The market for electric vehicle (EV) batteries has exploded in recent years, with private companies dominating production in China thus far. Now, through CALB Co., the Chinese state is looking to muscle its way in.

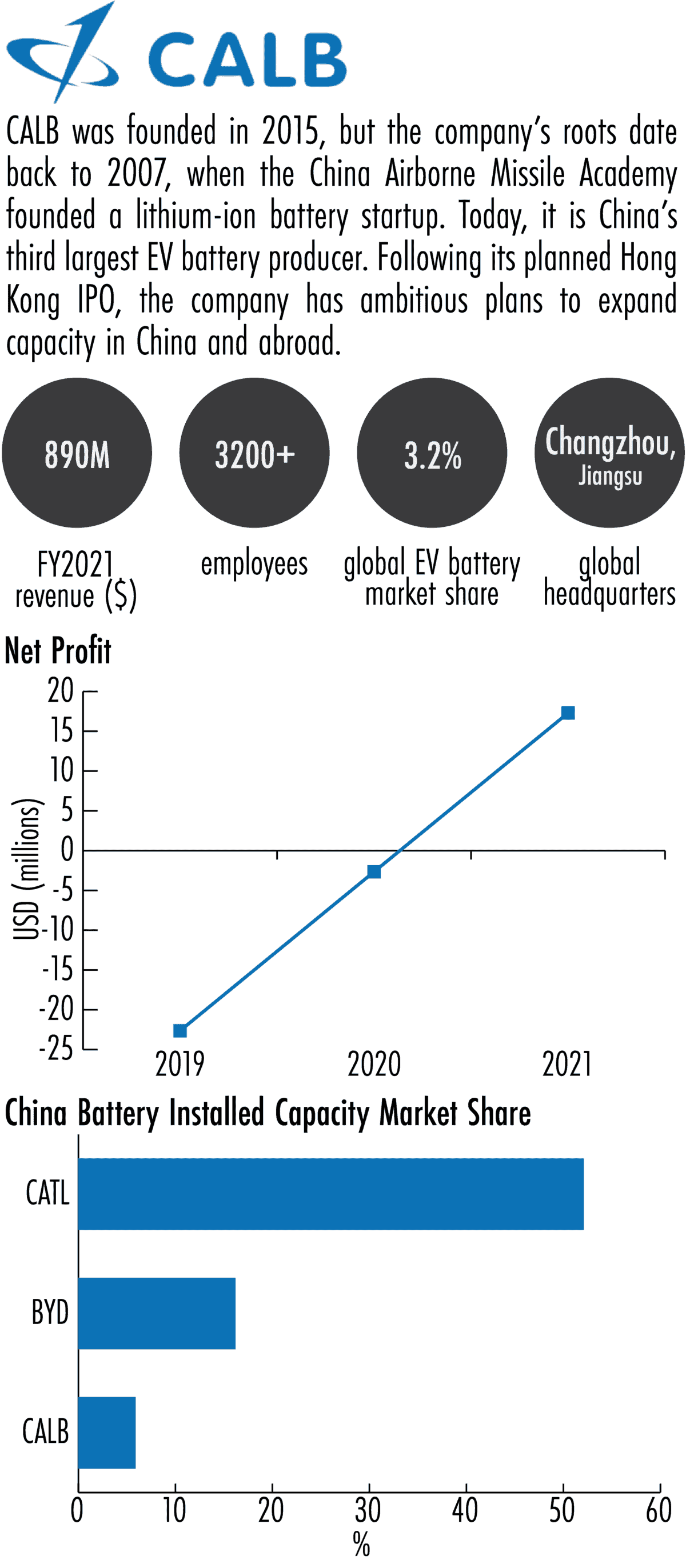

CALB’s share of the Chinese battery market stands at just 5.9 percent, but that already makes it the country’s third largest EV battery maker. Last week, the company filed for an initial public offering in Hong Kong, looking to raise $1.5 billion to catapult its growth and expand production capacity six-fold in the next two years.

But obstacles stand in its way, most notably the company’s affiliation with AVIC, the state-owned aerospace and defense conglomerate sanctioned by the U.S. government. This week, The Wire looks at CALB, its investors, and its ambitious plans to take on the world’s leading battery makers.

AVIC ROOTS

CALB produces batteries for civilian uses, but the company got its start as a subsidiary of Chinese military-linked entities. Its roots date back to 2007, when the China Airborne Missile Academy, which is engaged in the production of missiles and launchers, established a company called Sky Energy (Luoyang) to research lithium-ion batteries.

Sky Energy was restructured in 2009 as China Lithium Battery Technology (Luoyang) Co, with ownership later transferred to a company controlled by AVIC, the aerospace and defense conglomerate. CALB, which stands for China Aviation Lithium Battery Technology Company, was then established in 2015, with the Luoyang company as its controlling shareholder.

As an early entrant into the lithium-ion battery business with state backing, CALB seemed well positioned to take advantage of the lithium battery boom in the late 2010s. But the company was slow to react to a 2017 policy change which altered the kind of battery that would receive state subsidies, allowing rival manufacturers CATL and BYD to get ahead.

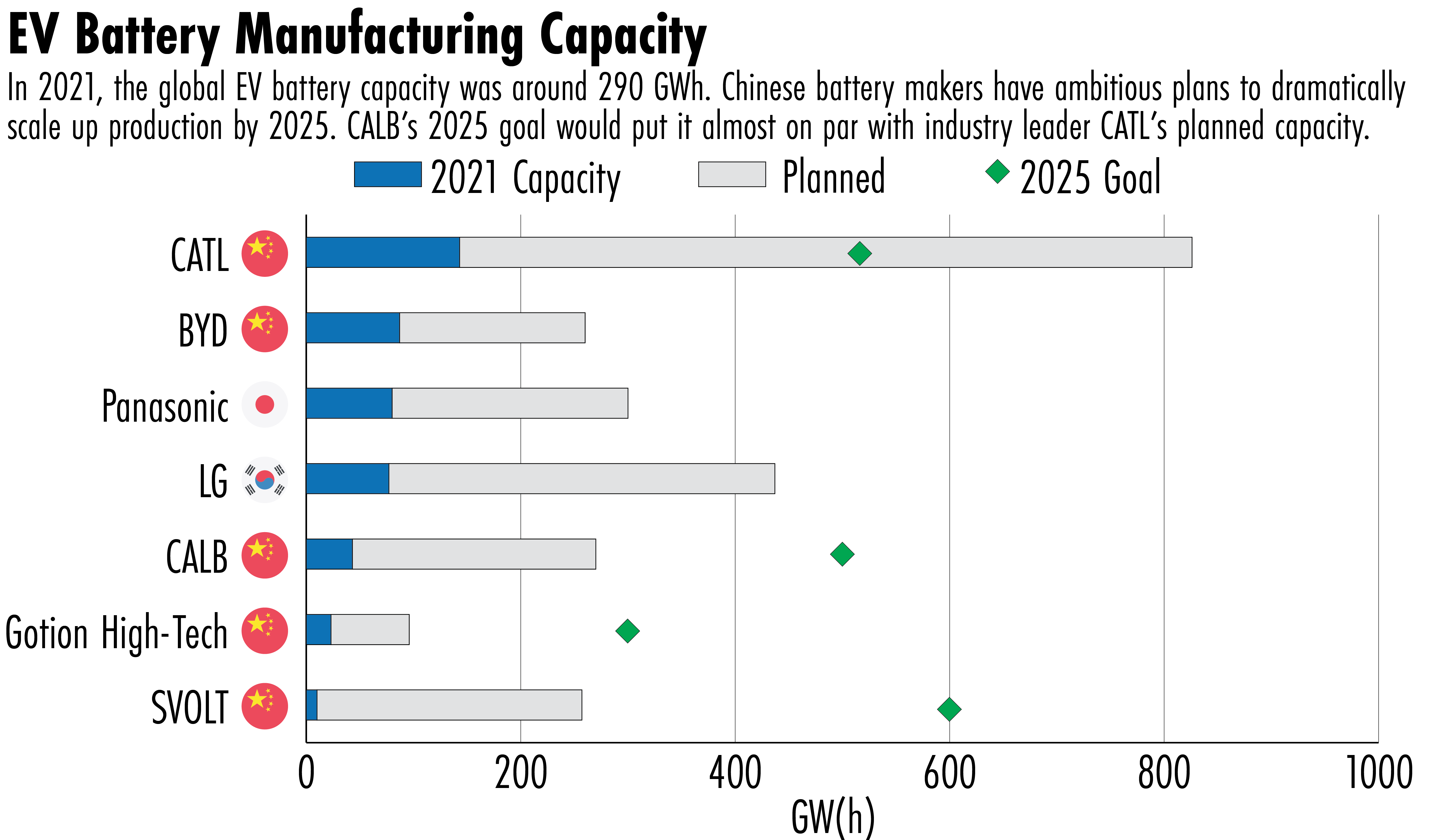

CATL and BYD, which are majority privately owned, today dominate China’s market, accounting for close to 70 percent of production capacity. But CALB plans to go head-to-head with its larger rivals within a few years: its 2025 production target of 500 GWh is just shy of CATL’s own projected capacity, according to data from Wood Mackenzie, an energy consultancy.

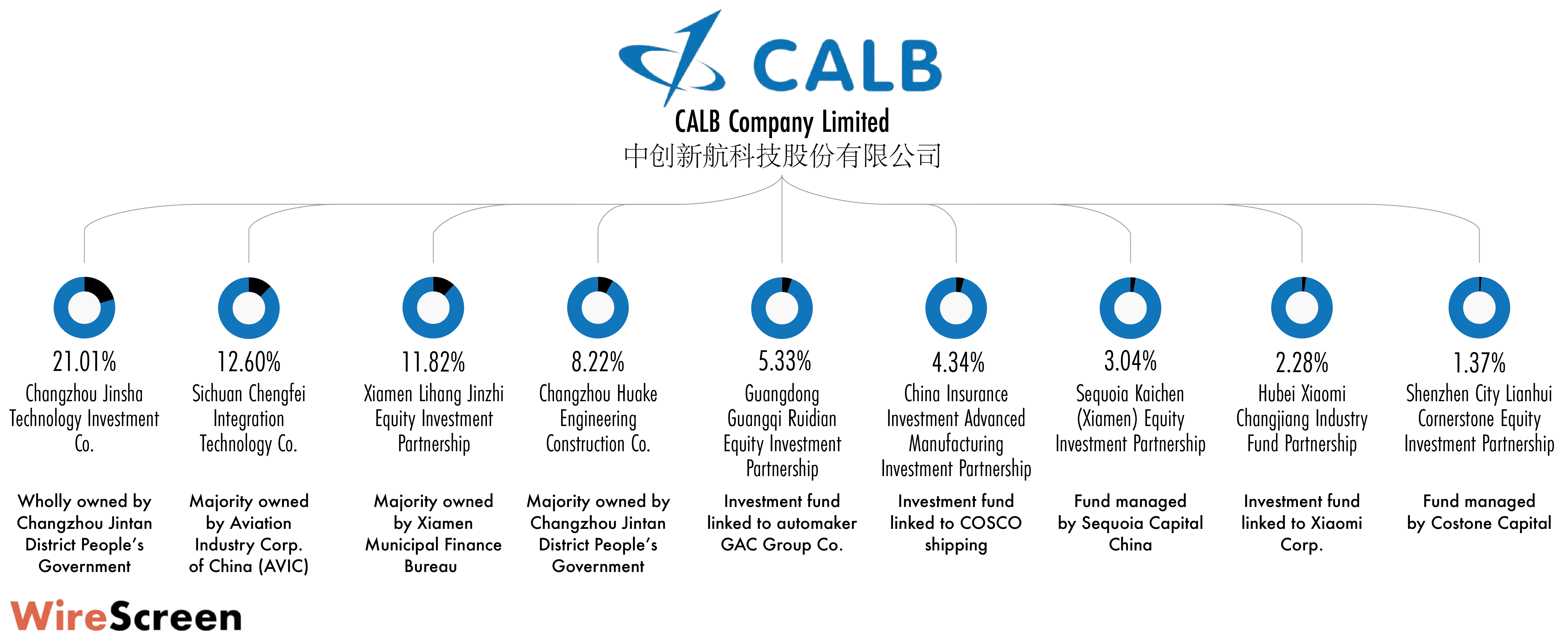

“CALB’s strong links with state-owned companies give it more channels to gain local government support and find different ways to raise capital,” says Kevin Shang, a battery materials analyst at Wood Mackenzie. The company’s two largest beneficial shareholders are the municipal governments of Changzhou and Xiamen, where the company has major production bases.

CUSTOMER COMPETITION

CALB’s customer base is small, but it includes some of China’s largest and fastest growing EV manufacturers. 70 percent of its 2021 revenue came from battery sales to state-owned car makers GAC and Changan — whose Aion S and Benben EV models were among China’s best selling last year — as well as privately held XPeng.

The deals to supply XPeng and GAC were big wins for CALB, as both manufacturers had previously been clients of rival CATL. Among China’s top three battery makers, competition for third-party customers is likely to be strongest between CATL and CALB, as second-ranked BYD’s batteries go toward its own vehicles. CATL sued CALB for IP infringement in two lawsuits last year filed in Chinese courts, seeking some $30 million in compensation. Those cases have yet to be resolved. CALB said in its IPO prospectus that it filed patent invalidation applications against the five patents CATL alleges it infringed upon, and maintains the company has always adhered to independent research and development.

But state-backing alone might not be enough to propel CALB to equal status with its larger competitor. “CATL’s vertical integration from mining to recycling provide advantages in terms of controlling cost,” says WoodMac’s Shang. The top Chinese producer has made investments in lithium and cobalt mines from Chile to the DRC, giving it an edge over its rivals at a time when mineral prices have soared. CALB also lacks the broad overseas customer base that CATL has, Shang adds, although the company is trying to change that by adding a battery plant in Europe.

CALB’S INVESTORS

One potential risk factor for CALB’s investors is the company’s links to AVIC. In August, AVIC and several affiliates were added to the U.S. Treasury Department’s list of companies sanctioned for military-industrial complex links, banning U.S. investors from investing in the company. AVIC is the majority shareholder of Sichuan Chengfei Integration Technology Co., which in turn is the third largest shareholder in CALB, with a 12.6 percent stake according to WireScreen.

CALB has taken steps ahead of its IPO filing to distance itself from any military links. A 2019 restructuring saw China Lithium Battery Technology (Luoyang) Co., then CALB’s controlling shareholder, restructured as a subsidiary of CALB. The Luoyang company was involved in the production of EV batteries for civil and military customers. CALB then sold its stake in the Luoyang company between November and March of this year to minimize the risk to its business from its links to a military supplier, according to CALB’s IPO prospectus.1See page 146

In addition to local governments and AVIC, CALB has some notable private investors, including smartphone maker Xiaomi and venture capital firms Sequoia Capital China and Costone Capital, a Shenzhen-based investment firm. These are some of CALB’s investors:

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen