The Biden administration’s sweeping round of higher tariffs on Chinese imports this week are the latest sign of Western governments’ alarm at China’s growing capacity to dominate vital industries, from electric vehicles to solar panels.

The message back from Beijing is already clear, however: Expect more.

In a series of recent speeches published in March, Chinese leader Xi Jinping has expressed his desire to harness the country’s financial sector in support of his economic agenda. In practice, that means steering capital towards favored sectors to expand their capacity even further.

“The rise of a great power cannot be separated from the support of a strong financial system,” Xi said in one speech in January, in which he emphasized the need for a system that is “people-oriented,” allowing “the broad masses of people [to] share the fruits of financial development.”

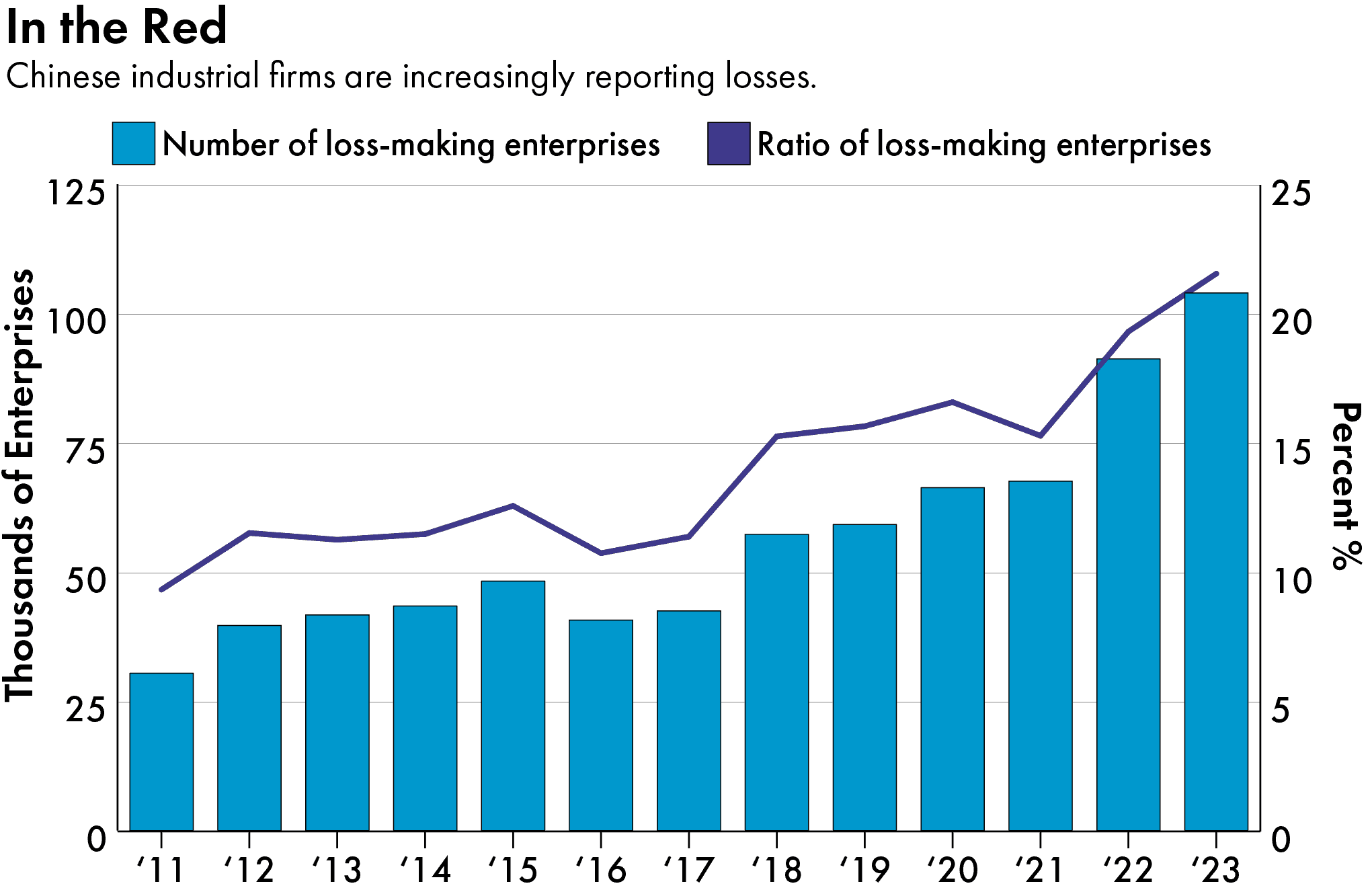

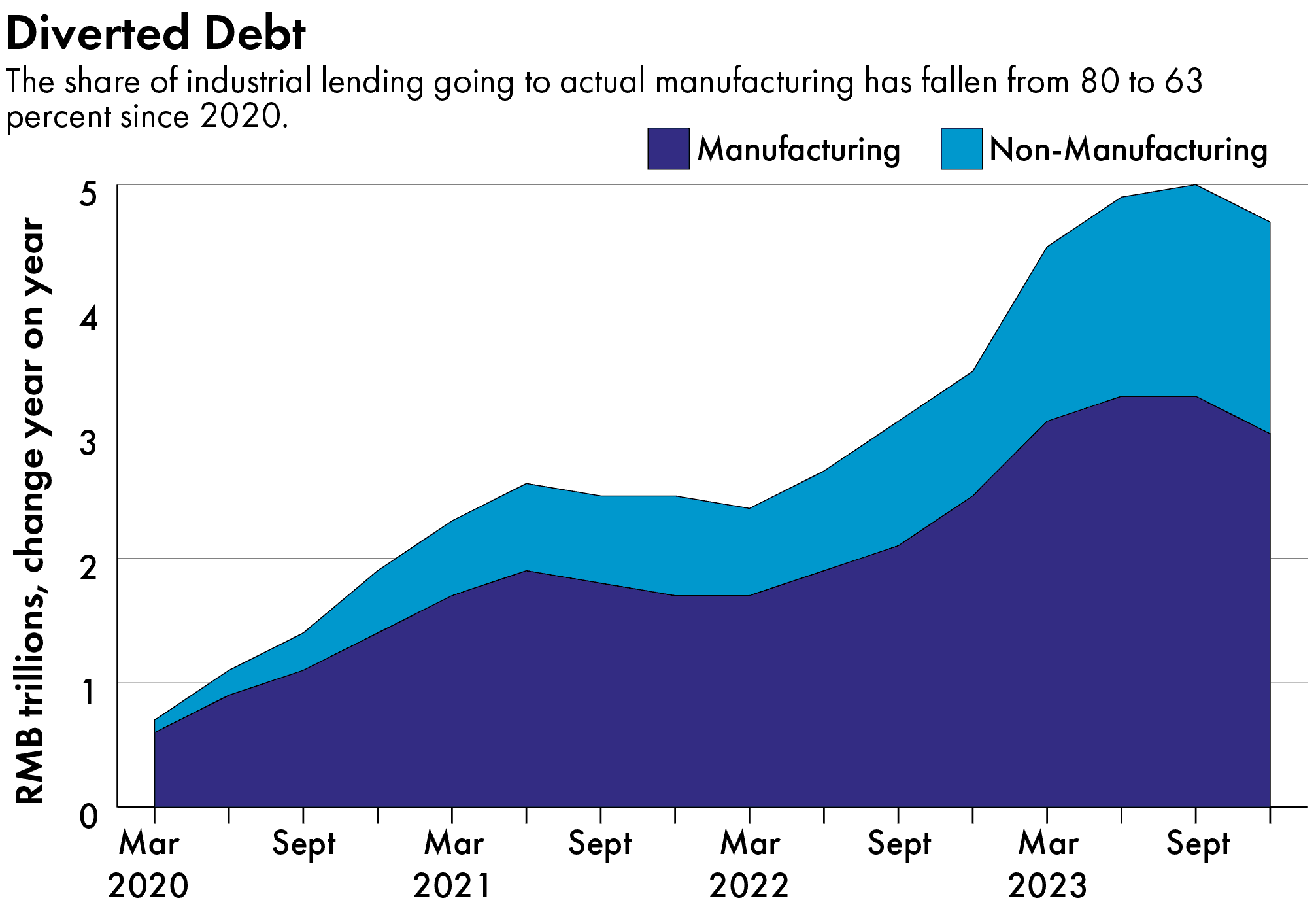

The question is, are Chinese banks listening? Data from China’s central bank show a fivefold surge in state lending to the industrial sector between 2020 and 2023. But recent research from consultancy Rhodium Group suggests that the share of those loans going to actual manufacturing fell from 80 percent to 63 percent over the same period. Instead, much of the lending went to other causes including debt relief for Covid-battered businesses, refinancing for China’s ailing local government financing vehicles — companies which borrow on behalf of municipalities to fund infrastructure projects — and financial speculation.

While the banks are not the only way that Beijing channels money towards its policy priorities, their laggardness shows how the baggage of the country’s long-simmering economic problems is limiting the financial sector’s ability to support Xi’s economic ambitions.

“China’s banking sector has always been a key instrument of industrial policy, but it’s become very inefficient in the last few years,” says Camille Boullenois, an associate director at Rhodium. “Some of this credit is fuelling an increase in capacity, but a lot of it is wasted.”

China’s major state-owned banks — which include Industrial & Commercial Bank of China, the world’s largest bank by assets — have historically favored lending to their state-owned enterprise peers, both because of their government backing and their ability to provide strong collateral. By comparison, banks have been reluctant to lend to smaller firms that often drive innovation and new technologies — because they perceive them as riskier, and often only are able to offer loan collateral that is harder to value, like patents.

Last October, Xi signaled his focus on reorienting the banking sector by visiting the central bank for the first time since assuming the top leadership in 2013. Recent reforms have tightened the Communist Party control over banks, so that they provide more funding for the “new productive forces” that Xi has referred to in speeches this year — a mantra that appears to mean more investment in everything from tourism to electric vehicles, batteries and renewable energy. The government created a new financial regulator in November, the Central Financial Commission, which reports directly to the Party.

A lot of the new loans are not actually new, but are actually old loans that are [being] refinanced. That prevents the whole building from collapsing…

Camille Boullenois, an associate director at Rhodium

But old habits die hard. In fact, according to Rhodium, recent bank lending has often been aimed at propping up troubled businesses. It estimates that more than one third of so-called ‘industrial’ loans at the end of last year have ended up going to non-manufacturing activity, including relief measures introduced during the pandemic that allowed small businesses to delay repaying their debts, and for LGFVs to refinance their loans.

“A lot of the new loans are not actually new, but are actually old loans that are [being] refinanced,” Rhodium’s Boullenois says. “That prevents the whole building from collapsing, especially since Covid when there was a big need to refinance loans and provide forbearance to companies that needed it,” she explains.

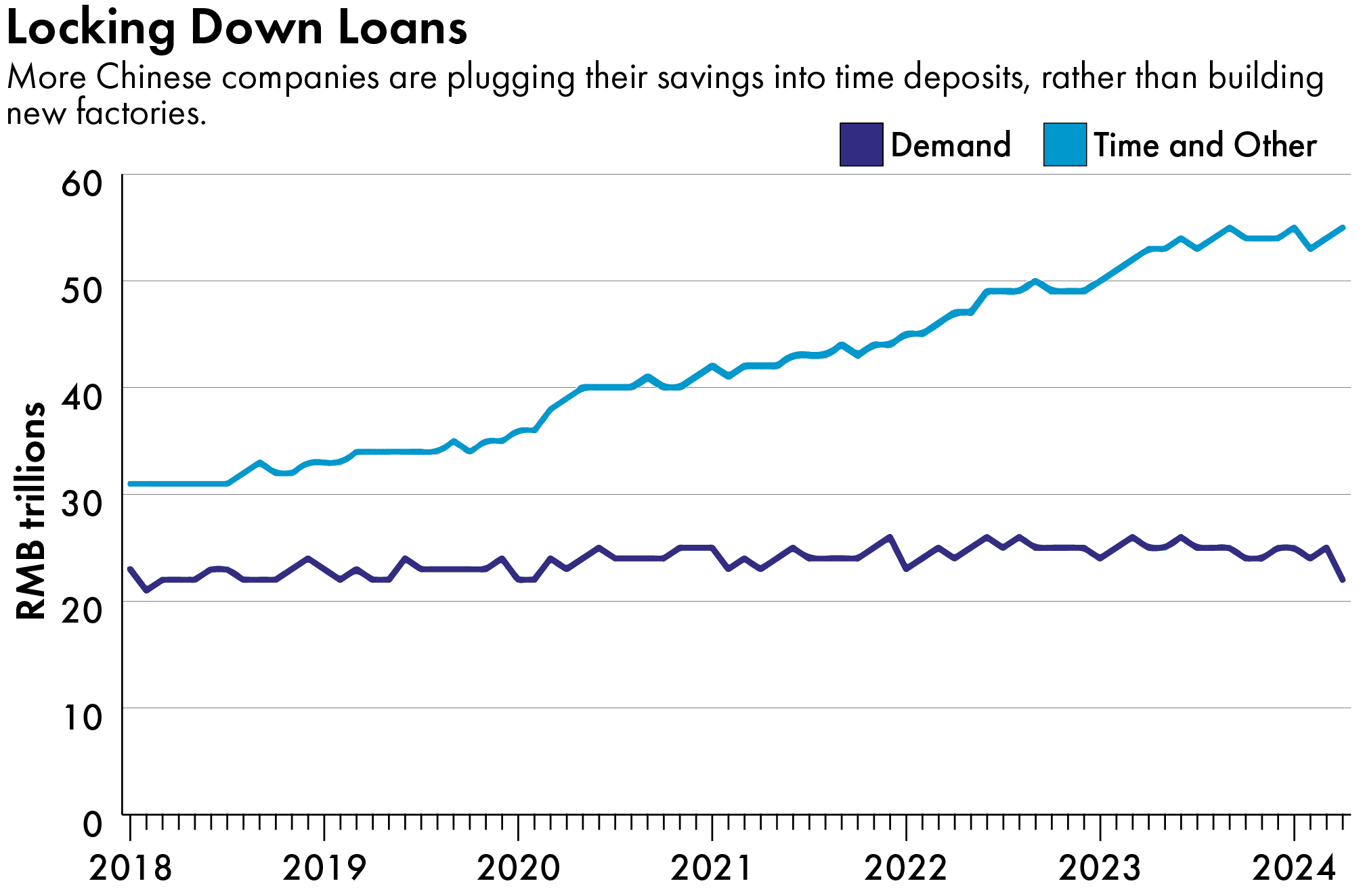

Rhodium’s analysis suggests that when companies are able to secure new loans, many are plugging the money into investment products rather than building new factories. As an illustration, the share of corporate deposits going to long-term corporate time deposits, an interest-bearing type of bank account, has risen by 20 percentage points since 2020.

For now, any shortfall in new bank lending isn’t preventing manufacturers from expanding. Some are dipping into their own resources, such as their past accumulated profits, to finance new projects.

“Companies have other ways of securing financing,” says Tianlei Huang, a research fellow at the Peterson Institute for International Economics, a Washington think tank. “70 to 80 percent of Chinese companies’ fixed asset investments come from retained earnings.”

Huang argues that the success of Xi’s economic agenda won’t hinge on him resolving the financial sector’s problems.

“The Chinese state has a wide variety of tools to pursue its developmental goals that don’t require asking the financial sector to pivot its resources,” he says. “The government, including local governments, are also active investors through thousands of guidance funds; they’re very active in making investments in private companies in policy priority areas.”

The ability for Chinese companies to either keep funding themselves or obtain other government funds suggests that other sources of financing are driving China’s overcapacity problems. By comparison, the financial sector is playing second fiddle, by propping up uncompetitive or failing companies through loan extensions and refinancing.

But that could change if Xi has his way. The government’s annual work report, for instance, has pledged to “prevent funds from sitting idle or simply circulating within the financial sector.” Should it succeed in unclogging the banking spigot, the flood of Chinese factory goods will only rise higher.

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen