Gracelin Baskaran, the director of the Critical Minerals Security Program at the Center for Strategic and International Studies in Washington, is a leading expert on the elements buried in the Earth’s crust and how they affect the global economy. The International Energy Agency estimates that China controls 60 percent of the global mining and 90 percent of the refining of rare earths, which are vital components in goods such as semiconductors, engines, and missiles.

We spoke shortly after the United States and China last week agreed to a deal in which Beijing will delay for a year imposing an extensive rare earths export control regime. Washington in return agreed to lower tariffs on China and postpone its own expansion of a trade blacklist that would have affected thousands of Chinese companies. During our conversation, which has been lightly edited, we discussed how the United States is seeking to reduce China’s control over the rare earth supply chain and whether these efforts are likely to succeed.

Illustration by Lauren Crow

Q: Is the U.S. right to trade lower tariffs and expanded export controls in exchange for China postponing its own export controls on rare earths?

A: Yes. It is in both Washington’s and Beijing’s interest to cool tensions. The U.S. depends on access to rare earths and permanent magnets for its defense industrial base, economic competitiveness, and energy resilience. China, meanwhile, needs urgent tariff relief as its economy faces one of the deepest deflationary spirals in modern history, compounded by high youth unemployment, stagnating growth, and a collapsing property sector. Of course, the United States will not back down in its efforts to warp speed the development of resilient supply chains to insulate critical industries from future coercion.

How much difference will another year of the U.S. and its allies having access to Chinese rare earths make in their efforts to bring back their own industries for these elements?

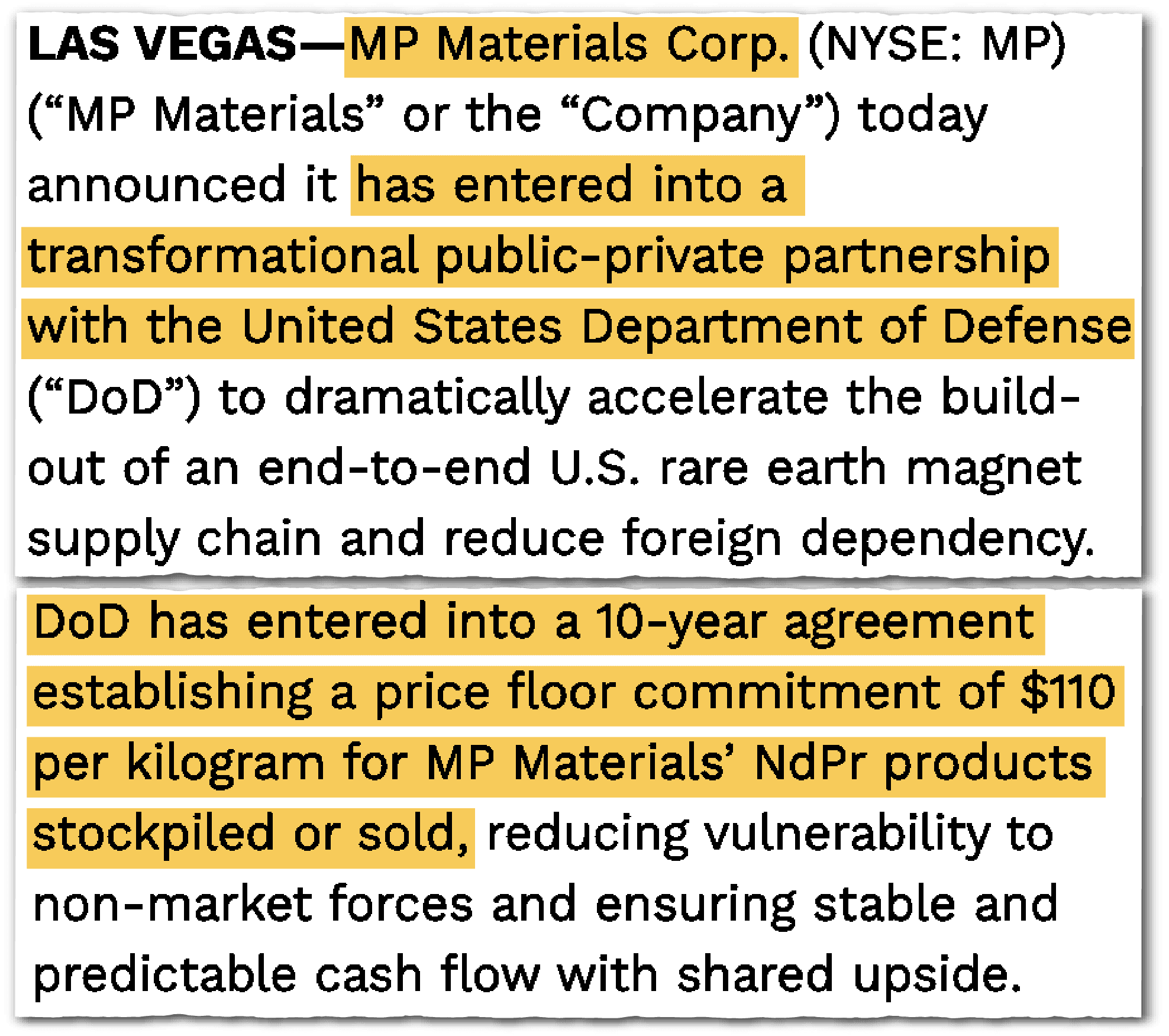

A year helps. The United States is far ahead of where it was just twelve months ago. Who could have imagined that the U.S. government would become the largest shareholder in America’s leading rare earth company? Certainly not me. [In July, the Department of Defense invested $400 million in Las Vegas-based MP Materials, which owns the only significant rare earths mine in the United States.] The truth is, we won’t be self-sufficient a year from now, but we will be less dependent.

| BIO AT A GLANCE | |

|---|---|

| AGE | 33 |

| BIRTHPLACE | Galveston, Texas (but I moved to Michigan pretty young and call it home!) |

| CURRENT POSITION | Director, Critical Minerals Security at the Center for Strategic and International Studies and Adjunct Associate Professor at Georgetown University |

Still, the hardest work lies ahead. Building secure supply chains means building people: engineers, miners, metallurgists, and technicians who can power this industrial revival. By 2029, the U.S. is projected to lose 221,000 mining workers, amounting to half of today’s domestic workforce. To secure our future, we must invest not only in projects and plants, but in people and permanence — the long-term foundations that will sustain this industry for generations to come.

How long can Beijing keep playing the rare earth card before the rest of the world develops a supply chain that excludes China?

China has already overplayed its hand. Over the past year, as it has repeatedly imposed and tightened rare earth export controls, countries around the world have begun fast-tracking their own capabilities. Australia, Saudi Arabia, Brazil, the United States, Japan, and Malaysia are all moving at remarkable speed to develop alternative supply chains. With China’s rapid escalation of restrictions, several rare earth production and processing networks are now taking shape outside of its borders.

But are those supply chains currently capable of replacing China as a source of supply, or does it still have this rare earths ace card in trade negotiations?

Some of these capabilities have already started coming online slowly. The first heavy rare earth processing facility outside of China came online earlier this year when [Australian company] Lynas started separating Australian heavy rare earths in Malaysia. The United States has one company already manufacturing permanent magnets here [Texas-based Noveon Magnetics].

Globally, what we’re starting to see is we’re ramping up capability. So are we self-sufficient now? No. And does China retain short and medium-term leverage? Yes. But in the same stroke, we are rapidly bringing new capabilities online to ensure that this vulnerability does not continue.

Did Beijing’s increasing willingness to play this card accelerate the creation of an ex-China supply chain?

It was shortly after China imposed the April 4 rare earth export restrictions that the United States announced that it would become the biggest shareholder in MP Materials. Around the same time, Washington deployed an unprecedented set of policy tools, including price floors, concessional financing, equity investments, and guaranteed offtake agreements, to strengthen MP Materials and other mining companies. All of these measures were designed to blunt the impact of China’s export controls. There’s a global trend here: as China tightens its grip on rare earth exports, other nations are accelerating efforts to build more secure and resilient supply chains.

Given China’s export controls, is it possible that measures like price floors and equity stakes mean taxpayers will end up propping up firms that aren’t internationally competitive, if they can’t get the technology that they need to process rare earths?

It’s a strategic imperative to support industries vital to our national and economic security. Fiscal support isn’t designed to be permanent; it’s supporting a nascent industry until it has the legs to be commercially viable on its own. It’s common practice. In their early days, Japan subsidized Honda and Finland subsidized Nokia.

…China’s relationship with the U.S. is highly volatile. This year, there have already been at least three rounds of negotiations with China to restore access to minerals and magnets. No solution has remained permanent… Even if things improved in the short term, it is not a relationship that you would trust or put all of your eggs back into that basket.

Historically, the U.S. has provided significant support to sectors to ensure the stability of our supply chains. Back in 2007-08 we provided a significant bailout to the U.S. automotive industry, in the order of many billions of dollars. In May 2025, that same automotive industry had to stop manufacturing operations because of a rare earths shortage. By supporting the development of a domestic rare earth and permanent magnet industry, we are helping avoid another bailout when they halt production long-term.

We are already seeing that this industry is becoming more economically viable. The $400 million equity investment in MP Materials is now worth over $800 million. There’s no indication that taxpayers are losing money. Instead, we are supporting a nascent industry that, once it is commercially viable, will give taxpayers a return on investment while also ensuring we have a reliable supply of minerals here in the U.S. It’s a win-win.

How did the U.S. lose its lead in the global production of rare earths?

A British comedian once quipped, “there’s no such thing as new news, just old news happening to new people,” and that perfectly captures what we’re seeing today. If you look back to 1910, the U.S. established the Bureau of Mines to oversee domestic and international mining — from extraction and processing to R&D and geological data — ensuring American leadership in the field. The Bureau played a critical role in ensuring we had the minerals we needed for World War II, the Vietnam War, Korean War, etc. But when the Bureau was shut down in 1996, it symbolized a wider deprioritization of mining across the country. That deprioritization was likely part of the broader peace dividend (the tendency to shift resources away from strategic industries, such as mining and manufacturing, during periods of relative peace and stability).

| MOST ADMIRED |

|---|

| My dad arrived in the United States from India in 1987 with just $20 and a dream of something more. Against all odds, he became the first in his family to attend university — then earned a PhD in Physics. His story is one of grit, sacrifice, and an unshakable belief that a better life was possible. |

Regardless, while the U.S. was stepping back, China was stepping up. Beijing launched an aggressive foreign policy to secure mineral resources, including rare earths, worldwide, while simultaneously investing heavily in its domestic refining industry. That dual strategy gave China a commanding advantage — one it has maintained for over three decades.

We’re now back in a period of potential conflict, particularly in the Indo-Pacific, but without the reliable access to rare earths we need to build our defense industrial base.

Is processing the biggest challenge for the U.S. and its allies to reshore rare earth supply chains? How did China get so dominant in processing in particular?

China has really prioritized building up its processing capacity. Rare earth processing is pretty environmentally unfriendly. Producing a ton of rare earths generates approximately 13 kilograms of dust, between 9,600 and 12,000 cubic meters of waste gas, 75 cubic meters of wastewater, and one ton of radioactive residue. That’s substantial. Historically, the United States has taken a “not in my backyard” approach, preferring that this type of processing occur elsewhere. China, meanwhile, has been willing to absorb those environmental costs. And the rest of the world, by and large, was content to let it.

Chinese firms have also been willing to produce a lot more, bringing down the price of rare earths. How much of a factor was a decline in rare earths prices in the loss of the domestic U.S. rare earths industry?

Overproduction has been a key part of China’s rise to dominance. Across various critical minerals, China has surged production, thereby depressing prices and forcing western companies out of business. In recent years, however, Beijing has had to confront the reality that it cannot sustain large-scale production at a commercial loss indefinitely. Even China has begun idling some mines to stem financial losses. Still, its state-backed model has allowed it to withstand prolonged losses far more easily than market-driven Western firms.

One thing that’s become apparent over the past six months is the way that rare earths have become part of China’s economic arsenal. Back in the 1990s, as it was building up its rare earths industry, did it foresee the day that rare earths would become a part of its international economic toolkit?

Minerals played a central role in China’s economic growth model, fueling years of double-digit GDP growth rates. China didn’t just extract and process them. It used them to become a manufacturing superpower.

| MISCELLANEA | |

|---|---|

| FAVORITE BOOK | Chip War by Chris Miller is a good one. |

| FAVORITE MUSIC | Country |

| FAVORITE FILM | I’ll admit it’s a little cheesy, but I absolutely love Holiday in the Wild. |

It wasn’t until 15 years ago, when China got into a dispute with Japan over a fishing trawler, that it began weaponizing these minerals by cutting off rare earth exports. We really should have woken up to the challenge at hand then. But we didn’t until China began using them for a whole basket of minerals starting in 2023. That’s the great tragedy here. This was largely avoidable.

The direction of U.S.-China relations right now seems fraught, but if ties improve, what is stopping buyers from sourcing rare earths from Chinese companies again, especially if they’re willing to sell for less?

No company wants to be on the other end of a supply chain disruption because President Xi Jinping woke up and decided to cut off access to the United States. Companies recognize that the U.S.-China trade relationship is highly volatile. We’ve already had three public rounds of negotiations to restore access to minerals this year and no solution has proven to be permanent. The pattern has been a constant back-and-forth of tightening and easing restrictions. Even if conditions improve temporarily, it’s not a relationship companies can rely on. The disruption became so severe that production of the Ford Explorer in the U.S. had to be halted due to material shortages. So now, companies like General Motors and Apple are prioritizing supply chain security, even if it means paying a premium to avoid future disruptions.

How complicated will it be for the U.S. to rebuild its own rare earth industry? And how much will it cost?

I don’t think there’s a single, definitive cost. The real question isn’t whether it’s difficult, because we’re already doing it. Heavy rare earth separation and permanent magnet production are now happening outside of China. The real issue is timing — how long it takes to scale-up to be self-sufficient. Mining isn’t an overnight industry; developing and expanding mines, processing plants, and separation capacity requires years of investment and construction. So the challenge isn’t capability. It’s the pace of ramp-up.

How critical is working with allies to this effort to develop secure supply chains in the rare earths?

There’s a reason that minerals are now at the center of nearly every major U.S. foreign policy move in 2025 — from Ukraine and the DRC to Saudi Arabia, Japan, and Australia. The reality is simple: America cannot achieve minerals security on its own. Securing reliable supply requires access to high-quality, economically viable deposits, which is shaped by the depth of the reserve, ore grade, and the value of byproducts. And many of those critical resources lie within the territories of our closest allies. We’re stronger when we approach this collectively by combining our capital, technical know-how, and infrastructure to harness our shared strengths and build a more resilient global supply chain.

Is it possible that the U.S. or its allies could make technological advancements that make rare earths less important?

Of course. The U.S. comparative advantage is not in mining or processing. It’s in innovation. The Manhattan Project allowed us to develop the world’s first atomic weapons and we developed a Covid-19 vaccine in under a year for a virus we didn’t know existed. We have the best research labs and universities on the planet here in the United States.

We’ve already seen that innovation will reduce the amount of primary material we will need. BMW now has an engine that doesn’t need magnets made with rare earths — a clear sign of what’s to come. We’re learning how to substitute materials, use less of them, and recycle more effectively. These are the areas where I expect to see the most progress in reducing reliance on primary raw materials.

Noah Berman is a staff writer for The Wire based in New York. He previously wrote about economics and technology at the Council on Foreign Relations. His work has appeared in the Boston Globe and PBS News. He graduated from Georgetown University.