As China’s population ages, the country’s authorities are facing the daunting question of who will cover the cost. When top leaders realized at the turn of the century that state pension funds would struggle to support the ballooning retired population, they created the National Social Security Fund (NSSF).

With more than $400 billion in assets under management at the end of 2020, the NSSF has since become one of the world’s largest sovereign wealth funds. One feature of its operations stands out: unlike the U.S. Social Security Trust Fund, which invests mainly in U.S. government securities, the NSSF is permitted to invest in equities and stocks.

This week, The Wire looks at the NSSF, what it invests in, and the challenges it faces as China confronts its looming old age crisis.

INVESTMENTS

The main pillar of China’s pension system is the country’s state-managed pension program, which encompasses a basic pay-as-you-go pension system — where contributors deduct a certain amount from their paychecks, often matched by an employer, to put in a personal pension pot — supported by the National Social Security Fund. A 2018 estimate by the Economist Intelligence Unit suggests the state-managed system accounts for 77 percent of China’s pension schemes, covering close to one billion people. Corporate retirement savings plans, the equivalent of a 401k in the U.S., account for most of the remaining share.

Founded in August 2000, the NSSF was designed as a strategic reserve to buttress state pension funds, particularly in provinces facing difficulties in paying their social security bills. Starting out with around 100 billion yuan in assets, the fund has posted an average annual return on investment of around 8.5 percent since it was set up (China’s average GDP growth rate over the same period was 8.7 percent). The fund logged a 15.9 percent yield in 2020, its highest in a decade, owing to a strong domestic stock market that year. It also earns revenue from funds allocated directly from the central government, and dividends from state-owned enterprises.

The fund is managed by the National Council for Social Security Fund, a ministerial-level agency overseen by a board of directors appointed by the Ministry of Finance. The NCSSF makes its own direct investments but a steadily increasing proportion of its funds are managed by an external investment manager. Overseas investments made up 9.7 percent of the total portfolio in 2020.

Regulations set in 2001 placed caps on the types of assets the fund is allowed to invest in:

- Bank deposits and treasury bonds (no less than 50 percent of total assets)

- Corporate and financial bonds (no more than 10 percent)

- Securities investment funds and stocks (no more than 40 percent)

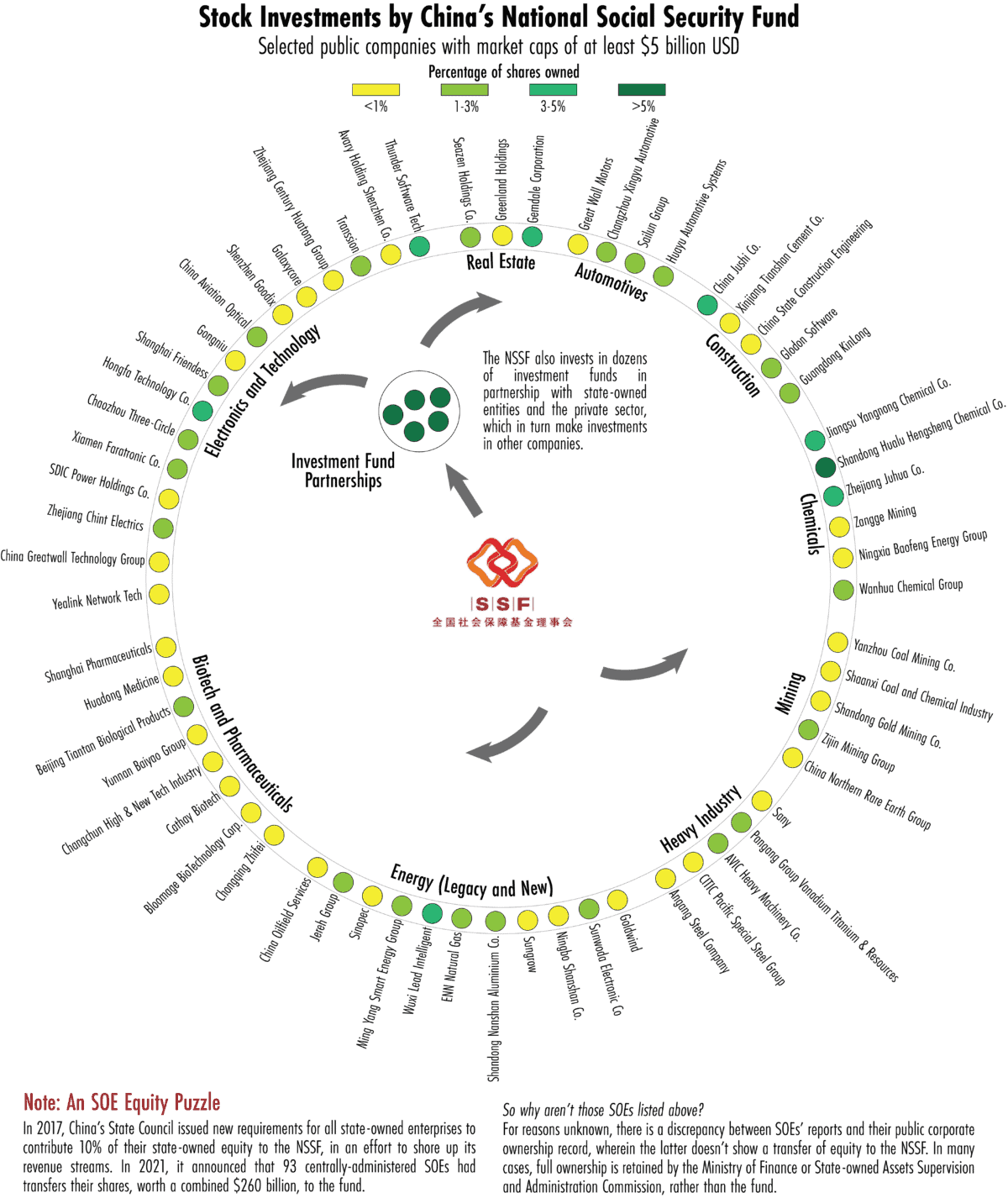

These are some of the NSSF’s major investments:

OUT OF POCKET

The need to address the widening deficit in China’s state pension system may have driven the decision to allow the NSSF to invest in funds and stocks, according to Nicholas Lardy, a senior fellow at the Peterson Institute for International Economics, a Washington D.C. think tank.

“I think the idea was that they were running short of funds, and if they continued to put their modest surplus just into government bonds, they were going to fall further and further behind, and be less able to meet the promised retirement benefits for Chinese workers,” says Lardy.

“So they decided to take a little more risk with the hope that they would get higher returns. Of course, that has not really been born out in the Chinese stock market in recent years.”

Following a crash in China’s stock market in 2015, the NSSF was part of the so-called “national team” of state-controlled financial institutions that bought billions of dollars’ worth of stocks in order to prop up share prices. At one point the national team, which also included China Securities Finance Corp. and investment company Central Huijin Investment, owned an estimated 6 percent of the mainland stock market.

But even steady growth in the NSSF’s assets over the last two decades has failed to alleviate pressure on the pension system from China’s graying population. A 2019 report by the Chinese Academy of Social Sciences predicted the country’s main pension fund would run dry by 2035.

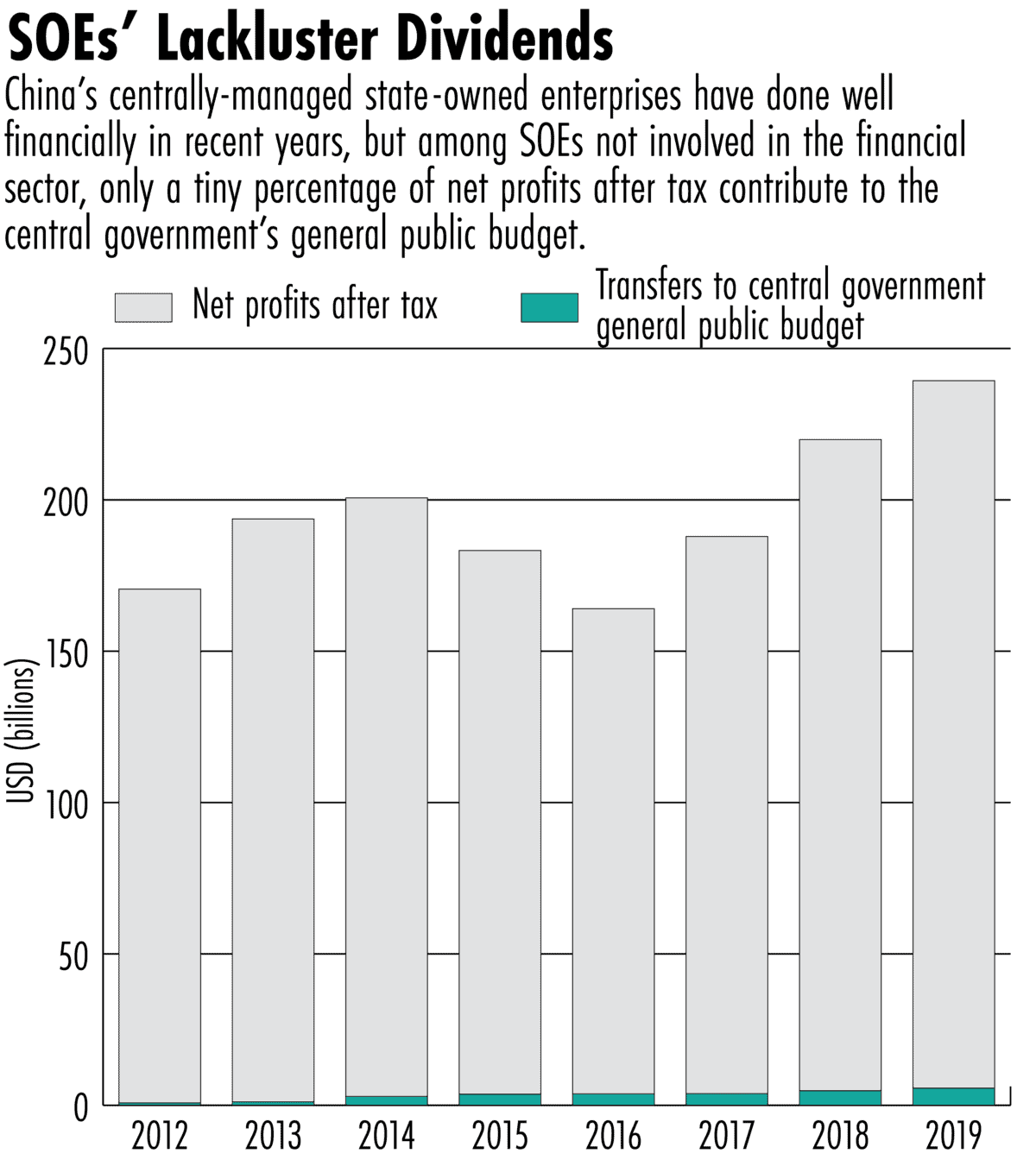

In an effort to shore up the NSSF’s finances, a new policy was announced in 2017 that required large and mid-sized state-owned enterprises to donate 10 percent of their state-owned equity to the fund, allowing it to earn income from state firms’ dividends. But progress has been slow, as government departments have proved reluctant to relinquish income from their stakes in SOEs, particularly at the local level. After years of wrangling, the Ministry of Finance announced last year that shares in 93 centrally administered SOEs worth around $260 billion had been transferred to the NSSF.

Even so, experts have warned that dividend payments from state-owned firms can be surprisingly small. “Overall, central firms turned in little dividends to the state in the past, well below what is asked for by the central government,” says Tianlei Huang, a research fellow also with the Peterson Institute, who conducted an analysis of SOE dividends in 2020. “If this continues, the NSSF might not be able to collect much from being a owner of so many gigantic central state firms, and the equity transfer program may turn out to be somewhat meaningless,” he says.

HARD CHOICES

Beyond juicing the NSSF’s reserves, more structural reforms will be needed to solve China’s pension deficit. Authorities are under pressure to raise the country’s retirement age, which remains one of the lowest in the world, at between 50 to 55 for women and 60 for men. But the idea is deeply unpopular, and Beijing has put off making the change for years. Part of the worry is that raising the retirement age risks further discouraging working-aged adults from having children, at a time when China’s birth rate has already plummeted.

Facing a population and pension crisis, Beijing has few good options, according to Lardy. “Eventually the authorities either have to cut back on the benefits, increase the contribution rate, or delay the age of retirement,” he says. “Those are the three policy instruments that they have. And so far, they’ve done nothing.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen