The secret operation got underway late last year. A small army of researchers were told to fan out across China, to cities big and small, to collect documents and videotape the activities of the prime target.

The organizers had a hunch that Luckin Coffee, China’s fast-growing challenger to Starbucks and a company traded in the U.S. stock market, was falsifying financial statements to exaggerate its sales. The organizer set out to prove it, deploying 1,510 investigators to count sales and record traffic at more than 600 of the company’s retail stores, one mobile phone video at a time.

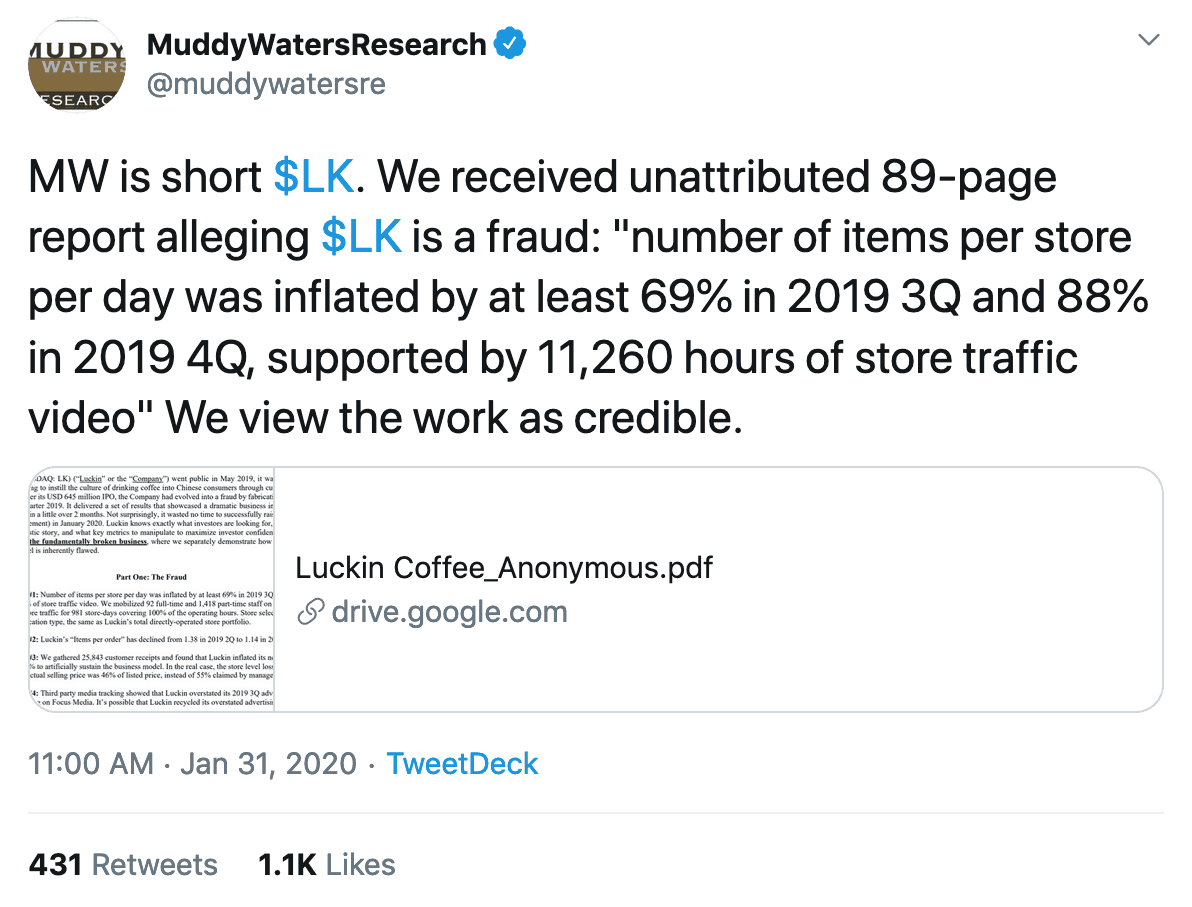

A few months later, an anonymously written 89-page report landed on Wall Street and leveled one of China’s hottest startups. A pack of short-sellers — who backed the report’s harsh conclusions — pounced. They positioned themselves to profit from a collapse in Luckin’s stock price and began releasing more allegations of fraud, staggering the company just as the world was going into lockdown over the Covid-19 pandemic.

Caught in the maelstrom were some of the world’s most sophisticated banks and investment firms, including the Capital Group, Credit Suisse and Point72 Asset Management, which is run by Steve Cohen, the hedge fund manager who at one time ran SAC Capital.

From The Wire’s graphics team: The Players Behind Luckin’s Rise and Fall

In this week’s graphic, meet the people behind Luckin Coffee, the institutional investors who fell for the inflated numbers, and the short-sellers who suspected it was too good to be true.

“People should have seen this coming,” said Michael Norris, a research and strategy manager at Agency China, in Shanghai. “There was this disconnect between what Luckin was and how it was portrayed in the English language press. People couldn’t get past this idea that it was the Starbucks of China or a Starbucks challenger.”

On Sunday, one of China’s top regulators, the State Administration of Market Regulation, raided Luckin’s headquarters in the city of Xiamen, in southern China, as part of an investigation into the company’s accounting practices, according to the Wall Street Journal.

The downfall of Luckin, which declined to comment for this article, has intensified scrutiny of Chinese companies listed in the U.S., cast suspicions on the due diligence process at global investment banks and accounting firms, and provided new ammunition to Washington lawmakers already antagonistic towards China.

Senator Marco Rubio, R-Fla., recently called Luckin’s alleged misdeeds “outrageous.” In June, he helped introduce a bill that calls for U.S. exchanges to delist the companies that fail to comply with American regulations, a proposal clearly aimed at Chinese companies.

And last Tuesday, the chairman of the U.S. Securities and Exchange Commission and the head of the Public Company Accounting Oversight Board released an unusually candid warning about the risks that investors in U.S. markets face with listed companies that operate predominantly in emerging markets like China. The joint statement noted that neither the S.E.C. nor the accounting oversight board have access to accounting documents in China, or the ability to engage in enforcement actions. The Chinese government has routinely denied access to overseas regulators, citing state secrets laws.

In the Luckin case, the anonymous exposé leaked out of China and fell into the hands of a group of American and global short-sellers. It was reviewed and made public by Carson C. Block, the head of Muddy Waters Capital, a San Francisco-based firm that specializes in profiting from falling stock prices. He has declined to say who produced it.

Data: S&P CapitalIQ

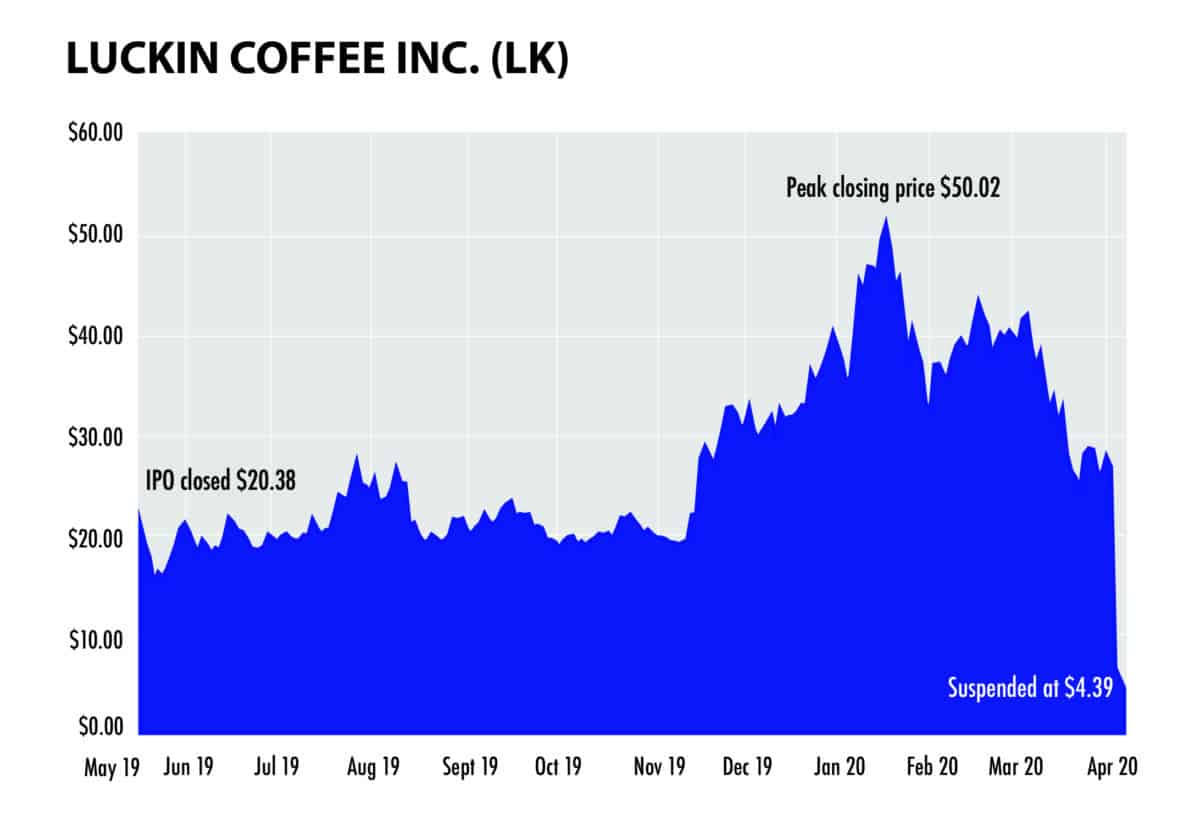

The company, after initially disputing the allegations, confessed to one key finding in the report: that the three-year-old startup vastly overstated its sales. In early April, the company said a special audit led by Ernst & Young found that Luckin’s chief operating officer, Liu Jian, and other employees had carried out a scheme to fabricate more than $300 million in revenue in the six months ending Sept. 30. The stock tumbled by more than 90 percent from its high. About $11 billion in wealth vanished.

It was a dramatic turnabout for a company that had backing from some of the biggest names on Wall Street, including Credit Suisse and Morgan Stanley. It had also hired powerful law firms and an affiliate of one of the big four accounting firms.

Now, some of those backers are reviewing their vetting process and counting losses because of loans made to Luckin’s top executives with their Luckin shares pledged as collateral. And in an unusual move, the China Securities and Regulatory Commission issued a statement earlier this month condemning Luckin, even though the regulator has no jurisdiction over Chinese companies listed in the United States.

Luckin, in many ways, exemplified the China hype. What Baidu is to Google and Xiaomi to Apple, Luckin was supposed to be to Starbucks — a homegrown competitor, backed by state and private financing and cheered on by state media. Luckin promised low-priced coffee, ubiquitous store locations, and delivery to your home in 30 minutes. It also promised a way for global funds to invest in China’s economic miracle.

THE PERCOLATING

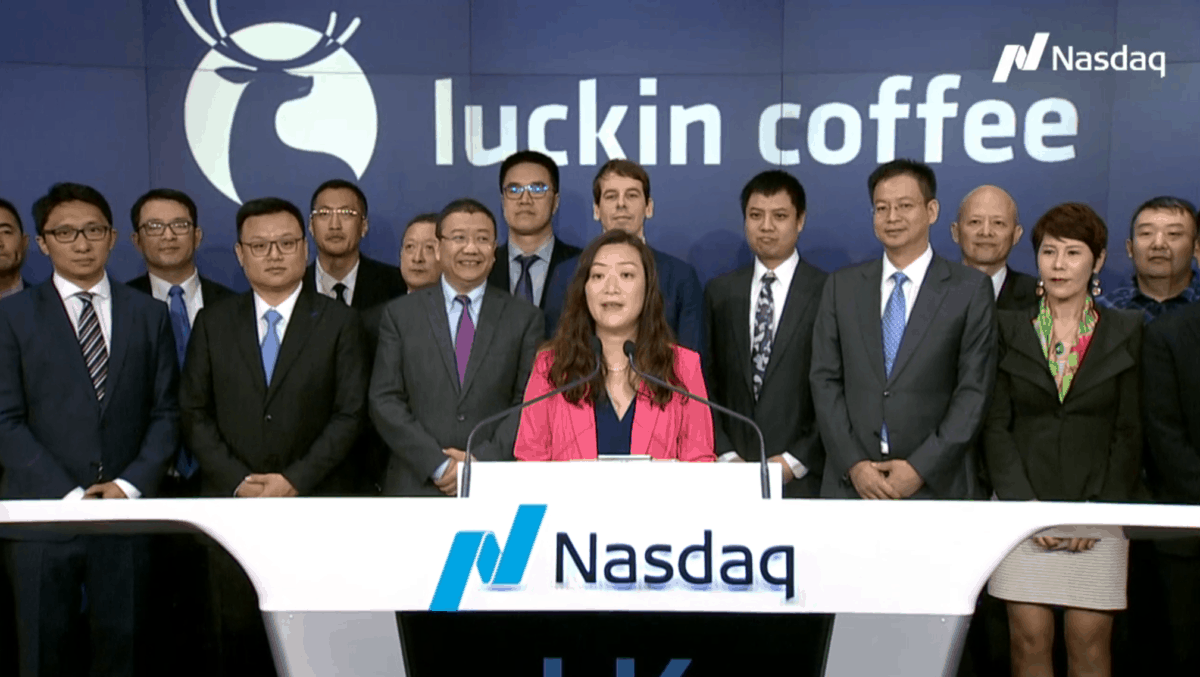

As she stepped to the podium at the Nasdaq’s headquarters in New York last May, Jenny Zhiya Qian’s bright pink blazer stood out against the backdrop, which was the signature deep blue of a Luckin Coffee cup and featured the silhouette of a stag, Luckin’s logo. Qian, Luckin’s chief executive officer, was preparing for the opening bell, a celebration of the Chinese coffee chain’s first day of trading as a public company.

There would be confetti and photo-ops to commemorate what was unmistakably Luckin Coffee’s moment. But Qian seemed to have Starbucks on her mind.

“Luckin’s listing is the start of equality for Chinese coffee consumers,” Qian declared in Chinese. Some people say a Chinese company might not have what it takes to match Americans when it comes to selling coffee, she said, but “what’s lacking is those people’s self-confidence.”

Credit: Nasdaq (video posted on Facebook)

Qian’s comments reflected Luckin’s obsessive drive to overtake Starbucks, one of the most successful U.S. companies in China. Starbucks opened its first coffee shop in the country in 1999 and now has 4,300 of them. By the time of its initial public offering, not even two years after its founding, Luckin was more than halfway to matching the market leader.

“We have done what most people do in 15 or 20 years,” Luckin Chief Financial Officer Reinout Schakel told CNBC on the morning of the Nasdaq debut.

China consumes nine times as much tea as coffee, but Qian saw that statistic as an opportunity. According to an account in Xinhua, the official state news service, she was drinking more and more coffee during long hours at her previous job and grew interested in why coffee hadn’t caught on in China as in other countries and why its cost was so high.

Until 2017, neither Qian nor Luckin’s chairman and largest shareholder, Charles Zhengyao Lu, had much to do with coffee shops. Lu studied industrial electric automation at the University of Science and Technology in Beijing and worked for the government in the northern city of Shijiazhuang for three years before getting the business itch. He started and ran a string of companies in information technology, telecommunications and automobile services.

“Entrepreneurship is like a marathon without an end,” he said at an award ceremony for China’s biggest business names in 2016.

His most successful venture at the time was CAR Inc., a car-rental company that had U.S. financing from Hertz and Warburg Pincus, the private equity firm. It listed on the Hong Kong stock exchange in 2014, and within eight months, its stock value had nearly doubled. The boom was short-lived — the share price dropped below its initial offering price by the beginning of 2016 — but by then Lu, along with Hertz and Warburg Pincus, had sold the bulk of their stakes.

Before she was Luckin’s CEO, Qian had worked for Lu at CAR and then Ucar, an affiliated ride hailing service where Lu was CEO. In November 2017, Qian announced she was stepping down from Ucar to start Luckin. She rented space for Luckin from Ucar.

Lu eventually became Luckin’s largest investor, and most of its directors and executives came from Lu’s companies or worked at firms that had invested in them.

Although Luckin’s leaders didn’t have much experience selling beverages, they had a plan: create a coffee chain for Chinese consumers in the internet age.

In China, Starbucks’ appeal was a foreign brand, serving expensive drinks made by trained baristas in cozy shops. Luckin built its model around technology and cost. Customers would order and pay with a mobile device, which facilitates orders for pickup or delivery. Because everything happens online, the company is able to collect massive amounts of data about its customers, which it uses to “engage” them and tailor its many promotions and discounts.

For example, in April, a large Starbucks latte cost $4.53 in Beijing. At Luckin, the same drink was listed at $3.54. Luckin users are plied with so many discounts and free cups that the company’s reported average price per item sold is just $1.54.

Luckin’s business model also relies on convenience. At the end of 2017, Luckin had nine stores. By the end of 2018, it had added over 2,000 more — or five new stores per day. Even though it had racked up huge losses, traffic was brisk.

Credit: N509FZ, Creative Commons

Major investors clamored to get in on the action. Venture capital firms poured $500 million into the company to help the build out in the two years before it went public. Early backers included China International Capital Corporation, the state-owned investment bank; the Singapore’s sovereign wealth fund GIC; and New York’s BlackRock, the world’s largest money manager.

When Qian stepped up to the Nasdaq podium on May 17, 2019, Luckin had been in operation for just 20 months. Its $17 a share public offering raised another $645 million, and its underwriters included CICC, Morgan Stanley and Credit Suisse.

Luckin shares hovered around $20 each after its IPO, but its third-quarter results, announced in November, set off a new wave of excitement. The company reported $216 million in revenue, a 640 percent increase from a year earlier. There still was no net income, but Luckin said it had achieved operating profit at the store level, a calculation that excludes corporatewide costs. On January 7, the company said it had more than 4,500 stores, enough to overtake Starbucks in China.

Howard Penney, an analyst for the online financial program Hedgeye Risk Management, summed up the optimism surrounding the company’s story line. On Jan. 15, he said that Starbucks would never be able to compete with Luckin in China, and might as well try to acquire it. Penney called Luckin “the most digitally savvy company in the world.”

Two days later, Luckin’s stock hit its all-time high, just above $51 a share, pushing its market value past $12 billion.

THE SHORT-SELLERS

A decade ago, another Chinese company captivated investors — this time with promises of hundreds of thousands of acres covered with forests and valuable timber. Sino-Forest Corporation, a Chinese company, had secured a listing on the Toronto Stock Exchange, prominent investors such as American billionaire John Paulson’s hedge fund and a stock market valuation of $5 billion.

Courtesy of Carson Block

That is, until Block, then a 35-year-old short-seller, began investigating its Chinese operations and discovered that Sino-Forest didn’t have nearly as much timber or as many customers as it claimed in its financial statements. Block, who was trained as a lawyer, shorted the stock, went public with his findings and then watched as Sino-Forest collapsed. After an initial round of strong denials, the auditors resigned, the company filed for bankruptcy and the authorities in Ontario accused the company of fraud and deception.

Today, Block lives in Sonoma County, Calif., and manages a $200 million fund that makes global bets. His firm, Muddy Waters Capital, seeks to profit by identifying fraud and accounting manipulations and then taking short positions on the stocks. His early years as a short-seller are depicted in the 2017 documentary film, “The China Hustle,” produced by Alex Gibney and Mark Cuban.

China, of course, remains a focus. Block, who lived and worked for years in Shanghai, and even published a book on doing business in China, insists that Chinese companies, including many of those listed in the U.S., are prone to deception.

“China is to stock fraud,” he likes to say, “as Silicon Valley is to technology.”

It was only a matter of time, then, before he would look more closely at Luckin Coffee, which he considered the fairy tale company of the moment. As Block tells it, a short-seller he knew chatted him up in early January 2020 and mentioned that his firm had been investigating Luckin. The unnamed individual, who was preparing to short Luckin, had operations in China and worried about his personal safety and that of his staff. Could Block publicize the research?

There was reason to worry. The scandals of a decade before, around 2011, had exacted a serious toll on the value of Chinese companies listed overseas and angered the Chinese government, which came under pressure from American regulators seeking to investigate the claims.

China is to stock fraud as Silicon Valley is to technology.

Carson Block

When things go right for them, short-sellers make their money by borrowing shares, selling them, then, after the stock falls, buying the shares at a cheaper price than what they sold them for in the open market. They use the new shares to repay the loan of stock and pocket the difference.

“Shorts,” as they’re called, are not popular among businesses in any country, but in China, the dislike can take a dark turn. Firms that do research for the short-sellers can get death threats and even visits from local authorities.

In a case that highlighted the government’s concerns, Huang Kun, a Canadian citizen working in China, was arrested and sentenced to two years in prison in 2013 for illegally gathering information and “spying” on a mining operation in central China, apparently to aid a Canadian short-seller who published online using the name Alfred Little, according to The New York Times. (After serving out his sentence, Mr. Huang was deported to Canada).

Gillem Tulloch, who runs GMT Research, a Hong Kong-based accounting services firm that advises hedge funds and short-sellers, says no one living in China would admit to being a short-seller and that even Hong Kong is considered dangerous.

“There’s no bad news in China,” Tulloch said with a chuckle. “If there is, you’re hauled off to the gulag for re-education.”

In an interview, Block said he initially declined to publicize the exposé on Luckin because that would have involved attaching his name to someone else’s work. But soon after his talk with the short-seller who produced the report, he began getting calls about Luckin from other short-sellers, asking whether he had read the exposé. He got hold of a copy.

The 89-page report, written in English, reads like a corporate thriller. Luckin, the report said, was a “fundamentally broken business.” With video, photographs and receipts of customer transactions gathered by more than 1,500 researchers, the report claimed that Luckin inflated its sales, obscured its advertising and marketing spending and hid some of its losses.

According to the report, the investigators established monitoring stations at Luckin stores in 53 Chinese cities, and collected 11,260 hours of video and 25,000 receipts. Often, the researchers just sat inside the store, recording video of the transactions. The report also contained detailed spreadsheets and analysis of everything from the company’s pricing strategy to its advertising spend.

“It took a tremendous ground game,” Block said, noting that such a project could cost more than $500,000 to complete.

There were also troubling corporate governance issues noted in the report. It alleged, for example, a series of related party dealings with other companies affiliated with the founders; noted that a Luckin director had ties to other Chinese companies that had been accused of fraud; and it said Luckin was not forthcoming about its co-founder and chief marketing officer, Yang Fei, who in 2015, before he joined the company, was sentenced to 18 months in prison for engaging in illegal marketing practices. Mr. Yang, who apparently joined Luckin after his release from prison, was not listed as a top executive in the company’s IPO prospectus or on its English language website.

Block’s team went to work. They asked to examine the anonymous short-seller’s online data warehouse. They combed through the report to analyze its methodology and documents. And within days, they determined that it was not only credible, but powerful.

On Jan. 31, while in Miami on a business trip, Block tweeted out three sentences to his firm’s 90,000 Twitter followers. It began, “MW is short $LK.” (LK is Luckin’s stock ticker symbol.) He attached a copy of the report.

The stock immediately tumbled 27 percent, before recovering some ground.

Other short-sellers jumped into the fray. Andrew Left of Citron Research, which had a reputation for shorting Chinese companies listed overseas, said he had read the report and was unconvinced; he was backing Luckin. But Anne Stevenson-Yang of J Capital, also well known as a short-seller, responded a few weeks later with her own detailed report alleging deception at Luckin. Then Jim Chanos leapt in. The head of New York-based Kynikos Associates, Chanos had established himself as a prominent short-seller by spotting Enron as a loser before its collapse. In April, he said publicly that he had also shorted Luckin.

“Three short-sellers is almost unheard of, and it’s a very elite group that went after them,” says Tulloch at GMT Research, which advised its own clients to avoid Luckin. “Very few companies can survive that type of attack.”

Luckin fought back. The company issued a strong denial and its stock crept back up. Some of the short-sellers believe big institutional investors were mounting a counterattack, and even trying to influence Left at Citron Research, something Left denies.

“I called people who had hundreds of millions of dollars invested. They said they saw the report and ‘We believe their business is doing well,’” Left said in an interview with The Wire. “Did that turn out to be wrong? Of course.”

THE RECKONING

Some of the biggest names in U.S. investing may have been caught holding large Luckin positions as the storm was breaking, according to their most recent disclosures to the SEC.

The filings indicate that Capital Group, a mutual fund giant managing more than $1.8 trillion, held 8.9 million Luckin shares on Jan. 31 worth $290 million based on the closing price that day. Luckin’s stock price fell 86 percent from that point until trading was halted after the April 6 close. A person familiar with the matter said Capital exited its position in the first quarter.

Billionaire Stephen Mandel’s Lone Pine Capital hedge fund held $459 million of Luckin shares on Jan. 9, according to its filings. By April 2, Mandel had sold the entire position. Lone Pine’s indicated portfolio loss would have been about $196 million, if the fund sold at the average closing price between those two dates. Lone Pine, based in Greenwich, Conn., declined comment.

After buying a large position in Luckin last August, hedge funder Steven Cohen’s Point72 pared back its holdings by the end of the year, when it reported holding 1.1 million shares valued at $45.2 million. That was less than three weeks before Luckin hit its peak price over $50 a share before dropping to less than $5. It isn’t known how the Luckin bet worked out for Point72, which declined to comment.

Goldman Sachs said that Lu and Qian, the chairman and chief executive, were in default on a $518 million loan that had been collateralized with their Luckin shares. Acting as agent for a group of lenders it didn’t identify, Goldman said it was proceeding to sell the equivalent of 76.4 million shares of the Nasdaq-traded Luckin stock. By the time of the announcement, however, the shares were already worth less than the value of the loan.

Goldman, however, had taken the equivalent of its own short position in Luckin’s shares. At the end of the fourth quarter, its filings show it held a put-option to sell 7.9 million Luckin shares. Like a short position, put options also make money as a stock falls. The filing suggests that Goldman may have been hedging its position as a lender holding some of the Luckin collateral shares. The put position was a sizable insurance policy against a drop in the stock. Goldman declined to comment for this story.

Luckin and the underwriters are also facing potential liability from two lawsuits that have been filed by investors against it in federal court in New York. One of those suits also names the underwriters of the Luckin share offerings as defendants. Both suits allege fraud against the shareholders.

But if Luckin does not settle, the plaintiffs would face hurdles in recovering any judgment made against it, since China rarely enforces U.S. court orders. The SEC reminded investors of the difficulty of pursuing cases and recovering judgments against Chinese companies in a statement emphasizing the risks of investing in overseas companies on April 21, after Luckin said some of its 2019 financial statements were inaccurate.

Another hurdle to recouping losses from Luckin is its complex corporate structure, which the company referenced in its IPO documents as a “risk factor” in investing in the stock. Luckin’s investors in the U.S.-listed shares do not directly own all of Luckin’s assets, according to the offering prospectus, due to a structure designed to circumvent Chinese restrictions on foreign ownership of its companies. The structure could make it difficult for U.S. lenders or investors to recover money from Luckin.

A spokesman for Sen. Rubio — who favors delisting Chinese companies that are non-compliant with U.S regulations — told The Wire that American exchanges are part of the problem. “It’s no secret” that “the exchanges make money by having listings, so the more listings they have is also better for the bottom line.” He added that the U.S. financial industry has incentives to push lawmakers to allow Chinese companies to trade in the U.S., even though they flout American securities regulations.

Luckin, of course, doesn’t represent Chinese companies. But it does represent a country that has grown into a force in new global stock listings. And its collapse could deal a blow to the ecosystem of banks, funds and professional services firms that are betting that Chinese companies will make up a large share of the global brands of the future.

Block, the short-seller, sees the China story through a much darker lens. “When it comes to China, everyone has this willingness to overlook these things,” he says, noting the allegations of fraud and deception in the Luckin case. “China has always gotten a pass.”

Eli Binder is a New York-based contributing writer for The Wire. He previously worked at The Wall Street Journal, in Hong Kong and Singapore, as an Overseas Press Club Foundation fellow. @ebinder21