The U.S.’s latest attempt to contain China’s chip ambitions lasted little more than a month.

Back in May, the Trump administration introduced a ban on exports of electronic design automation (EDA) software to China, a suite of tools used by chip designers to create the blueprint for semiconductors before they go into production. The ban targeted a major chokepoint in China’s chipmaking sector, given the country’s heavy dependence on foreign software.

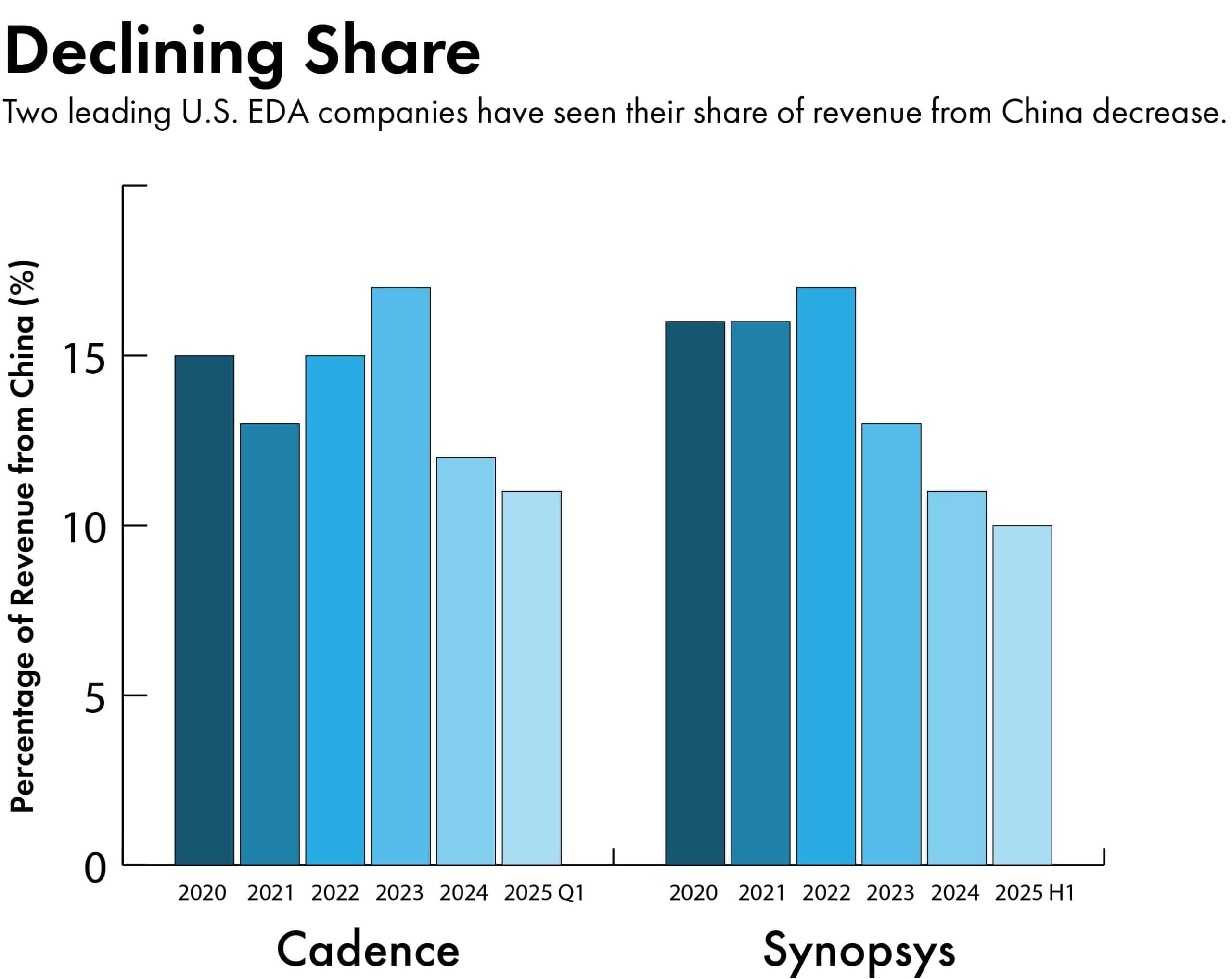

But following the most recent trade truce with China inked late last month, the Trump administration has rolled back its restrictions. Industry leaders such as the U.S.’s Cadence and Synopsys — which both have large businesses in China — announced earlier this month that they would restore access to affected customers there.

In return, China’s market regulator on Monday greenlit Synopsys’s $35 billion acquisition of Ansys, a Pennsylvania-based company that specializes in simulation software, on condition that it doesn’t discriminate against Chinese clients.

The easing of the restrictions on EDA exports has come as a relief to the U.S. companies and their Chinese customers. But it may be too early to celebrate.

While the temporary ban gave Washington some leverage in the most recent trade negotiations, it has also served as a fresh wake-up call for the Chinese semiconductor industry to get its act together on EDA. As a result, Western companies could soon face greater competition in the country, where their Chinese counterparts are on the rise.

“China presents significant revenue for Western EDA companies that can’t be easily replaced elsewhere,” says Woz Ahmed, a former semiconductor executive and managing director of the consultancy Chilli Ventures. “Secondly, they know that each time they’re leaned on by the U.S. government, it’ll only speed up Chinese efforts to replace them.”

EDA software has long been one of the weakest links in China’s indigenous semiconductor supply chain. One expert says chip designers without access to such software are like an artist trying to create a digital picture without being able to use a tool like Photoshop.

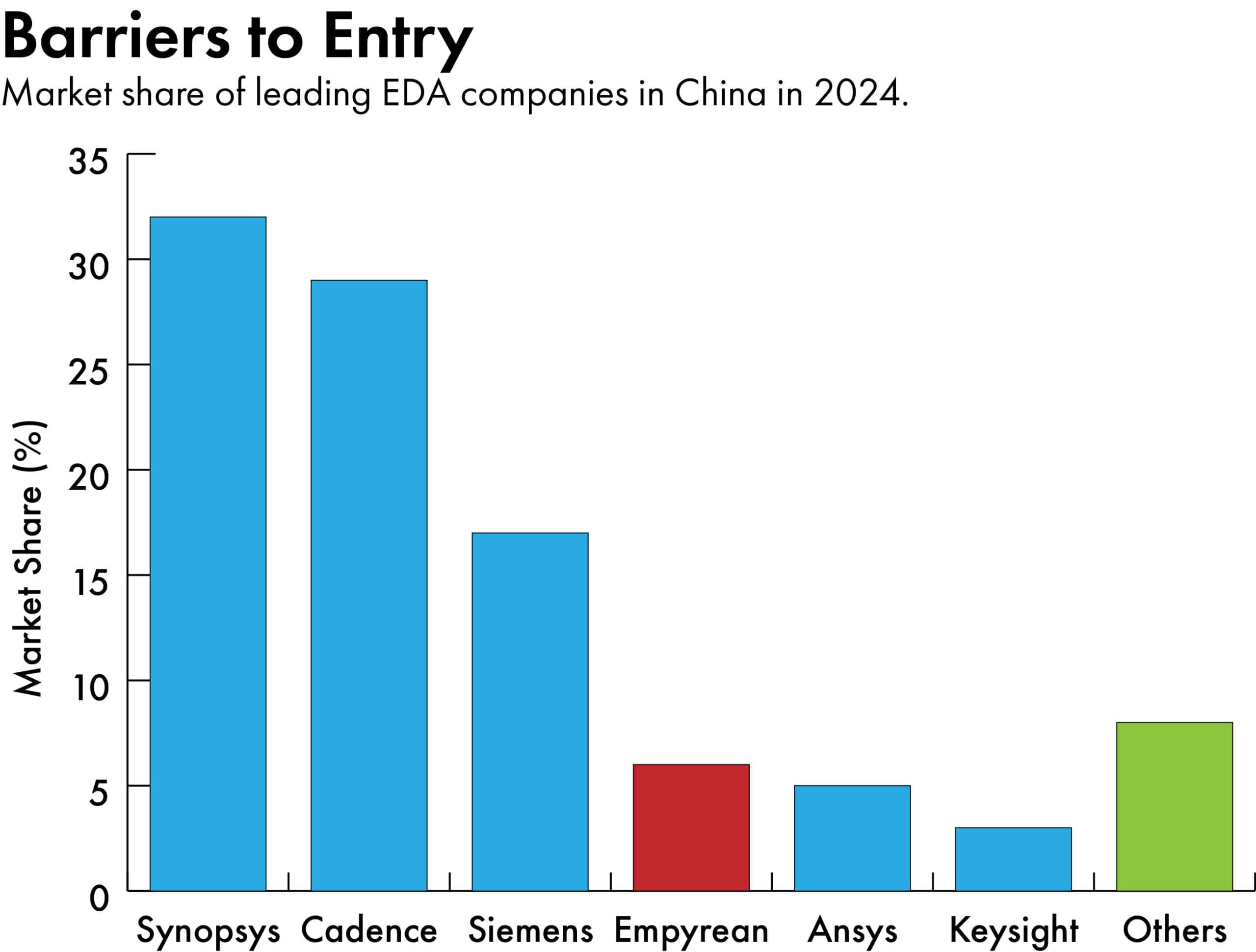

The industry’s Big Three – Cadence, Synopsys, and the U.S.-dominciled Mentor Graphics, which was acquired by Germany’s Siemens in 2017 – currently hold around three-quarters of the global market, according to Trendforce, a market research firm based in Taiwan. They gained that dominant market leadership in part through continuous consolidation over the past few decades, buying up emerging competitors and their technology.

By comparison, only 10 percent of chip designers based in China use locally developed EDA tools, Trendforce estimates. Empyrean Technology, a state-owned domestic champion, accounted for only 6 percent of the Chinese market last year, according to a Chinese securities firm.

China has been trying to change that since 2019, when the U.S.’s blacklisting of Huawei — and its consequent loss of access to American EDA software — exposed the country’s vulnerability and galvanized the government and industry to take action. More than a hundred Chinese startups have since emerged, up from a dozen five years ago, with many founded by former employees of Cadence and Synopsys.

Shares in several of the Chinese companies that are listed rose after the U.S. imposed its export ban in May, amid expectations they would act to further accelerate the self-sufficiency drive. UniVista from Shanghai, for instance, has offered free trials to Chinese users on the back of the ban.

The Chinese government is also lending a hand: It is devoting the third phase of its national chip investment fund – targeted at $47.5 billion – to resolving chokepoints like EDA, Bloomberg reported last month.

“In the past, Chinese firms felt that using indigenous EDA tools was not as convenient as foreign ones,” says Zhang Guobin, founder of Eetrend, a website that tracks the Chinese tech industry. “After the latest ban, they realize even if they don’t adopt domestic EDA immediately, they must have it as a backup.”

“China’s made impressive progress. But it’s not yet enough to fully replace the Western EDA giants.”

Jimmy Goodrich, senior advisor for technology analysis to the RAND Corporation

Experts say Chinese companies still lag behind industry leaders in terms of both capability and scale. Unlike in the U.S., where these tools are concentrated in the hands of a few giants, the Chinese industry is still relatively fragmented. Empyrean is the only Chinese player that has a full suite of tools that can be used to design analog and mixed signal chips, which are used to process signals such as sound and temperature or manage power in electronics. None yet has a comprehensive solution for digital chips, which drive modern computing.

Still, Chinese companies have already collectively developed sufficient domestic alternatives to most basic tools to cover the entire chip design flow, according to Zhang, enough so that losing access to foreign EDA software would not be fatal to the industry.

“It just simply means a Chinese client may have to work with a few more EDA firms instead of one,” he says.

The consolidation now starting to happen in the Chinese industry is another sign of a maturing market. In April, Primarius Technologies, a leading Chinese EDA company from Shanghai that is privately owned, snapped up Chengdu Analog Circuit Technology, a smaller firm known for its valuable IP, for an undisclosed sum. The deal was the latest in a string of acquisitions by Primarius to grow its portfolio.

Similarly, since going public in 2022, Empyrean has acquired XinDA Automation Design, a Hong Kong company that specializes in the verification of mixed-signal circuit designs, and has taken stakes in a few other firms — although it faced a recent setback after a deal to take over Xpeedic, a firm that excels in simulation, fell through last week.

Some smaller Chinese startups are aiming to gain market share by specializing in specific areas of EDA software, such as chiplets – small, modular integrated circuits that have distinct functions and are more customizable.

An online tutorial for Aether, a software developed by Empyrean Technology. Credit: Video via bilibili

Their goal is to avoid direct competition with homegrown mainstream players as well as the Western behemoths. “This is what I would always recommend to startups, look at that one problem which you can solve better than someone else,” says Mike Demler, an independent consultant who has spent decades in the EDA industry. “Don’t try and tackle the whole thing.”

Many are counting on AI to improve efficiency, hoping that the integration of machine learning could help them catch up to or even surpass their foreign counterparts.

“While foreign giants are still accelerating on the original track, we are already running in a new lane,” Liu Weiping, chairman of Empyrean, said in an interview earlier this month.

Leapfrogging incumbents is an ambitious goal, says Demler, adding that “[Chinese companies] may have an opportunity as they’re starting with a blank sheet of paper to develop a model specifically for some steps in the integrated circuit design process.”

Despite the momentum, Chinese EDA companies still face a major limitation in developing the advanced tools needed for semiconductors with smaller and more complex nodes, such as the chips that power AI. Whether they can eventually move towards designs for high-end chips depends on their access to leading foundries like TSMC, whose knowhow and support is crucial.

“Where China has a challenge is EDA for advanced logic and memory chips, and EDA used in the manufacturing process, particularly for optimizing things such as lithography tools,” says Jimmy Goodrich, senior advisor for technology analysis to the RAND Corporation.

“China’s made impressive progress. But it’s not yet enough to fully replace the Western EDA giants,” he says.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.