“We’re living in the midst of India’s automotive renaissance,” Shah Rukh Khan, Bollywood’s most-coveted megastar, announced at the 2023 Auto Expo outside of New Delhi.

|

|

| Illustration by Nate Kitch | |

| More in this series: | |

| The Japan Model |  |

| Rare Earth Reshore |  |

| Out of Bounds |  |

In sunglasses and a dark suit, Khan was on hand for the India-launch of Hyundai’s all-new Ioniq 5 electric. As a brand ambassador for the South Korean carmaker for over 25 years, Khan has had a front row seat to Hyundai’s growth in India, especially recently: In September, Hyundai reported its highest-ever monthly results in the country, and so far this year, Hyundai generated close to 19 percent of its total global vehicle sales in India.

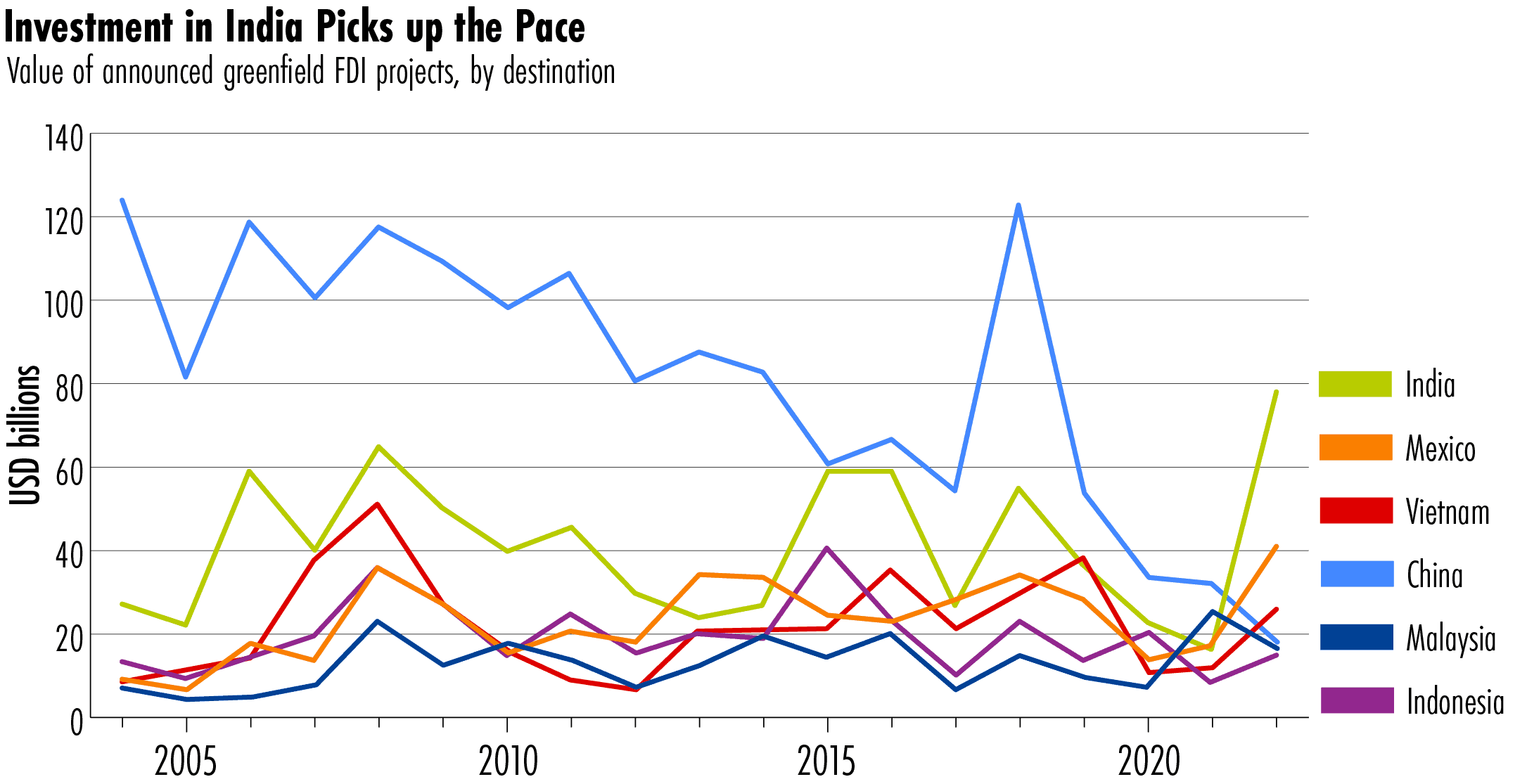

Indeed, Khan was on to something: India is quickly becoming a country that global automakers can’t ignore. With over 4.7 million vehicle sales last year, the Indian market surpassed Japan to become the world’s third largest.

Sales in India still pale compared to the over 13 million vehicles purchased in the U.S. and the nearly 27 million in China – by far the world’s largest market. But unlike those markets, India’s experienced strong growth last year of over 26 percent, according to the Society of Indian Automobile Manufacturers. China, by contrast, saw a 2 percent uptick while the U.S. and Europe saw declines.

India’s automobile scene is also shedding its reputation as a market for mostly small, low-priced vehicles; last year, SUVs accounted for over 40 percent of sales. Consequently, the average price of a car has more than doubled over the past decade to $14,000, boosting revenues and profit margins.

The rising spending power of Indian consumers has driven up car sales. A recent survey by the Indian research center PRICE found that the number of middle class Indians may already number 400 million today and rise to over 1 billion by 2047.

“India is the only remaining place in the world that has the potential to bring a middle class online that can consume technologies at scale,” says Stephen Ezell, Vice President for global innovation policy at the Information Technology and Innovation Foundation (ITIF).

India may even surpass Japan to become the world’s third largest economy, with a projected size of over $7 trillion by 2030. Last year, the Indian economy grew nearly twice as fast as the average emerging market economy, and the World Bank projected it will continue to expand at above 6 percent for the next three years.

This potential for growth is appealing on its own for multinationals like Hyundai, but adding to India’s allure is the fact that many boardrooms are looking to the country as a way of diversifying their supply chains away from China.

The “China plus one” strategy, as it’s known, was pioneered by Japanese companies and highlights the importance of establishing manufacturing hubs outside of China. Although destinations like Mexico and Vietnam have less regulation, better infrastructure, and higher-skilled labor than India, India has the benefit of its large and growing market.

“At the end of the day, [multinationals] no longer go somewhere just to re-export. They want a market too,” says Alicia García Herrero, chief economist for Asia Pacific at the investment bank Natixis.

Hyundai realized India’s potential long before most multinationals. The company’s chief manufacturing officer, Gopala Krishnan, told The Wire that Hyundai’s manufacturing facilities in India account for nearly 18 percent of the company’s total global production. India’s domestic market, he says, is “crucial,” but the country also “acts as an export hub to the global markets.”

A long line of American multinationals seem ready to follow suit. Google recently announced it will manufacture its flagship Pixel smartphones in India beginning next year while Apple appears to be all-in on the country. Cisco Systems says it will establish a manufacturing facility in India to diversify its global supply chain. And after succumbing to its competition in China, Amazon intends to increase its India investments to the tune of $26 billion by 2030.

Altogether, the U.S. Bureau of Economic Analysis tallied American investment in India at over $6.7 billion last year — one of the highest levels ever recorded by U.S. companies.

“I think India has more promise than any other large country in the world,” Tesla’s founder Elon Musk said after meeting Indian Prime Minister Narendra Modi this June in New York. The global EV frontrunner is in discussions with Indian officials to invest in a plant for a new low-cost vehicle.

“There is a massive change of perception of India,” says García Herrero. “India went from being untouchable to a place where everyone wants to go.”

Washington, of course, is pleased with this development.

India has been the economy of tomorrow for the past 30 years. If it can ever just get its policy environment right, India could become the economy of today.

Stephen Ezell, Vice President for global innovation policy at the Information Technology and Innovation Foundation (ITIF)

On a summer visit to Gujarat state, U.S. Treasury Secretary Janet Yellen echoed the words of President Biden in calling India “an indispensable partner” to build resilience in supply chains. Yellen pointed to Apple and Google’s expanding smartphone production in India as examples of successful “friendshoring” — moving manufacturing to countries that the U.S. shares closer geopolitical affinity with than China.

Friendshoring emerged as a U.S. strategy during the Covid-19 pandemic, when America’s overreliance on Chinese manufacturing became painfully evident. But the idea has become all the more urgent as Beijing’s policies have proven increasingly unpredictable for businesses.

“India’s diversity, political pluralism and open market economy put its bonds with the U.S., and more broadly the West, on more sure footing,” explains C. Raja Mohan, Senior Fellow at the Asia Society Policy Institute in New Delhi.

Despite Beijing’s recent overtures to attract U.S. investment, on-the-ground challenges in China are mounting for foreign companies. For instance, Foxconn, Apple’s main supplier, came under a sudden tax probe by Chinese authorities last month, presumably for political reasons since Foxconn’s founder, Terry Gou, is running for president in Taiwan. The disturbance underscored the need behind Apple’s recent moves into India.

“Some people might say that it is next to impossible to diversify from China, but it has become a matter of necessity for businesses around the world,” says Seung-Youn Oh, an associate professor at Bryn Mawr College.

This represents a golden opportunity for Prime Minister Modi and his longstanding “Make in India” initiative to bolster India’s manufacturing competitiveness.

But even after recently upping the stakes by offering billions in new incentives across a long line of manufacturing sectors, success isn’t guaranteed. For years, New Delhi’s industrial strategy has struggled to raise the share of manufacturing in the domestic economy and maintain steady growth in foreign investment. The biggest failure to date is the exit of Foxconn from a $19 billion joint venture with the Indian conglomerate Vedanta to establish semiconductor plants.

Indeed, making it in India is not easy, and what seems an obvious idea in geopolitical or boardroom foresight sessions is harder to get done in practice. If there is any chance of American multinationals diversifying away from China’s highly skilled workforce and well-oiled logistical machine, they must both negotiate New Delhi’s localization demands and overcome multiple domestic challenges, from thick bureaucratic red tape to patchy infrastructure.

“India has been the economy of tomorrow for the past 30 years,” says Ezell. “If it can ever just get its policy environment right, India could become the economy of today.”

THE SUBCOMPONENTS OF GLOBAL POWER

This spring, when India officially became the world’s most populous country at 1.425 billion people, China brushed off losing the long-held and oft-celebrated number one spot. As a Chinese foreign affairs spokesperson said, “When assessing a country’s demographic dividend, we need to look at not just its size but also its quality.”

Doubt is often cast on the Indian market living up to expectations because of its low per capita income, a deficit of skilled manufacturing labor and poor infrastructure. Despite the growth of its middle class, many Indians still live by the Hindi phrase of roti, kapada aur makaan, seeking the basic necessities of ‘food, clothing, and shelter.’ India’s life expectancy and literacy rates are still below those China reached in 2001, and the last “Doing Business” report by the World Bank ranked India 63rd and China 31st out of 190 countries.

Yet industry insiders take exception to the notion that India’s workforce lacks quality, pointing to its robust IT services sector, lead ranking of STEM graduates, and talent pool of software developers. Moreover, quantity still matters. Natixis research ranked India as the most attractive among Asia’s youthful countries for offshoring labor-intensive manufacturing because of the sheer size of its young, under-40 workforce.

“We have a huge educated, English-speaking workforce that is a ready-made natural resource if you want to train Indian engineers,” says Harshvardhan Sharma, head of Auto Retail Practice at Nomura Research Institute, a global consulting firm.

As several industries go through digital transitions, Sharma adds, India is well-positioned to reap the benefits with expanding research and development activities.

“One of the transformations happening today is the software-ization of the automobile industry,” he says. “Cars are now gadgets with wheels since there is so much code that goes inside. That’s a great advantage for India.”

Others point to Apple’s steady progress in India. After numerous operational challenges since 2017, when it first turned to India, Apple contractors now assemble 7 percent of iPhones in Indian factories. Some analysts even estimate that India will match China’s iPhone output, making 45 to 50 percent by 2027.

“Global players are really trying to exploit the fact that India’s working age population is already quite big and is primed to grow dramatically,” says Puneet Gupta, a director at S&P Global Mobility.

But, especially when it comes to mobile phones, critics are quick to point out that Modi’s “Make in India” initiative is essentially “Assemble in India.” Even for companies that appear to be performing well in India, China still has a strong hold on essential inputs in electronics, solar, pharmaceuticals and elsewhere. Hyundai sources tires, seats, and other parts from local manufacturers, for instance, but nearly one-third of auto components vital for the industry still come from China. That share will likely rise as more electric vehicles — a green technology in which Chinese suppliers are critical — hit Indian streets in the years to come.

This conundrum introduces subtraction to multinationals’ coveted “China plus one” equation. But there are signs that workable solutions are possible. For starters, assembly may represent a small share of the value-added manufacturing activity, but with a competitive edge of low-cost labor and a helping industrial hand, it can blossom into more.

“We see that, progressively, final assembly investment is drawing in more downstream investments,” says Agatha Kratz, a director at Rhodium Group. Kratz points to Vietnam as an early example of this co-location process in digital and green technologies.

Southeast Asia benefited from investments from Chinese players, which India often shuns. But suppliers are still rolling into India over time.

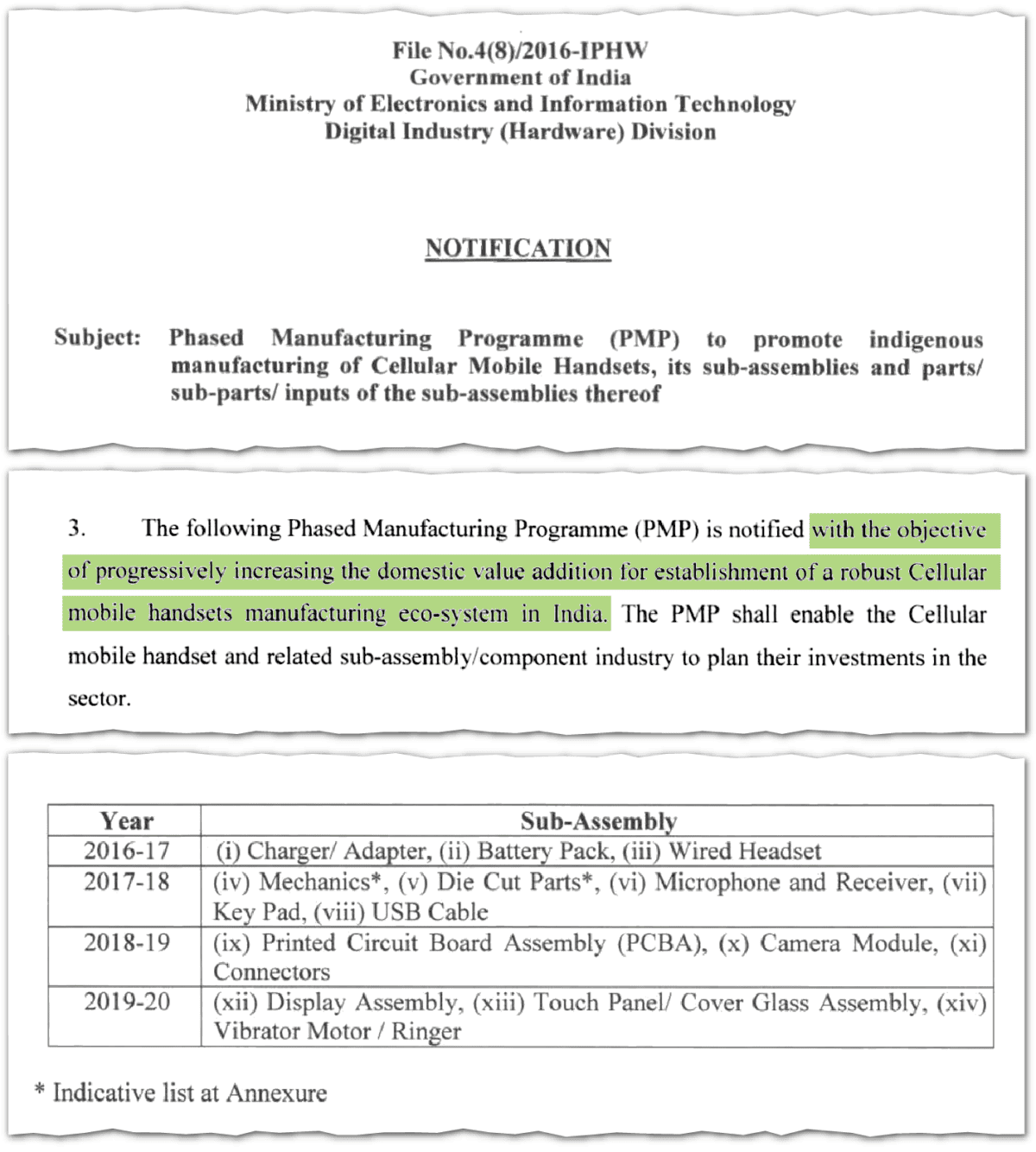

After New Delhi introduced import duties on finished mobile phones, for example, it then targeted components, such as chargers, battery packs and printed circuit boards, which helped to draw in foreign investment. First movers, such as South Korea’s Samsung, advanced activities to the sub-assembly of components and some manufacturing. According to Counterpoint Research, on average, local value addition in mobile phone manufacturing in India grew from the low single digits in 2014 to 16 percent in 2023.1There are key differences between foreign investors. For example, Samsung, which is India’s smartphone market leader, has a relatively high local value added at 25–30 percent.

“India is in the right place at the right time,” says Tarun Pathak, research director at Counterpoint Research. “By 2030, we expect India to reach at least 35 to 40 percent of valuation.”

As a point of comparison, Chinese components make up only 47 percent of the value in Huawei’s new flagship Mate 60 smartphone.

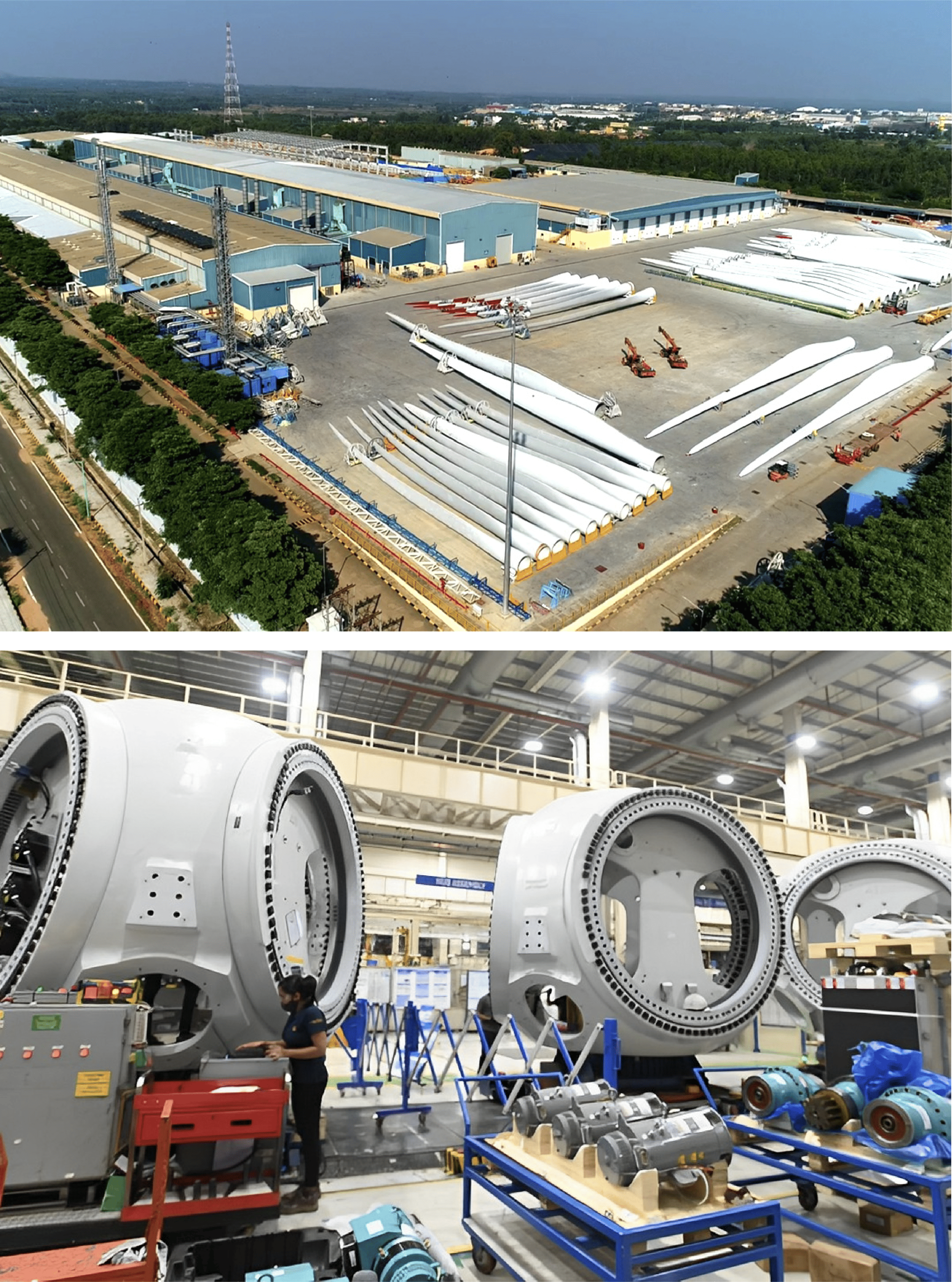

The investments of European and American wind manufacturers in India present another case in point for the potential to develop new supply ecosystems outside of China.

China dominates green supply chains. According to the International Energy Agency, China holds between 60 and 75 percent of the global manufacturing capacity in wind, solar and battery technologies. It also commands the processing of over half the world’s production of lithium, nickel and cobalt and 90 percent of processed rare earths — all of which are essential in making green technologies.

Business executives need to change their mindsets. It should not be about running away from a changing China but about exploring new markets and new opportunities.

Seung-Youn Oh, an associate professor at Bryn Mawr College

But in the late 2010s, leading Western wind companies began closing some facilities in China due to weakening demand, rising domestic competition, and the growing unpredictability of the Chinese government. Beginning in 2016, tens of thousands of factories across China were temporarily shut down by environmental authorities to enforce emission limits. The crackdown rarely affected multinationals directly, but the sudden closures represented a serious supply chain disturbance.

In response, the Denmark-based Vestas as well as America’s GE Renewable Energy began building manufacturing capacity in India.

“From time to time, the Chinese government takes drastic measures that force people to look into alternatives,” says Charles McCall, who was a senior director at Vestas in India until this spring. “I spent an awful lot of time and energy convincing suppliers to invest and build factories in India.’

By 2019, McCall says, around 80 percent of his factories’ bill of materials (the costs associated with a finished product) came from foreign and domestic suppliers based in India.

Although they may not have known it at the time, the wind energy companies were among the first western multinationals to start de-risking from China: A foundation for wind turbine manufacturing was put in place.

“There are still certain critical components and subcomponents, like casting and forging, that need to come from China and outside markets,” says Francis Jayasurya, India director at Global Wind Energy Council (GWEC), a global trade council for wind industry. “But almost everything is made in India.”

According to GWEC, India accounts for 7 to 12 percent of global manufacturing capacity in blades, generators, and gearboxes — some of the main components of a wind turbine. That figure may not seem like a lot, especially since China accounts for between 60 and 75 percent of the global supply chain for these components — but the manufacturing capacity in India has already proven valuable: When production facilities were closed in China during the pandemic, the Indian factories served as “a stopgap solution.”

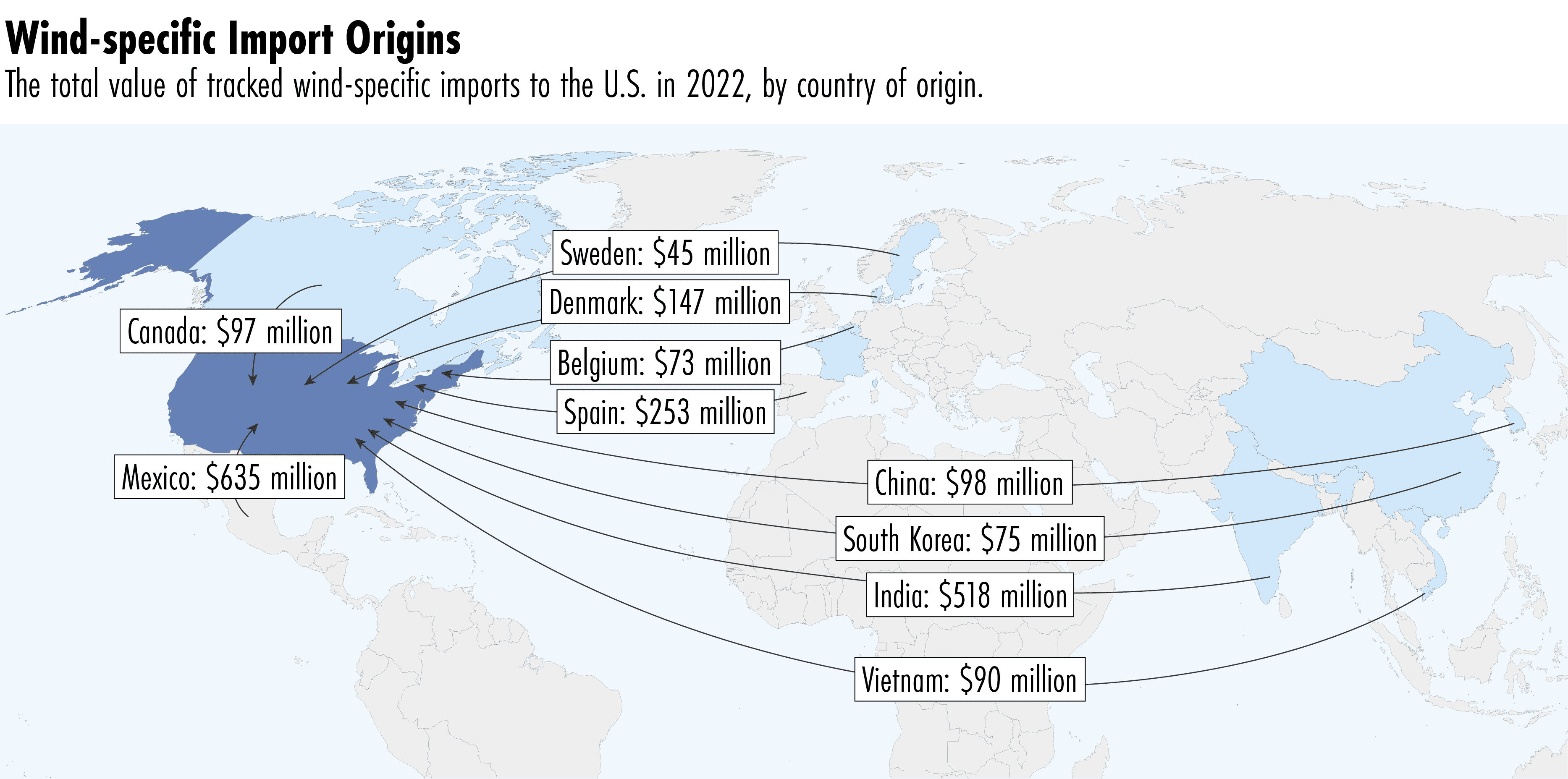

Since then, geopolitical winds have been at India’s back, with industrial strategies in the U.S. and European Union making it difficult for China-based wind exporters.

Indian wind components grew from representing 19 percent of total U.S. imports in 2020 to 24 percent in 2022. (China’s fell from 13 to 4 percent in the same period.) India only trails neighboring Mexico as America’s main source of wind turbine components.

Indian turbines, however, remain 30 to 60 percent more expensive than their Chinese counterparts, according to GWEC. The Indian market, and much of the global wind industry, is also in recovery after the Covid downturn and manufactured capacity levels in Indian factories are presently underutilized.

“We have the technology and talent, but we need to make investment in India more viable,” Jayasurya says.

For the Indian wind industry to have a real chance in realizing its full potential, Jayasurya argues that New Delhi should launch an incentive scheme specifically for wind components — as it has for several other industries. Even if Washington’s Inflation Reduction Act undermines some Indian wind component exports to the American market, a U.S. Department of Energy report projects that American production in blades and other subcomponents will be lower than demand and require outside supply.

McCall, the former Vestas director, also explains that India’s infrastructure deficit is not as crippling as some make it out to be. A Goldman Sachs study, for instance, found that a 2,000-kilometer delivery can be completed within 24 hours in China but could take as long as five to seven days in India.

But India’s main manufacturing hubs are extremely well connected and reliable, says McCall. “The transit times are long because the average speed is pretty low in India, but if they say it is four days, it is usually four days, and we can configure our buying system accordingly.” he says. “It is variability that is difficult to handle.”

India cannot match China’s decades-long infrastructure binge. But since 2014 it has rolled out a massive highway and road expansion, doubled its airports, and recently launched an important freight train corridor to bolster transportation capacity.

For India and its corporate suitors alike, de-risking decisions will involve billions of dollars, moving talents within corporations and making new political connections. But Oh, of Bryn Mawr College, argues that multinationals must quickly adapt or else risk paying a steep price.

“Business executives need to change their mindsets. It should not be about running away from a changing China but about exploring new markets and new opportunities,” she says. “They need to learn how to turn geopolitical risk into geopolitical premium.”

THE NEXT COMPETITOR?

The Indian market may play an important role in the de-risking story for American multinationals, but multiple analysts also warned that India’s tomorrow may not look like what America imagines. India’s changing politics and sometimes contradictory business environment could present foreign investors with new complications down the road.

This year, for example, Indian authorities have both raided the offices of Chinese phone maker Xiaomi for alleged foreign exchange violations and accused its more geopolitical-friendly Korean counterpart Samsung of evading import duties. This week, Indian officials also announced a tax probe of Apple, Google and Amazon. Whether these represent deeds of corporate misconduct or not, the U.S. State Department has warned American investors of “discriminatory” government policies that favor domestic companies.

The big question in the long term is whether New Delhi and India’s leading companies will be content watching their foreign counterparts dominate the Indian market. Similar to China, India has a proud nationalism about its place in the world. Before the forceful intervention of western colonialism, Indian textiles and spices drained the Roman Empire’s coffers of gold, and its trade stretched across Southeast Asia, the Middle East and Africa, making it the world’s leading economy.

“There is a long and relatively unbroken tradition from Nehru to Modi of taking pride in India’s past civilizational greatness that was ruined by the depredations of external empires,” says Rohan Mukherjee, assistant professor at the London School of Economics and Political Science.

India now looks to the 21st century to fully realize its economic miracle and regain its lost worldly significance. Although Modi and his top officials stress that their new mantra of self-reliance does not translate into economic protectionism, Indian officials are indeed insistent on foreign multinationals meeting their terms. Headway on Tesla’s investment has been slowed, for example, by New Delhi’s demands that the Austin-based company make strong commitments on sourcing components locally.

“There are many great opportunities for American companies in India,” says David Moschella, a nonresident senior fellow at ITIF, “but just like China in hardware, India is moving up the value chain in software, R&D, semiconductor chip design, and innovation in cloud computing and AI.”

Some believe the new bonhomie is linked to the current shared concerns about China, but deepening commercial ties and expanding security ties are at the heart of the new relationship.

C. Raja Mohan, Senior Fellow at the Asia Society Policy Institute in New Delhi

Moschella warns that no one in Washington is paying heed to America’s widespread dependencies on IT and other computing services from Indian companies such as Infosys and Tata Consultancy Services and has called on American policymakers to manage these issues.

“Dependency is dependency and at some point, people are going to exploit it,” he says.

Others see a more promising geopolitical path ahead for India-U.S. relations. “Some believe the new bonhomie is linked to the current shared concerns about China,” says Asia Society’s Mohan. “But deepening commercial ties and expanding security ties are at the heart of the new relationship.”

General Electric Aviation and Hindustan Aeronautics previously signed an MOU to develop and supply ring forgings for military and commercial engine programmes, February 4, 2021. Credit: HAL

Indeed, just as Washington aims to halt advanced technology investments in China that have dual use purposes, it green-lighted a partnership between General Electric and India’s state-owned Hindustan Aeronautics to jointly make engines for jet fighters of the Indian Air Force.

Yet experts agree that New Delhi is not seeking to become another American ally and is itself conscious about the risks of its American dependencies.

“Self-reliance for India doesn’t mean a pro-Western stance; it means a pro India stance,” says Mukherjee from LSE.

For the time being, at least, what’s good for Western economies is also good for India’s — with none of it good for China’s. India alone may not make a major dent in China’s overall role in global manufacturing, but alongside Vietnam, Mexico, and other de-risking destinations, it represents a critical multiplier in diversification strategies.

And the “China plus one” strategy, argues García Herrero from Natixis, can offer better returns for the multinationals willing to embrace it, especially as China’s market becomes less relevant in the years ahead.

“Companies do not necessarily value systemic risk,” she says. “But they care about the market. And if the market shrinks, they run.”

Indeed, India’s role as the economy of the future may seem to be a long way off. But tomorrow is just a day away.

Luke Patey is a senior researcher at the Danish Institute for International Studies. He is author of How China Loses: The Pushback Against China’s Global Ambitions. His work has been published in The New York Times, Financial Times, The Guardian, The Hindu, Foreign Affairs and Foreign Policy. @LukePatey