As countries make the switch to clean energy, governments are paying more attention to the resources they need for the transition. Some Western governments are concerned that the supply chains for many critical minerals have converged in one country: China.

China is a major consumer of such minerals, but stands apart in its role in processing raw materials, even those mined far beyond its borders. Thanks to years of planned industry consolidation, a small number of Chinese companies now have an outsized influence over the world’s supply.

This week, The Wire looks at China’s role in the production of the ‘neo-commodities’: the resources needed to produce the breadbasket goods of the future, and the key Chinese companies that stand to gain.

SOME DEFINITIONS

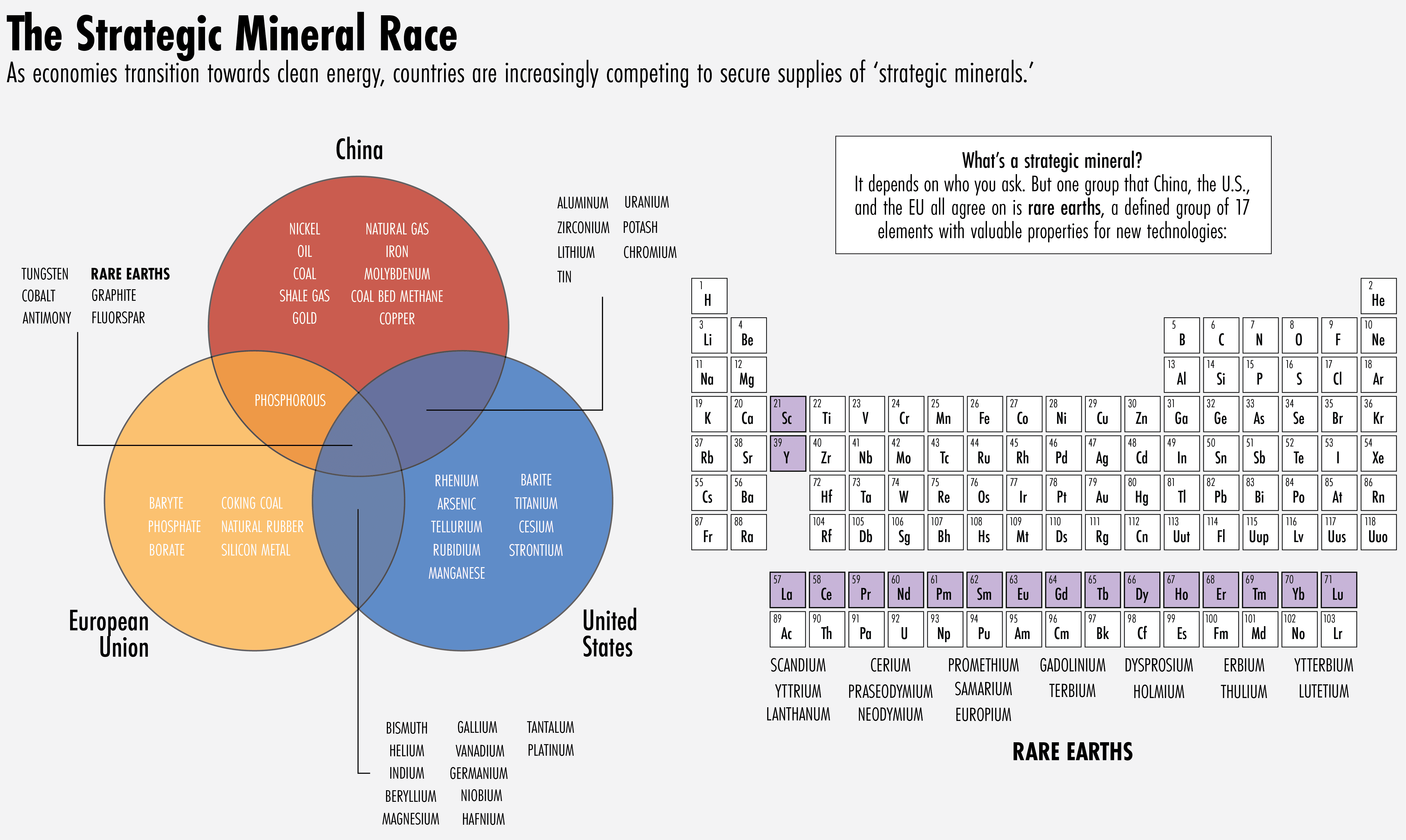

Most of the major powers have their own definition of strategic minerals — also known as critical minerals — reflecting their differing economic priorities. China, for example, has a list of 24 strategic minerals, while the U.S. Department of Commerce has a list of 35, and the EU’s contains 27. Overlap between the three is not strong, with consensus on just six minerals: tungsten, cobalt, antimony, fluorspar, graphite and rare earths.

Unlike strategic minerals, rare earths are a defined group of 17 elements. They are not, in fact, rare, but are seldom found in concentrations high enough to be mined on their own, and are instead collected as byproducts of other mining. Rare earths contain properties that make them essential to the new economy: they are magnetic and highly electrically conductive, playing crucial roles in components for electric cars, batteries, and smartphone touch screens.

HOW MUCH DOES CHINA CONTROL?

China has been enhancing control over its strategic minerals supply for years, to the alarm of some policymakers abroad. Last year, the U.S. Geological Survey identified 23 mineral commodities that pose the greatest supply risk for the U.S. manufacturing sector. China is the U.S.’s main supplier for eight of those vulnerable minerals. For five minerals, the U.S. is 100 percent reliant on overseas imports, including for minerals critical to certain defense systems such as gallium and germanium.

| At risk mineral | Net import reliance | Main suppliers | China’s share in global processing |

|---|---|---|---|

| Gallium | 100% | China, UK, Germany | 88% |

| Rare earths | 100% | China, Estonia, Japan, Malaysia | 62% |

| Indium | 100% | China, Canada, Republic of Korea | 56% |

| Tantalum | 100% | China, Germany, Australia, Indonesia | 41% |

| Bismuth | 94% | China, South Korea, Mexico, Belgium | 82% |

| Antimony | 81% | China, Belgium, Thailand, India | 90% |

| Tungsten | >50% | China, Bolivia, Germany, Austria | 82% |

| Germanium | >50% | China, Belgium, Germany, Russia | 67% |

| Niobium | 100% | Brazil, Canada, Germany, Russia | <5% |

| Platinum group metals | 79% | South Africa, Germany, Italy, Switzerland | NA |

| Cobalt | 76% | Norway, Canada, Japan, Finland | 50% |

| Titanium | >50% | Japan, Kazakhstan, Ukraine | 40% |

| Aluminum | 49% (alumina*) | Brazil, Australia, Jamaica, Canada | 40% |

Data: U.S. Geological Survey, Holslag (2021)

There are several reasons why China has become so dominant as a mineral processing hub.

Strong state support for industry consolidation and overseas expansion has created a number of powerful mining giants. This month, Chinese authorities approved the creation of a new state-owned rare-earth giant, China Rare Earth Group, formed from the merger of several state firms including Aluminum Corp of China, China Minmetals Corp, and Ganzhou Rare Earth Group, each already major rare earths producers in their own right. Larger companies enjoy economies of scale, such as higher bargaining power when negotiating contracts with mining companies overseas.

Beijing has invested heavily not just in its mining companies, but in geological surveys in neighboring countries, especially those it believes will cooperate on resource extraction.

Another reason for China’s dominance is that most rich economies just aren’t that interested in maintaining a domestic minerals processing industry, according to Jonathan Holslag, a professor at Free University Brussels and author of a recent paper on China’s mineral strategy. Processing is energy and transport-intensive, as well as heavily polluting. In China, by contrast, where the minerals industry has a turnover of $130 billion and employs 11 million people, authorities view its presence as critical.

“What China did was attract those traditional industries by offering laxer environmental policy in the 1990s, and then slowly moved them up to more advanced segments,” says Holslag. “What it’s doing now that it’s more demanding in terms of environmental standards, is not to rid itself of those basic industries, but to consider the transition to more efficient production as an important driver of innovation and productivity gains. Whereas in the West, it’s still ‘not in my backyard.’”

BIG MINERAL

These are some of China’s biggest companies involved in mineral extraction and processing in the lithium, cobalt, and rare earths sectors:

| Company | Market Cap | Description |

|---|---|---|

| Lithium | ||

| Zijin Mining | $39.43 billion | The gold and copper miner has been moving into lithium, recently paying over $700 million to acquire Canada’s Neo Lithium, which has major projects in Argentina. |

| Ganfeng Lithium | $32.3 billion | Holds lithium resources across Australia, Argentina, and Mexico. Recently engaged in a bidding war with Chinese battery giant CATL to acquire Canadian Millenial Lithium. |

| Tianqi Lithium | $25.75 billion | World’s largest hard-rock lithium producer, with assets in Australia, Chile, and inside China. |

| Cobalt | ||

| Huayou Cobalt | $22.84 billion | China’s biggest cobalt refiner, Huayou owns or has a stake in at least three cobalt mines in the DRC. But the company has come under fire for particularly poor working conditions at its DRC sites. |

| China Railway Group | $20.04 billion | The state-owned construction company partnered with another SOE, Sinohydro, to set up a joint venture at a DRC cobalt mine for around $3 billion. |

| China Molybdenum | $17.66 billion | The state-backed molybdenum and tungsten miner is the world’s second largest cobalt producer, having paid $2.65 billion in 2017 for a stake in the Tenke Fungurume mine in the DRC, one of the biggest cobalt mines in the world. |

| Rare Earths | ||

| China Northern Rare Earth Mining Corp | $30.51 billion | The largest rare earths manufacturer of the “Big Six” Chinese state-owned rare earth producers. Dominates in China’s northern provinces. |

| Aluminum Corporation of China Limited | $14.36 billion | Also known as Chinalco, it is the world’s second largest alumina producer in addition to a major rare earths producer. In December, the Chinese government announced Chinalco would be merged with China Minmetals to form a new rare earths giant. |

| China Minmetals | $7.15 billion | The state owned miner is the dominant rare earths producer in southern China. In December, the Chinese government announced Minmetals would be merged with Aluminum Corp of China to form a new rare earths giant. Its merger with Aluminum Corp of China would form China’s second-largest rare earths producer, behind only China Northern Rare Earth Mining Group. Also involved in cobalt mining in the DRC. |

For now, China’s control over the processing industry gives it significant leverage over the metals market, but one limit to China’s influence is that its domestic market absorbs very little of the minerals it processes. More than half of the lithium it produces is re-exported, for example. That creates an opportunity for foreign countries to wrest back control, according to Free University Brussels’ Holslag.

“If overseas markets organize their own production, they will effectively dilute China’s clout and sway the international market,” he says. “But alternative supply chains are developing, notably in Japan. I think very slowly, we’re going to have a diversification of international production.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen