Every March, China’s Two Sessions set the country’s political and economic agenda for the year ahead. This tightly scripted gathering of the National People’s Congress (NPC) and the Chinese People’s Political Consultative Conference (CPPCC) is where Beijing unveils its official GDP growth target, outlines fiscal and monetary priorities, and signals the leadership’s broader policy direction. While always significant, this year’s meetings take on even greater weight than usual.

2025 marks the final year of China’s 14th Five-Year Plan, making it a critical moment for policymakers to assess progress on key economic and industrial goals. The economic backdrop is particularly challenging: China’s post-pandemic recovery remains uneven, consumer confidence is fragile, local government debt is mounting, and global trade dynamics are shifting following the return of President Trump. The Two Sessions must provide answers — not just to investors and businesses at home, but to a world closely watching how China navigates its next stage of growth.

But we don’t need to wait until March 5, when Premier Li Qiang formally announces this year’s economic targets, to get a sense of where things are headed. China’s provinces have already held 31 of their own mini-Two Sessions meetings. Taken together, they paint a picture of tacit acknowledgment of challenges and uncertainties, a leadership that seems to finally grasp the need to ignite demand, and an economy undergoing a decisive push for industrial transformation.

The provincial meetings made one thing abundantly clear: China is entering a new phase of economic transformation, defined by what the leadership calls “new quality productive forces”…

We can expect those themes to take center stage again when the national Two Sessions gets underway. At the same time, capital market reforms will prioritize attracting long-term funds — not just to fuel industrial ambitions, but to restore investor confidence. While the Two Sessions won’t explicitly frame economic policies around U.S.-China tensions, nuanced shifts in policy language and fiscal priorities may hint at how Beijing is positioning itself for Trump’s second term.

Growth Target: Managing Expectations

Data: World Bank

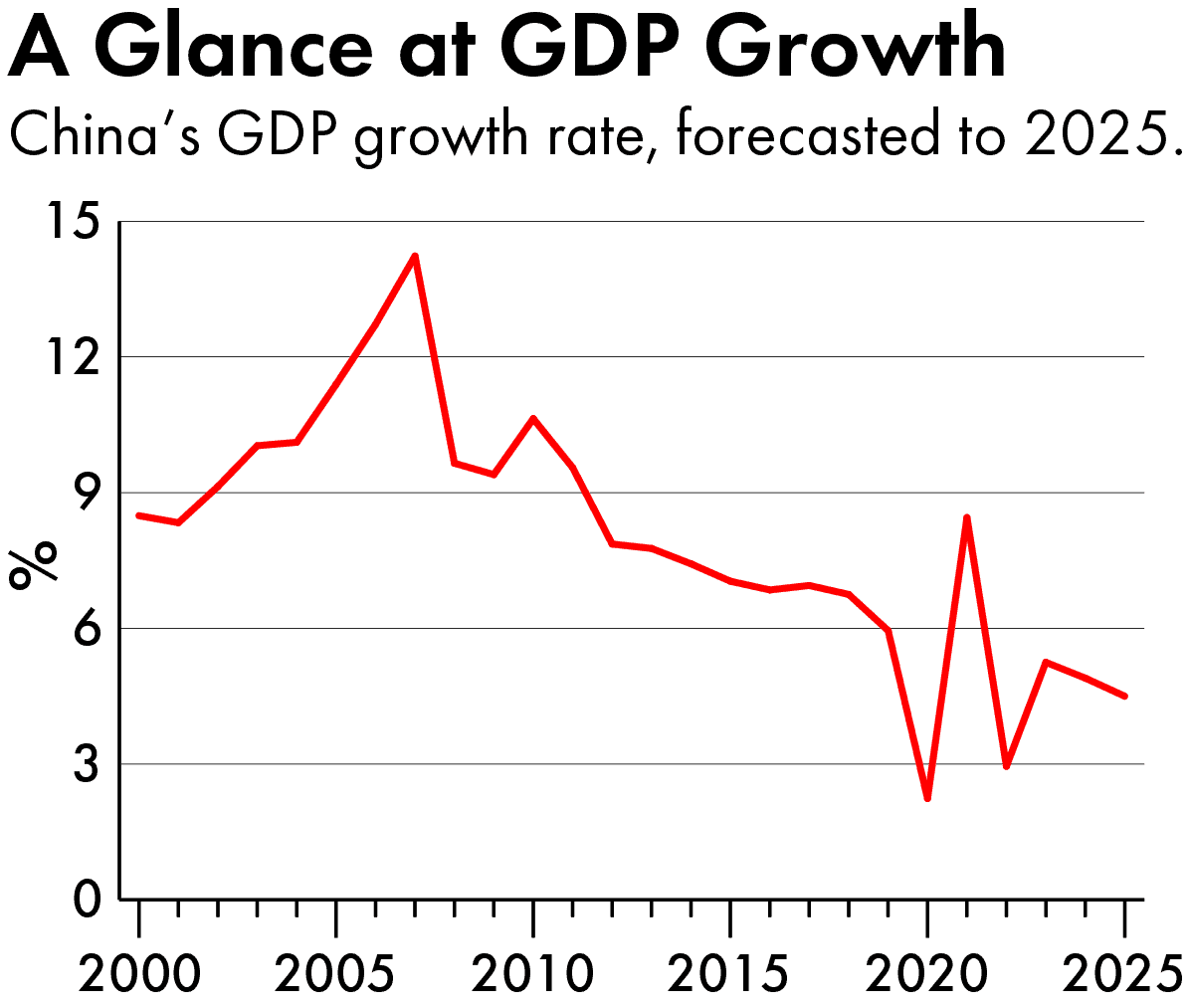

One of the clearest signals from the provincial meetings is that China’s leadership is not overpromising on growth. The average of provincial GDP growth targets sits at around 5.25 percent, slightly below last year’s 5.4 percent — a strong indication that Beijing will likely maintain its national target at “around 5 percent.” This is not a sign that China is retreating on economic ambition. Quite the opposite: China has a history of meeting its GDP targets, and the fact that the leadership is keeping the bar steady reflects a sober assessment of economic headwinds.

Consumption: The Make-or-Break Factor

If there is one area where Beijing must take decisive action, it is consumption. For too long, China has relied on investment to drive economic growth, while household spending has remained an afterthought. But that approach is running out of steam. Without a meaningful recovery in consumer confidence, economic momentum will remain sluggish.

One of the quickest levers Beijing can pull is trade-in subsidies, designed to incentivize households to upgrade cars, home appliances, and digital products like smartphones. Officials estimate that 100 billion renminbi’s worth of subsidies could generate more than double the amount in additional consumption.Past versions of these programs have had only temporary effects, often pulling demand forward rather than creating sustained momentum. The real test is whether these incentives will be paired with broader efforts to boost household incomes and consumer confidence — without which, the impact will likely be fleeting.

Provincial governments are turning to experience-driven spending as a new growth engine. In cities like Shanghai and Beijing, authorities are expanding live-stream commerce, entertainment tourism, and digital consumption, betting that younger consumers will continue prioritizing immersive, tech-driven experiences. In the cold northeastern region, provincial leaders are embracing winter sports and ice tourism. Meanwhile, coastal hubs like Guangdong and Zhejiang are investing in e-sports, digital culture, and creative industries.

At the same time, the government is waking up to the potential of China’s aging population as a key driver of domestic consumption. Nearly every province has prioritized elderly care, health services, and aging-friendly technology. Guangdong is making major investments in rehabilitation equipment, while Jiangsu is expanding healthcare and household services for seniors. The message is clear: China’s next wave of consumption won’t just come from digital-native Gen Z shoppers, but from an older generation with distinct spending needs.

But here’s the fundamental challenge: confidence. Beijing has been reluctant to introduce broad-based income support or social safety net expansions, relying instead on targeted industry incentives. Unless households feel more secure about their financial future, they will keep saving instead of spending. The Two Sessions will be a crucial test of how serious Beijing is about making consumption a true pillar of growth.

Industrial Policy: The AI-Led Transformation

One area where Beijing’s ambitions remain steadfast is industrial policy. The provincial meetings made one thing abundantly clear: China is entering a new phase of economic transformation, defined by what the leadership calls “new quality productive forces,” a phrase that has appeared with increasing frequency in official discourse over the past year.

AI stands at the center of this transformation. Over two thirds of the 31 provinces have outlined roadmaps for integrating artificial intelligence into manufacturing, finance, healthcare, and logistics, an indication that Beijing views AI as a pillar of long-term national competitiveness. Compute infrastructure is another major focus. Inner Mongolia and Guizhou, both home to expanding cloud computing clusters, are racing to build out AI supercomputing hubs. Cities like Shanghai and Shenzhen are embedding AI-driven efficiencies across supply chains, reinforcing the leadership’s broader vision of an intelligent, automated economy.

Another frontier is China’s “low-altitude economy” — a policy term that encompasses urban air mobility, drone logistics, and unmanned aviation. Provinces such as Shandong and Shanghai are laying the groundwork for dedicated drone industrial parks, an unmistakable sign that China is betting big on autonomous aerial logistics as the next major breakthrough in transportation and supply chain management.

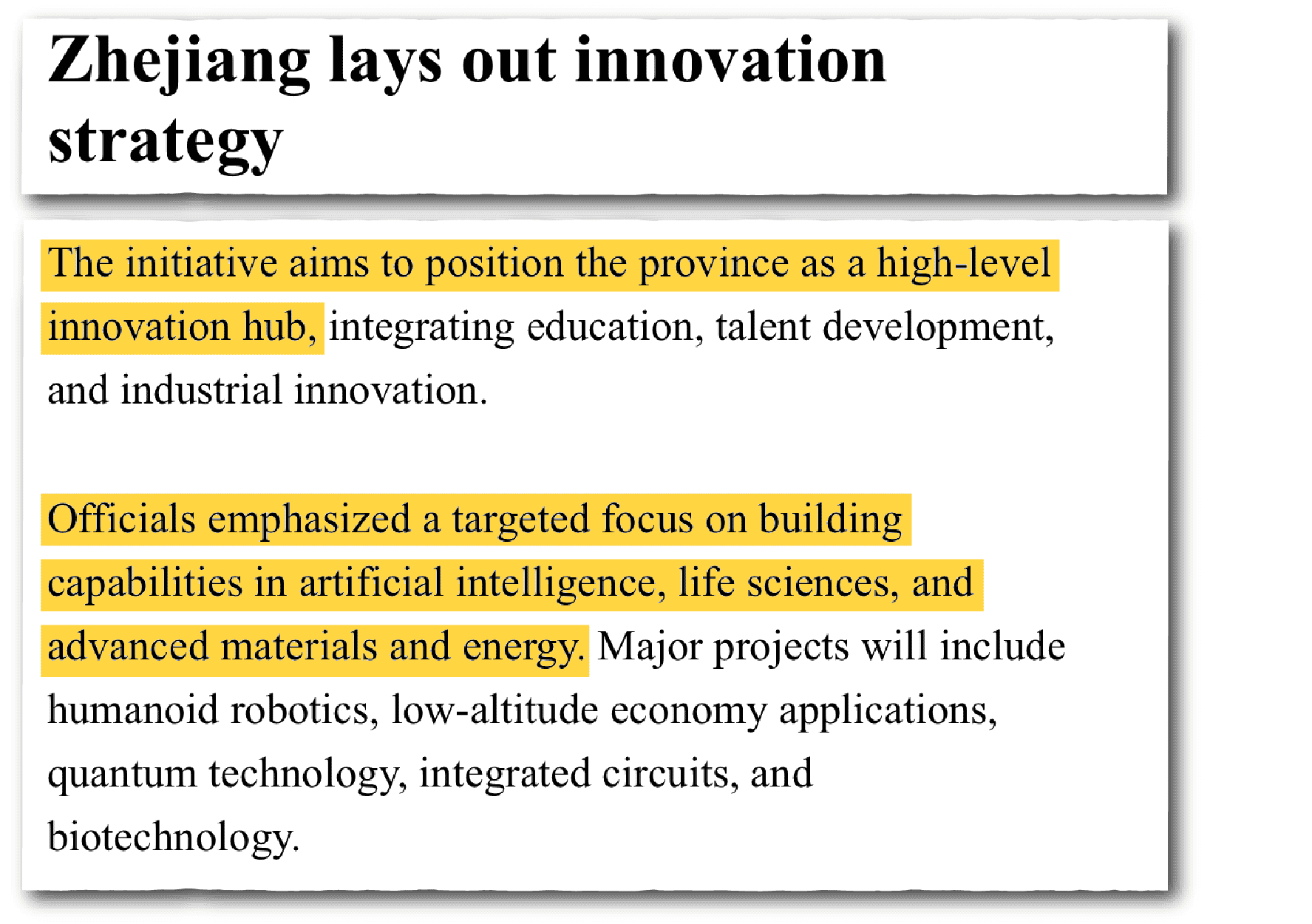

Credit: Hangzhou Government

Quantum computing and synthetic biology are also emerging as strategic priorities, with leading tech hubs like Guangdong and Zhejiang spearheading efforts to commercialize next-generation technologies. This reflects a broader shift in Beijing’s industrial strategy: rather than just catching up to the West, China is determined to set the pace in frontier industries.

Capital Markets: Summoning the Slow Bull

One major issue that has not yet been fully addressed in the provincial Two Sessions is capital market reform. If Beijing wants to pull off its ambitious economic transformation, it needs a healthy, resilient stock market — not a casino prone to boom-and-bust cycles, but a slow, steady bull that can channel capital into the real economy. China’s leadership understands that capital markets are about more than just asset prices. A strong, functioning stock market most crucially allows companies, particularly in high-tech sectors, to raise funding through equity financing rather than relying on bank loans. .

But summoning a slow bull is easier said than done. After years of erratic policy interventions, investors remain wary. Chinese regulators are now pushing a “1+N” framework for market stability, with an emphasis on attracting institutional investors, improving corporate governance, and refining merger-and-acquisition rules to enhance market discipline. The goal is clear: make China’s capital markets a reliable and attractive destination for long-term capital.

During the Two Sessions, expect the leadership to double down on capital market reforms, reinforcing the idea that China is committed to playing the long game. Whether that means opening up more channels for foreign institutional investors, further strengthening financial regulation, or finding new ways to insulate retail investors from extreme volatility, the message will be clear: China’s stock market should no longer just be a numbers game. Without deep and liquid financial markets, China’s most ambitious industrial policies — from AI to biotech — will struggle to secure the funding they need to scale.

Will We See a Response to Trump 2.0?

While the Two Sessions won’t explicitly frame policies around U.S.-China tensions, the fine print in official language and shifts in fiscal priorities may hint at how Beijing is positioning itself for the renewed unpredictability of Trump’s second term.

The real test will be whether Beijing’s response is merely a tactical hedge against near-term volatility or a more fundamental recalibration of its economic strategy — one that prioritizes long-term insulation from U.S. policy swings over short-term accommodations.

One key moment to watch will be foreign minister Wang Yi’s press conference, where China’s top diplomat may offer clues about Beijing’s geopolitical and economic posture. China is unlikely to announce direct retaliatory measures, but the policy priorities emerging from the provincial meetings suggest a quiet but forceful pivot toward economic security. Expect a sharper focus on supply chain resilience, industrial self-sufficiency, and fiscal support for sectors most exposed to U.S. trade pressure — moves designed to cushion China against external shocks without escalating tensions outright.

At the same time, the risks aren’t all one-sided. Trump’s transactional, deal-making mindset leaves room for maneuvering. While his administration has signaled a hardening stance on high-tech export controls, it has been less aggressive on broad-based tariffs — a notable contrast from his first term. This opens a potential window for negotiations, selective economic cooperation, and even deal-making on trade issues where mutual interests align.

The real test will be whether Beijing’s response is merely a tactical hedge against near-term volatility or a more fundamental recalibration of its economic strategy — one that prioritizes long-term insulation from U.S. policy swings over short-term accommodations. This year’s Two Sessions may not provide all the answers, but they will offer the clearest signals yet of how China plans to navigate the next phase of its complex relationship with Washington.

Lizzi C. Lee is a Fellow on Chinese Economy at the Asia Society Policy Institute’s (ASPI) Center for China Analysis (CCA). She is an economist turned journalist, and graduated from MIT’s Ph.D. program in Economics before joining the New York-based independent Chinese media outlet Wall St TV.