For anyone hoping that the National People’s Congress (NPC) in Beijing last week might have filled the economic policy void left by the silence of policymakers over the long winter months —and the still unannounced Third Plenum — there was only disappointment. There were no surprises in the main speeches and policy documents, no new or comprehensive proposals to address China’s systemic economic problems, and no convincing case that the government’s ‘around 5 per cent’ GDP target for this year might be met.

An segment from a CGTN video of Li Qiang meeting the press last year, after the closing of the first session of the 14th National People’s Congress, March 13, 2023. Credit: CGTN

Premier Li Qiang’s first Government Work Report, though, still merits attention and scrutiny for reasons of both transparency and content.

Before the NPC opened, it was announced that the Premier’s post-parliamentary press conference, a 30-year tradition offering the opportunity for China’s Premier to engage with the media openly, and away from the often clunky language deployed in formal speeches and reports, would be scrapped. Whether this was Xi Jinping’s way of signaling what he thought about Li’s status, or about the state of the economy, the optics were poor.

A clue to content can be deciphered by analyzing the frequency of certain key words in Li’s Work Report. According to analysts at Yuekai Securities, the biggest increases in the number of mentions were for terms such as ‘high quality development’, ‘science and technology’, ‘innovation’, ‘risks’ and ‘security’. The biggest decreases were for ‘economy’, ‘enterprise’, ‘reform’, and ‘markets’. This less than scientific interpretation is quite revealing.

For some time, Xi Jinping’s policy rhetoric has presented economic growth or development as being in a trade-off with security and stability, a point underlined by Li at the NPC. It is debatable if these goals are alternatives or complementary, but Xi has certainly shifted his emphasis between the two, mostly coming down on the side of security and control, but sometimes, as now, finding space to emphasize the former.

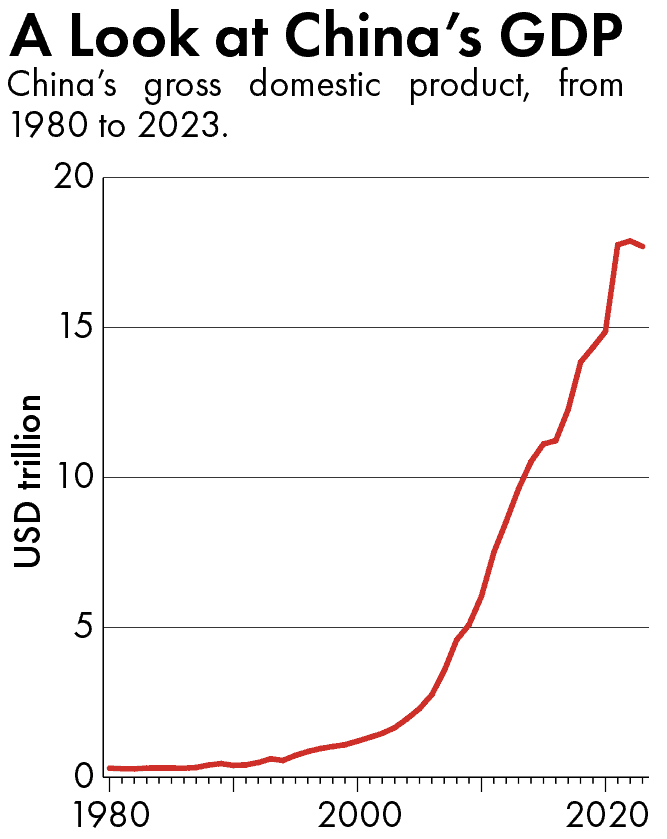

The decision to set a 5 per cent real GDP growth target (that is, inflation adjusted) should be seen in this light. It is an optimistic, even über-ambitious objective when the economy’s trend, or potential growth rate may be little more than 3 per cent. It is going to be much harder to hit such a target without last year’s easy comparison with the Covid slowdown in 2022. Even last year’s official 5.2 per cent GDP growth rate seems unrealistic, with some economists suggesting this was at least twice as high as what was actually achieved.

The government is certainly hopeful that 5 per cent real GDP growth can be realized. From the Ministry of Finance Budget Report, we can deduce that the government expects nominal GDP — before adjusting for inflation — to rise by an unrealistic 7.3 per cent this year. This follows a mere 4.6 per cent rise in 2023, when the price level for GDP dropped for the first time in 30 years, pointing to deflationary risk in China. If demand in China remains soft, which is likely in the absence of stronger measures to bolster household incomes and consumption, prices will remain weak, and real GDP will struggle to grow more than in 2023.

This means that the government’s target can only be met under two scenarios. Either it does a most unlikely volte-face on economic policy and embraces income redistribution and tax reform; or it will have to deploy much more fiscal stimulus later in the year than it currently deems desirable.

As things stand, the government, whose reports to the NPC were peppered with references to fiscal discipline and the need for local governments to pay close attention to resolving financial risks, seems to be anticipating a widening of the fiscal deficit, but perhaps by no more than about 1 per cent of GDP. If the GDP growth target starts to look out of reach, greater policy support will be more likely, along with some ‘miss and massage’: In other words, failing to hit the target would result in the data being manicured to minimize the miss.

The 5 per cent growth target is clearly part of the toolkit being used to present and talk up a brighter economic outlook. To this end the government is also emphasizing some other things, though none are likely to shake things up for the economy.

…the simple truth is that the government still seems to be underestimating both the scale of the headwinds in the economy…and the systemic nature of these problems.

In policy terms, the authorities will continue to ease monetary conditions, to ensure adequate liquidity and lending so as to enable property developers to muddle through and bring their estimated 20 million of pre-sold but uncompleted housing units to their owners. The hope is that this will stabilize real estate prices and construction. The government is adamant that high levels of job creation are important but seems to have a blind spot for the deterioration in the pay and skill composition of most new jobs nowadays. It has offered proposals to lift demand, at the margin, by encouraging consumers to trade in old for new durables, upgrading elderly and child care services, raising pensions a bit, and rolling out a so-called ‘worry-free’ consumption initiative, whatever that is.

Politically and strategically, the government is trying to lift spirits. Not for the first time since zero-Covid was abandoned, it has softened its rhetoric and approach with regard to private firms and entrepreneurs at home, and towards foreign firms. It may, though, prove hard to restore trust, bearing in mind the panoply of laws and regulations that weigh heavily on the private sector and foreign businesses, and given Xi’s insistence that ‘the party leads everything’.

A clip from a speech delivered by Li Qiang at the opening ceremony of the first China International Supply Chain Expo (CISCE) in Beijing, November 28, 2023. Credit: CCTV

On the other hand the government clearly intends to make cutting-edge science and technology, or what Xi calls ‘new productive forces’, the core of ‘high quality development’ as the party tries to shift the structure of the economy away from property and infrastructure. ‘New productive forces’ are deemed to be the incubator of innovation, productivity, supply chain resilience and self-reliance. Li Qiang was effusive in his enthusiasm for the term, as we would expect.

Major questions persist, however, about whether China’s science and technology capacities match its aspirations, and about whether its islands of technological excellence are even the right or relevant answer to the systemic economic problems, including weak demand and imbalances, which run through the arteries of much larger swathes of the economy. New productive forces will never match these factors in terms of scale.

In a short but candid moment, Li said that ‘growth is not solid, as evidenced by a lack of effective demand, overcapacity in some industries, low public expectations, and many lingering risks and hidden dangers’.

It would have been helpful, and markets would have found it instructive, if he had elaborated on these phenomena and spelled out the risks and dangers. For the simple truth is that the government still seems to be underestimating both the scale of the headwinds in the economy coming from real estate shrinkage, local government financing strains, financial instability risks, and weak demand and productivity growth — and the systemic nature of these problems. They require transformational and institutional change, not tinkering at the margins.

To recognise this, however, would immerse the government in complex policy questions that are politically extremely inconvenient, even out of order. That would not have made for an uplifting state-of-the-nation address, and would certainly have been inconsistent with a 5 per cent GDP growth target.

George Magnus is a research associate at Oxford University’s China Center and at SOAS, and the author of Red Flags: Why Xi’s China is in Jeopardy. He is the former Chief Economist of UBS.