Listen to SupChina editor-at-large and Sinica podcast host Kaiser Kuo read this article.

The roadshow kicked off on a steamy autumn morning in Singapore. Over the course of two days, CLSA, a Hong Kong-based brokerage firm, hyped up a $250 million, three-year bond deal for CEFC China Energy Co., a huge oil and gas firm.

It was 2016, and CEFC was flying high. The company was fresh off a deal to take a stake in a Kazakhstan oil and gas company and a Czech Republic-based bank, plus the company was in the process of developing a massive oil reserve in Hainan, an island province of China.

CLSA was tasked with finding investors for CEFC’s dollar-denominated bond. And during the roadshow, bankers pushed its growth story: the company had more than $40 billion in annual revenue, 30,000 employees and had been recognized as “China’s Most Influential Company” and an “Asia Excellence Brand.” The company was also portrayed as being “closely aligned with national policies,” including China’s Belt and Road projects in Africa, the Middle East and Central Asia.

Privately-held CEFC seemed to be thriving in a market dominated by state owned firms, due in large part to its political connections. During the roadshow, according to Debtwire reporting at the time, the company’s founder and chairman, Ye Jianming, was presented as the grandson of Marshal Ye Jianying, one of the founders of the People’s Republic of China and whose family was reportedly close to President Xi Jinping.

Those family connections would explain a lot. For starters, how Ye got photographed with Xi Jinping in 2015, and why he had emerged, seemingly out of nowhere, at the top echelons of the Chinese business world. In 2017, CEFC even agreed to pay $9 billion to buy a stake in Rosneft, the state-controlled Russian oil company. And Ye traveled the world to court global elites, like Hunter Biden, former CIA director James Woolsey, and Miloš Zeman, the Czech president who later appointed Ye as special economic advisor.

For CLSA, the brokerage firm underwriting the 2016 bond deal, Ye’s purported connections allowed the bank to paint an attractive picture to investors — namely, that the deal provided a unique opportunity to invest in a company with ties to China’s political elite.

“For energy companies who are not state owned, everyone knows that it requires some type of special connections,” says Chen Zhiwu, finance professor and director of the Asia Global Institute at the University of Hong Kong (HKU). “Otherwise, buying the shares or bonds offered by oil or natural gas companies who are private and with business based in China, that should mean political risk, regulatory risk, crack down risk.”

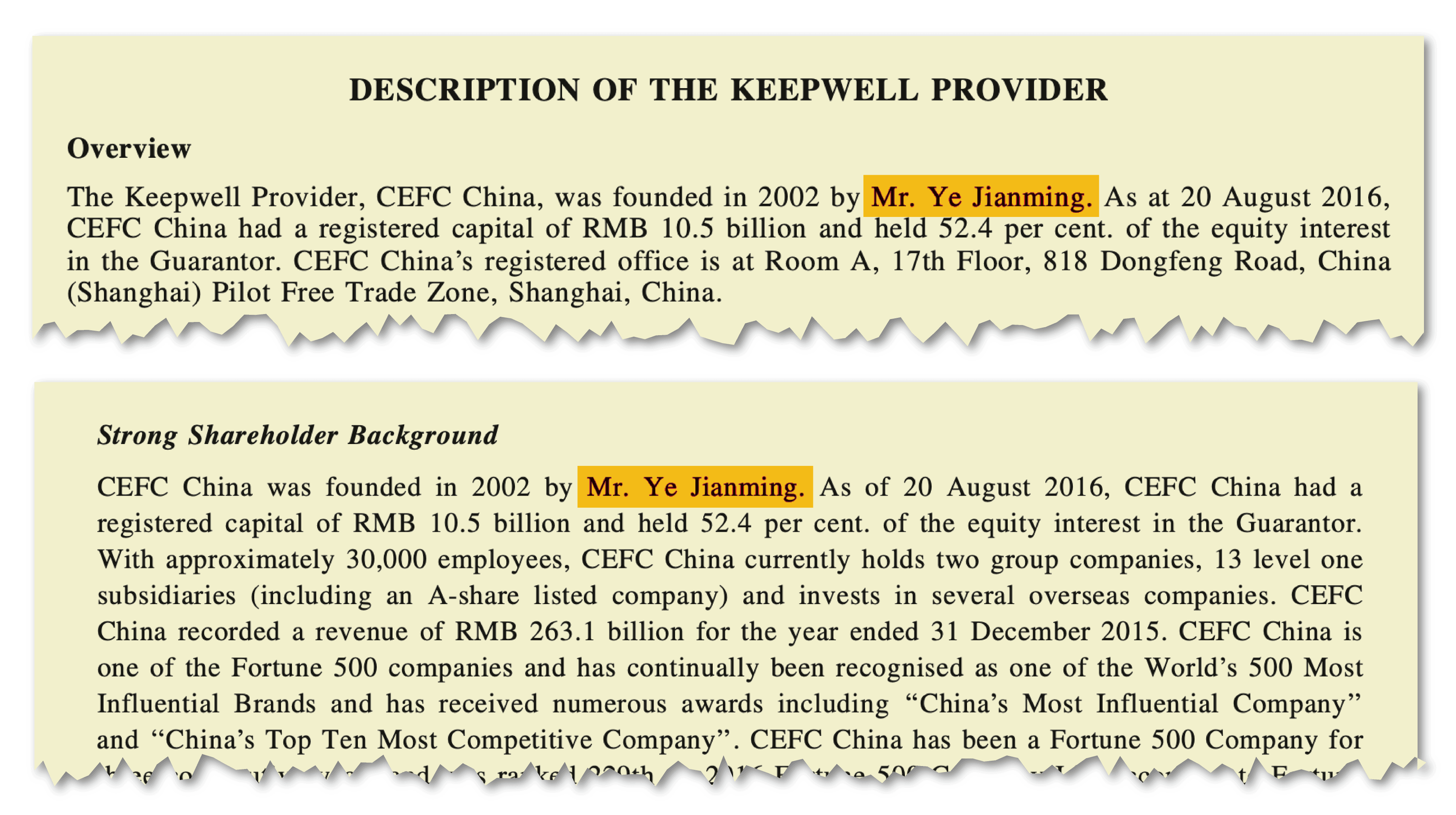

Curiously, however, CLSA, which is owned by CITIC Securities Co., whose biggest shareholder is state-owned conglomerate CITIC Group, minimized Ye’s role in the company in the bond prospectus. The Wire confirmed that the prospectus does not offer any background on Ye and only mentions him twice, describing him as the founder of the company. It does not list him as a director, supervisor or member of the senior management team.

While it is still unclear, no credible evidence has surfaced indicating that CEFC’s Ye Jianming is indeed the grandson of Marshal Ye.1The New York Times explored Ye and his background here. In fact, in 2018, Ye came crashing down in the same fashion as he rose — rapidly and without explanation. He was detained by Chinese authorities, and in the aftermath, his company, CEFC, collapsed. The bond, which CLSA had so enthusiastically marketed only two years before, went into default. Bondholders lost virtually everything.

And now, three years later, a whistleblower has emerged from inside CLSA. A senior investment banker who left the company two years ago has accused her former employer of wrongdoing, lack of due diligence and blatant conflict of interest on the CEFC bond offering. It is an extraordinary move, given that investment bankers rarely challenge their firms and publicly accuse them of wrongdoing.

In this case, the whistleblower is Kathy Liu, the former head of debt capital markets for CLSA and a longtime bond market veteran. Liu says CLSA misrepresented Chairman Ye of CEFC — both to boost interest at the roadshow and to conceal his essential role in the prospectus — and she claims this was just one element of CLSA’s fraudulent practices. After conducting her own investigation, she also alleges the firm engaged in a faulty due diligence process, bought some of the bonds itself, without disclosing that purchase to other investors, and ultimately snapped up valuable CEFC assets as the company imploded.

Liu came forward by name first in a Bloomberg News article, and has since pressed a more public campaign to get the Securities and Futures Commission (SFC), the Hong Kong regulator, to punish CLSA. Part of the reason may stem from her own interest in the deal. While at CLSA, she invested nearly $1 million of her own money in the CEFC bond offering, making her too a victim of what she calls a fraud.

The SFC should be doing an intense investigation on this. If they are not, they are not doing their job.

Andrew Collier, managing director of Oriental Capital Research

Since CLSA is owned by CITIC, Liu is now the public face of a battle that pits a former investment banker against one of China’s most powerful state enterprises. And for her, it’s not just about recouping the money she lost by investing in the CEFC bond deal; she says it’s about ensuring that Hong Kong maintains its integrity as a global financial center.

“I’ve been a banker for 20 years — I am by no means poor,” Liu told The Wire. “For me, the goal is to make sure that something like this cannot happen again in Hong Kong. I want SFC to make it clear that things like conflicts of interest or manipulation of the market are not allowed. Financial markets need to have some type of standards, like in the United States. And if the rules are not clear, I want the SFC to make it very clear.”

CLSA declined to respond to the specific allegations in this article, and instead issued a statement this week, which reads: “CLSA has been complying with the applicable laws and regulations, upholding the best international standards and putting clients’ interest as the priority of the firm. Other than this, we do not consider it appropriate to comment. The fact that we are responding only by saying ‘no comment’ should not be taken as our form of acceptance of the accuracy of the contents of your proposed article.”

The Wire was unable to independently confirm the allegations of fraud outlined by Liu, but interviews with Liu, former CLSA colleagues and others familiar with the 2016 CEFC bond offering suggest, at the very least, that CLSA may have failed to adequately disclose key details about CEFC and the investment bank’s own role in the bond offering.

Indeed, if Liu’s allegations are true, they paint a picture of fraud, conflict of interest and under the table deals: CITIC using CLSA2CITIC Securities merged its international business with CLSA around the time of the deal and some of the bankers signing off on the CEFC deal were originally with CITIC Securities International, or CSI. — its Hong Kong investment arm — to raise money for a shadowy and ultimately doomed company, and then making out with valuable assets in return after CEFC collapsed. Liu and three other bond holders have filed complaint letters to the SFC. It’s unclear, though, whether the Hong Kong regulator has opened an investigation into the deal. (The SFC, as a practice, does not comment on the existence of ongoing investigations.)

“The SFC should be doing an intense investigation on this. If they are not, they are not doing their job,” says Andrew Collier, managing director of Orient Capital Research and the author of Shadow Banking and the Rise of Capitalism in China. Yet Collier and other analysts also say they doubt the SFC will actually take action against CLSA because of mainland politics.

“CITIC is a powerful organization,” Collier notes. “And SFC doesn’t want to get involved.”

Given the lack of regulatory action thus far against CLSA, analysts say Liu’s allegations also tell the story of how Hong Kong’s financial system is increasingly at the mercy of Beijing.

Credit: Lucie Mikolaskova (CTK via AP Images)

ALLEGATIONS OF A “BLATANT SECURITIES FRAUD”

Kathy Liu says she paid $950,000 to purchase bonds from the CEFC offering on the secondary market in March 2017. She made the purchase privately, using her own broker, outside of CLSA. She had not attended the Singapore roadshow and she knew almost nothing about Ye Jianming or CEFC. Liu says she was busy, had some cash laying around and heard from a colleague that it was a good bond, so she invested.3Though investment bankers are often restricted by conflict of interest rules from purchasing stocks or bond offerings when their own bank is the underwriter, Liu says the CEFC bond was not on the restricted list and that she got permission from a superior to make the purchase.

“At this time, this bond was publicly traded, so there’s no insider information,” she says. “There is no particular reason why I bought it. It was a big Chinese oil and gas company so I thought it was pretty safe — nothing out of the ordinary, no warning sign of any sort. And I trusted my team. I always thought that we had pretty high standards.”

But a year later, in March 2018, Ye disappeared from public view and was arrested. Liu says she didn’t pay much attention to his disappearance, but she noticed when the CEFC bond price started going down. By May, it had cross-defaulted, and Liu started to realize she was out a million dollars. The loss stung — Liu says she was “kind of depressed for a long time” — but still, she saw it as a bad investment, her own bad decision.

Credit: CEFC prospectus

“By that point, I knew something was wrong with the company, with CEFC. But I didn’t know something was dodgy with CLSA, with the underwriter.”

That is, until CLSA held a company retreat at the end of October and Liu happened upon some company gossip.

After a long dinner at an elegant seaside resort in Hong Kong, Liu says she was walking with two other managing directors at the company. The women were chatting about life, work, and religion when Liu decided to ask one of her companions, who was involved in due diligence on the CEFC deal, how she came to approve the deal. The woman, according to Liu, replied that she hadn’t signed off on it, but the deal went forward anyway.

“I was completely shocked,” says Liu. “That has never happened in my seven and a half years at CLSA, or even in my entire banking career — that the responsible officer of the deal could be overridden by her boss.”

At that point, Liu realized that CLSA may have known that CEFC wasn’t a solid company even at the time of the bond issuance, and still went forward with the deal. She asked around, probing different colleagues for answers, and started to receive curious answers.

Prior to that, Liu says she loved her job at CLSA. The Hong Kong-based firm4CLSA began as an Asian investment arm of the French banking giant Credit Lyonnais had been founded by two former journalists and was famous for incisive research and wild investment conferences with unlikely celebrity guests like Sarah Palin and Rihanna.5CLSA stands for Credit Lyonnais Asia Securities. Liu joined CLSA to head up debt capital markets after CITIC bought the firm in 2013. At one point, she was earning a base salary of as much as $320,000 before her bonus. Previously, she had worked for Citigroup for nine years and China International Capital Corporation (CICC), a Chinese investment bank, before becoming the head of fixed income syndicate for CITIC’s Hong Kong office.

CLSA was an unlikely target for CITIC, the staid state conglomerate. Cultures clashed, and much of the senior management eventually left the company over disputes on issues such as corporate strategy and bonus sizes. But regardless of the changes afoot, Liu says that she enjoyed working there and had no issues with the firm. She’s never seen herself as a particularly ideological person. After getting a doctoral fellowship to the Massachusetts Institute of Technology, Liu says she switched her PhD from political science to management of technology because “a lot of people want to do Chinese political science and criticize China. I was reluctant to do that.”

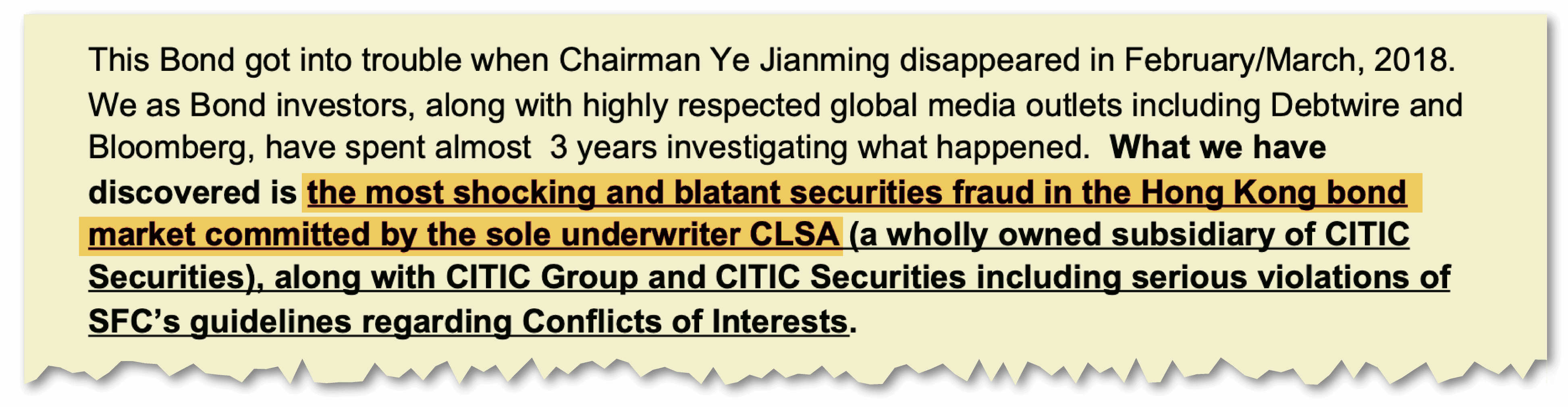

For a while, investment banking seemed like her calling. But after she learned more about the CEFC bond deal, Liu says she started to feel like Erin Brokovitch, the environmental whistleblower played by Julia Roberts in the eponymous movie. She joined forces with three other bondholders, who are all senior bankers in Hong Kong, and on January 13 of this year, she filed a detailed and exhaustive complaint letter to the SFC. Taken together, Liu says the CLSA-CEFC deal represents “a shocking sequence of blatant securities fraud.”

Credit: Complaint filed to the SFC, courtesy of Kathy Liu

First, Liu alleges that CLSA engaged in misrepresentation in the marketing of the bond. While spreading false rumors about Ye’s background at the roadshow to boost interest, as corroborated by Debtwire’s reporting, CLSA also minimized Ye’s role in the company in the bond prospectus. On both fronts, according to Liu, this misled investors and omitted material facts, which may have influenced investors’ decisions.

She also claims there was a failure of due diligence on the part of CLSA. According to Liu, the woman in charge of the deal’s due diligence did not approve or sign off on the deal, citing the fact that more than 50 percent of CEFC’s assets were receivables, and not tangible assets, which Liu says is often a sign of corporate fraud. But despite this red flag, according to Liu, the deal was pushed through. The Wire was not able to independently confirm that the CLSA employee initially did not sign off.

Next, after CLSA agreed to market the bond, according to several people who worked in senior roles at CLSA at the time, the firm ended up buying 40 percent of the bond themselves — and never disclosed it to the public.6Liu claims CLSA and CSI, a division of Citic Securities that was being integrated into CLSA, together acquired a big slice of the bond offering. This allowed the company to conceal the fact that there may have been little interest from investors in buying the bond, and to maintain interest while it traded on the secondary market. If this had been disclosed, Liu and other bondholders say they would never have bought the bond.

“CLSA failed to disclose to the market that the order book only covered 60 percent [of the bond offering],” says another former CLSA executive familiar with the CEFC bond offering. “Why? They purposely did it.”

For mainland investment banks [like CITIC Securities], such practices — relying on relationships and side agreements — are very common. Now, they have brought that practice to Hong Kong.

Chen Zhiwu, finance professor and director of the Asia Global Institute at the University of Hong Kong (HKU)

Liu — the whistleblower — also believes CLSA pushed the bond offering as a favor to CITIC, which had developed a relationship with Ye Jianming and CEFC.7In 2016, CEFC Hong Kong agreed to buy a 15 percent stake in CITIC International Asset Management. While it is impossible to know exactly what happened between the two powerful Chinese companies, Liu alleges that after the bond defaulted, instead of protecting the bond holders, CITIC, CLSA’s parent company, grabbed up valuable CEFC assets in the Czech Republic and CLSA made a side deal with CEFC that disadvantaged bondholders. That side arrangement meant that a unit of CLSA bought back a stake in CITIC International Asset Management from CEFC, and Liu claims that CLSA intended to use defaulted CEFC bonds as payment for that deal.

CITIC did acquire assets from CEFC in 2018, but The Wire was unable to determine whether there was anything unusual about the transactions, or whether CITIC may have used the bond losses to better position itself to acquire the assets. But Chen Zhiwu, the former Yale University professor now at Hong Kong University, says something like this was destined to happen after CITIC agreed to purchase CLSA in 2013.

“When the takeover took place, I thought at the time that the two cultures would not merge well. I thought that the clash would manifest in some bad deals,” he says. “For mainland investment banks [like CITIC Securities], such practices — relying on relationships and side agreements — are very common. Now, they have brought that practice to Hong Kong.”

BACKROOM DEALINGS

Many observers say that shady deals are increasingly common in today’s Hong Kong, partly because the SFC has been reluctant to show its teeth. The regulator is an independent body — distinct from the Hong Kong government — but its board and chairman are appointed by Hong Kong’s Chief Executive, and analysts say it is mindful of the mainland’s regulatory system.

“They wouldn’t do anything that Beijing doesn’t like,” says Johannes Petry, a research fellow at SCRIPTS Cluster of Excellence in Berlin, where he focuses on Chinese financial markets. Petry points to the example of Luckin, the Chinese coffee company that was embroiled in scandal last year and ended up being delisted from Nasdaq. “The same thing probably wouldn’t happen in Hong Kong, in terms of delisting and scrutiny,” Petry says. “Hong Kong is turning from a global financial center to a much more Chinese dominated one.”

But while the CLSA bond deal is unique in highlighting this change, analysts say it likely won’t amount to much. For starters, it’s difficult to prove illegality, especially in the bond markets, which are generally far less regulated than the equity side. After all, most bond holders are professional investors — like Liu — who are not as easily exploited. Indeed, some say Liu should have looked closer at CEFC before investing.

“You have to begin with the idea that whatever harm was done to her, she participated by her negligence,” says Edward Kane, a finance professor at Boston College’s Carroll School of Management and former president of the American Finance Association. “It is her money, she is supposed to take care of it.”

Credit: Ged Carroll, Creative Commons

Those with extensive experience in the Chinese securities market say that the legal bond documents for Chinese companies are often ambiguous — if an investor isn’t comfortable with that, they shouldn’t buy the bond. And some say that even the other allegations, including falsely marketing the bond and not disclosing that they bought 40 percent themselves, can be interpreted as reckless, but some say may not necessarily be against the law.

Still, legality aside, many analysts say that professionalism matters for financial institutions.

“Reputation is one of the safeguards for investors. Maintaining a good reputation is one of the ways banks compete with one another,” says Kane. “So one would figure that CITIC, one of the top banks in the world, wouldn’t screw the customers as badly as this deal did. They not only screwed them going in, they screwed them when they took a position and unloaded responsibility for the losses.”

While the ultimate goal of Liu’s campaign is to get the SFC to punish CLSA, she also says the biggest takeaway from the case is that a large conglomerate like CITIC shouldn’t be allowed to own an investment bank like CLSA. In the U.S., although an industrial conglomerate could technically acquire an investment bank, it is an extremely rare arrangement and regulators would likely limit its activities. In 1986, for instance, General Electric acquired Kidder, Peabody & Co., but after the firm ran into financial difficulties and insider trading scandals, they sold it off only eight years later.

“With investment banks doing this underwriting, there are all sorts of conflicts of interest,” says Andrew Winton, a finance professor at University of Minnesota’s Carlson School of Management. “And it gets worse if you are owned by a company with its fingers in many pies. There is always room for conflict of interest, but if the owner is a conglomerate with lots of different businesses, that increases the chance.”

One would figure that CITIC, one of the top banks in the world, wouldn’t screw the customers as badly as this deal did.

Edward Kane, a finance professor at Boston College’s Carroll School of Management

For Simon Chen, one of the bondholders and a former senior banker at HSBC and Lehman Brothers, the CLSA saga shows how secretive the Chinese markets can be, with companies continuing to engage in backroom deals.

“I came back to China to make a transparent economy,” he says, describing how he went to study business in Canada before coming back to Hong Kong and Beijing when Chinese firms were first beginning to list on overseas exchanges. “So I feel very personal about this. I have a vision for what China should become: open and transparent. I play a very small role, and some investments are bad, some are good. But I was manipulated. These people did very bad things.”

Chen has signed on to Liu’s complaint letter with the SFC, and says he hopes the story of the CLSA-CEFC bond will “turn the rock upside down and let the public see what is happening.”

That, in the end, is what Liu hopes to do as well. After leaving CLSA in 2019 in a round of restructuring, she is now pursuing an advanced degree in clinical psychology. But in any time not spent studying or caring for her daughter, Liu works on bringing attention to what she perceives as CLSA’s gross wrongdoing.

“Why am I doing this? Why am I making so much noise and putting myself out there,” Liu says. “Because I’ve reached the stage that I know enough to say there is a right, and there is a wrong. And I feel like something is truly wrong, and it’s not getting corrected.”

Katrina Northrop is a journalist based in New York. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. @NorthropKatrina