As China wrestles with sluggish domestic demand and slowing economic momentum, a perplexing question arises: Why has Beijing refrained from deploying direct stimulus to help its consumers? Putting cash directly into the hands of citizens — as the U.S. government did during the pandemic — appears an obvious remedy to invigorate spending and rejuvenate the economy. Yet, Chinese policymakers have consistently eschewed this route.

Some attribute this reluctance to ideology, pointing to Xi Jinping’s reputed aversion to “welfare” policies that could erode the values of diligence and self-reliance that the leadership seeks to instill. Another theory is that the government is hesitant to empower consumers whose spending choices may not align with national development objectives.

Others suggest that institutional inertia or the absence of effective mechanisms within China’s complex bureaucratic framework may be hindering the implementation of broad-based cash transfers.

These theories capture facets of the issue, but the reality is more nuanced, reflecting a delicate balance of pragmatic concerns, long-term developmental goals, and the accumulated wisdom from both domestic and global experiences with economic stimulus.

Indeed, considering why Beijing is keeping its wallet closed tells us much about how it seeks to run the world’s second largest economy. It also helps to understand why the Chinese authorities may yet be forced to put aside their reluctance to flash their cash.

STABILITY OVER STIMULUS

The Chinese government has long preferred the fine-tuning of monetary policy via the country’s central bank rather than broad fiscal interventions. And it believes that the Chinese economy’s unique dynamics require a tailored response that prioritizes stability over the transitory effects of direct cash infusions.

Rather than viewing such one-off stimulus efforts as a panacea, Beijing’s aim is to address the structural challenges that temper consumer confidence. This involves enhancing social safety nets, unlocking the latent consumption potential of migrant workers, and resolving persistent inefficiencies within the property market.

Rather than attributing imbalances to governmental inertia or the leadership’s prioritization of high-tech manufacturing sectors, many Chinese experts identify structural flaws within the fiscal framework as the root of the problem.

While several commentators have compared China’s current circumstances with Japan’s deflationary spiral in the 1990s, Chinese academics and policy makers regard this as overly reductive. Japan’s malaise, shaped by a shrinking labor force and an absence of growth catalysts, was complicated by a balance-sheet recession following the collapse of the 1980s real estate bubble, meaning that for years deleveraging took precedence over spending or investment.

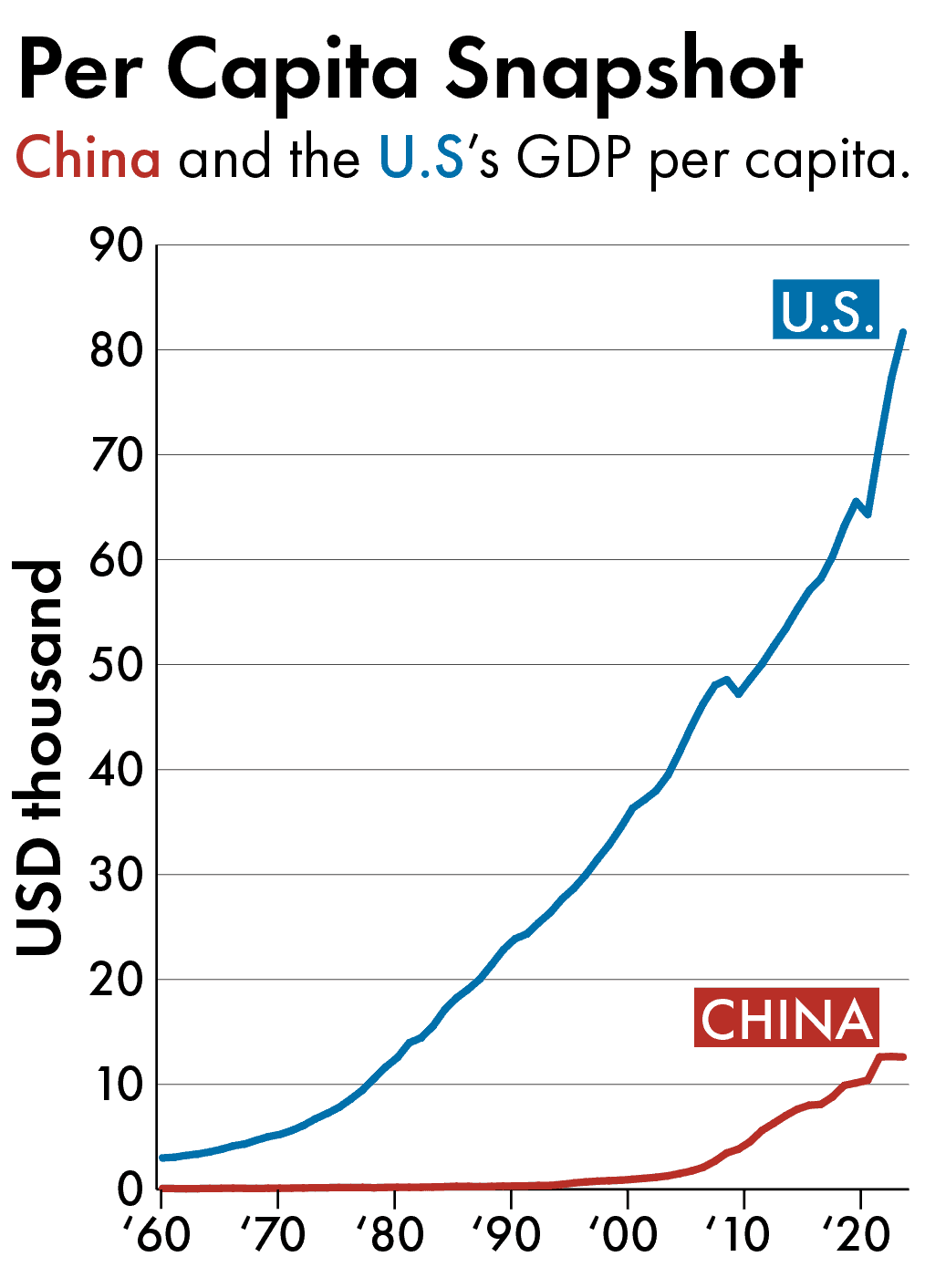

China’s economic landscape is also beset by challenges such as a real estate slowdown and rising youth unemployment. But policy makers still see it as retaining significant growth potential, reflected in the still-wide disparity in per capita GDP between China and the United States. Additionally, they view China’s ongoing industrial upgrades as presenting growth opportunities that were absent in Japan during its period of stagnation. That still broadly positive outlook has made policy makers reluctant to press the panic button.

For sure, a complicating factor for Beijing in recent years has been the significant gap between low interest rates in China and higher ones in the United States. This differential has limited the People’s Bank of China (PBOC)’s capacity to reduce Chinese rates, without triggering capital outflows and further depreciation of the yuan.

However, with the Federal Reserve signaling a shift toward rate cuts, this gap is narrowing. In August 2024, the yuan posted its largest monthly gain since November, rising 1.9 percent against the dollar. The PBOC responded with a 100 billion yuan net bond purchase, exploiting the favorable conditions to stabilize the yuan. Analysts suggest this may offer Beijing greater flexibility to ease monetary policy without sparking capital outflows, thereby reducing the urgency for broader fiscal stimulus.

Beijing’s leadership also views direct cash handouts as likely to be less effective in China. The U.S. economy, driven predominantly by consumption, saw stimulus checks quickly translate into increased demand, supported by a cultural inclination toward spending and a well-established social safety net.

Chinese consumers, faced with economic uncertainty and a less comprehensive welfare system, are more inclined to save rather than spend. So cash handouts in China may not yield the same economic stimulus as they did in the U.S..

Moreover, broad-based stimulus measures are an inefficient way to target sectors or populations most in need of support, particularly given the complexities of reaching migrant workers and rural residents who are less connected to traditional banking systems.

Importantly, Beijing’s policymakers identify the current economic slowdown as primarily driven by internal, structural factors rather than external shocks. The significant downturn in the property sector, for instance, has had far-reaching consequences for local government finances and consumer confidence. Injecting additional liquidity into the economy is viewed as insufficient to address these fundamental issues.

Instead, the government has concentrated its resources on alleviating the vast overhang of excess stock in the real estate market. Beijing has also opted to reinforce social safety nets for vulnerable populations, for example, by increasing basic pension payments for rural and urban residents — particularly the nearly 165 million low-income elderly.

Concurrently, Beijing is implementing policies designed to incentivize childbirth through financial subsidies, tax breaks, and expanded access to affordable childcare and education — alleviating the financial burdens on young families and stimulating spending on goods and services related to child-rearing.

In addressing these structural factors, Beijing is seeking to create a more sustainable foundation for domestic demand growth. By “treating the underlying causes, rather than just the symptoms,” as one policy advisor remarked, the government aims to unlock significant consumer potential and foster long-term economic stability.

CRACKS IN THE SYSTEM

Despite Beijing’s aversion to direct cash transfers, there is a growing recognition among those close to the leadership that greater consumption is vital for ensuring long-term economic vitality. However, their diagnosis of the underlying causes diverges markedly from prevailing Western narratives.

Rather than attributing imbalances to governmental inertia or the leadership’s prioritization of high-tech manufacturing sectors, many Chinese experts identify structural flaws within the fiscal framework as the root of the problem.

Central to this issue is the misalignment of incentives between the central and local governments, which traces its origins to the 1994 Tax-Sharing Reform that consolidated fiscal resources at the central level, leaving local governments heavily reliant on land sales and production-based taxes to sustain their budgets. Consequently, local authorities tend to prioritize attracting manufacturers and stimulating production, even when the central government emphasizes the urgency of bolstering domestic demand.

This tension is illustrated by the handling of consumption taxes, which are predominantly levied on producers rather than consumers, with the entirety of the revenue accruing to the central government. As a result, local governments have scant fiscal motivation to nurture consumption or develop consumer-centric sectors such as tourism.

Meanwhile, with revenues from land sales plummeting, many local authorities have resorted to aggressive tax enforcement and punitive measures to shore up their financial positions. However, these actions risk further undermining business confidence and stifling economic activity, creating a vicious cycle of declining demand and shrinking tax bases.

Escalating tensions with major trading partners have put China’s traditional growth engines increasingly under strain. In this scenario, broad-based cash transfers could emerge as a viable tool to counteract the adverse effects of trade restrictions…

In response to these systemic challenges, Chinese leaders are now fixated on “comprehensive fiscal reform”, including potential measures to redirect consumption tax revenues to local governments, broaden the tax base to include a wider array of consumer categories, and potentially shift the point of tax collection from producers to retailers. Such reforms are aimed at realigning local government incentives, encouraging them to actively promote consumption through direct subsidies or investments in public services such as healthcare and education.

WHAT COULD TIP THE SCALES?

While Beijing has thus far resisted broad-based consumer stimulus, the evolving economic landscape could yet prompt a reassessment.

The PBOC’s concern over persistently low long-term Chinese government bond yields — evidenced by recent interventions to cool a market rally — reflects deeper anxieties about the country’s economic stability. These declining yields are more than a technical market anomaly; they serve as a harbinger of broader economic malaise, signaling waning investor confidence amid weak domestic demand and intensifying deflationary pressures.

As investors increasingly seek refuge in bonds, their prices rise and yields continue to fall, exacerbating the very conditions that drove the flight to safety. This dynamic creates a self-perpetuating cycle where low yields are interpreted as a lack of confidence in other asset classes, such as equities or real estate, further deepening the economic slowdown.

Moreover, the fall in long-term yields erodes the profit margins of financial institutions, particularly China’s large state-owned banks, by narrowing the spread between the cost of funding and lending rates. This squeeze on profitability can lead to tighter credit conditions, further stifling economic growth.

Recent data reveals a fragile recovery. The official manufacturing PMI slipped to a six-month low of 49.1, while the Caixin PMI, covering smaller exporters, crept into expansion at 50.4. Services held steady, with the non-manufacturing PMI at 50.3, though the construction subindex hit its lowest since 2020. Analysts caution that while fiscal support is expected to rise, any recovery may be short-lived as the property downturn deepens and export risks grow.

Should these conditions persist the Chinese authorities may find that more direct and aggressive fiscal measures, such as broad-based cash transfers, become increasingly necessary. Such interventions could play a crucial role in breaking the cycle of low confidence and weak demand.

Yi Gang, the former governor of the People’s Bank of China, recently echoed these concerns in a rare public statement, emphasizing that while targeted monetary policy remains the central focus, “more direct fiscal support may be needed to counter structural deflationary risks.” His comments have sparked renewed speculation that Beijing may be forced to reconsider its stance on cash transfers if current measures fail to lift domestic demand.

The global geopolitical environment is another significant variable that could compel Beijing to reconsider its stance. Escalating tensions with major trading partners have put China’s traditional growth engines — exports and investment — increasingly under strain. In this scenario, broad-based cash transfers could emerge as a viable tool to counteract the adverse effects of trade restrictions and geopolitical frictions on China’s economy.

The real estate sector represents another potential trigger for policy change. Despite recent efforts to stabilize the property market, the sector remains precarious. A continued downturn would exacerbate economic stagnation, particularly as property-related investments and consumer spending constitute a significant portion of China’s GDP. In such a context, Beijing might find it increasingly necessary to implement broad-based cash transfers as a means of shoring up consumer confidence and supporting domestic demand.

The broader challenge of meeting GDP growth targets could also drive a shift in policy. China’s GDP growth has already fallen short of expectations. As the government grapples with these challenges, the pressure to achieve its growth objectives becomes more pronounced. If the current policy mix proves insufficient, Beijing may be compelled to consider more aggressive stimulus measures.

In such circumstances, broad-based cash transfers could be seen as a necessary step to inject liquidity directly into the economy and stimulate consumption. The long-closed wallet may, after all, be finally prised open.

Lizzi C. Lee is a Fellow on Chinese Economy at the Asia Society Policy Institute’s (ASPI) Center for China Analysis (CCA). She is an economist turned journalist, and graduated from MIT’s Ph.D. program in Economics before joining the New York-based independent Chinese media outlet Wall St TV.