For some time now, the smart take on China’s currency has been that the Chinese authorities have been intervening — but to prop up the yuan not to hold it down. In other words, perennial U.S. complaints about China artificially manipulating its currency to gain a trade advantage were out of date.

That claim itself is now, well, dated. And clearly wrong.

The preponderance of evidence now shows that China is once again intervening to hold its currency down. It is doing so to gain a trade advantage — both to counter U.S. tariffs by exporting more to other markets, and to compensate for China’s own lack of internal demand.

But China is not intervening directly, by adding foreign exchange assets to the balance sheet of the People’s Bank of China, the country’s central bank — as most countries trying to hold their currency down would do.

Instead, China is now relying on the state banks to manage the currency.

Doing so helps China to avoid scrutiny — the International Monetary Fund, for example, doesn’t seem to have caught on to this new method of intervention — and allows the central bank to avoid the domestic criticism that would come if it kept visibly adding to its already huge pile of U.S. Treasury holdings [in the past, the PBOC has bought Treasuries to help stop the yuan appreciating too much].

Here are the key things to know.

China’s trade surplus is now huge. The goods surplus, as reported by China’s customs service, is on track to reach $1.2 trillion this year — up by $800 billion from the $400 billion surplus typical before the pandemic. Chinese tourists travelling to places like Thailand and Japan generate a $200 billion or so offsetting deficit in services. But the total surplus — which combines goods and services trade — is still massive.

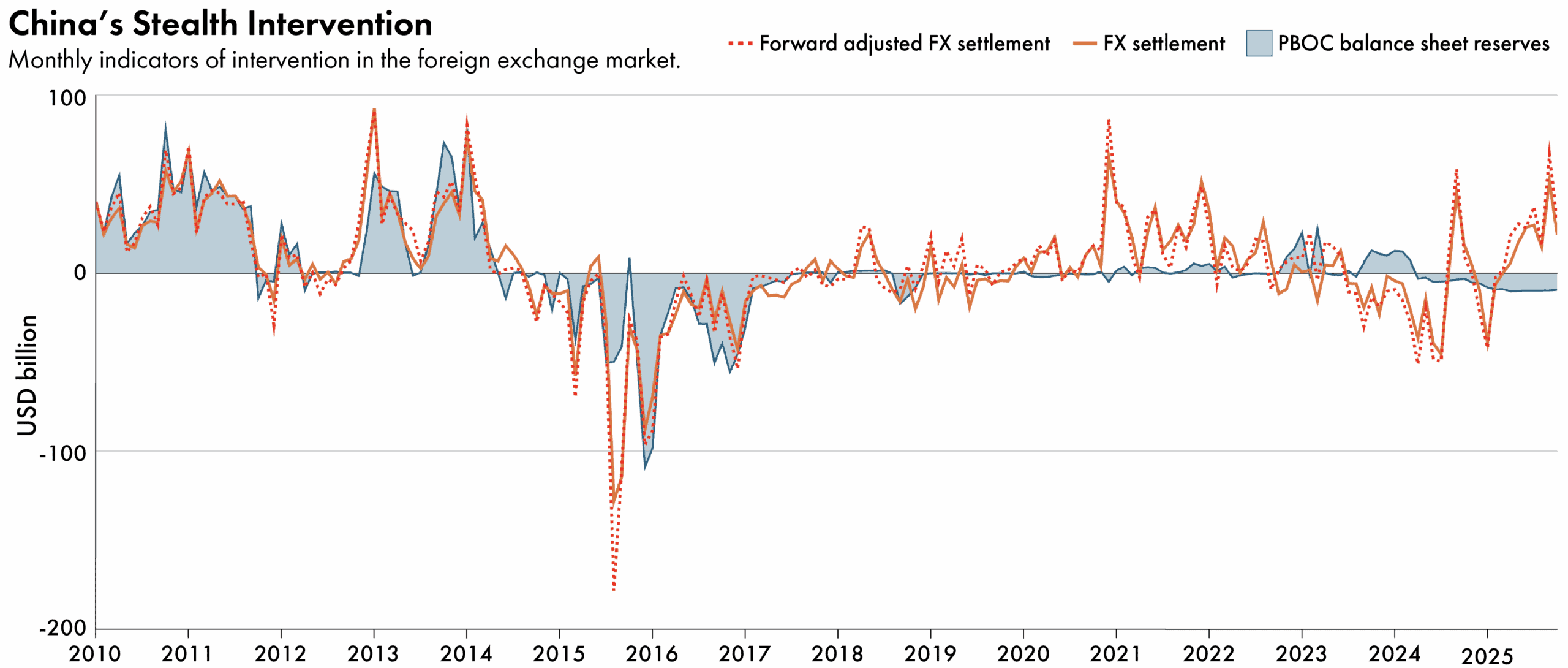

…Chinese state banks are doing the central bank’s dirty work. By building up their foreign exchange piles, they are the ones keeping the yuan from rising in the way it ought to, given China’s monumental trade surplus.

China has masked the true size of its goods surplus in its balance of payments statistics thanks to a methodological change introduced back in 2022 that has mucked up the data. But it can’t hide the impact: China’s own data on how it grows still shows that net exports have added a huge 6 percentage points to its GDP since 2018. That is larger than the growth in China’s trade surplus.

Meanwhile, financial outflows from China have been big, but not big enough to offset the goods surplus. Yes, foreign firms have stopped doing much new direct investment in China, and Chinese firms are investing heavily abroad — especially in southeast Asia. Chinese exporters also like holding dollars abroad, at least so long as the interest rate on dollars tops the interest rate on Chinese yuan.

But those outflows, large as they are, have not been big enough to absorb all of the foreign exchange generated by the trade surplus.

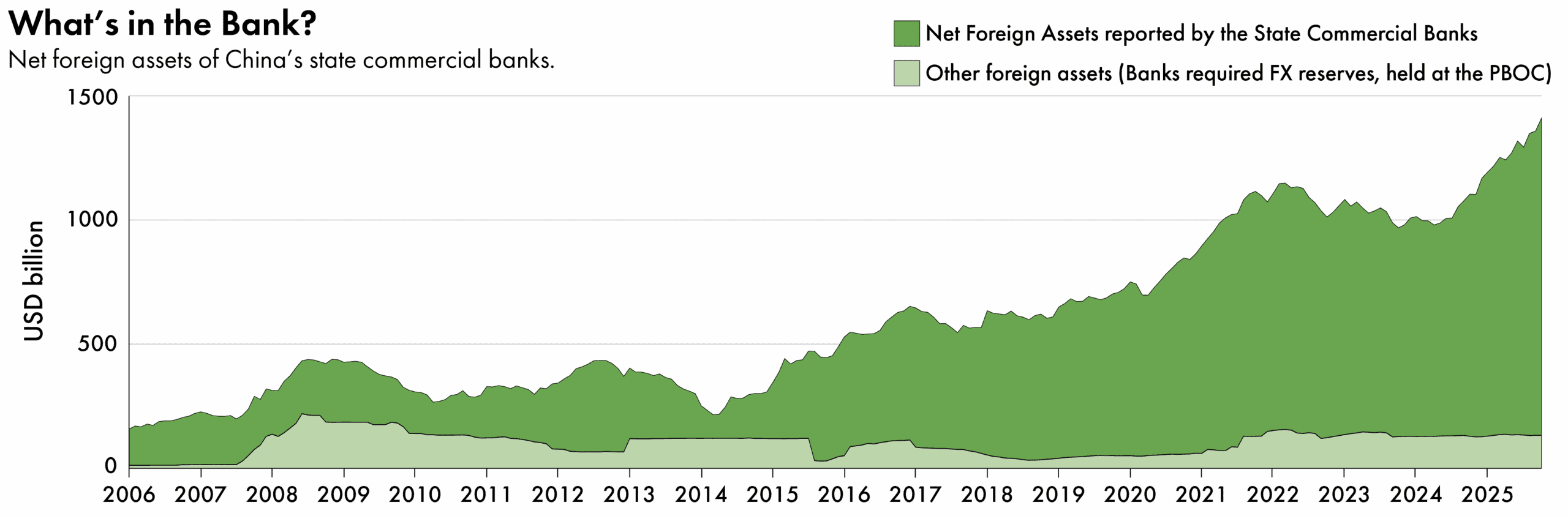

That brings me to the third and crucial point: China’s state-owned banks, including Industrial & Commercial Bank of China (ICBC) and Bank of China, have once again resumed adding to their substantial foreign assets. The state commercial banks now collectively have $1.4 trillion in foreign assets, relative to only $200 billion in foreign liabilities. These banks are on track to add $300 billion to their foreign assets in 2025, and the bulk of that is likely to be in foreign currency. A separate data set shows the banks are on track to buy about $250 billion in foreign exchange — net of the PBOC’s reported sales (themselves a bit of a mystery).

That’s a big increase. And there could be up to $1 trillion of additional foreign assets on the books of the two big policy banks, the China Development Bank and the Export-Import Bank, which aren’t reported in the state banking data.

This big national foreign exchange book is being funded domestically — out of domestic foreign exchange deposits at the state commercial banks, and through more mysterious methods for the policy banks: Ask the PBOC about the “diversified use” of its foreign exchange reserves.

All this fits well with what we know from credible third parties. AIDdata has shown that the external loans of China’s state commercial and policy banks now reach $2 trillion, and the Bank for International Settlements reports total external assets of the Chinese banks are approaching $3 trillion.

Now the exact mechanics of China’s backdoor intervention in the foreign exchange market remain a bit of an enigma — one that the IMF hasn’t cracked.

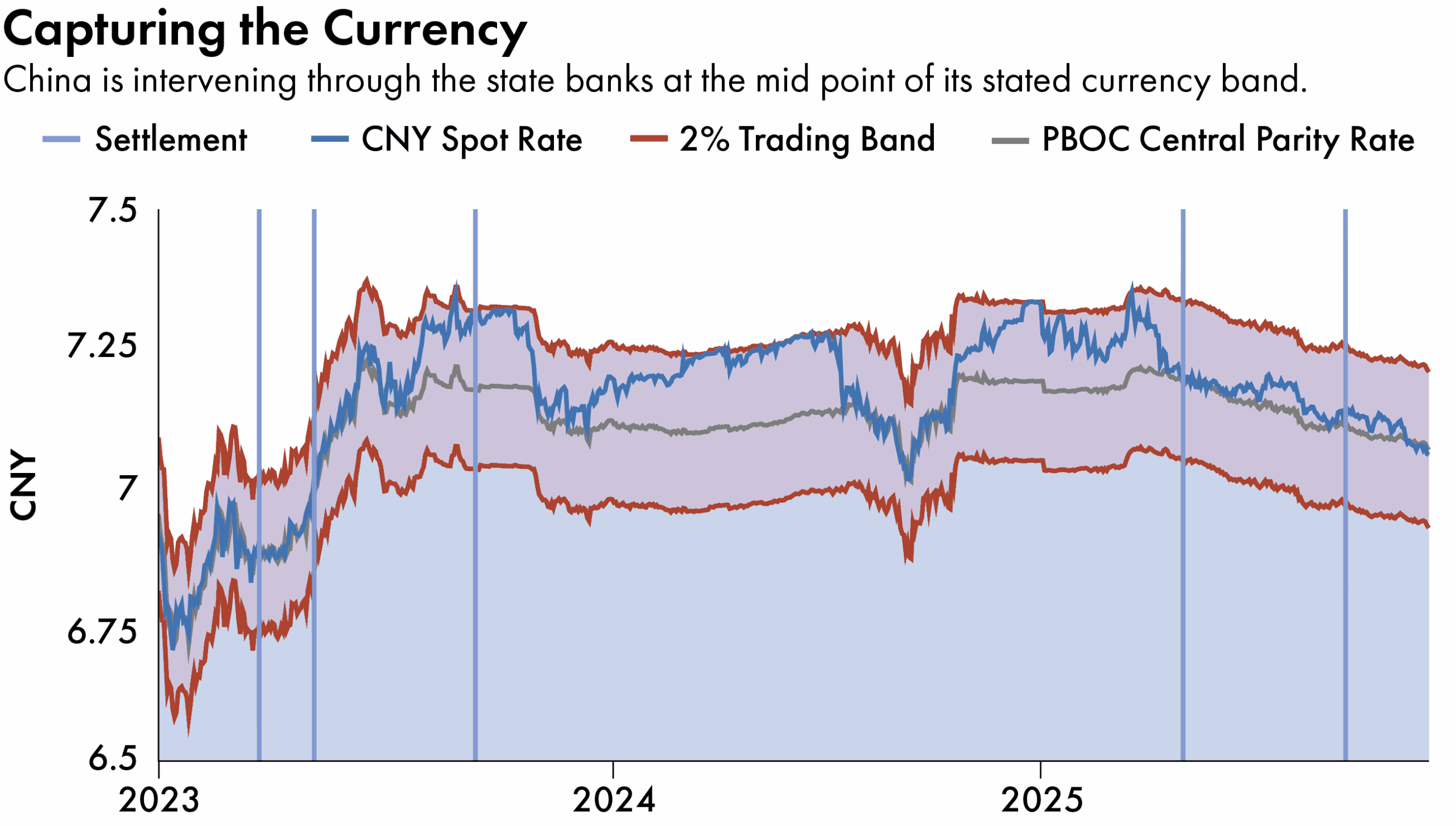

But here is what seems to be going on — rather than intervening directly or giving direct orders, China’s central bank sets the daily fix so as to signal to the state banks when they should intervene [China’s central bank sets a daily number for the yuan/dollar exchange rate around which the currency can trade]. The banks are then expected to keep the yuan from depreciating by more than 2 percent below the fix — whether by denying customers access to foreign exchange or drawing on their balance sheets. And the state banks are also apparently expected to buy foreign currency to keep the yuan from trading above the daily fix.

A smart, American manufacturing first administration would make common cause with the rest of the G-7 to press China to bring down its outsized trade surplus — and that, fundamentally, means letting market flows strengthen the yuan.

The strong half of the band hasn’t been used in a couple of years — there is not even any real effort to disguise the direction of China’s currency management these days. And foreign exchange settlement — the best indicator of backdoor intervention — tends to spike up when the onshore currency market trades close to the fix.

Bottom line: the Chinese state banks are doing the central bank’s dirty work. By building up their foreign exchange piles, they are the ones keeping the yuan from rising in the way it ought to, given China’s monumental trade surplus.

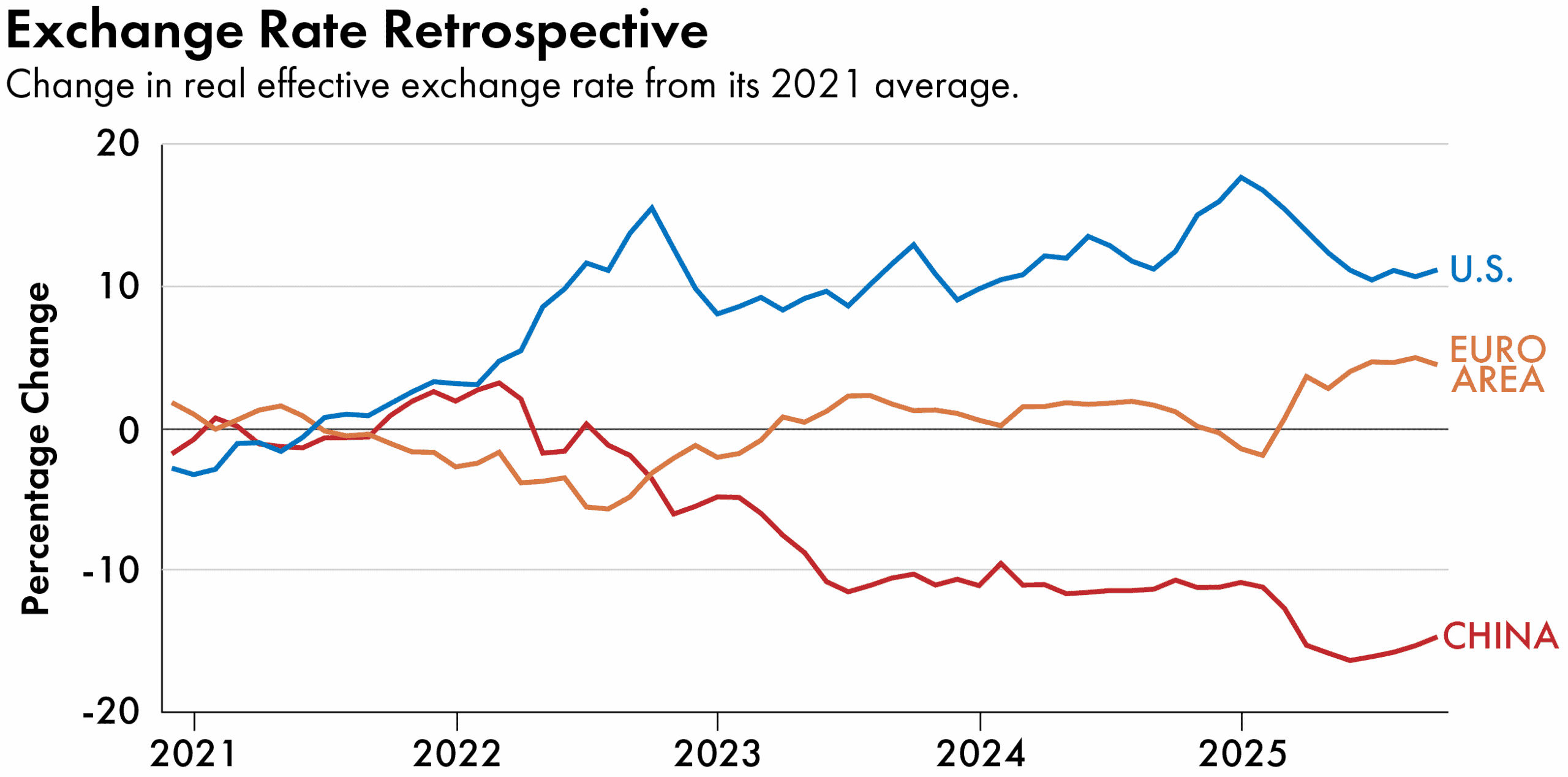

Most of the G-7 countries have now taken note of the yuan’s weakness. When the yuan followed the dollar down earlier this year the Europeans started to worry. China’s trade surplus with Europe was exploding — and global trade data shows that China’s export outperformance has largely come at Europe’s expense. France now wants to make global payments imbalances the focus of its G-7 Presidency in 2026.

Meanwhile, Treasury Secretary Scott Bessent, somewhat strangely, has given China a free pass to intervene to keep the yuan down, as he kept his focus on securing Chinese soybean purchases and access to rare earths — a significant oversight. A smart, American manufacturing first administration would make common cause with the rest of the G-7 to press China to bring down its outsized trade surplus — and that, fundamentally, means letting market flows strengthen the yuan.

Brad W. Setser is the Whitney Shepardson senior fellow at the Council on Foreign Relations (CFR). His expertise includes global trade and capital flows, financial vulnerability analysis, and sovereign debt restructuring.