From coffee to cars, intense price wars have broken out across several Chinese industries, driving down the costs of various consumer goods and contributing to the slide into deflation in the world’s second-largest economy.

This week, The Wire takes a look at how low prices have become for Chinese shoppers, and the knock-on effects for the broader economy.

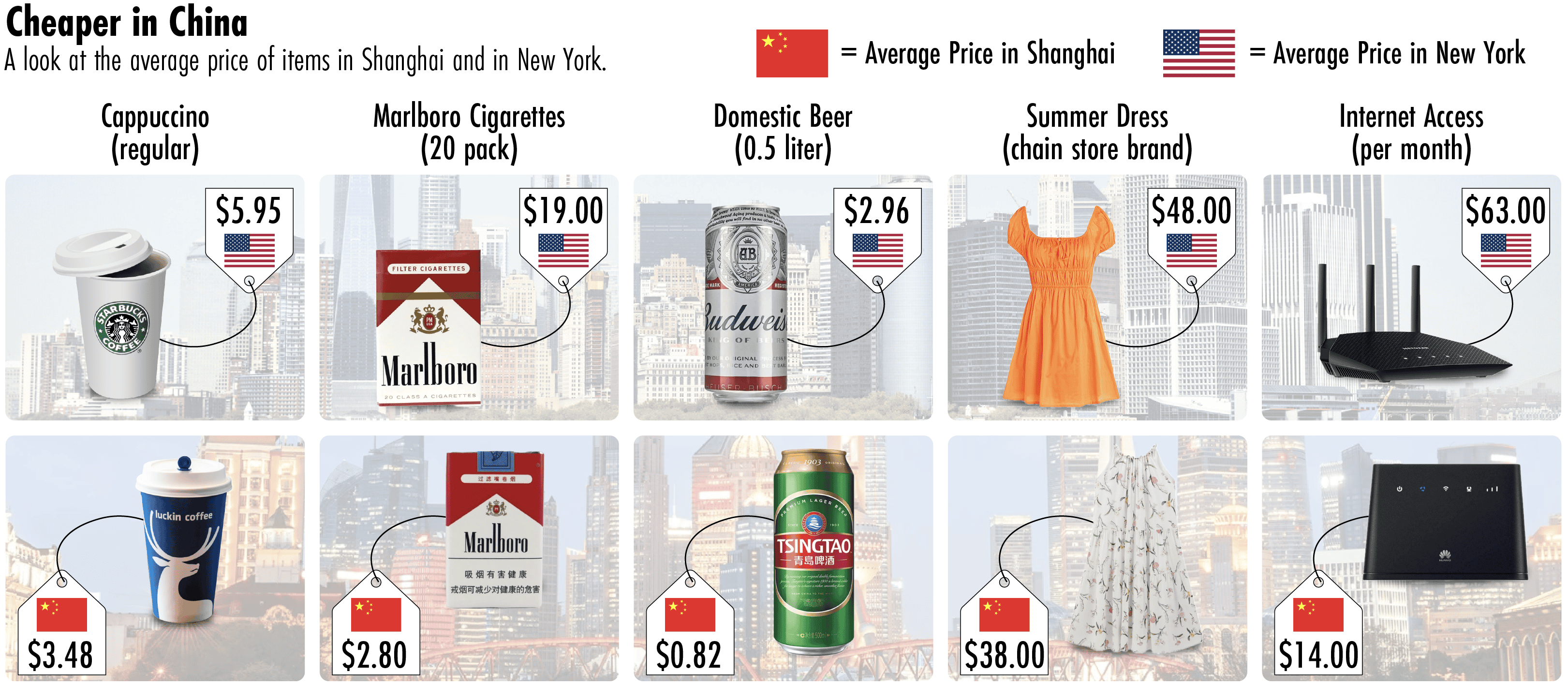

Shanghai may have earned a reputation as the ‘New York of China’, but when it comes to consumer expenses, the two cities diverge — as the graphic above shows. The data is taken from a new report from the Deutsche Bank Research Institute comparing the cost of living across 69 leading global cities.

To illustrate how much prices can differ, the institute has created a “cheap date” index: how much it would cost in various cities for a night out including a meal for two in a mid-range restaurant (plus a bottle of wine and coffees), cinema tickets, transport to the date — and a 5km taxi afterwards — plus a new pair of jeans and a dress beforehand.

Based on Deutsche’s figures, a date like this would indeed be pretty cheap in Shanghai, costing just $173 — placing the city at 54th among the nearly 70 cities surveyed (Beijing is even cheaper at $161). A comparable night out in New York — sixth on the list — would cost twice as much at $354, although that’s still some way below top-ranked Geneva, where a quiet night in might be preferable. A Deutsche-defined cheap date there costs an eye-watering $471.

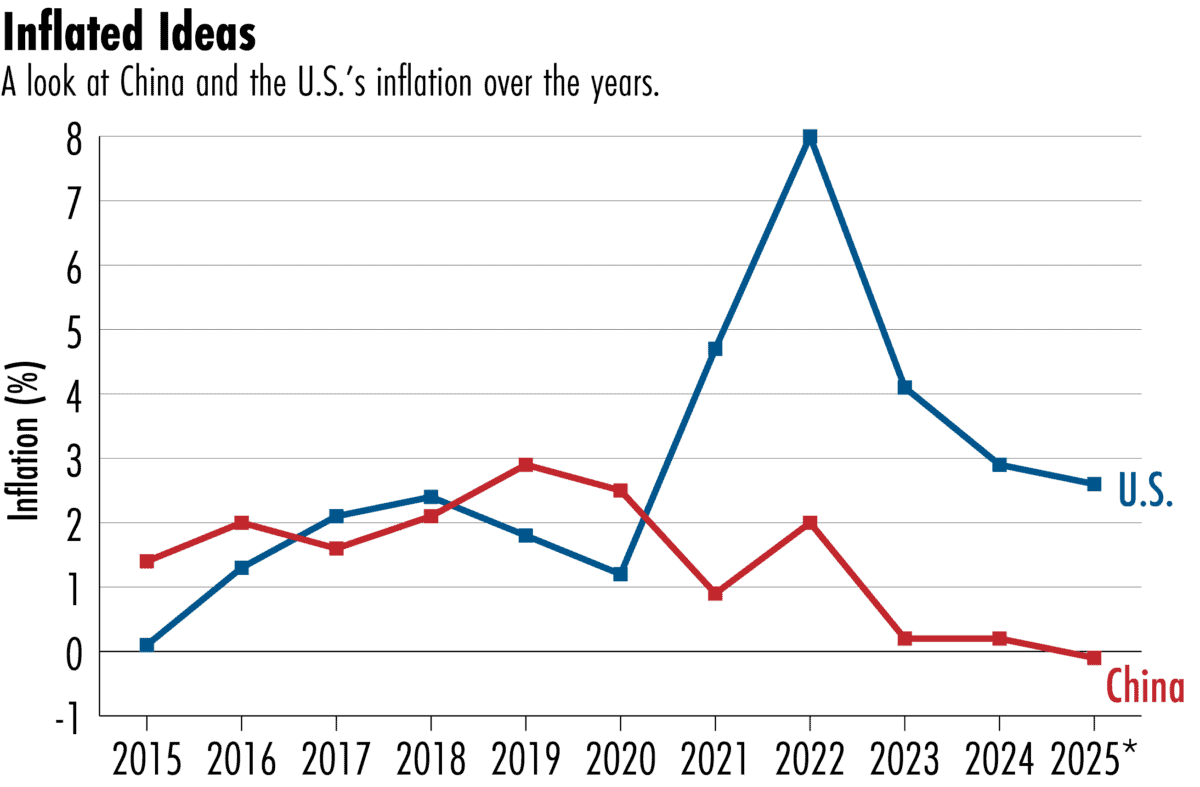

Just as striking is how far prices have fallen in China. That cheap date in Shanghai would have cost $258 back in 2012, meaning it’s now one third less expensive. By contrast, a cheap date in New York now is over 40 percent higher than it was back then.

The contrast is indicative of the divergent paths inflation has taken in the United States and China in recent years.

Chinese goods have long been cheap due to a variety of factors including the relatively low cost of labor and financing for companies. Even so, the country has experienced notable deflationary trends over the past decade.

Consumer behavior started shifting particularly at the end of the Covid-19 pandemic, notes Yaling Jiang, Chinese consumer trend expert and founder of Aperture China.

“Around that time, consumers became more value driven, price sensitive, and more aware of the premium they were willing to pay,” she says.

Price wars in China tend to follow a well-established historical pattern. Chinese companies trade price cuts and offer steep discounts, burning money to gain market share. Eventually, one or two dominant players emerge and raise their prices to recover.

These days, food delivery companies like Meituan, Taobao, and JD.com are competing fiercely, leading to low prices for items like coffee. Past rivalries have included those between ride-hailing taxi apps Uber and Didi — which ended when Didi acquired Uber in 2016; and between bicycle sharing companies Ofo and Mobike, whose battle in the late 2010s eventually allowed Didi Bike and Hello to surface.

As Chinese companies fight for market share, their profits tend to shrink. Since 2020, net profit margins for Chinese companies within the Fortune Global 500 have ranked consistently below those of their economic peers.

Ultra-competitive industries like retail and consumer goods help to drag down overall profit margins for China Inc. The net profit margin for the broader Fortune China 500 was 4.8 percent last year, with individual companies often recording even narrower margins. Online retailer JD.com’s 2024 margin was just 2.2 percent while its peer Suning.com’s fell to negative 6.5 percent, to take two examples.

Chinese companies — especially those owned by the state — are able to weather low profits to some extent as they face less pressure to pay dividends to shareholders, says Alicia García-Herrero, chief economist for Asia Pacific at Natixis. Some are prepared to endure low margins temporarily as part of a “game of scale and volume,” she says, before hopefully emerging as national champions in their sectors.

In the past 20-30 years, China became the factory of the world, with manufacturers focusing on low-end products and not caring much about profit. In the past 5-10 years, they have realized this is not sustainable long-term to compete with the U.S..

Miro Li, a Chinese brand expert and founder of Double V. Consulting

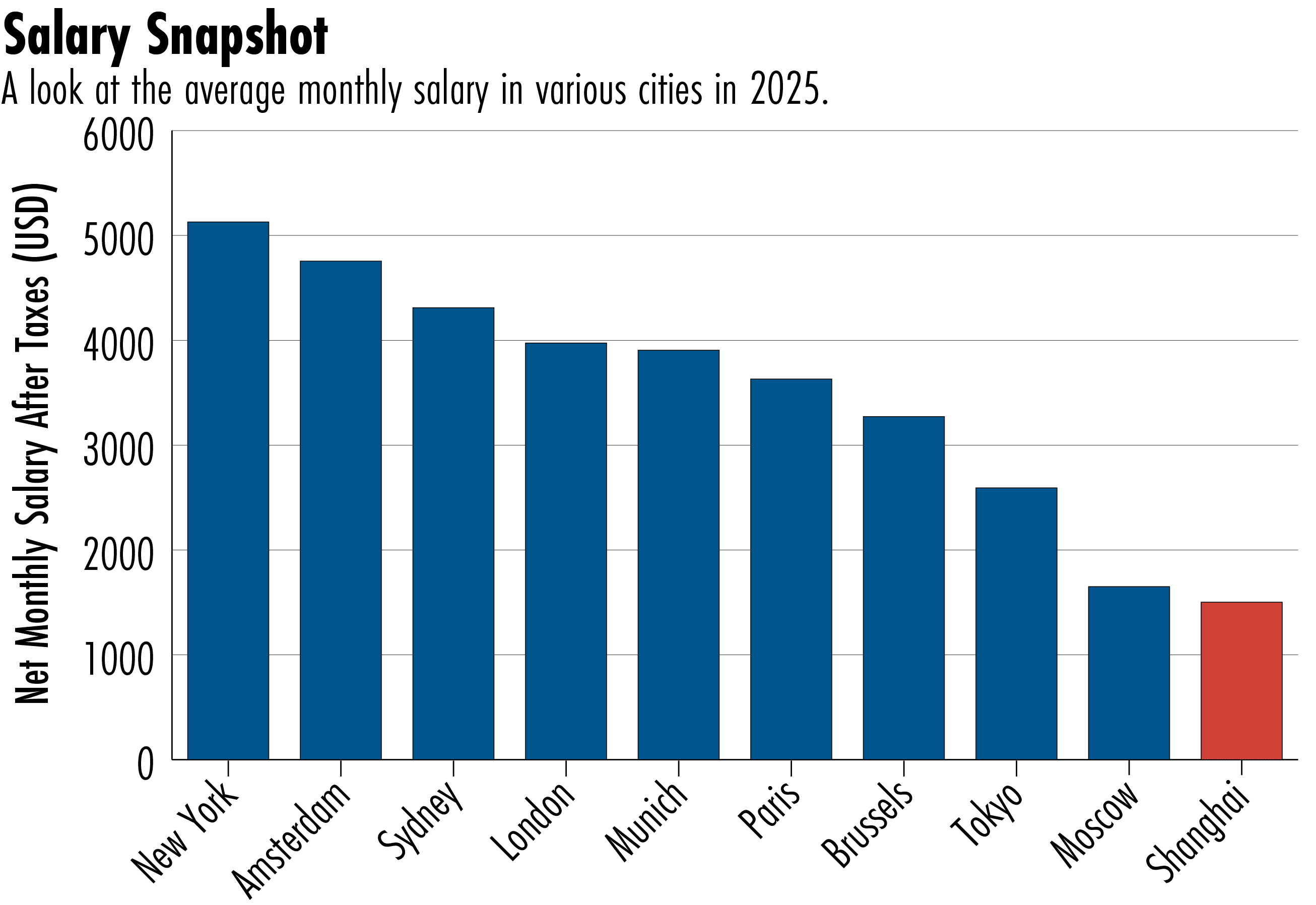

For sure, other factors contribute to weak price pressures, including weak demand, overcapacity and the lingering effects of China’s real estate slowdown. Low consumer prices also reflect the fact that salary levels remain lower in China than in many other countries.

In the short term, deflation benefits consumers, as long as it doesn’t become entrenched. But price wars can hurt brands longer term — especially when intensified by external distributors. Take the battle between coffee brands Cotti and Luckin, which has been amplified by the rivalry between JD.com and Meituan, which layer on their own discounts. The resulting low prices risk setting a new, unsustainable standard for the coffee producers to meet.

Chinese manufacturers are now more aware that ignoring profitability is not sustainable long-term, says Miro Li, a Chinese brand expert and founder of Double V. Consulting. She sees opportunities for increased profit margins through brand building and the development of cutting-edge technologies, particularly in electronics or home appliances.

“In the past 20-30 years, China became the factory of the world, with manufacturers focusing on low-end products and not caring much about profit,” she says. “In the past 5-10 years, they have realized this is not sustainable long-term to compete with the U.S..”

Dean Minello was a summer staff writer for The Wire based in New York. He is a junior at Princeton University studying Public & International Affairs with a minor in East Asian Studies, and does research at Princeton’s Center for Contemporary China. Proficient in Mandarin, Dean is interested in authoritarian politics, human rights, and U.S.-China relations.