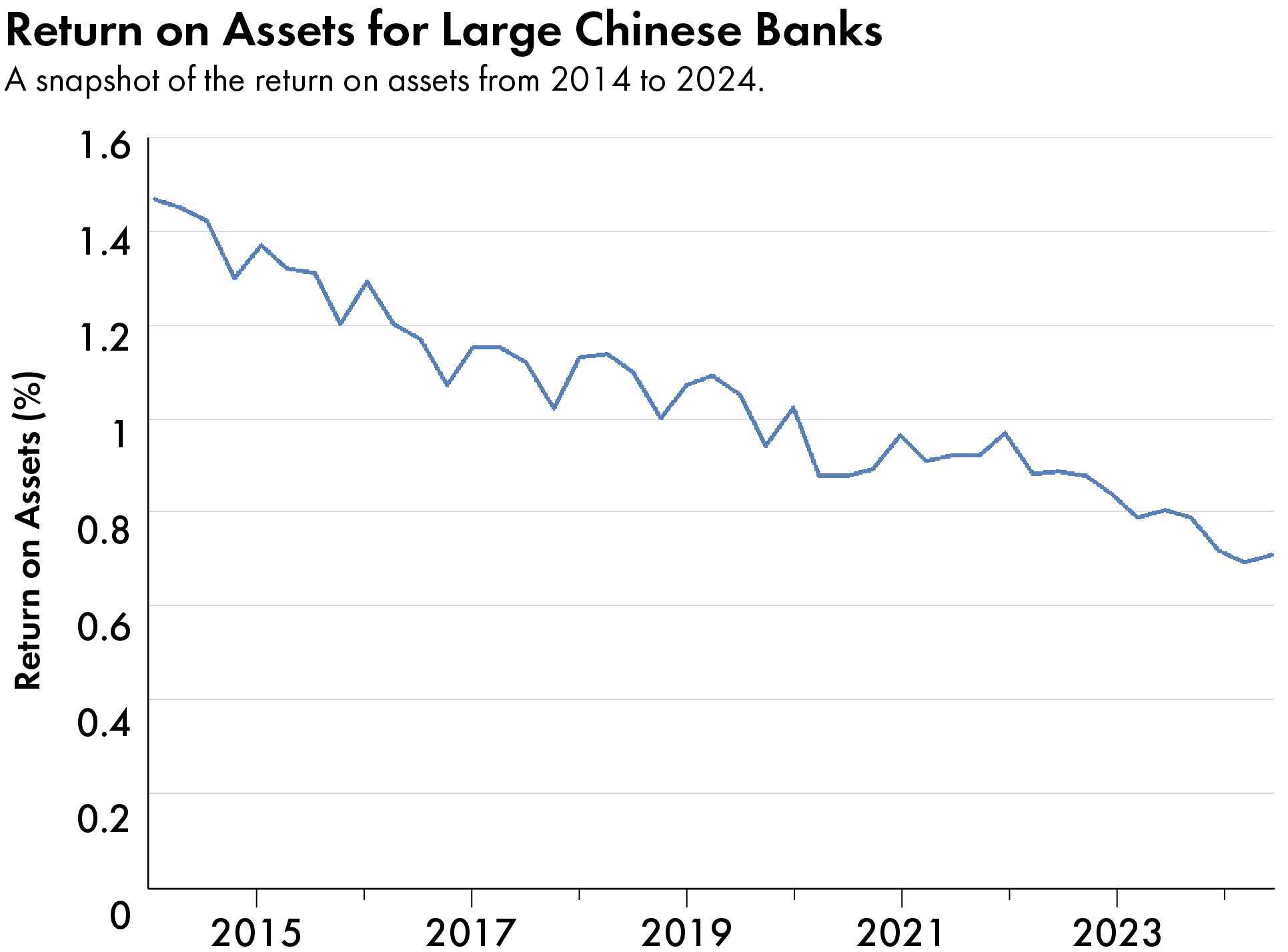

Loan write-offs, disposals, and restructurings come at the expense of banks’ profits. China’s large banks have experienced a steady decline in their return on assets over the past decade. Fewer profits means that banks have less retained earnings that can be used to bolster capital — a major reason why the MoF is now resorting to issuing special purpose bonds.

Financial Stability

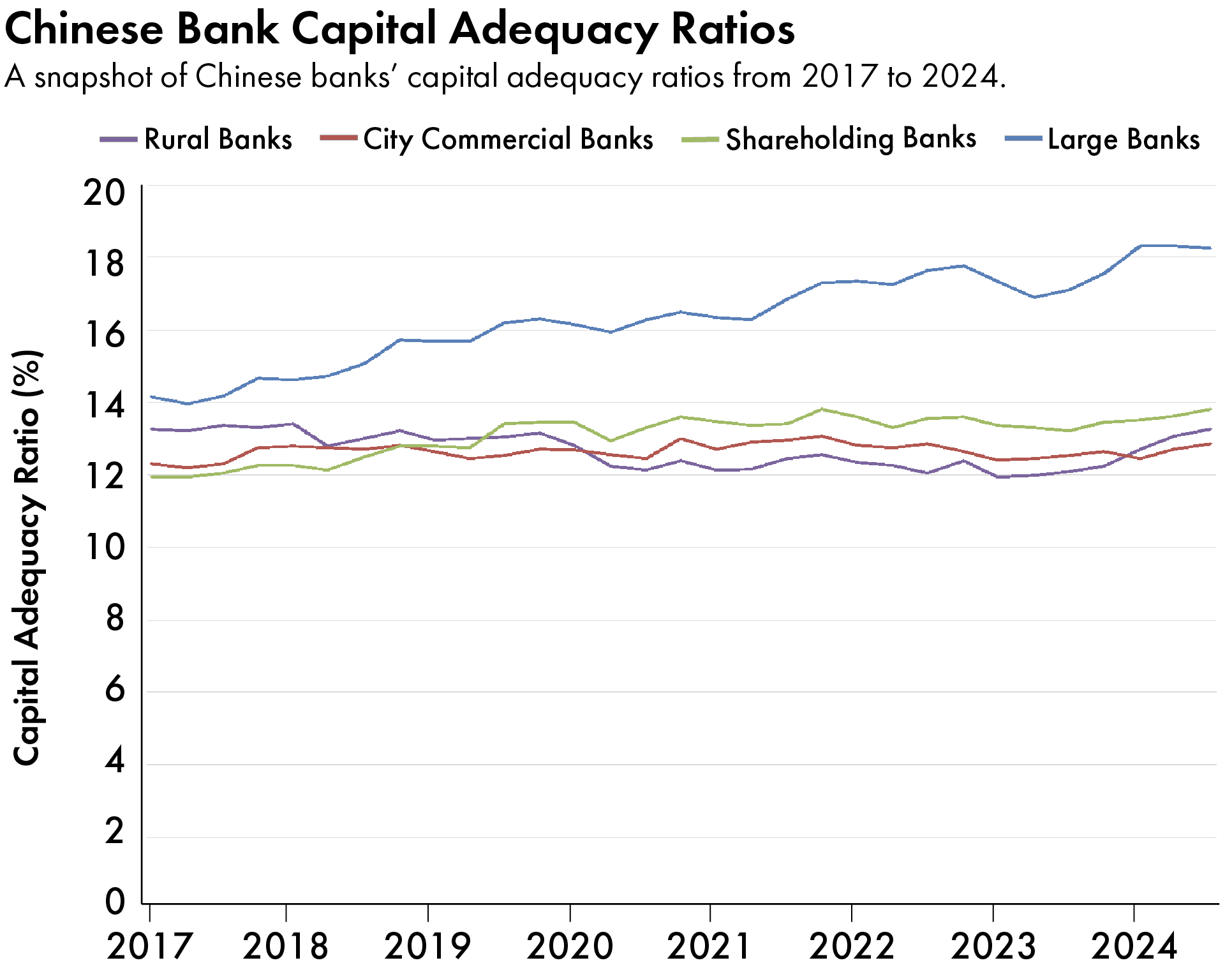

The second source of pressure on large banks is the critical role they play in preserving stability within the Chinese financial system. Since the so-called “Regulatory Windstorm” of 2016-18, China’s regulators have pushed banks to boost their capital levels in an effort to stamp out risks in the system. While large banks have increased capital and liquidity, China’s thousands of regional, city, and rural banks have not kept pace. Large Chinese banks have boosted their capital adequacy ratios by around four percentage points since 2017, in contrast to the rest of the banking system, where capital levels have remained flat.

Chinese Bank Capital Adequacy Ratios

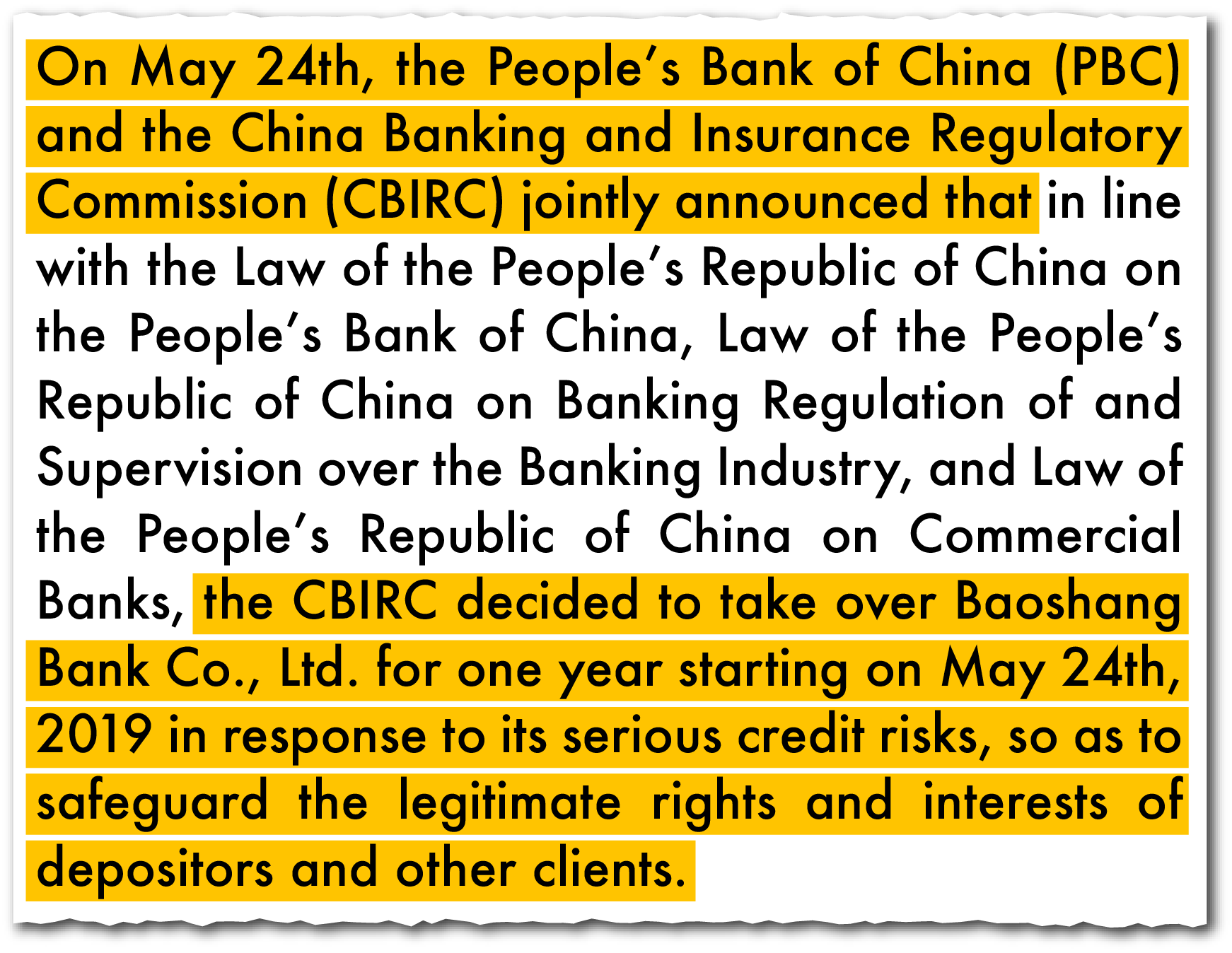

These increased capital levels are necessary, given that large banks act as shock absorbers for the rest of the financial system. They provide trillions of renminbi in interbank loans and repurchase agreements to smaller banks and non-bank financial institutions. When liquidity pressures mount within the system, such as when small banks faced liquidity shortages after Baoshang Bank failed in 2019, regulators direct the large banks to provide additional support through the interbank market.

The ability of large banks to provide this sort of support to other financial institutions is an important release valve for pressures within the system. Occasionally, large banks are called upon to use their own balance sheets to bail out smaller peers. For example, in 2019, the Bank of Jinzhou, a regional bank in northeast China, was on the verge of failure. The investment arm of ICBC, China’s largest bank, provided it with a capital injection and became its largest shareholder.

Dividends

The final source of pressure on large banks is regulatory guidance to continue paying large dividends, despite an economic slowdown and reduced profitability. One reason dividend payments have not been adjusted is that doing so would undermine a government campaign to boost share prices.

Last year, the securities regulator announced a plan calling on listed companies to pay more dividends. The motivation behind this is a belief that increasing dividends and buybacks will help boost the valuation of Chinese stocks, which sit well below other major global markets. Many of China’s banks are below the 30 percent dividend payout ratio guideline set by the securities regulator. While lowering payout ratios would ease pressure on bank capital, doing so would undermine the campaign to boost dividends. To square the circle, the government is injecting more capital via special purpose bonds into the banks, giving them more resources to keep making payouts, much of which will go right back to the government.

Liquidity Pressures

Problems at banks often first show up as liquidity pressures before becoming solvency issues. While solvency issues can be papered over through loan evergreening, liquidity pressures can appear suddenly and violently. Chinese banks, eager to avoid reporting bad loans, are restructuring loans at a growing rate. While restructuring avoids recognizing a loss, it makes a bank less liquid as repayment is pushed into the future. Over time, a bank’s balance sheet may become riddled with illiquid assets that produce no actual cash flows, even as losses remain unrecognized and capital intact in a bank’s financial statements.

A capital injection provides banks with cash, the most liquid instrument of all. This liquidity will be essential for the large banks to continue serving as a financial bulwark amid growing economic pressures.

Currently, China’s small and medium-sized banks face evident liquidity problems. These banks often have weak deposit bases, concentrated exposures to distressed borrowers, and rely on wholesale financing through the interbank market. These problems have been somewhat offset by the large banks, which serve as a liquidity backstop.

However, the growing pressure on large banks means they may struggle to continue supporting their smaller peers as their own liquidity deteriorates. Therefore, increased liquidity, rather than improved solvency, may be one of the most important outcomes of bank recapitalization. A capital injection provides banks with cash, the most liquid instrument of all. This liquidity will be essential for the large banks to continue serving as a financial bulwark amid growing economic pressures. The Chinese government’s pledge to recapitalize the banks is a welcome sign it understands the system is weaker than it looks on the surface. The next question is: has it done enough to make Chinese banks secure again?

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect Seafarer Capital Partners’ current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only, and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Seafarer does not accept any liability for losses either direct or consequential caused by the use of this information.

As of September 30, 2024 Seafarer’s client accounts did not own shares in the securities referenced in this commentary.

Nicholas Borst is Vice President and Director of China Research at Seafarer Capital Partners. Prior to joining Seafarer, he was a senior analyst at the Federal Reserve Bank of San Francisco, the China Program Manager at the Peterson Institute for International Economics, and an analyst at the World Bank. @NBorstSF