China’s AI darlings like DeepSeek have achieved global fame over the last year. But some Chinese companies now riding the AI gold rush — and drawing investor attention — are names of whom few consumers will ever have heard.

Take Victory Giant Technology, a Huizhou-based company that last month raised HK$20.1 billion ($2.6 billion) in Hong Kong’s largest listing this year so far. It manufactures printed circuit boards, a key element of the servers used to run AI workloads.

That may not be as exciting as the latest model from one of China’s AI developers. But thanks to heavy demand from the likes of Nvidia, which uses Victory Giant’s circuit boards in its servers, the company’s revenue nearly doubled to 19.3 billion yuan ($2.8 billion) last year. Its Shenzhen-listed shares have risen twenty times in the last three years.

Companies providing the backbone to AI’s growth, like Victory Giant, are now emerging as the biggest beneficiaries of the fever for the technology. Just as in the U.S., capital has been moving from companies that produce AI models and software to those that produce physical infrastructure. And while Chinese AI companies, from ByteDance to DeepSeek, are under pressure to commercialize their models, companies that serve the growing demand for computing capacity and chips — and which already have profitable models — are thriving.

“The more obvious near-term AI trade is often the enabling layer — power, semiconductors, cloud, telecom infrastructure, data centers and hardware suppliers,” says Philip Reschke, a Hong Kong-based investor with a focus on China. “Those businesses can benefit from broad AI adoption regardless of which individual model or application developer ultimately wins.”

For sure, investor appetite for Chinese AI model developers remains strong. Tech giants and investors are currently scrambling to get in on DeepSeek’s maiden funding round: the Hangzhou-based startup, which is in talks with the national AI fund as its lead investor, could be valued at up to $50 billion, according to media reports.

Shanghai-based StepFun recently secured $2.5 billion from industrial investors as it prepares for an IPO, while Moonshot AI raised $2 billion last week in a funding round led by the venture capital arm of food delivery company Meituan.

But a pressing question for all Chinese AI companies is how to monetize their offering. To date, many have prioritized developing open source models, which users can download and run on their own devices for free, in order to maximize their appeal. Finding a way to earn recurring revenue has proven harder.

…the capital markets this year have been really focused on [AI infrastructure], because this demand-and-supply pinch has been quite prominent and persistent in a number of product categories.

Eric Wong, founder of Stillpoint Investments, a U.S.-based hedge fund

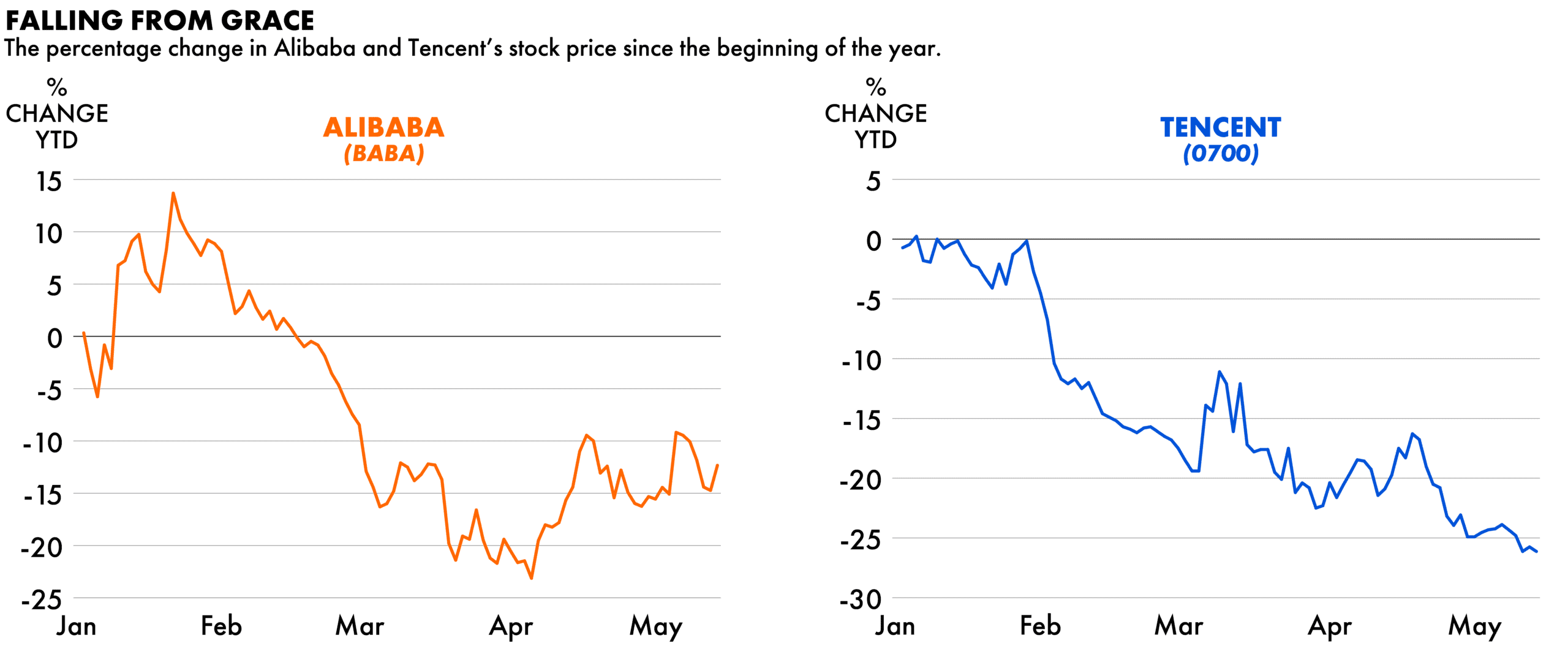

Tech giants Alibaba and Tencent have meanwhile underperformed over the past year amid concerns about the returns on their AI investments. Both missed analysts’ sales estimates for the first quarter of the year, with their heavy outlays into AI infrastructure weighing on their profit margins.

Alibaba’s shares have fallen by around a quarter from their peak in October, after a rally last year. Tencent’s shares have also dropped by 25 percent since the start of this year.

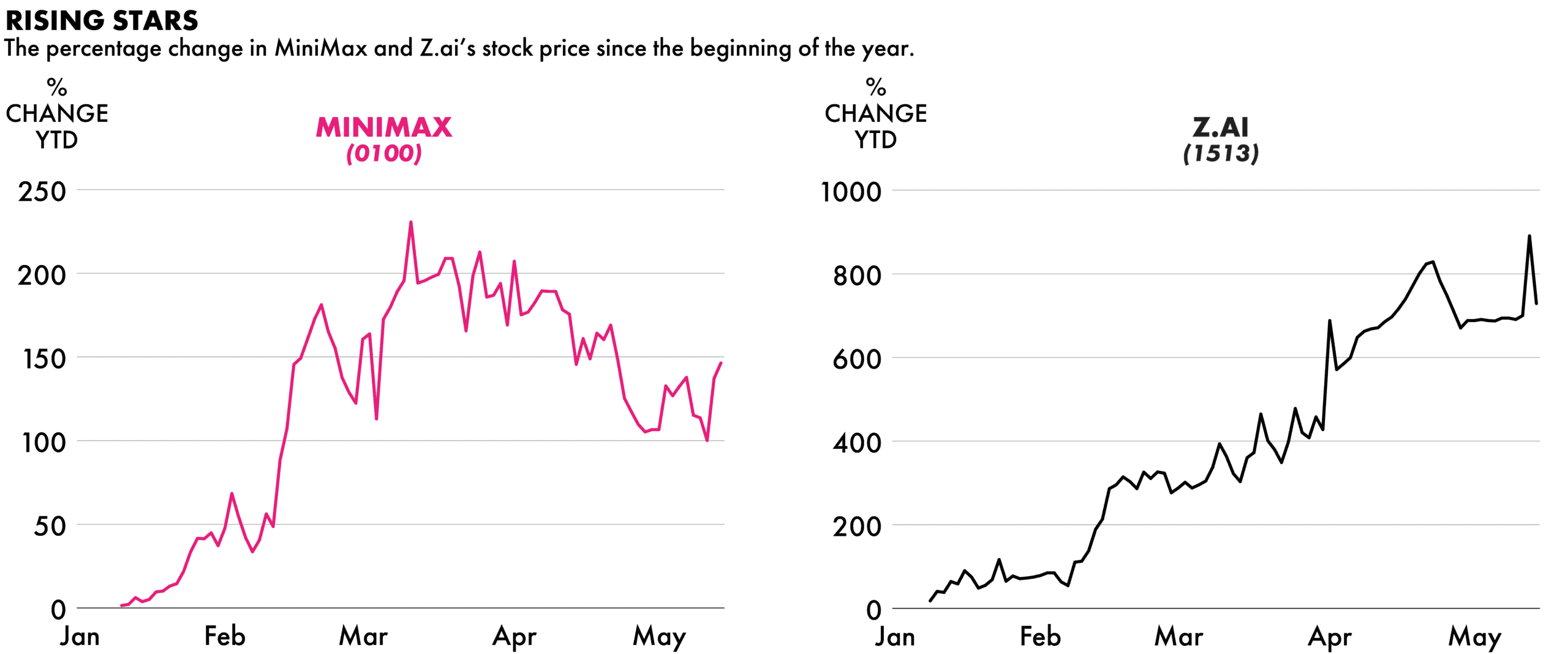

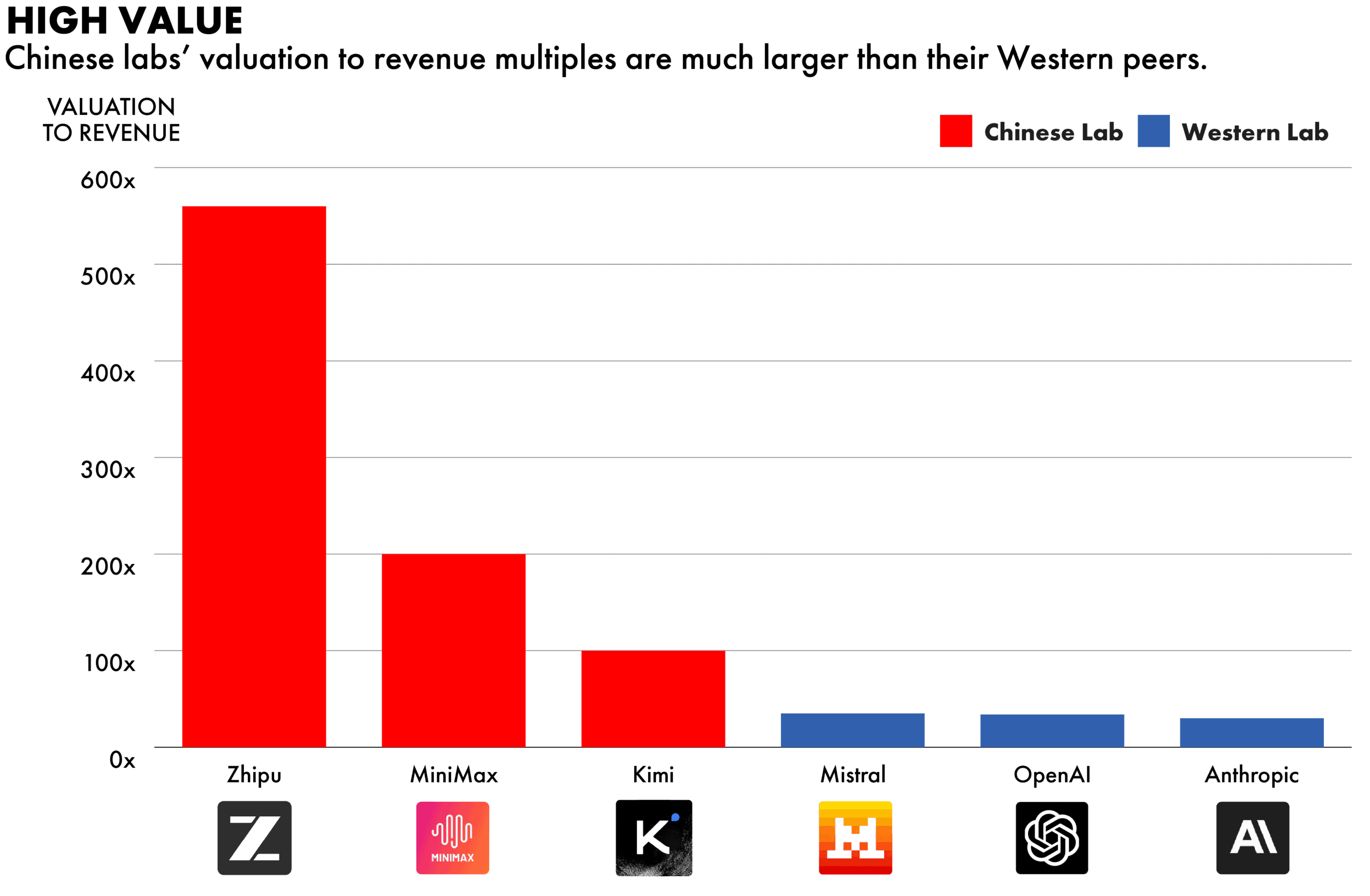

Startups such as Zhipu and MiniMax are faring better. Both made strong market debuts in Hong Kong in January, and saw their shares skyrocket on the back of their new models. The rise of AI agents, which run autonomously and consume more AI tokens, has helped their revenue soar.

The question is whether they can lock in paid users.

“Every few weeks a new, cheaper, competitive model arrives and resets pricing expectations,” says Dermot McGrath, a tech investor based in Shanghai. Both Zhipu and MiniMax are already trading at frothier levels than their Western peers, based on the ratio of their full enterprise value to sales. If intense competition were to unleash a price war among Chinese AI developers, their growth trajectory could be hard to sustain, McGrath adds.

Meanwhile, smart money is moving towards companies that provide the ‘picks and shovels’ for the AI industry, as the likes of Alibaba and ByteDance pledge hundreds of billions in capital expenditure.

“The money that the hyperscalers are spending is flowing into the physical infrastructure supply chain,” says Eric Wong, founder of Stillpoint Investments, a U.S.-based hedge fund. From chip manufacturing to power generation, “it is a very comprehensive supply chain that’s benefiting from this capital expenditure cycle.”

The profitable infrastructure companies — storage, packaging, equipment — are model-agnostic. They sell into demand regardless of which lab is on top this month.

Dermot McGrath, a tech investor based in Shanghai

The classic example in the U.S. market is Nvidia, whose advanced AI chips are powering the technology’s global rollout. In China, some of the most obvious choices are also chip foundries and designers, which are benefiting too from the country’s ongoing push for self-sufficiency in technology.

But investors have already crowded into this sector, inflating valuations and creating volatility. Cambricon, a domestic chip designing substitute for Nvidia, for instance, is currently trading at 290 times its earnings, an exceptionally high level, according to data from Google Finance.

Instead, some institutional investors are looking into more obscure parts of the AI supply chain, particularly where there are supply bottlenecks.

Wong, for instance, sees an opportunity in the manufacturers of diesel and gas engines that power data centers. Companies in this area have order backlogs that extend till next year, he says. And given the energy capacity crunch brought on by demand from data centers, they can fetch higher prices and stronger margins.

A leading company in this space is Shandong-based Weichai Power. Its shares have doubled over the past six months as the company pivoted from making engines for cars to power solutions for AI data centers. The company recorded three-digit growth in sales of products in this new segment in the first quarter of the year.

“That’s why the capital markets this year have been really focused on [AI infrastructure], because this demand-and-supply pinch has been quite prominent and persistent in a number of product categories,” Wong says.

Hidden gems can also be found in areas within the AI supply chain where many small- and mid-sized companies are competing against each other, and where there are more opportunities for outsized returns, says Winnie Wu, head of Asia Pacific equity strategy at Bank of America Global Research.

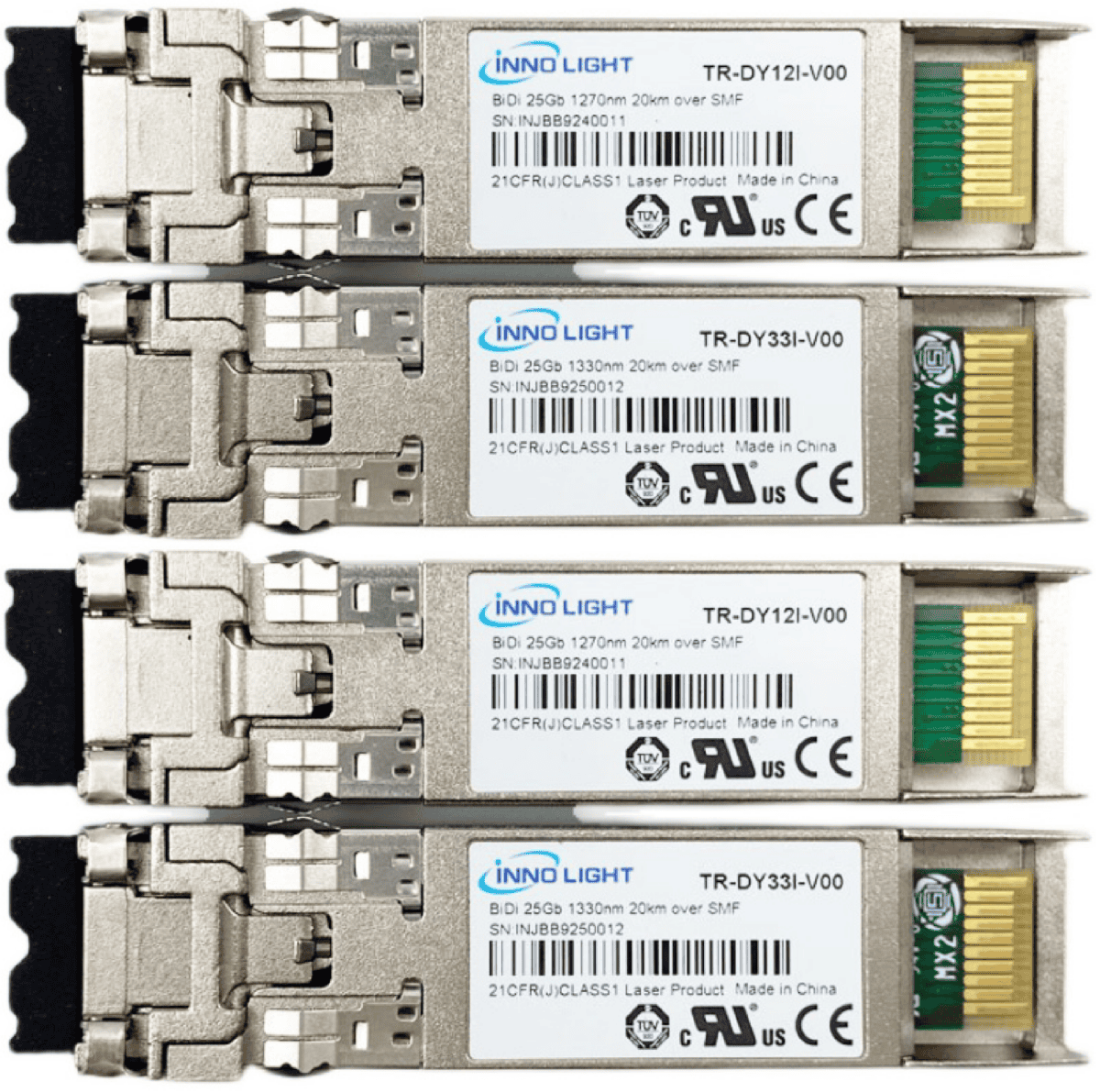

One example is producers of optical modules — a critical component that connects graphic processing units within a cluster of chips. Wu’s team at Bank of America expect these companies to be most profitable in the AI supply chain this year, with returns on equity of around 40 percent.

Shenzhen-listed Zhongji Innolight, for instance, saw a nearly tenfold jump in its shares over the past year. Its revenue in the first quarter of this year nearly doubled year-on-year to 19.5 billion yuan ($2.8 billion) while its profit increased 262 percent to 5.7 billion yuan ($840 million).

Another area is printed circuit boards. Kingboard Laminates, a rival of Victory Giant, recorded triple-digit gains this year as its share hit an all time high. Its profit jumped 84 percent last year to reach HK$2.4 billion ($300 million).

“For hardware companies, what investors like is the earning growth and that monetization is very transparent and straightforward,” Wu says.

As demand for AI infrastructure is structural, there is less risk of these companies falling out of favor no matter how the competition in the AI application layer shakes out. “The profitable infrastructure companies — storage, packaging, equipment — are model-agnostic. They sell into demand regardless of which lab is on top this month,” says McGrath.

When model shocks hit, such as the so-called ‘DeepSeek moment’ last year that wiped hundreds of billions off U.S. stocks, “those are the names that recover,” he adds.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.