China’s industrial robot industry has undergone a dramatic transformation in the last few years, driven by insatiable end-user demand, strategic government support, rapid product development, and competitive pricing. Domestic manufacturers have captured a growing share of the local market, and there is increasing concern that China’s robot makers will do to the global robot industry what they’ve done to solar cells, batteries, and electric vehicles.

But reality is more nuanced. The focus on the rapid growth of China’s installed robot base obscures the fact that Japanese and European robot makers are still capturing much of the value in the industry. Chinese firms meanwhile continue to face significant challenges, particularly in innovation, software, and high-end market segments.

Foreign robot makers likely remain a formidable presence in the fast-growing Chinese market partly because pragmatic Chinese customers know domestic robots still have a material technology and performance gap; and partly due to inattention from policy makers in the West — especially the United States, where there is no real scaled industrial robotics industry to protect, and hence limited leverage despite China’s extensive use of foreign robotic technology.

The question is whether the Chinese intend to close the gap through continued industry support and investment, risking an involution spiral; or whether they will conclude that such dominance isn’t necessary to accomplish their top-down goals of industrial supremacy.

The inexorable robotization of Chinese manufacturing

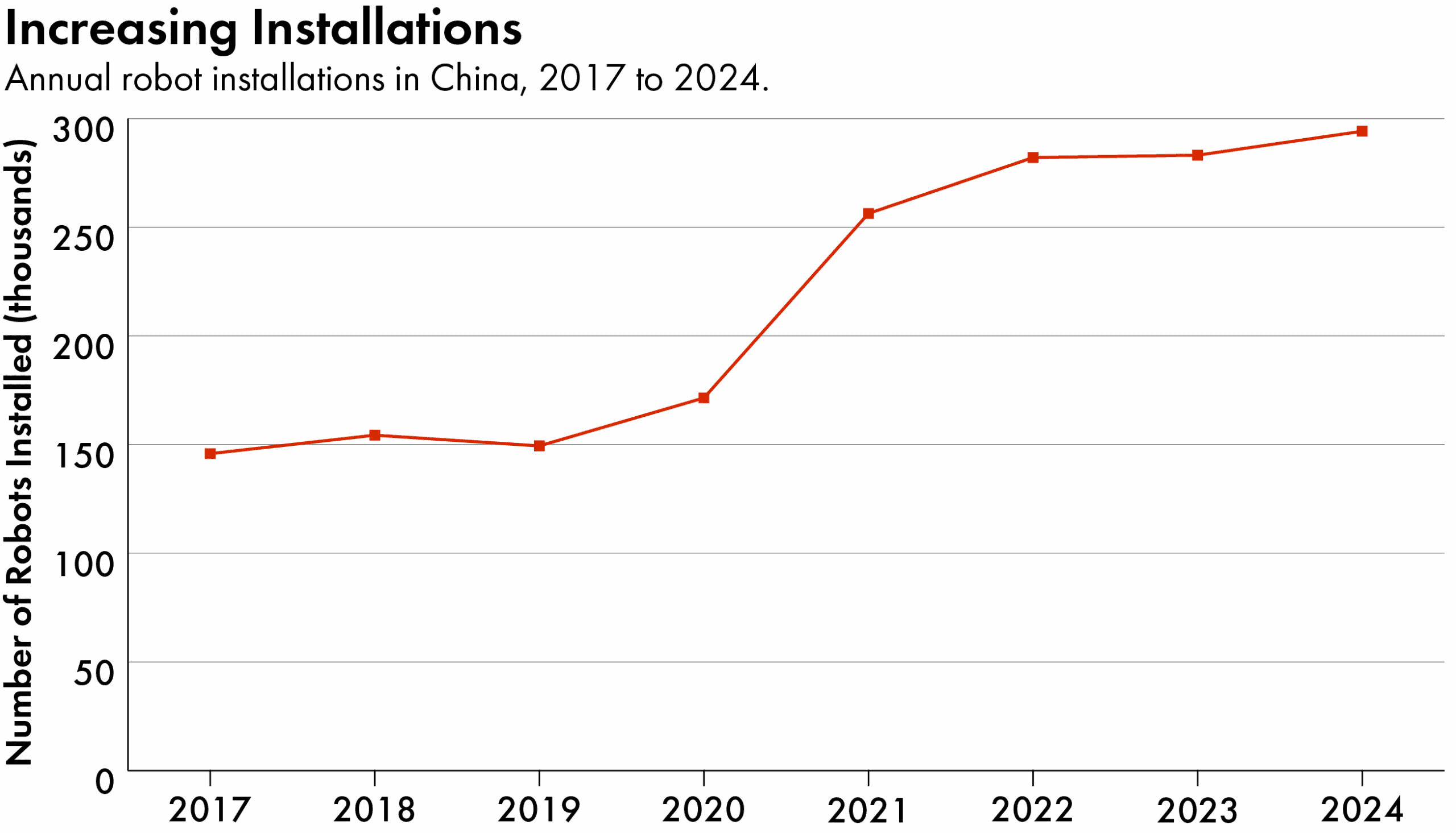

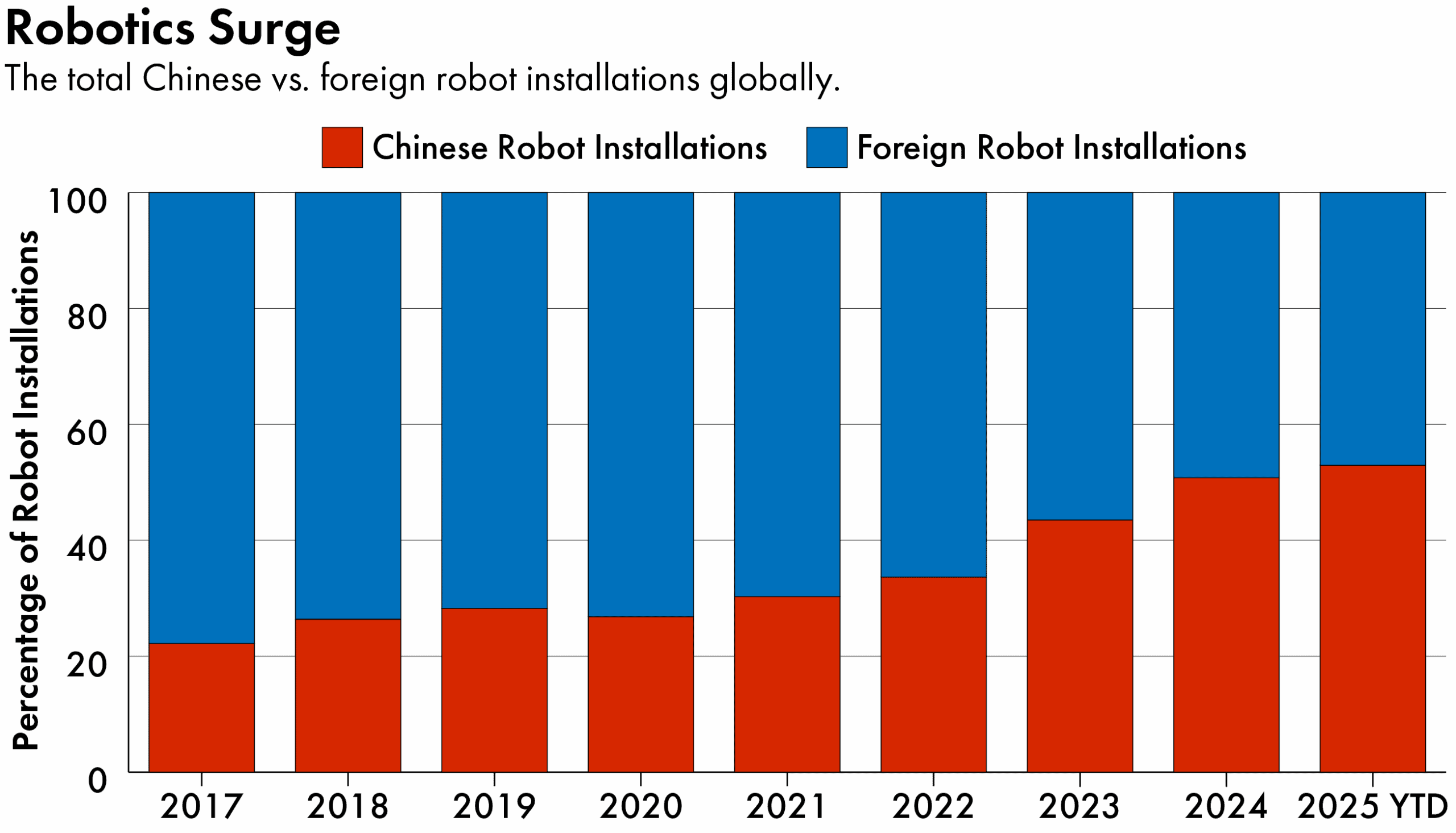

Over the past decade, worldwide industrial robot shipments have more than doubled, from 221,000 units in 2014 to 541,000 in 2024. Much of that growth has been driven by China, which has experienced an extraordinary surge in industrial robot adoption.

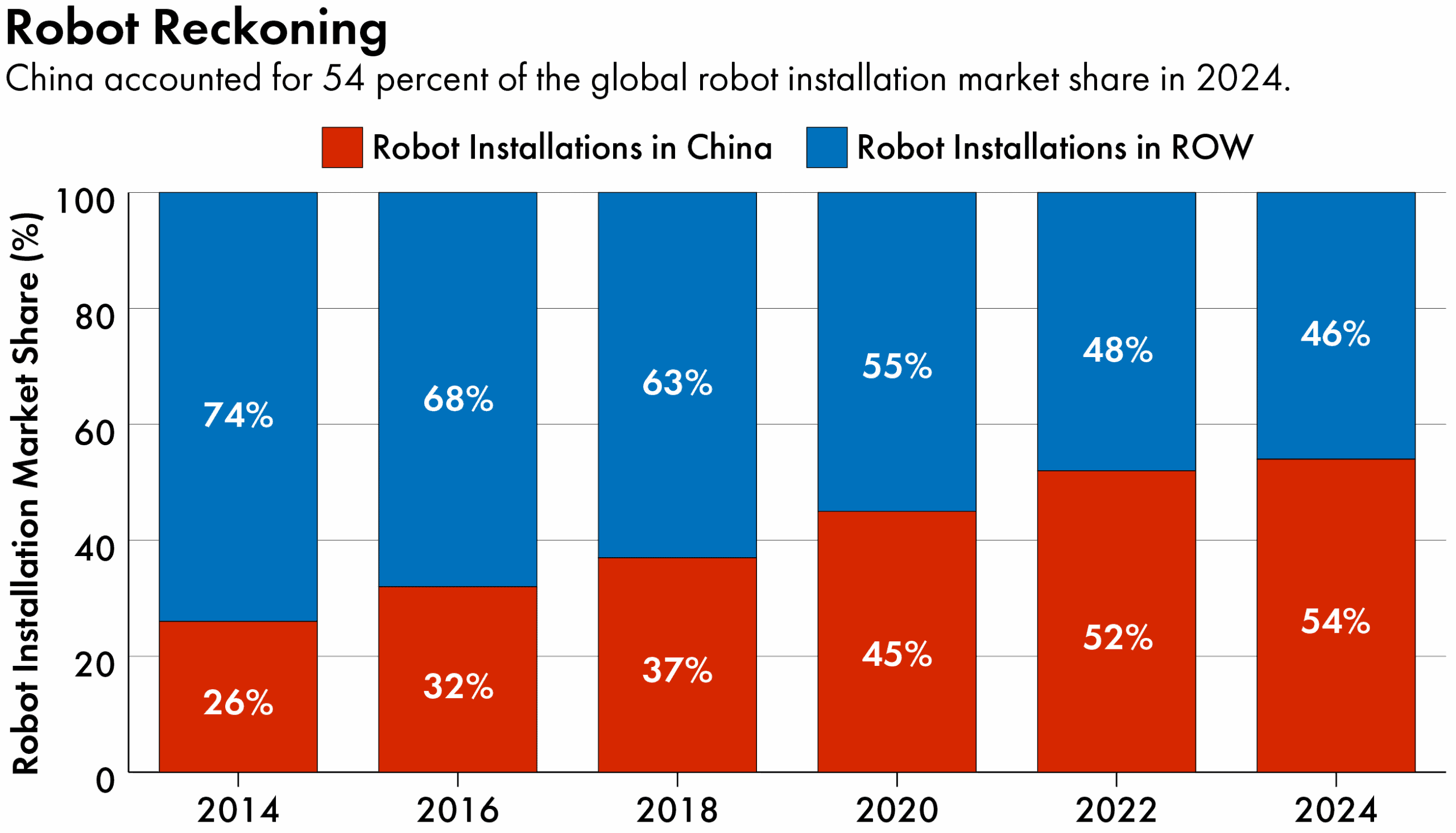

In 2014, China accounted for a hefty 26 percent of all robot installations, making it already the world’s largest robotic market. By 2024, that share had more than doubled to 54 percent. The most recent data shows that 295,000 industrial robots were installed in China in a single year — the highest annual total ever recorded.

The Covid-19 pandemic was a catalyst for China’s robot adoption, as Chinese industrial concerns turned to automation in response to supply chain shocks. As a result, robot density has also risen sharply. By the end of 2023, Chinese manufacturers had installed 470 robot units per 10,000 workers, according to the International Federation of Robotics (IFR), about three times the global average, and surpassed only by Singapore and South Korea.

The drive towards automation has accelerated as China faces a shrinking population and looming labor shortages. Put all these factors together, and it is likely to remain the world’s largest market for industrial robots for the foreseeable future, dwarfing other markets.

Made in China 2025 and the Chinese robotics market

Despite this extraordinary growth in demand for robots, China’s domestic robotics industry has fallen short of the government’s ambitious targets, as set out in the famous Made in China 2025 (MiC) industrial plan. That plan tasked local manufacturers with capturing 70 percent of the Chinese robot market. While Chinese firms have made significant progress — rising from 18 percent market share in 2015 to an estimated 51 percent in 2024 — they are still well short of the MiC goal.

Several structural factors help explain why. Chinese industry has in general struggled in markets dominated by a handful of powerful global incumbents, where barriers to entry are high, due to large upfront investment requirements and specialized intellectual property tightly controlled by established firms.

Robotics fits this pattern. Foreign industrial robots — especially those produced by Switzerland’s ABB, and Japan’s FANUC, and Yaskawa — are widely regarded as superior in precision, reliability, and longevity. As a result, foreign brands continue to dominate the premium segment, while Chinese suppliers have gained ground primarily in low-to-mid-end market segments.

Competing mainly on cost is becoming risky as more players enter the market and undercut each other, similar to what has happened in other Chinese industries like electric vehicles and solar panels, where intense price competition has squeezed profits and slowed real innovation.

For sure, domestic suppliers have steadily improved product quality and expanded their presence, aided by pandemic-era supply chain disruptions that lengthened delivery times for foreign manufacturers and prompted Chinese factories to rely more on local providers. In addition, fast-growing industries such as those for lithium batteries and solar panels have boosted demand for automation that does not require the most sophisticated robots, aligning well with the capabilities of Chinese vendors.

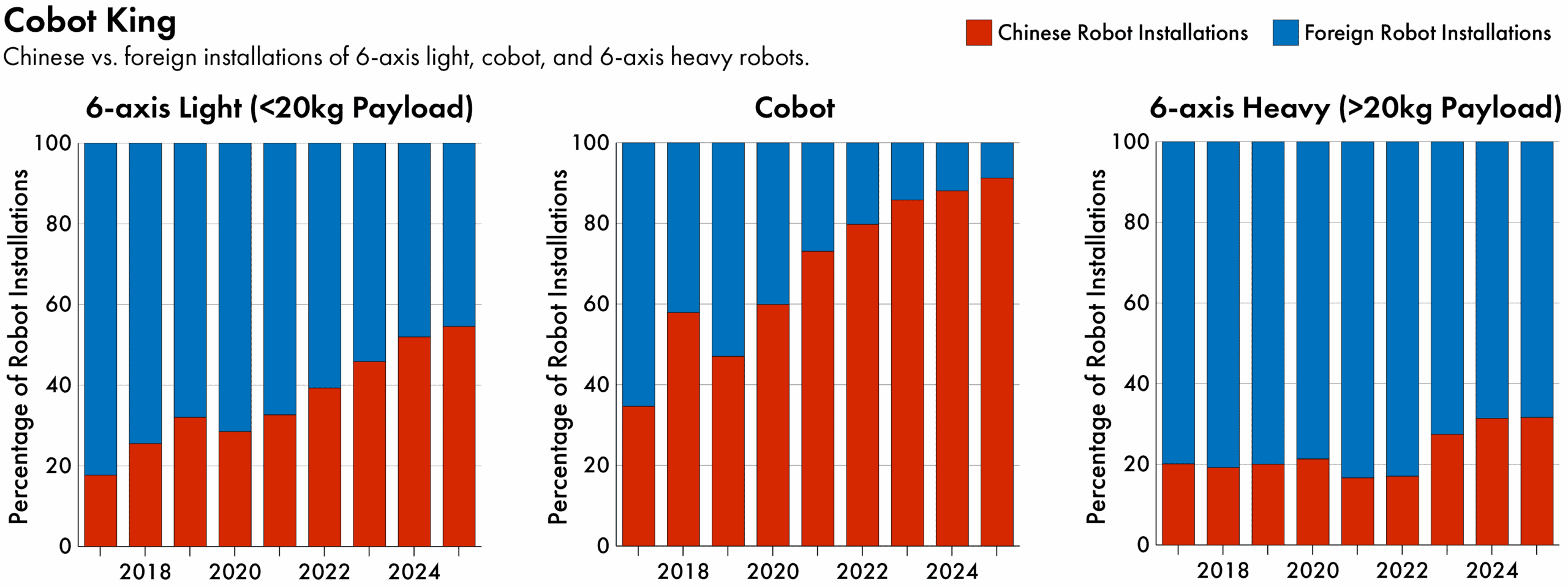

A detailed look at the domestic robot maker share data bears these trends out. The real strength of domestic manufacturers is in collaborative robots, or cobots — designed to work safely alongside people in a shared workspace — where local manufacturers have a market share now close to 90 percent. Unlike traditional industrial robots that typically operate behind fences, cobots have built-in safety features and are easier to program and redeploy. Their typical uses are in pick-and-place, packaging, machine tending, screwdriving, gluing, inspection, lab automation, and kitting.

The Chinese cobot market, as expected, has dozens of players and is extremely aggressive, with serious price competition the norm. Indeed, there are concerns that the low-end robot market in China is in the throes of “involution” (Chinese: 内卷, nèijuǎn), a term that describes an escalating, self-perpetuating competition where companies pour in more time, money, and effort but see little or no meaningful gain — either individually or collectively, a crowded “rat race” with diminishing returns.

By contrast, Chinese manufacturers’ share of the heavy duty (bigger than 20kg payload) robot market has fluctuated between 20 and 30 percent over the last 8 years, and there is no indication of a breakthrough in domestic robot capability. Put simply, Chinese robot makers have failed to achieve the technical sophistication required to build a reliable large duty robot.

What is holding up the Chinese robot industry?

China’s industrial robot makers have grown quickly by offering low- and mid-range machines at attractive prices, helped by government subsidies, tax breaks, and even buying foreign companies. This has led to strong numbers in terms of robots sold. However, they have struggled to match the most advanced foreign brands in quality, performance, and long-term value.

Competing mainly on cost is becoming risky as more players enter the market and undercut each other, similar to what has happened in other Chinese industries like electric vehicles and solar panels, where intense price competition has squeezed profits and slowed real innovation.

The core problem is that Chinese firms have not yet secured or developed enough cutting-edge intellectual property, particularly in the most sophisticated hardware components and software that determine how well robots actually work in demanding environments. Several performance metrics determine the range of demanding applications a robot can reliably perform over its lifetime, and hence the value to the end user.

Most important for advanced uses are point accuracy — which measures how close the robot gets to an exact, absolute position in space; and trajectory accuracy — a measure of how closely it follows a desired path as it moves. Getting them right depends heavily on the robot’s mechanical design: how rigid its structure is, how good its components are, and how carefully it is assembled.

Another key indicator is the ratio of the robot’s own weight to the weight it can safely lift, called its payload. Lighter robots with the same payload are typically faster, more responsive, and better at handling complex, dynamic motions, and they tend to last longer and break down less often.

For Chinese robot makers to escape a low-price trap and become true global leaders, they would need to shift from competing mainly on cost to competing on technology. That means focusing on the “invisible” elements that determine performance…

Electronics and control systems are also crucial. Robots operate in very fast cycles, often needing to measure, decide, and adjust their movements in less than a thousandth of a second. This is done by tightly integrating the control and drive electronics in one system, cutting down on delays. The control system includes embedded algorithms — deeply programmed mathematical rules that convert a planned movement into precise instructions for the motors. These algorithms depend on intimate knowledge of the robot’s hardware and dynamics, which means it is hard to build general-purpose controller hardware and software that can be commoditized, as in PCs.

On top of this, trajectory planning software helps the robot move quickly without crashing into obstacles or getting stuck in positions where its arm cannot move stably, known as singularities. For tasks like bin picking, where robots identify and grab randomly piled objects, this planning must happen in real time.

Application software packages add another layer, tailoring robots to specific jobs such as welding, painting, or palletizing goods. The better companies also provide powerful “offline programming” tools, which allow users to design and test robot tasks in a virtual environment and then transfer them accurately to the real machine.

Foreign robot makers, especially the big four of FANUC, ABB, Yaskawa, and KUKA — a Chinese-owned company which still does most of its product development in Germany — generally outperform leading Chinese brands such as Estun, SIASUN, EFORT, and Inovance across all of these performance dimensions. Foreign firms also offer a wider range of ready-made software packages, with ABB and KUKA each covering more than a dozen applications, whereas Chinese companies tend to focus on a narrower set of core uses.

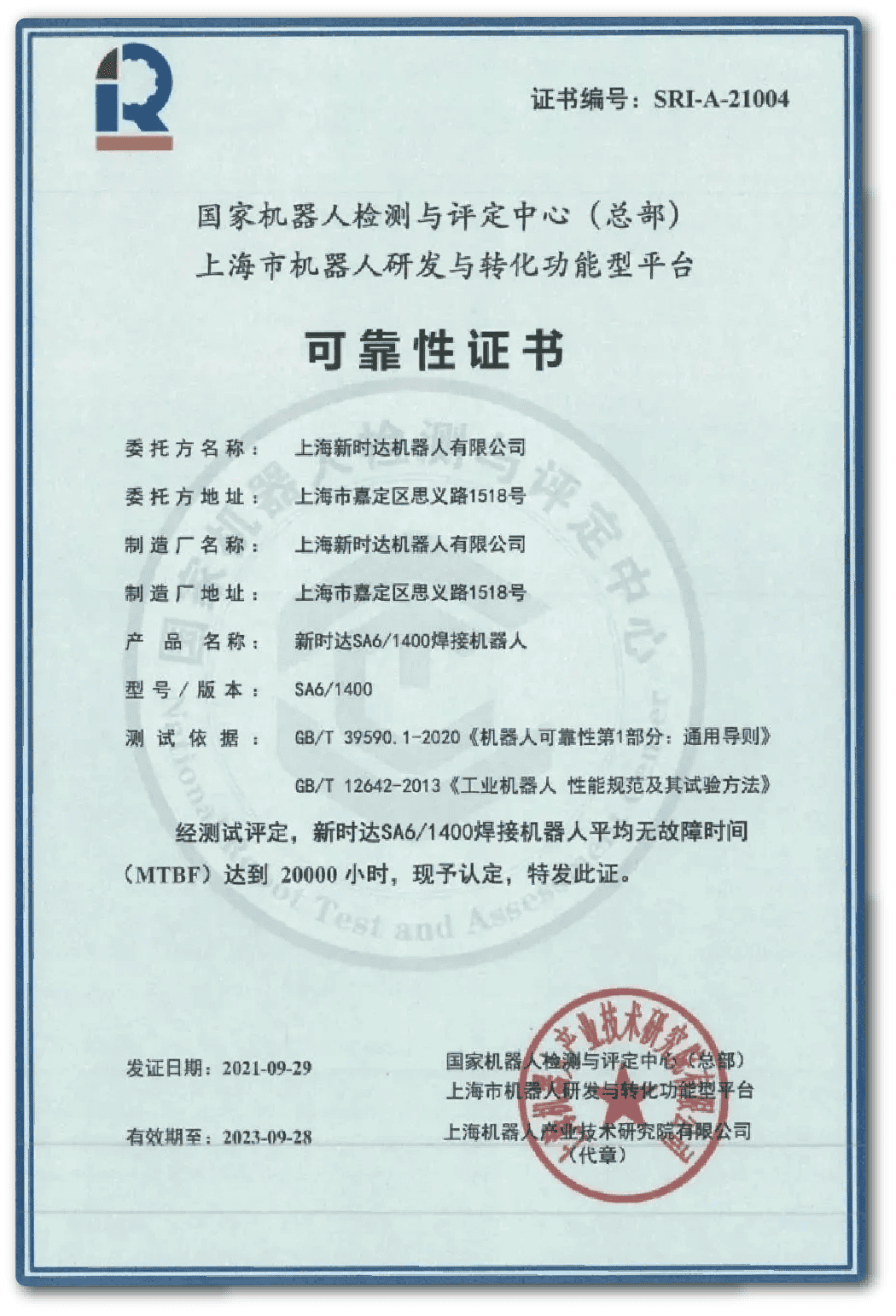

But a robot application not only has to meet stringent performance requirements, it has to be economic to the end user. The difference between an economic and an uneconomic application hinges on reliability, often measured by mean time between failure (MTBF) — the average operating hours a robot can run before a breakdown. Chinese robots typically have MTBF ratings of 20,000 hours, corresponding to 2.3 years of continuous round-the-clock operation, while foreign brands’ MTBF ratings are around 80,000 hours, or over 9 years of continuous operation. This is a meaningful difference in industries where an hour of downtime can cost hundreds of thousands dollars of lost production.

For Chinese robot makers to escape a low-price trap and become true global leaders, they would need to shift from competing mainly on cost to competing on technology. That means focusing on the “invisible” elements that determine performance: high-quality control algorithms, tighter integration between controllers and drives, more accurate models of robot motion and dynamics, better structural design and vibration control, and broader, more user-friendly software tools. They would also need to invest heavily in raising reliability through better components, tougher testing, smarter diagnostics, and stronger after-sales service.

Which begs the question, why haven’t Chinese robot makers managed to master the highest reaches of robot capability, as they have done so in other technologies, such as solar cells, electric batteries, or high-speed rail?

One explanation is that this technology evolution is a work in progress, and we will see Chinese robot makers slowly move up the performance curve, reaching the same dominance in high performance large payload robots as we saw in collaborative robots.

Another explanation is that the Chinese authorities feel no urgency to dominate high end robotics, meaning the pressure on domestic robot manufacturers to meet Made in China targets is not as relentless as it is in semiconductors or biotechnology.

High-end robotic equipment is freely and readily available in China from the leading Japanese and European players, and the industry’s economics dictate that it is better to buy a high-quality robot than to make a technically inferior one. China does not need an import substitution model, as there are no geopolitical barriers to the country acquiring what it needs, unlike those in areas like advanced semiconductor equipment or AI chipsets.

Although the United States has a vibrant robotics startup ecosystem, it is not a major supplier of industrial robotics for mass production applications. Hence it has limited leverage, as Chinese manufacturers do not really buy any robots from the United States. This limited leverage may also be why the United States has not pressured Japan and Europe to limit exports of its high-end robotic technology (as it has done with lithography equipment, in the case of Dutch company ASML). It could also be due to American inattention to an “under the radar” technology transfer.

Either way, the result is that China may not come to dominate the global robotics industry — at least, its most valuable segment — in the same way it has in some many other areas of technology.

Alberto Moel is a Professor of Practice at Hong Kong University Business School. He also been an analyst and consultant for robotics and manufacturing, and an executive at Veo Robotics, a machine vision startup. He can be reached at amoel@hku.hk.