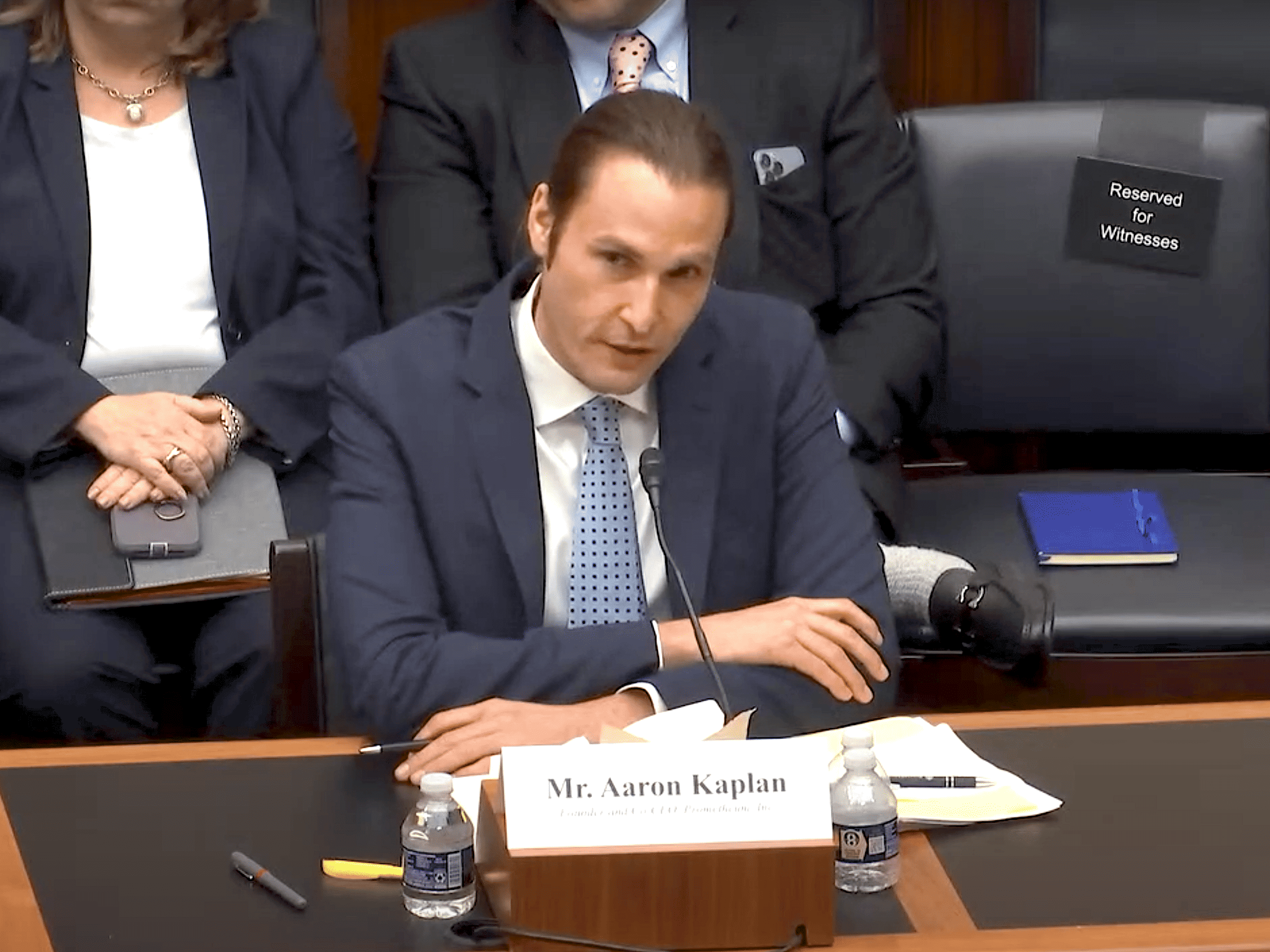

When Aaron Kaplan, the co-chief executive of New York-based cryptocurrency company Prometheum, testified in front of Congress in June, he caused quite a stir among the watching crypto community.

During his testimony, Kaplan revealed that the little-known firm, founded in 2017, had received the first license under Securities and Exchange Commission (SEC) and Financial Industry Regulatory Authority (FINRA) guidelines to operate as a digital asset securities broker-dealer. This move to effectively treat crypto currencies as equivalent to things like stocks and bonds is important for crypto firms like Prometheum, which argue that it will make it much easier for them to comply with regulators’ requirements.

Prometheum’s breakthrough isn’t the only intriguing aspect of its rise: the key role played by Chinese interests is also now drawing scrutiny from U.S. politicians and regulators. In 2018, Prometheum agreed to jointly develop blockchain technology with Wanxiang Blockchain, a subsidiary of the large Chinese auto parts manufacturer Wanxiang Group; it also received $12 million in investment from Wanxiang’s Hong Kong-based blockchain arm, HashKey Group. While the tech cooperation deal ended in 2021, HashKey still owns 19 percent of Prometheum, according to an interview Kaplan conducted in June.

The extensive Chinese involvement in the emergence of a small New York crypto firm underscores an often overlooked reality: despite Beijing’s aversion to cryptocurrencies, China has been deeply intertwined in the global industry’s rise.

“Historically, China has always been at the center of crypto,” says Zennon Kapron, the director of Kapronasia, a financial technology research and consulting firm. “And that still continues today, even though there’s not much officially happening in mainland China itself.”

You had a bunch of people in the mining world, and rather than pulling the money out of crypto, they put it into other crypto.

Tim Swanson, head of market intelligence for London-based blockchain company, Clearmatics

China has been a crypto industry hotbed since its early days. The first bitcoin exchange in China opened in 2011 — just three years after the virtual currency was invented — and energy-intensive bitcoin mining operations soon sprang up in remote Chinese provinces, taking advantage of their abundant low-cost electricity. By 2019, 75 percent of the world’s bitcoin was mined in China, according to data from the Cambridge Centre for Alternative Finance.

“There was an incredible amount of virtual wealth minted by the miners,” says Tim Swanson, head of market intelligence for Clearmatics, a London-based blockchain company. “You had a bunch of people in the mining world, and rather than pulling the money out of crypto, they put it into other crypto.”

That process spurred the creation of a Chinese cryptocurrency ecosystem. Some of the world’s largest exchanges, like Binance, Huobi and OKX were founded in China, while FTX, Sam Bankman-Fried’s firm which imploded into bankruptcy last year, was founded in Hong Kong.

Wanxiang Group, the Chinese auto parts manufacturer, entered the cryptocurrency world during this boom period. In December 2014, Xiao Feng, a Wanxiang executive and former Chinese central bank official, organized a forum on digital currencies during a conference in Hainan, where he spoke about ethereum — now the world’s second largest cryptocurrency. Afterwards Xiao — who is also a director at Yunfeng Capital, the investment firm set up by Alibaba founder Jack Ma — wrote a blog post describing that event as the “first time in China the topic of digital currencies including Bitcoin and Ether was brought up and discussed at a high-level forum.”

Just hours after his speech, Xiao received a WeChat message from a man offering to connect him to Vitalik Buterin, ethereum’s Russian-Canadian founder. Buterin and Xiao struck up a friendship, with Xiao impressed by Buterin’s “very impressive” command of Chinese, according to his blog. When Buterin was later struggling with a cash crunch in April 2015, Xiao provided a $500,000 donation in the name of ‘Wanxiang Blockchain Labs’ to Buterin’s Ethereum Foundation, a non profit which supports the blockchain. In the months afterwards, Wanxiang Blockchain Labs was officially established and Buterin became its chief scientist.

In subsequent years, Wanxiang launched several blockchain investment firms, including Shanghai Wanxiang Blockchain Company and HashKey Group, which are now known for hosting splashy crypto conferences drawing big names. One such, a Hong Kong conference in April, boasted a speaker lineup including Binance’s CEO, Changpeng Zhao, and the Hong Kong government’s financial secretary.

“They’ve been around for a very long time,” says Jehan Chu, the founder of Kenetic Capital, a Hong Kong-based blockchain venture capital firm, referring to Wanxiang Blockchain. “And they were one of the early supporters of ethereum in the Asian region.”

Wanxiang Blockchain’s crypto expansion led to its tie-up with Prometheum in 2018, with Xiao, who still leads Wanxiang’s crypto efforts, joining the Prometheum board. Wanxiang’s interest in digital currency had continued despite Beijing’s souring on crypto: The Chinese government had banned initial coin offerings (ICOs), the crypto equivalent to an IPO, in 2017. By 2021, it had halted all crypto mining or trading inside China.

Prometheum has other connections with China. Network 1 Financial Securities, a New Jersey-based firm known for bringing small Chinese firms public on U.S. exchanges and has encountered repeated regulatory issues — for failing to address potential insider trading, for example, and failing to comply with securities law — served as Prometheum’s underwriter on a private placement fundraising effort in 2021. Network 1 did not respond to requests for comment.

Those risks, around evading cross border currency controls and investor protections, are still there. So until we see that they’re a little bit more stabilized, I wouldn’t imagine that the market would open up to much more in China.

Zennon Kapron, the director of financial technology research and consulting firm, Kapronasia

Amid increased scrutiny on Chinese investment in the U.S. and worsening U.S.-China relations, such ties have started to cause trouble for Prometheum. In June, 2021, the Committee on Foreign Investment in the U.S. (CFIUS) inquired about the company’s foreign investors, according to Kaplan’s testimony. Prometheum says it has received no further CFIUS inquiries and a formal inquiry was never launched. Still, five months later, the firm terminated its technology agreement with Wanxiang: Prometheum declined to comment on why it ended the agreement.

In recent months, the firm has further distanced itself from its Chinese partners.

“Prometheum is proud to be an American-born, bred, and controlled company,” Kaplan declared in his congressional testimony, explaining that the firm does “not use any resource, code, or other assets from Wanxiang or its affiliates.” Twelve days after Kaplan’s testimony, Xiao left the Prometheum board. Prometheum declined to comment on why Xiao departed and Xiao did not respond to requests for comment.

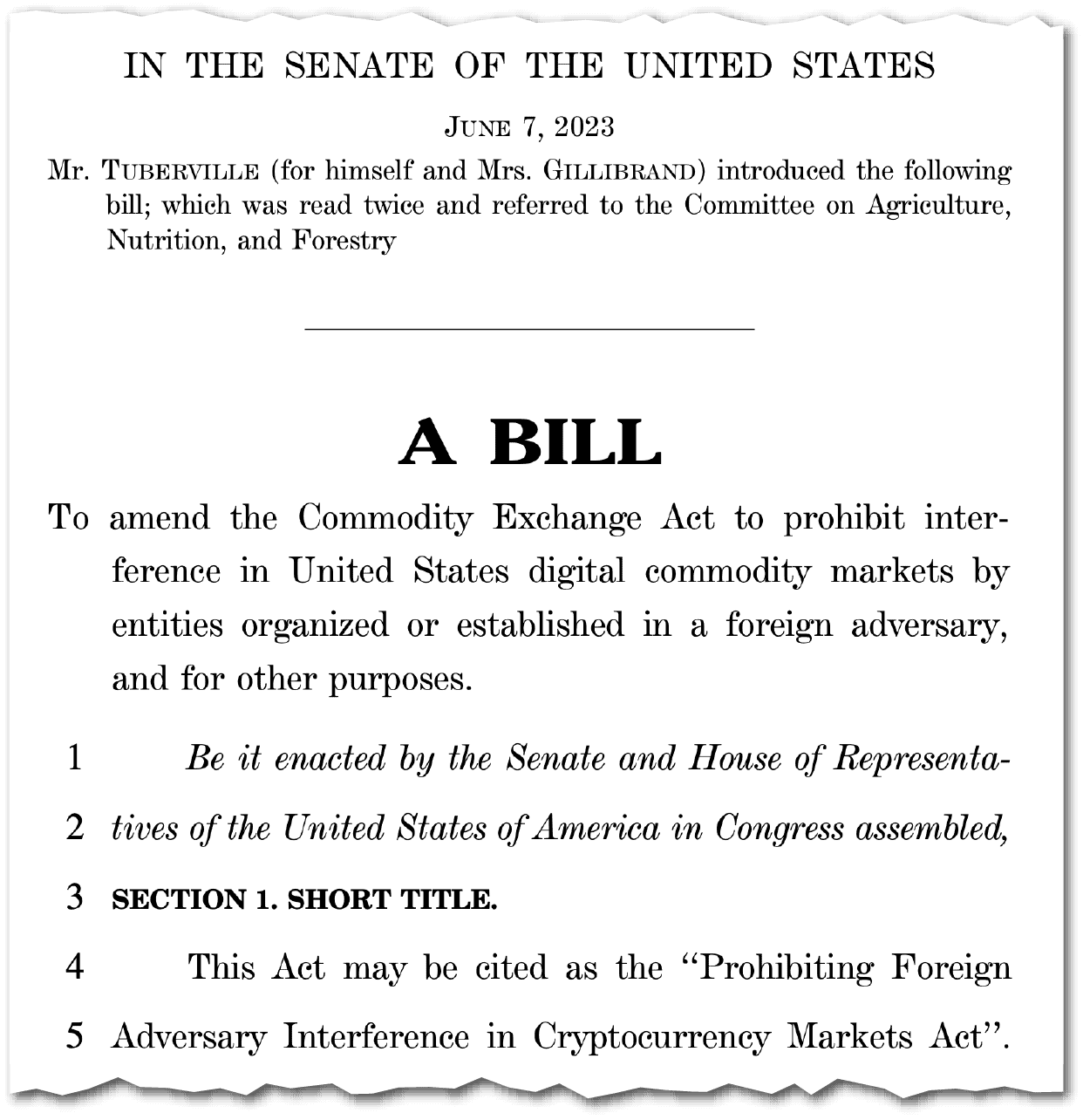

These attempts to establish Prometheum’s American bona fides have not convinced everyone on Capitol Hill. A few days before Kaplan’s testimony, Senator Tommy Tuberville (R-Alabama) and Kristin Gillibrand (D-New York) proposed a bill that would ban entities from China, and other ‘foreign adversaries’, from acquiring stakes in U.S. digital commodity companies. In a Wall Street Journal op-ed about Prometheum’s ties to China, Tuberville wrote that the legislation would “help wall off the burgeoning American digital commodity industry from Communist Party interference.”

The skepticism in the U.S. about the crypto world’s links to China has come at a point when the industry’s future in China is itself in the balance. Users in China still trade about $90 billion of cryptocurrency-related assets monthly on Binance, the world’s largest cryptocurrency exchange, making it the firm’s largest market, according to a report in The Wall Street Journal.

But some experts are doubtful that China can continue to play a central role in the global crypto industry, given the government’s continued prohibitions.

“Fundamentally, crypto was a risk [for the Chinese government] that didn’t solve any problems,” Kapron says. “Those risks, around evading cross border currency controls and investor protections, are still there. So until we see that they’re a little bit more stabilized, I wouldn’t imagine that the market would open up to much more in China.”

Katrina Northrop is a journalist based in Washington D.C. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. In 2023, Katrina won the SOPA Award for Young Journalists for a “standout and impactful body of investigative work on China’s economic influence.” @NorthropKatrina