China’s economy keeps posting solid headline numbers — around 5 percent GDP growth in 2025, hitting the official target once again. Yet look closer, and a troubling picture emerges. Corporate profits have barely budged. Industrial earnings across the country rose just 0.6 percent in 2025, finally ending three straight years of declines but still scraping along at near-zero levels. This isn’t a sign of robust health; it’s the symptom of a deeper issue: intense, cutthroat competition that forces companies to slash prices relentlessly, even when they can’t cover their costs.

In many sectors, including those that would appear most successful when one looks at China’s global dominance — such as electric vehicles, solar panels, batteries, and other green technologies — Chinese firms engage in endless price wars. They keep selling at rock-bottom levels, sometimes below what it costs to produce, just to hold onto market share. A growing number of these companies cannot earn enough revenue to even service their debt, let alone other costs. These “zombie” companies survive only because banks roll over loans and local governments provide subsidies to avoid job losses and keep tax revenues flowing.

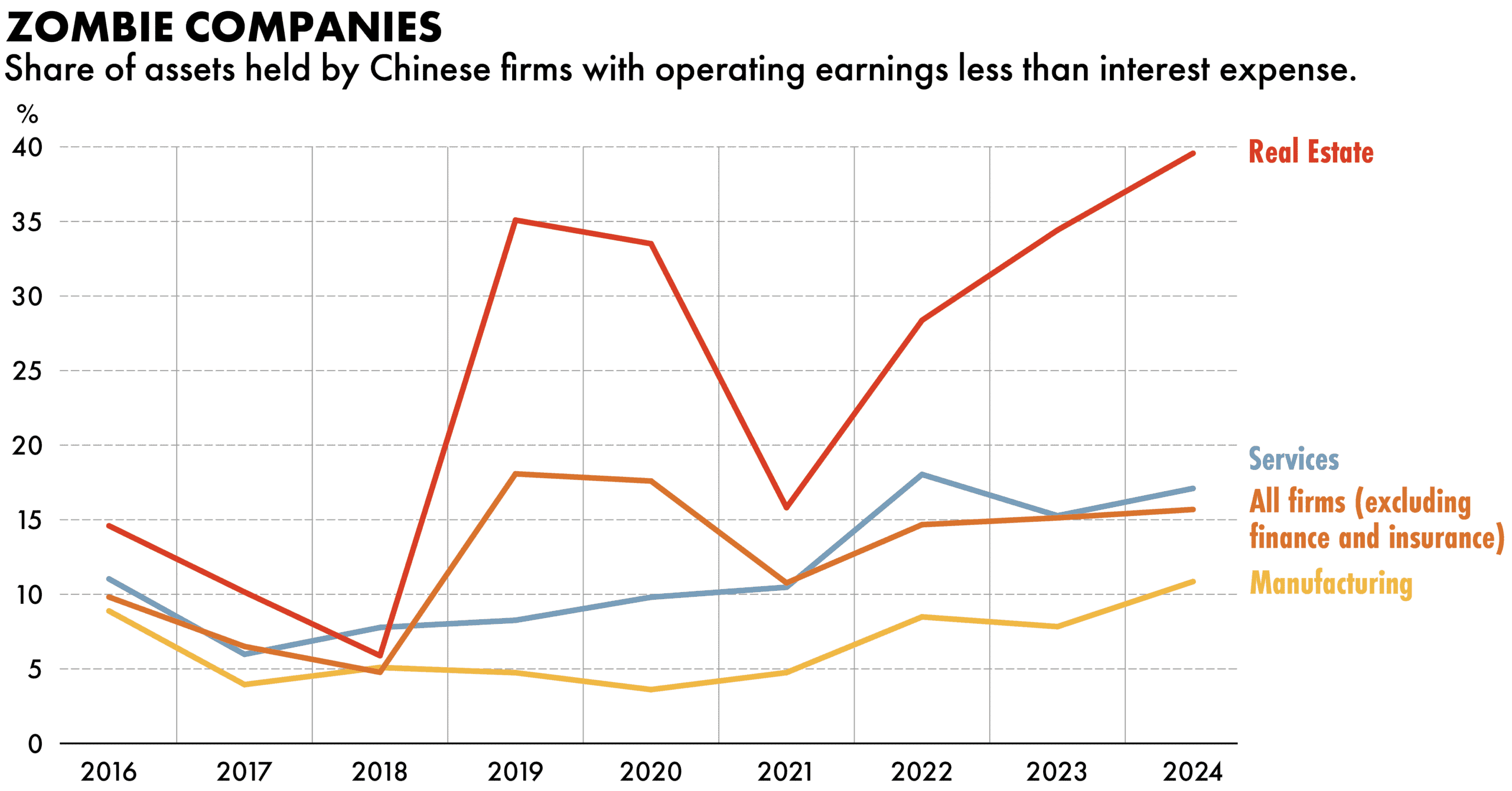

Recent estimates show this problem is spreading. The share of non-financial corporate assets held by zombies climbed from about 5 percent in 2018 to 16 percent in 2024. In newer, high-priority sectors like green tech, the share of zombie companies has hit 30 percent of total listed companies.

The key dynamic here is uneven. Some Chinese companies manage to survive — and even thrive — despite the brutal price competition. These tend to be the more productive ones: they’ve improved efficiency, cut costs through better technology or scale, and can afford to lower prices without immediately bleeding red ink. Their productivity gains give them a buffer, allowing them to maintain revenue streams even as margins shrink.

True sustainability demands accepting short-term pain for long-term gain, namely letting market forces operate so that unviable firms fail and capital can be allocated to productive ones.

But this is only a small share of Chinese corporates. Most firms lack those efficiency improvements. Without real productivity advances, they still join the price-slashing frenzy to stay in the game thanks to external support from banks or local governments. They cut prices aggressively, not because they’re getting leaner or smarter, but because everyone else is doing it and they fear losing customers entirely. The outcome is predictable: collapsing profit margins across the board, even for the better companies, whose productivity is increasing.

In sum, unproductive companies are hurting the productive ones, which is clearly not good for the Chinese economy. This is a very unhealthy creative destruction. Schumpeterian style creative destruction would require exactly the opposite, namely that more productive firms force unproductive ones to exit — through bankruptcy, mergers, or shutdowns. This would free up workers, capital, and market space for more efficient players. Another positive consequence of this healthy creative destruction would be that pricing power would return for good companies so that genuine profit growth can resume. Delaying that process, as Japan did in its lost decades, will inevitably lead to chronic misallocation of resources and stagnant productivity for the Chinese economy.

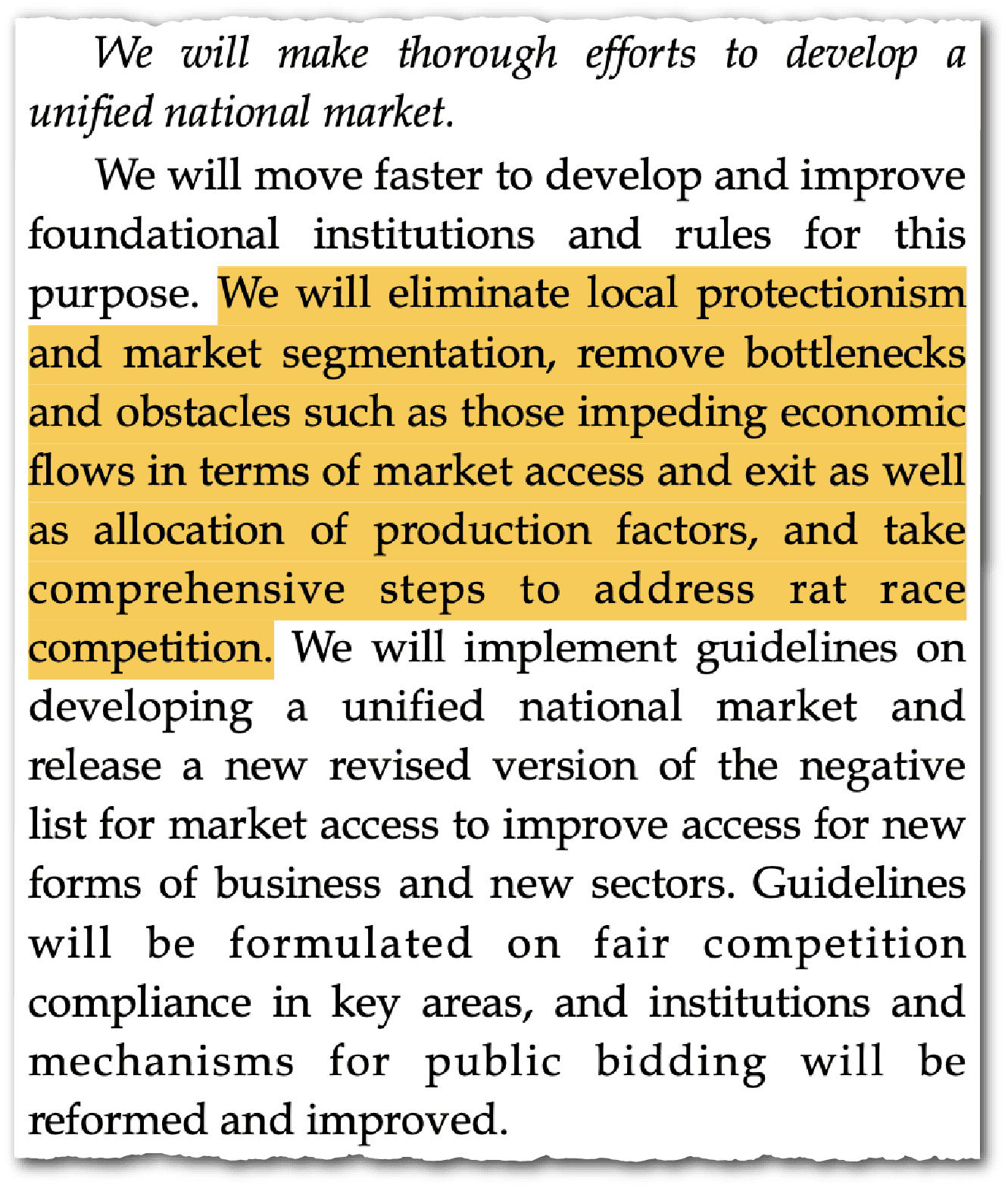

Yet in China, there’s little evidence of a broad wave of exits. Beijing has talked tough about ending “disorderly low-price competition” and encouraging “orderly” capacity reductions since mid-2024. Regulators have tweaked laws on pricing and competition, and some subsidies on EVs and solar panels have been dialled back. But the core mechanism persists: unproductive firms hang on, supported by local interests and reluctant banks.

The fallout spills overseas too. Overcapacity at home pushes ultra-cheap exports abroad, flooding markets with EVs, solar panels, and batteries. Trade partners respond with tariffs and defences, turning domestic distortions into international friction.

True sustainability demands accepting short-term pain for long-term gain, namely letting market forces operate so that unviable firms fail and capital can be allocated to productive ones. This would hurt — job cuts, local budget strains, bank cleanups — but it’s the path to healthier companies, higher wages, and stronger consumption.

Without it, the shift to “high-quality” growth stays mostly words. Debt keeps building, innovation incentives weaken, and the economy relies on more stimulus and export dumping, which is becoming increasingly harder. As we watch involution unfold in China, we should all hold our breath as to whether the current unhealthy competition can turn healthy soon for the benefit of the Chinese economy, and that of the rest of the world.

Alicia García-Herrero is an Adjunct Professor at the Hong Kong University of Science and Technology, and the Chief Economist for Asia Pacific at Natixis. She also serves as a Senior Research Fellow at European think-tank Bruegel.