Zongyuan Zoe Liu is the Maurice R. Greenberg Fellow for China studies at the Council on Foreign Relations, where she specializes in Chinese studies with a focus on international political economy. Her new book, Sovereign Funds: How the Communist Party of China Finances its Global Ambitions, explores the history and impact of the enormous investment funds China has set up over the last two decades in order to utilize its huge pile of foreign exchange reserves. In the following lightly edited interview, we discussed Beijing’s evolving ambitions for its sovereign wealth funds, their controversial investments in the U.S. and elsewhere, and their future in a world often growing more skeptical towards Chinese capital.

Illustration by Kate Copeland

Q: Sovereign wealth funds (SWFs) have become a huge force in international finance, in places from Norway to Saudi Arabia. Can you start by explaining what they typically are?

A: There isn’t a universally accepted definition of what is or is not a sovereign wealth fund. But one thing that people do agree on is that SWFs are government-owned investment institutions.

They are increasingly important today for three reasons. The first one is their size: As institutional investors, they are big. They manage more than $11 trillion in assets, using a conservative estimate, which means they can move markets and even define investment trends.

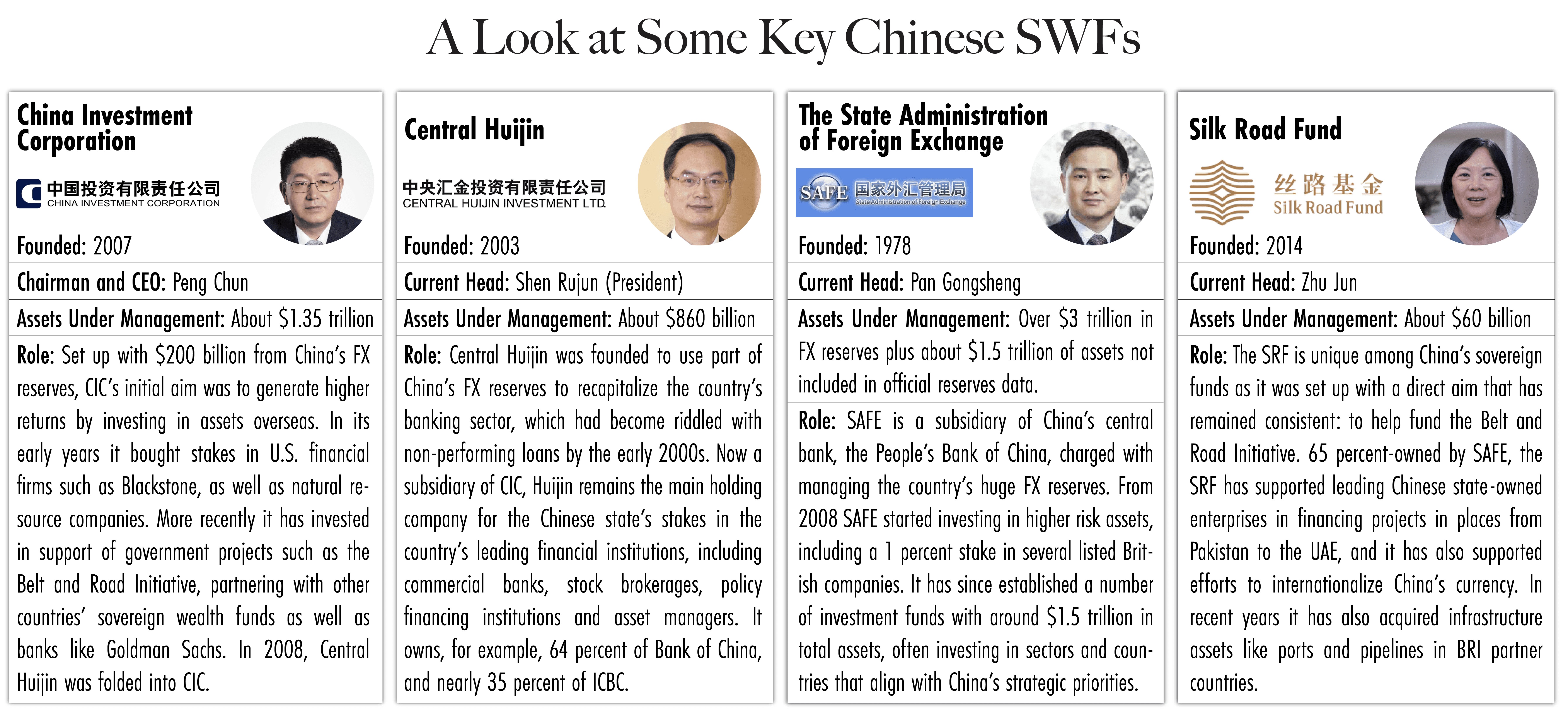

China is important because it has more than one SWF. The one that many people are familiar with, the China Investment Corporation (CIC), is just one of China’s funds. As of last year, CIC had already become the largest sovereign fund in the world, managing more than $1.35 trillion in assets: that’s larger than Mexico’s GDP, and Mexico is the world’s 15th largest economy.

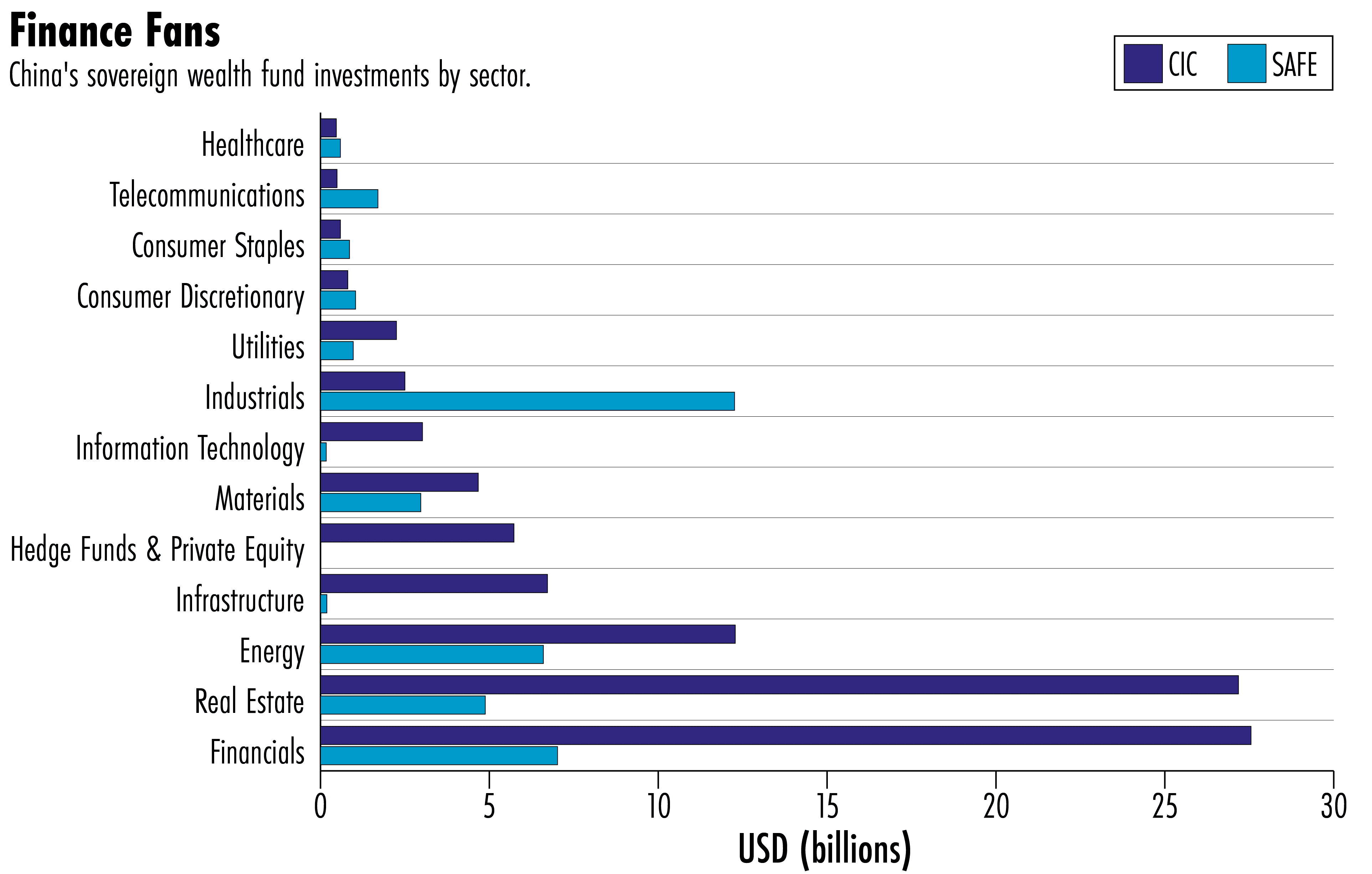

Moreover, funds owned by SAFE [the State Administration of Foreign Exchange, the part of China’s central bank which administers the country’s foreign exchange reserves] manage about $1.5 trillion assets that are not counted towards China’s foreign exchange reserves. These assets have been used directly to capitalize China’s strategically-oriented funds, such as the Silk Road Fund and major policy banks, to finance projects related to the Belt and Road Initiative, and to help Chinese state-owned enterprises to acquire overseas assets ranging from natural resources to infrastructure projects. So they are big, and important.

| BIO AT A GLANCE | |

|---|---|

| AGE | 36 |

| BIRTHPLACE | China |

| CURRENT POSITION | Maurice R. Greenberg Fellow for China Studies at the Council on Foreign Relations |

My second point is the role SWFs play in supporting the development plans and strategic visions of their host countries and their political leaders. China is perhaps the most representative of this trend, but it is not alone. It used to be that SWFs, such as those in the Middle East that were capitalized by revenue from commodities, were not supposed to invest domestically, whether in support of industrial policies or development plans. But now things have changed. Saudi Arabia’s huge (PIF) is financing a lot of Crown Prince Mohammed bin Salman’s strategic vision for the country.

This brings me to my third point, which is that a lot of existing SWFs have been established by non-Western countries, whose leaders may not share the same global vision and governance ideas as Western countries. Perhaps the most relevant example would be Russia. The reason why Putin’s regime has been economically and financially resilient so far, despite a concerted sanctions effort by the West, is because of the existence of the Russian sovereign wealth funds. Russia has several: perhaps the most notable, which is currently under Western sanctions, is Russia’s National Wealth Fund. According to Russia’s finance minister, it spent more than 3 trillion rubles to cushion the economy and cover the fiscal budget deficit last year, and despite sanctions on it, it was still able to grow. So a lot of this fits into the bigger picture of great power competition.

Why did China look to set up its own sovereign wealth funds and how did they differ from those we see in commodity-rich countries?

| MISCELLANEA | |

|---|---|

| FAVORITE BOOKS | Non-Fiction:The Great Transformation: The Political and Economic Origins of Our Time by Karl Polanyi. Novel: Dream of the Red Chamber by Cao Xueqin |

| FAVORITE MUSIC | Simon-Garfunkel type. I think my music taste has not changed since middle school. |

| FAVORITE FILM | So far it is The Usual Suspects. |

| MOST ADMIRED | My mom and dad, no doubt. |

The first fund that China established was actually a special purpose vehicle called Central Huijin. It was created out of a crisis — and this actually applies to the later birth of CIC, as well as a lot of SAFE-affiliated investment companies.

Central Huijin was created basically to solve China’s domestic banking crisis in the late 1990s and early 2000s. Major Chinese banks were suffering from the chronic problem of non-performing loans. The Chinese government ultimately decided to save the banks from insolvency and recapitalize them, by using the foreign exchange reserves managed by the People’s Bank of China [China’s central bank] to create Central Huijin. It later took on a life of its own, restructuring China’s other non-banking financial institutions.

The establishment of CIC came amid a domestic debate about how to diversify China’s foreign exchange reserves in a search for a higher return. People had started to realize that holding the majority of China’s foreign exchange reserve assets in U.S. Treasuries was not necessarily the best way to manage its investments. Against that background, people started to say that China really needed to invest in strategic assets and sectors, including natural resources and critical technologies, where it didn’t yet have enough capacity. The decision to create CIC was made in 2007, just before the 2008 global financial crisis. The transformation in the global financial system as a result of the crisis catalyzed the Chinese government’s decision to move forward with the plan to diversify its foreign exchange reserves.

While most people call these sorts of institutions sovereign wealth funds, in the case of China you describe them as ‘sovereign leveraged funds’. Could you explain that bit of jargon and why you use that term?

The reason why I use the term ‘leveraged’, is that China’s funds are different in terms of how they are capitalized, in how their balance sheet looks, and in the politics around them.

Your question goes to the heart of how I became interested in sovereign funds. Back when I was doing my doctoral dissertation, I was interested in energy security and the idea of China shifting in 1994 to become a net oil importer, rather than a net oil exporter. Quickly, within 10 years, China emerged as one of the world’s largest crude oil importers, and later one of its largest natural gas importers, particularly of liquefied natural gas (LNG). This presented a puzzle to me: Most of the world’s largest sovereign wealth funds had previously been established by commodity-exporting economies. From the Kuwaiti SWF established in 1953 to the Norwegian SWF, these institutions were about the monetization of God-given resources. Yes, China has natural resources, but it is not a commodity-based economy: so how was it able to have a sovereign wealth fund?

When I looked at how the Chinese funds were capitalized, I realized that in the case of CIC, it involved the use of leverage. The Ministry of Finance issued a special purpose bond, using the proceeds to purchase foreign exchange reserves from the People’s Bank of China (PBOC). So this whole process involved the expansion of the state’s balance sheet, through the issue of the new bond: hence, this is the use of leverage.

I would say Chinese leaders’ decision from the early 2000s to use the foreign exchange reserves to create China’s sovereign leveraged funds was primarily motivated by domestic considerations, rather than with an intention to weaponize their reserves.

In addition to this ‘explicit’ use of leverage, there was also the ‘implicit’ use of leverage. The implicit leverage applies to other Chinese sovereign funds directly affiliated with SAFE, which is a subsidiary of the PBOC. The idea there is slightly different: it involves a different risk profile. In normal foreign exchange reserve management, the cardinal rule is to be risk-averse. In other words you want to make sure that your foreign exchange reserves are liquid and risk-free.

That’s why they mostly invest in U.S. Treasuries, right?

Exactly. But because the PBOC had effectively lost some of the foreign exchange reserves it managed to the Ministry of Finance when it capitalized CIC, there was a kind of institutional battle between the two, which are perhaps the most influential policy making agencies in China’s economic and financial set up.

So what SAFE did was to re-characterize the risk profile of some of its foreign exchange reserve assets. Under the IMF’s definition, the moment when foreign exchange reserves assets are invested in [higher] risk-bearing assets, they are no longer officially classified as foreign exchange reserves. By extension, this means that when SAFE uses part of China’s FX reserves to invest in, say, critical infrastructure or a foreign company, these are no longer counted as part of China’s foreign exchange reserves, but instead they become risk-bearing assets. This process does not involve the expansion of the government balance sheet, hence, it is not the ‘explicit’ use of leverage. But it does mean the risk profile [of the central bank’s assets] has gone up. This is what I call ‘implicit’ leverage.

So China’s SWFs are not necessarily sovereign wealth funds to the same extent as the Abu Dhabi Investment Authority, or the Qatar Investment Authority, or for that matter Norway’s. But they involve the government using either ‘explicit’ or ‘implicit’ leverage.

To what extent was the current role of China’s SWFs planned at the outset? And to what extent has their role changed over time?

Most of China’s sovereign funds were not established with any strategic vision or any explicit economic or geopolitical ambitions. The primary example so far would be the Silk Road Fund, and also a number of smaller industrial cooperation funds such as China-Africa Industrial Capacity Cooperation Fund and China-Latin America Cooperation Fund. The Silk Road Fund was created specifically for the purpose of financing the Belt and Road Initiative and its largest investor is SAFE, China’s foreign exchange reserve management agency. Moreover, the Silk Road Fund has also been used to expand the role of the renminbi in BRI countries.

Apart from this, the others were created either to solve an urgent domestic crisis, in the case of Central Huijin, or to diversify China’s foreign exchange reserves. I would say Chinese leaders’ decision from the early 2000s to use the foreign exchange reserves to create China’s sovereign leveraged funds was primarily motivated by domestic considerations, rather than with an intention to weaponize their reserves. But as leaders change and as their ambitions change, they retrofit new mandates to the institutions.

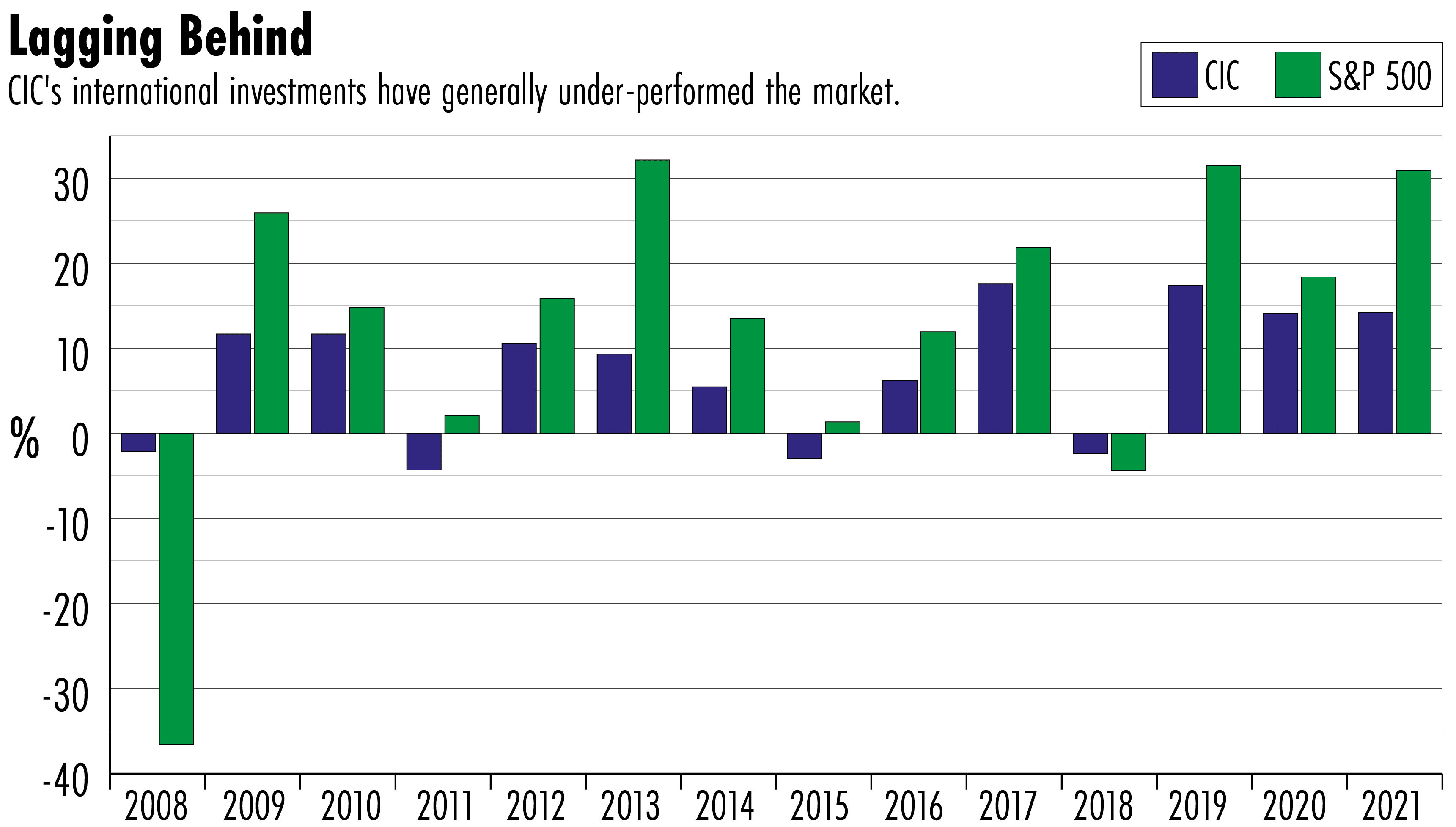

In its first few years, CIC made some pretty disastrous investments, at least in terms of financial returns. Can you talk us through those and, and how that was received within China?

Yes, in the early years, CIC’s investment record was not great. Looking at CIC’s international investment performance, benchmarking it against a global portfolio, it’s at most mediocre either compared to its international peers, or even the S&P 500 — in many years, it’s lower. In other words, if you were to just passively invest in an index fund it would probably generate more return.

In the early years, the subpar return was related to CIC’s lack of investment of talent. I remember talking with a former CIC equity investment manager who currently runs his own private equity fund in China. He had worked in the state sector before moving to Central Huijin, and from there moved to CIC’s international management division. He observed that when CIC was established back in 2007, it had less than a dozen investment officers and they had $200 billion dollars to invest. The time pressure to reduce the cash drag and to quickly make investments meant they did not have a lot of time to do due diligence on potential investments. On top of that, they did not have a huge amount of talented people familiar with international markets.

One particularly controversial investment CIC made was its very first investment, its debut in the international markets, which was to invest in [U.S. private equity firm] Blackstone. The timing of its investment in Blackstone was, to be honest, questionable. After CIC bought its shares in the pre-IPO subscription, Blackstone’s two founders, Stephen Schwarzman and Peter Peterson, sold combined shares worth more than $10 billion as part of the Blackstone IPO. People don’t sell their shares when they think they are undervalued: The fact that the founders sold their shares after CIC bought into the IPO speaks a lot to CIC’s investment decision. And obviously, CIC’s loss on paper was tremendous during the global financial crisis when Blackstone’s shares dropped from above $30 per share at the IPO to as low as around $3.50.

Of course, this was a loss on paper, it doesn’t mean CIC actually materialized the loss. When it eventually sold its Blackstone stake in 2018, it actually made money. So I would say yes, they made some questionable decisions. But that can partially be explained by the lack of talent in the initial years. Later, CIC built up its investment team. Its under-performance more recently can be better explained by its pursuit of non-financial returns.

Right — would it be fair to say that if one of the main initial aims of setting up CIC was to earn China a better return on its FX reserves, that objective has become secondary to other considerations, such as supporting China’s strategic objectives overseas?

Yes, I think that is fair. In the early days, CIC was in a rush to invest in high profile companies, in particular, in financial companies in the United States. Some of the people that I talked to disclosed that the decision to invest in Blackstone was actually strategic, in the sense that they were not just interested in U.S. financial companies, they were also interested in building a long term relationship, both in terms of having access to top financial or investment talent, as well as to people who can influence U.S. policy making.

In the broader context, I think the investment strategy actually played out quite well, both in terms of having access to very important people and policy influencers, like Schwarzman; or for that matter, building up a network with firms like Goldman Sachs.

On the other hand, if you look at CIC’s investment pattern, especially after the launch of the Belt and Road Initiative in 2013, it supported this initiative, by making investments directly, as well as supporting Chinese companies to expand overseas. This was not just done by CIC, but also by other Chinese sovereign leveraged funds, including ones that are affiliated with SAFE.

One of the interesting points that you make in your book, is that having CIC has enabled Beijing to exert influence over markets and to help to pursue China’s strategic objectives in the guise of having a big, professionally-run institutional investor. Can you explain that a bit more?

The Chinese economy has been characterized by scholars both inside and outside China as a form of authoritarian capitalism, or state capitalism. The idea is that the state, or the party, sits on top of economic and financial decision making. This applies to China’s domestic territory: the party and the Chinese government can govern, control and directly influence capital flows, the allocation of assets, and pick winners in the domestic market: that’s relatively easy.

…in spite of the fact that none of these institutions are directly following decisions from the top leader of the Party, they are definitely influenced by it, in the same way as other state owned enterprises do.

But it cannot control or assert its influence in territories beyond the Chinese market. So from that perspective, having a state-owned but market-facing institution helps the Chinese government and the CCP to indirectly expand its influence overseas. CIC is a great example in the sense that when CIC presents itself in the international market, what you see is a group of highly skilled, highly experienced investors, many of whom have experience in Wall Street as well as in Europe.

Countries do not make deals: people make deals. When people meet with CIC representatives they realize they are not necessarily someone who is going to give them the Party spiel, but somebody who actually understands finance; so at a person-to-person level, they start to trust them as market-oriented investors. But when you look at a CIC as an organization, you realize that the majority of CIC’s assets are managed by its domestic arm, Central Huijin.

How does it actually work in practice: Who is telling CIC what to do?

I would say that decision making at CIC has shifted as the broader Chinese domestic political and economic environment has changed. Initially, when CIC was established back in 2007, the idea was to build up the investment team, build up the talent, and establish global connections with more prestigious international financiers. At that time, the idea was not necessarily for China to use CIC to achieve its strategic agenda, simply because it was a new institution.

Over the years, this has changed. If you talk with people at Chinese sovereign funds, in particular CIC, they will say, “We are an independently run institution, just like any other financial institution that makes its own decisions.” But at the same time, the senior management is appointed by the [Communist] Party, whose HR department appoints and confirms the CIC senior management. And as with other state-owned enterprises, CIC has its own party division, the idea being to ensure the Party’s leadership over every important institution inside China. So in spite of the fact that none of these institutions are directly following decisions from the top leader of the Party, they are definitely influenced by it, in the same way as other state owned enterprises do.

When you look at CIC’s senior managers, they are men of the Party (apart from the chairwoman of the Silk Road Fund). They internalize the Party agenda. For them, making a political mistake is far more costly than making a financial investment mistake, because you can justify a financial mistake by saying that there are external factors beyond my control. But a political mistake is beyond remedy.

Despite what you’ve said about the real nature of these organizations, we’ve seen several Western countries and big financial institutions teaming up with CIC. Are they being hoodwinked, or are they just following the money and the political power in China? Should these examples of cooperation come under more scrutiny?

I would take a step back by saying that the reason CIC and China’s other state-owned investors, partnered with a lot of these prestigious financial institutions in the early days was about having access to influential financial talent, so that they could become better at making investment decisions.

But increasingly, the reason CIC and others have looked to make these tie-ups has been the enhanced Western scrutiny of Chinese investment. If CIC makes investments directly [in Western companies] that is going to be frowned upon, and CFIUS [the Committee on Foreign Investment in the U.S.] and others would start asking questions and obstruct the investment. By partnering with Western investment funds like Blackstone, like Goldman Sachs, CIC can invest through joint venture funds, and then invest in targeted companies either in the United States or in Europe.

Partnerships with institutions make previously unattainable investment targets obtainable. And it also gives China access to Western policymakers. I would give one example to illustrate this point, which is CIC’s cooperation with Goldman Sachs, the so-called China-U.S. Industrial Cooperation Partnership. The announcement came in 2017 when [former President] Trump visited Beijing. Since then, China and the U.S. have become embroiled in a trade war, and CIC has liquidated its stake in Blackstone: But within the broader context of the U.S.-China relationship going south, the partnership between CIC and Goldman Sachs has endured.

Much depends upon how successfully American financial institutions can exert their influence through lobbying. Despite the broader context of enhanced U.S. scrutiny of FDI screening by CFIUS, back in September 2019 the U.S.-China Industrial Corporation partnership invested $3 billion in a U.S. company based in California called Boyd Corp, a thermal management tech provider and leading maker of engineered materials. CFIUS came in and said, CIC cannot do this and asked CIC to divest, citing some concerns about data privacy and all that. However, Goldman Sachs successfully convinced CFIUS to allow the purchase to proceed with CIC remaining as a minority investor through the cooperation fund. So depending upon how influential U.S. financial institutions are, and how willing to assert their influence and shape U.S. economic policies, individual investments can be compartmentalized, and can be insulated from the broader relationship downturn. Additionally, there are also prestigious and highly competent U.S. law firms specializing in international mergers and acquisitions. They are often capable of advising their sovereign fund clients in deal making and facilitating investments.

Do you think that the U.S. should be joining with other Western countries in taking a more skeptical view of China’s sovereign funds?

Right now, finance is increasingly being intertwined with national security: It’s not just China that is making strategically-oriented investments and using the state power for strategic finance, but the United States, the members of the European Union, Japan, and members of the Gulf Cooperation Council are doing similar things. From that perspective, given the strategic nature of Chinese state-owned investors, there perhaps needs to be some boundaries set over what should be permissible, what should and shouldn’t be off limits. The EU’s investment screening regime is a reaction against strategic investors from China, from Russia and the Middle East.

Perhaps there needs to be some sort of coordinated foreign direct investment screening as well. The United States has had a relatively sophisticated FDI screening regime for a long time. But the nature of globalization and globalized supply chains means that the European market and the Australian market and the Japanese market are very much intertwined with those in the United States, China, Vietnam, India, and so on. One company may not necessarily only have operations in one country. A more coordinated FDI screening regime from the United States and its allies and partners is relevant in terms of expertise sharing and due diligence investigation in cross-border investments. No one country can guard against multi-jurisdiction acquisitions by highly-motivated sovereign investors.

If we accept your argument that Chinese sovereign funds now have more of a strategic objective, how successful do you think they’ve been?

I would say they have been doing a tremendous job. If you look at the entire spectrum, right now, the biggest global concern is that China is dominating the global supply chain for electric vehicles, robotics and cobalt and so on. A lot of this did not come about overnight, but actually started from China’s debate about how to diversify its foreign exchange reserves to acquire overseas strategic assets and natural resources in the 2000s. And if you look at a lot of the concerns about China owning all those overseas port facilities and critical infrastructures: again, Chinese sovereign leveraged funds supported the acquisition of shares in overseas port facilities from Turkey to Melbourne, Australia. China’s sovereign funds helped the Party and the government not just to secure access to overseas natural resources to finance China’s economic growth, but also directly supported the BRI project, as well as providing China with a technological edge by directly financing China’s domestic giants such as Alibaba and Didi, and also directly acquiring overseas companies. So China’s sovereign funds have played an important role in transforming its comparative advantage in international trade into long-term competitive advantage in strategic sectors prioritized by the Party.

…the problem at the moment is that all these major Chinese financial institutions are very much deeply embedded in the dollar based financial system.

What are the risks for China using its FX reserves in this way? And what lessons do you think Beijing has drawn from the sanctions applied to Russia and its foreign exchange reserves after it invaded Ukraine?

Certainly if there had been no Russian invasion of Ukraine, the strategic vulnerability aspect would be not as salient as it is right now. And of course few countries would dare to risk their foreign exchange reserves in risky assets. The reason why China can do this is because its reserves are so large, it has more than $3 trillion worth of exchange reserves, double the size of Mexican GDP.

Having a lot of reserves does become a burden: the opportunity cost of concentrated investment becomes the driver to seek higher returns, and higher returns inherently mean higher risk. Right now, the intertwining of national security and finance means that China’s sovereign leveraged funds are not just bearing financial risk, but also geostrategic risk. These funds and their assets are not an uncompromised geoeconomic strength. Countries can exert their influence in global markets and buy influence in boardrooms, and also access to foreign policymakers. But having assets overseas exposes them as a target of geo economic attacks. In U.S.-led global markets, the portfolio assets of China’s sovereign leveraged funds could become a major strategic vulnerability in times of economic warfare triggered by or preceding an actual war. Putin’s invasion of Ukraine is a major signal: that’s probably why President Xi Jinping has been doubling down on self-reliance, not just technologically, but also financially.

So as much as this is a strength for China, having these enormous sovereign funds that can exert influence, at the same time, it’s a weakness because it can be used against them?

Yes. And this is particularly relevant for China’s globalized financial institutions right now. When we think about the largest banks in the world, many of them are Chinese banks: ICBC, Bank of China and so on, and their largest shareholder is Central Huijin, the domestic arm of the China Investment Corporation (CIC). And CIC also has a tremendous amount of assets exposed overseas.

This could become a strategic vulnerability or target of Western sanctions. But I would take a step back by looking at what Xi Jinping has been doing by using sovereign funds to intervene to create an alternative financial system. For example, CIC has been doing this, SAFE and its affiliated institutions, including the Silk Road Fund, publicly saying that they are actually engaging in developing the use of a renminbi based financial system: the whole idea is to try to build an insurance scheme in case of China being sanctioned. But the problem at the moment is that all these major Chinese financial institutions are very much deeply embedded in the dollar based financial system. CIC’s book is denominated in U.S. dollars. It is a vulnerability for China, but Xi has been trying to do a lot to make sanctions against Chinese entities more costly for the sanctioners. Part of the reason is because all these companies are invested in different segments of global supply chains. That also means that China can potentially weaponize their ability to finance global supply chains.

Andrew Peaple is a UK-based editor at The Wire. Previously, Andrew was a reporter and editor at The Wall Street Journal, including stints in Beijing from 2007 to 2010 and in Hong Kong from 2015 to 2019. Among other roles, Andrew was Asia editor for the Heard on the Street column, and the Asia markets editor. @andypeaps